Blood Pressure Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

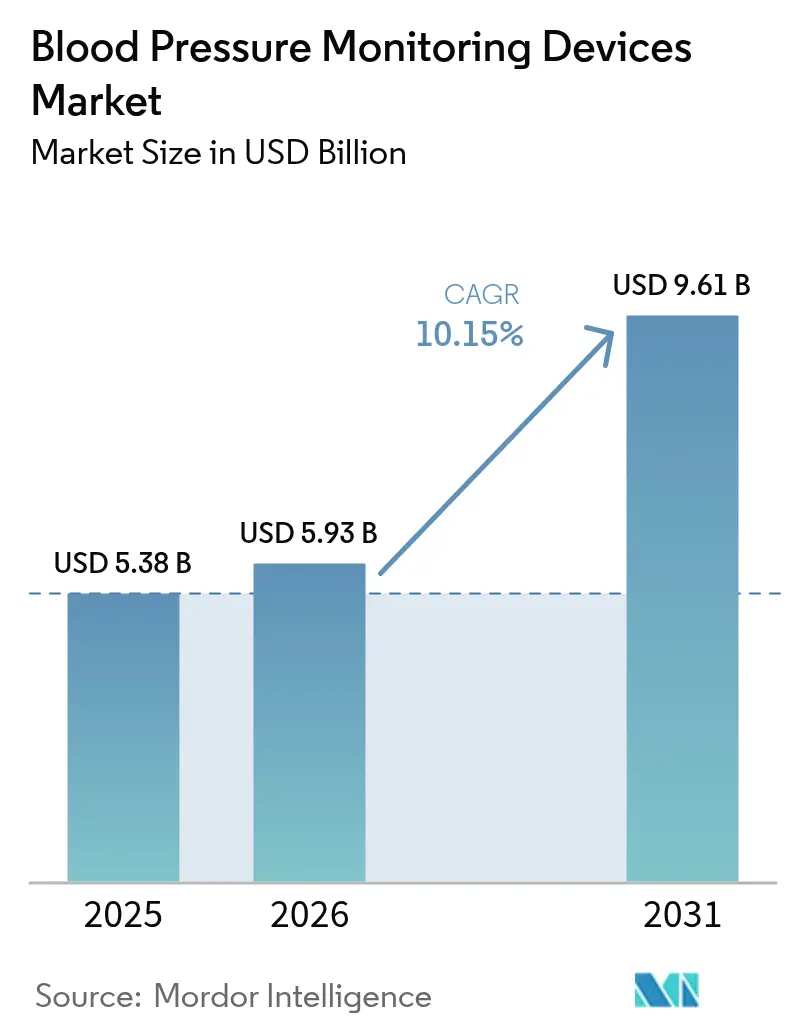

| Market Size (2026) | USD 5.93 Billion |

| Market Size (2031) | USD 9.61 Billion |

| Growth Rate (2026 - 2031) | 10.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Pressure Monitoring Devices Market Analysis by Mordor Intelligence

Blood Pressure Monitoring Devices market size in 2026 is estimated at USD 5.93 billion, growing from 2025 value of USD 5.38 billion with 2031 projections showing USD 9.61 billion, growing at 10.15% CAGR over 2026-2031.

Robust demand arises from the convergence of conventional cuffs with connected-care ecosystems, which shifts cardiovascular care from episodic checks to continuous oversight. Widespread preventive-care policies, payer reimbursement for remote patient monitoring, and stronger accuracy standards for cuffless wearables jointly sustain market expansion. At the same time, tariff-driven supply chain reviews and tighter approval rules reshape procurement strategies toward resilient and locally compliant suppliers. The blood pressure monitoring devices market therefore grows through parallel forces of technological progress and regulatory adaptation.

Key Report Takeaways

- By product type, upper-arm monitors led with 59.10% of the blood pressure monitoring devices market share in 2025, while cuffless wearables posted the fastest 12.07% CAGR to 2031.

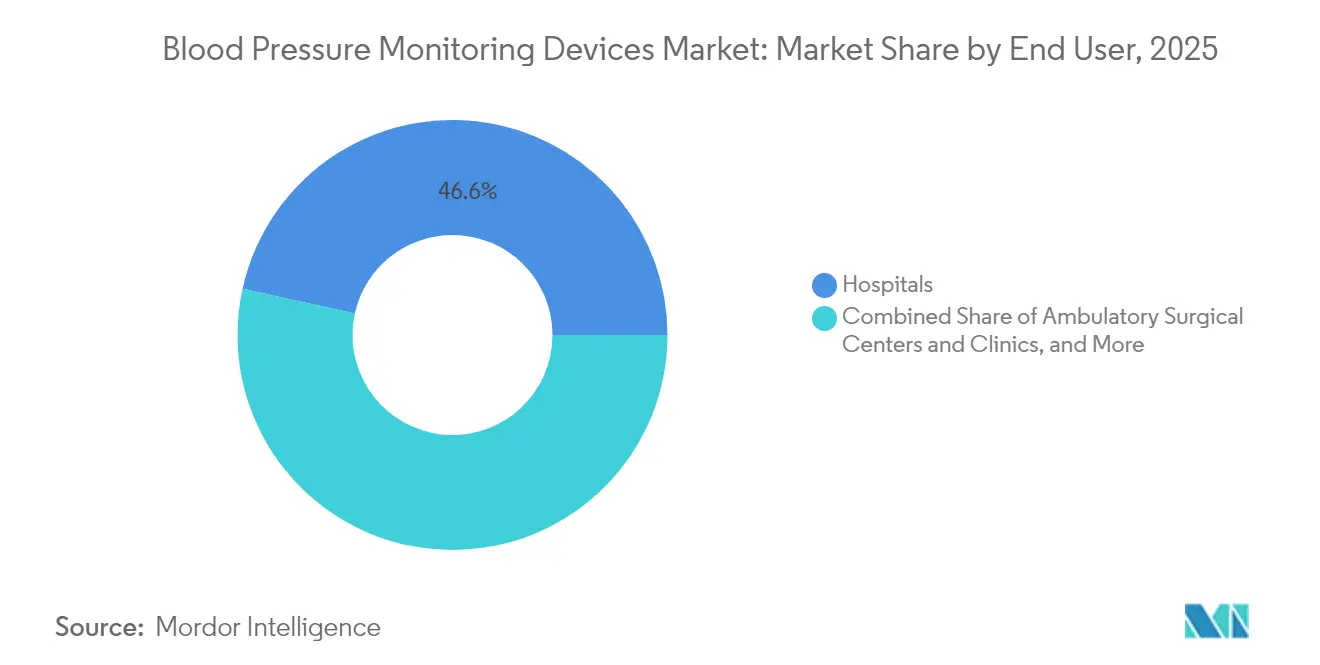

- By end user, hospitals held 46.55% of the blood pressure monitoring devices market share in 2025; meanwhile, home healthcare settings is projected to advance at a 11.05% CAGR from 2025 to 2031.

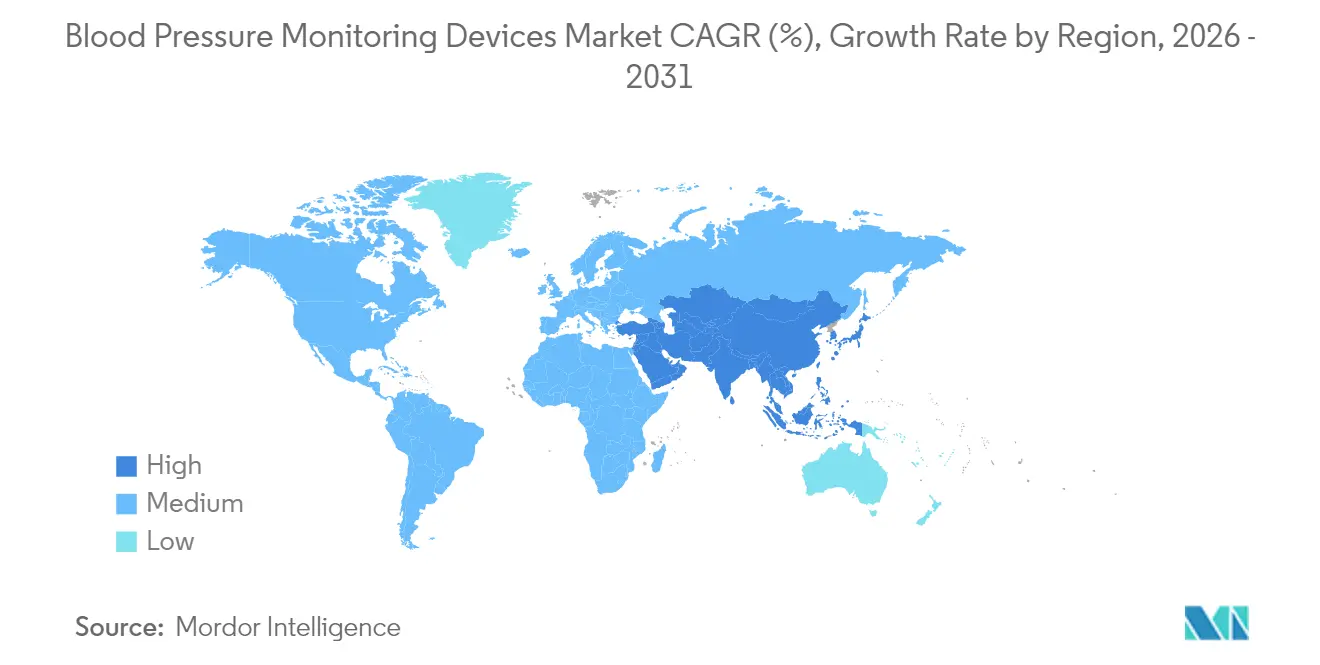

- By geography, North America dominated the market with a 35.20% revenue share in 2025, whereas the Asia-Pacific region is projected to expand at a 12.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Pressure Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Hypertension and Cardiovascular Diseases | +3.2% | Global, with highest impact in North America & Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements in Cuffless Monitoring | +2.8% | North America & EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Increasing Adoption of Remote Patient Monitoring | +2.1% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Growing Awareness of Home Healthcare Benefits | +1.7% | Global, with rural and aging population focus | Long term (≥ 4 years) |

| Aging Population Demographics | +1.4% | Global, with highest impact in developed economies | Long term (≥ 4 years) |

| Government Initiatives for Preventive Healthcare | +1.2% | APAC leading, North America & EU following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hypertension and Cardiovascular Diseases

Hypertension affects more than 1 billion people worldwide, and deaths attributable to elevated systolic pressure have continued to climb in absolute terms despite falling age-standardized rates. Screening programs inside large employers found that 17.6% of staff with no prior diagnosis register hypertensive readings, uncovering extensive silent disease pools. Health-system analyses show that early workplace detection boosted new hypertension diagnoses by 81% and raised antihypertensive prescriptions by 127%, confirming direct therapeutic value for continuous monitoring. These findings intensify procurement of scalable devices that work beyond clinics and drive the blood pressure monitoring devices market toward integrated solutions. They also reinforce payer interest in preventive benefits that offset future cardiovascular treatment costs.

Technological Advancements in Cuffless Monitoring

Cuffless blood pressure monitoring now sets the pace in product innovation. Nanowear’s SimpleSense-BP received FDA 510(k) clearance in 2024 as the first non-invasive continuous system, validating nanotechnology and AI analytics in routine hypertension care. Apple secured a patent for liquid-filled sensors that could bring medical-grade accuracy to future Apple Watch models, signaling Big-Tech entry into regulated cardiovascular wearables. Academic teams at Caltech introduced resonance sonomanometry, which uses sound waves plus ultrasound to generate full waveform readings without arterial lines. Each breakthrough raises expectations for real-time trend analysis, data portability, and patient comfort, fueling premium demand inside the blood pressure monitoring devices market.

Increasing Adoption of Remote Patient Monitoring

Medicare’s 2025 schedule pays providers USD 22.25 for RPM onboarding and USD 49.04 for monthly management when patients transmit at least sixteen readings every 30 days. Health systems, such as NYU Langone, have demonstrated returns of 22.2% on RPM-hypertension programs with 55% adherence, confirming financial sustainability.[1]Source: MedRxiv, “Cost and ROI of RPM-HTN at NYU,” medrxiv.org These reimbursement assurances encourage health networks to roll out remote panels that combine analytics dashboards with home units, driving recurring volume in the blood pressure monitoring devices market.

Growing Awareness of Home Healthcare Benefits

Consumer preference for home-based care persists beyond the pandemic era. Clinical validation studies across Asia found that 68.2% of patients kept morning systolic pressure within goals through home self-measurement compared with 55.5% under clinic checks. Withings launched the BPM Vision at USD150, featuring a color display and Wi-Fi sync, demonstrating how consumer-grade pricing can coexist with FDA-ready performance. National prevention guidelines from the CDC now recommend that employers integrate validated home monitors into their wellness programs. As confidence grows in at-home accuracy, procurement budgets tilt toward smart devices that extend monitoring beyond hospital walls, expanding the blood pressure monitoring devices market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Approval Complexities for Innovative Devices | -1.8% | Global, with highest impact in EU & FDA jurisdictions | Medium term (2-4 years) |

| High Costs of Advanced Monitoring Technologies | -1.3% | Emerging markets primarily, cost-sensitive segments | Short term (≤ 2 years) |

| Accuracy Concerns with Cuffless Devices | -1.1% | Global, clinical adoption barriers | Medium term (2-4 years) |

| Data Privacy and Security Concerns | -0.9% | EU & North America primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Approval Complexities for Innovative Devices

Validation protocols for cuffless devices remain in flux. The FDA recognized IEEE 1708-2014 but flagged certain observer-training clauses as incompatible with automated workflows, creating partial guidance only. Multicenter trials revealed that some optical wearables under-perform against ambulatory monitors, particularly after medication titrations, which slows payer adoption. Pediatric use requires separate 3-to-12-year trials, adding cost layers that deter smaller innovators. As a result, time-to-market elongates and compliance expenditure rises, applying a brake to the blood pressure monitoring devices market.

High Costs of Advanced Monitoring Technologies

Premium pricing for cuffless wearables poses barriers in cost-sensitive regions. Tariffs currently affect 70% of imported medical devices into the United States, forcing providers to lock in early contracts or pivot to domestic lines. Budget impact analyses show RPM programs break even only when compliance exceeds 55%, linking affordability to sustained utilization. Consequently, hospitals in lower-income geographies often favor mid-range digital cuffs rather than high-end optical devices, tempering upside in segments of the blood pressure monitoring devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Dominance Meets Cuffless Innovation

The upper-arm monitors category controlled 59.10% of the blood pressure monitoring devices market share in 2025, reflecting entrenched clinical confidence in oscillometric cuffs. Nevertheless, cuffless wearables are advancing at a 12.07% CAGR through 2031, translating into a fast-rising portion of the blood pressure monitoring devices market size for this segment. Hospitals and insurers are increasingly recognizing the importance of continuous waveform capture for managing nocturnal hypertension, which favors optoelectronic patches and smartwatches. Nanowear’s FDA-cleared SimpleSense-BP underscored this pivot by demonstrating real-world accuracy without inflation cycles, while Apple’s patent pipeline illustrates mainstream consumer potential.

Demand for ambulatory monitors also persists as clinicians prescribe 24-hour profiles to confirm white-coat or masked hypertension. SunTech Medical’s takeover of Meditech consolidated expertise that targets this niche, adding software that automates reporting into electronic records. Meanwhile, aneroid sphygmomanometers retreat as facilities modernize. Digital wrist cuffs benefit from comfort-driven upgrades though remain secondary in most guidelines. The overall competitive dynamic therefore hinges on balancing physicians’ insistence on validation with patients’ desire for unobtrusive wear, a balance that shapes long-run volume in the blood pressure monitoring devices market.

By End User: Hospital Leadership Yields to Home Healthcare Growth

Hospitals retained 46.55% of blood pressure monitoring devices market share in 2025 because acute settings still initiate diagnosis and titration protocols cms.gov. Yet home healthcare leads expansion at 11.05% CAGR to 2031, swelling the blood pressure monitoring devices market size for domiciliary channels. Medicare’s reimbursement of USD 49.04 monthly for RPM follow-up provides stable economics for health systems that ship pre-configured kits. NYU Langone’s RPM-HTN program realized a 22.2% investment return at USD 330 per patient and 55% adherence, highlighting profit potential in scaled home rollouts.

Ambulatory surgical centers and outpatient clinics upgrade to integrated vital-sign platforms that auto-document into electronic health records, cutting manual chart-time. Workplace and fitness centers represent emerging micro-channels as corporate wellness teams adopt validated devices to flag silent hypertension among employees. These decentralization trends redistribute procurement away from single-site bulk orders toward dispersed multi-stakeholder demand, enlarging the blood pressure monitoring devices market while diversifying service models inside the industry.

Geography Analysis

North America accounted for 35.20% of 2025 revenues, supported by advanced infrastructure and well-defined billing codes that facilitate remote monitoring. The region nonetheless examines supply resilience after tariffs disrupted 70% of inbound medical device volumes, prompting buyers to certify supplier origin and consider near-shoring options. Canada and Mexico boost regional momentum through e-health funding and cross-border regulatory alignment that shortens clearance timelines. These conditions sustain the blood pressure monitoring devices market, but they also promote investment in dual-sourced components.

The Asia-Pacific region delivers the swiftest growth at a 12.02% CAGR to 2031, reflecting demographic aging, hypertension prevalence, and an active policy that accelerates device approvals. China’s National Medical Products Administration cleared 61 innovative medical devices in 2023, representing an 11% year-over-year increase, under an accelerated pathway that prioritizes high-impact technologies. India projects its medical device sector to grow from USD 5.2 billion to USD 50 billion by 2030, driven by production-linked incentives and a single-window approval system. These reforms, together with local manufacturing grants, expand domestic supply and lower pricing, thereby broadening the regional market for blood pressure monitoring devices.

Europe benefits from entrenched universal healthcare that values validated accuracy. Adoption spreads as country panels harmonize cuffless performance requirements across notified bodies, giving innovators a predictable dossier route. Brazil, through ANVISA, now accepts FDA or TGA approvals to streamline entry, exemplifying regulatory convergence that also influences other Latin American markets. Additionally, the Pan American Health Organization’s HEARTS program mandates the exclusive use of validated monitors in primary care by 2025, fostering quality benchmarks across South America. Middle Eastern and African nations are allocating increasing capital to chronic disease management, installing telehealth hubs that integrate validated blood pressure monitoring modules. Across these varied geographies, policy alignment and disease burden continue to underpin the global expansion of the blood pressure monitoring devices market.

Competitive Landscape

The blood pressure monitoring devices market is moderately fragmented yet dynamic. Omron remains the leading brand, with more than 350 million units sold globally, and has recently received FDA De Novo clearance for its AI-enabled atrial fibrillation detection device, which exhibits 95% sensitivity and 98% specificity. The firm capitalizes on its NightView wrist monitor, which measures nocturnal blood pressure to meet emerging guideline demands. Philips and GE HealthCare integrate multi-parameter platforms that combine cuff modules with predictive analytics, embedding the blood pressure monitoring devices industry into hospital network upgrades.

Strategic deals accelerate capability bundling. BD acquired Edwards Lifesciences’ Critical Care portfolio for USD 4.2 billion, granting access to smart pressure sensors present in more than 10,000 hospitals.[3]Becton, Dickinson and Company, “Acquisition of Critical Care,” bd.com Additionally, SunTech Medical acquired Meditech to enhance its ambulatory specialism, while Spacelabs partnered with Masimo to integrate advanced optical metrics. Emerging challengers such as Nanowear and Aktiia focus solely on cuffless and calibration-free designs, targeting segments where convenience outweighs the benefits of traditional cuffs.

White-space opportunities exist in pediatric validation, enterprise wellness, and data-as-a-service layers that monetize continuous streams. Firms that secure broad-age validation and cybersecurity compliance stand to capture premium contracts. Overall, top players guard legacy volume but face steady share migration toward innovators, ensuring competitive tension that propels the blood pressure monitoring devices market.

Blood Pressure Monitoring Devices Industry Leaders

A&D Medical Inc.

American Diagnostics Corporation

Withings

GE Healthcare

Omron Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Withings introduced BPM Vision at USD 149.95 following FDA clearance, adding a color display and Wi-Fi sync.

- March 2025: Apple secured a patent for liquid-filled blood pressure sensors slated for future Apple Watch integration.

- January 2025: Omron received FDA De Novo authorization for AI-powered monitors with atrial fibrillation screening.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the blood pressure monitoring devices market as all professional-grade and consumer devices that determine arterial pressure through cuff-based or cuffless methods, together with the essential reusable and disposable accessories that enable a complete measurement cycle. Values are reported in USD at the manufacturer selling price and cover hospital, ambulatory, and home-care channels across 30+ countries.

Consumable sterile disposables used inside invasive catheters and stand-alone software dashboards not bundled with a measuring device are outside our scope.

Segmentation Overview

- By Product Type

- Upper Arm Monitors

- Wrist Monitors

- Ambulatory BP Monitors

- Cuffless Wearables

- Accessories (Cuffs & Others)

- By End User

- Hospitals

- Ambulatory Surgical Centers & Clinics

- Home Healthcare Settings

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with biomedical engineers, procurement managers, and cardiology clinicians across North America, Europe, and Asia validated adoption drivers, accessory consumption rates, and the typical device replacement cycle, filling data gaps that desk research left open.

Desk Research

Mordor analysts mapped hypertension prevalence, device trade flows, and average selling prices from tier-1 public sources such as WHO Global Health Observatory, UN Comtrade, the US FDA 510(k) database, and regional customs statistics. Supplementary detail on shipment volumes and company revenues was gathered from annual 10-K filings, investor decks, and peer-reviewed journals on remote patient monitoring. We then tapped paid archives, D&B Hoovers for financial splits and Dow Jones Factiva for multi-year news mentions to spot structural breaks in demand or pricing. The sources listed illustrate our process and are not exhaustive.

Market-Sizing & Forecasting

A top-down model starts with country-level hypertensive population pools, multiplies them by diagnosis and treatment penetration, and then by monitored-patient ratios to reconstruct annual device demand. Results are cross-checked through selective bottom-up roll-ups of leading supplier shipments and sampled ASP × unit calculations, thereby aligning totals. Key variables include: 1) hypertension prevalence shifts, 2) home-care share of treated patients, 3) average selling price by connectivity tier, 4) accessory-to-device ratio, and 5) remote patient monitoring enrollment growth. Forecasts use multivariate regression with ARIMA overlays, letting price elasticity and prevalence trends steer the base, while scenario analysis quantifies policy or reimbursement shocks.

Data Validation & Update Cycle

Outputs pass three-stage peer review, variance checks against trade tallies, and anomaly flags that trigger re-contacts with sources. Models refresh annually; material events prompt interim tweaks, and every delivery receives a last-minute sweep so users see the most current picture.

Why Our Blood Pressure Monitoring Devices Baseline Earns Trust

Published estimates often differ because publishers apply distinct device lists, price bases, and refresh speeds. Mordor's disciplined scope alignment, blended top-down and bottom-up reconciliation, and yearly recalibration minimize these disparities.

Key gap drivers stem from narrower product baskets, one-time currency conversions, or omission of self-monitoring accessories. Our cadence captures new FDA clearances and ASP slides early, anchoring a figure buyers can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.38 B (2025) | Mordor Intelligence | - |

| USD 4.10 B (2025) | Global Consultancy A | Excludes cuffless wearables and uses 2023 exchange rates |

| USD 2.15 B (2025) | Industry Tracker B | Counts only device revenues, omits accessories and home-care channels |

| USD 2.27 B (2025) | Regional Publisher C | Relies on hospital procurement data, lacks retail and e-commerce flows |

These comparisons show that when scope breadth, currency updates, and accessory inclusion are standardized, Mordor's number provides the balanced, transparent baseline decision-makers need.

Key Questions Answered in the Report

What is the current size of the blood pressure monitoring devices market?

The blood pressure monitoring devices market size is USD 5.93 billion in 2026 and is expected to reach USD 9.61 billion by 2031.

Which product segment is growing the fastest?

Cuffless wearable monitors are expanding at a 12.07% CAGR, the highest among all product types through 2031.

Why is home healthcare gaining traction for blood pressure monitoring?

Medicare reimbursement of USD 49.04 per month for remote monitoring and proven ROI of 22.2% in hospital programs make home settings economically attractive.

Which is the fastest growing region in global blood pressure monitoring devices market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What are the primary regulatory hurdles for cuffless devices?

Partial FDA recognition of IEEE 1708-2014, accuracy validation gaps, and separate pediatric studies extend approval timelines and raise costs.

Page last updated on: