Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

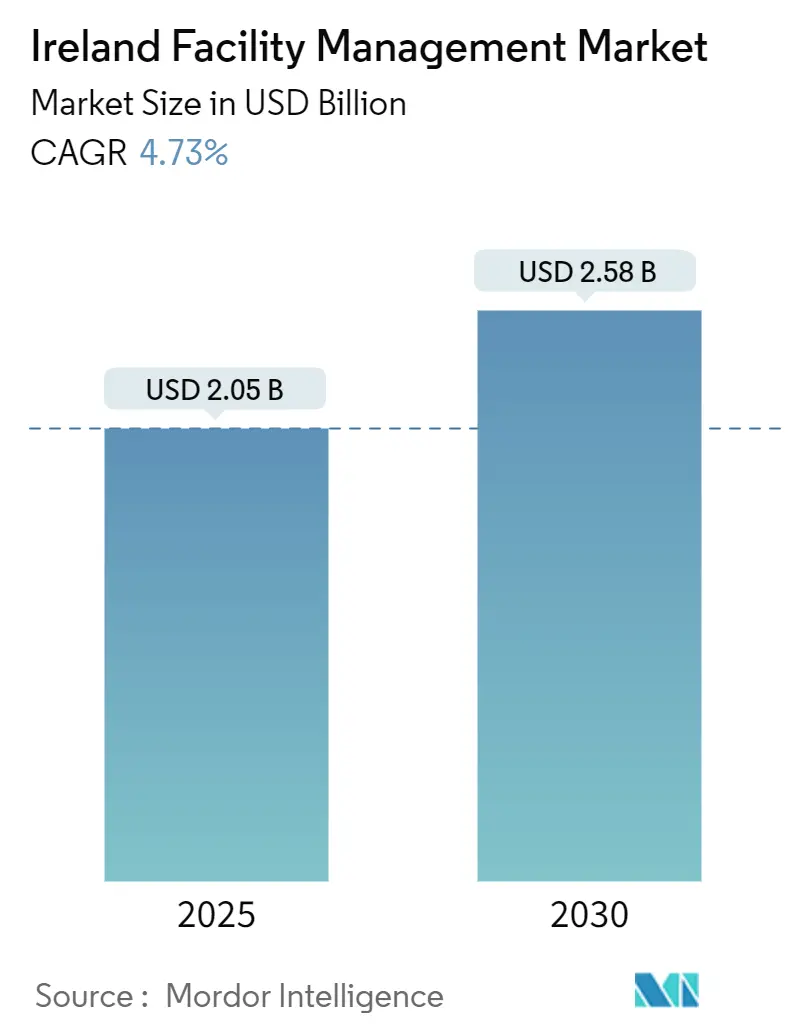

| Market Size (2025) | USD 2.05 Billion |

| Market Size (2030) | USD 2.58 Billion |

| Growth Rate (2025 - 2030) | 4.73% CAGR |

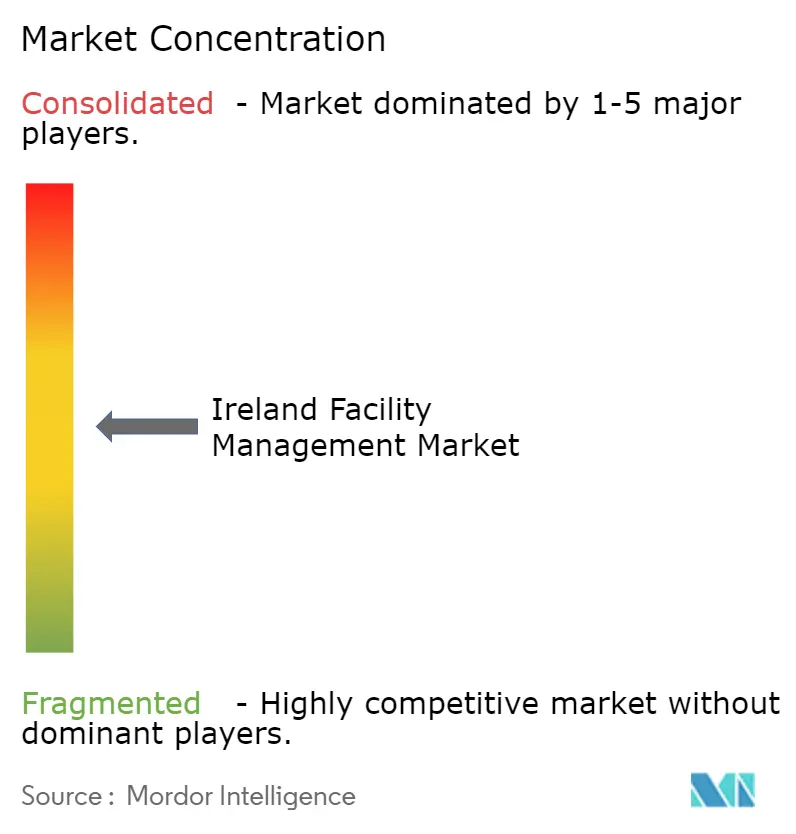

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ireland Facility Management Market Analysis by Mordor Intelligence

The Ireland facility management market size stands at USD 2.05 billion in 2025 and is projected to reach USD 2.58 billion by 2030, reflecting a 4.73% CAGR over the forecast period. Persistent vacancy pressures in Dublin’s prime districts and the recast Energy Performance of Buildings Directive are prompting companies to upgrade existing assets rather than expand footprints, thereby boosting demand for integrated hard-and-soft services that can cut energy use and ensure compliance[1]McCann FitzGerald LLP, “European mandating of building energy performance,” mccannfitzgerald.com. Labor shortages affecting 81% of Irish employers have accelerated outsourcing as clients rely on providers with deeper technical benches and training pipelines[2]Irish Times, “Ireland facing its worst talent shortage in decade,” irishtimes.com. Multinational occupiers, especially in technology and life sciences, now demand outcome-based contracts that guarantee emissions cuts and predictive upkeep, a shift enabled by IoT and AI platforms delivering energy savings of up to 61% in commercial combined heat-and-power units[3]F.S. Hafez et al., “Smart buildings with legacy equipment,” sciencedirect.com. Government retrofit grants administered by SEAI further bolster project pipelines in education and healthcare, where public-sector clients prioritize quantified carbon reductions and transparent reporting.[4]Sustainable Energy Authority of Ireland, “Insulation Grants,” seai.ie

Key Report Takeaways

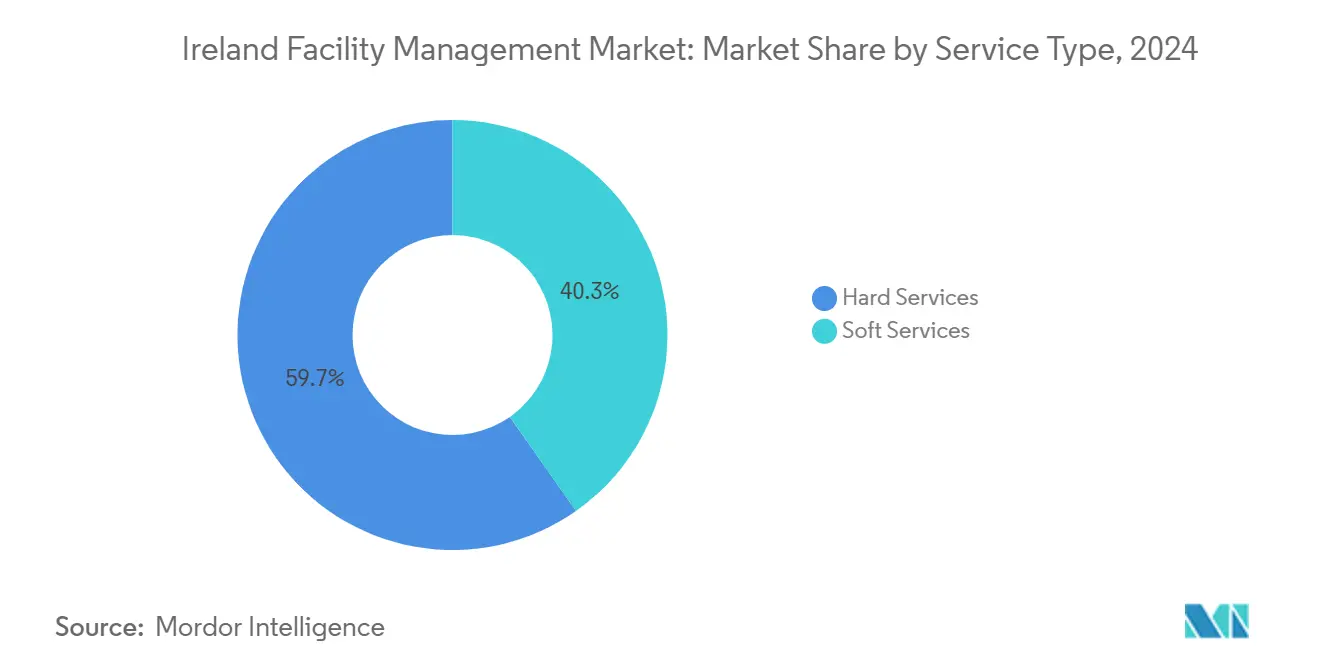

- By service type, hard services led with 59.73% of Ireland facility management market share in 2024; soft services are advancing at a 4.93% CAGR through 2030.

- By offering type, outsourced models accounted for 67.41% of the Ireland facility management market size in 2024 and are expanding at a 4.84% CAGR between 2025 and 2030.

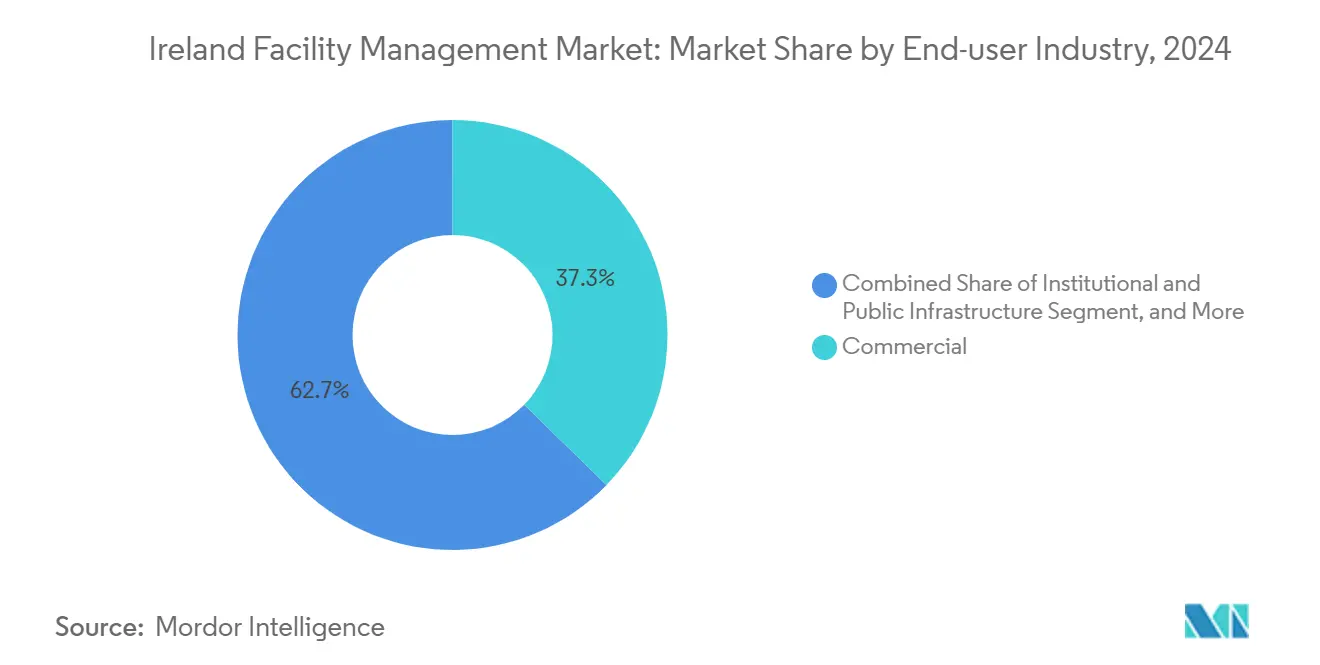

- By end-user industry, the commercial segment held 37.29% revenue share of the Ireland facility management market in 2024, while institutional and public infrastructure is poised for the fastest 5.01% CAGR to 2030.

Ireland Facility Management Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization & population growth | +1.2% | Dublin core; spillover to Cork & Galway | Medium term (2-4 years) |

| Labor & safety regulations | +0.8% | National; stricter in Dublin | Short term (≤ 2 years) |

| Technology-led integrated FM | +1.1% | Dublin & Cork tech hubs | Long term (≥ 4 years) |

| ESG-compliant FM solutions | +0.9% | National; early uptake in MNC sites | Medium term (2-4 years) |

| Hybrid workplace adoption | +0.7% | Dublin & key metros | Short term (≤ 2 years) |

| Government retrofit grants | +0.6% | National public assets | Medium term (2-4 years) |

Source: Mordor Intelligence

Urbanization and population growth in major metros

Dublin concentrates 25% of all commercial properties nationwide, yet its vacancy rate of 12% remains below the 14.5% national average, signalling stronger occupier demand even amid expansion delays. The clustering of global tech firms in the docklands elevates service complexity and pushes contract values 15–20% above regional equivalents. Growth corridors around Cork and Galway attract life-science and media tenants that require pharmaceutical-grade HVAC and broadcast-ready MEP maintenance. FM providers gain route-density efficiencies but must also juggle travel-time constraints in congested urban cores. As high-density mixed-use schemes proliferate, integrated models offering security, cleaning, energy optimisation and analytics from one dashboard become the norm. This metropolitan bias supports premium pricing, yet intensifies competition for licensed technicians willing to work night shifts and comply with strict safety audits.

Regulatory drivers specific to labor and safety standards

The Safety, Health and Welfare at Work Act 2005 continues to shape FM scopes, with recent Health and Safety Authority guidance intensifying oversight of contractor management and multi-tenant sites. New Corporate Sustainability Reporting Directive rules add ESG metrics to the compliance mix, forcing providers to capture waste volumes, scope-1 emissions and near-miss data within unified dashboards[5]Éamon Ó Cuív and David O'Keeffe, “Environmental, Social & Governance Law Ireland 2025,” iclg.com. Clients increasingly embed these metrics as key performance indicators, transferring penalties for non-compliance onto FM partners. As a result, service specs now include real-time incident logging, authorised-person training records and audited maintenance stamps. The dual safety-plus-sustainability burden inflates documentation workloads but also encourages adoption of sensor-based monitoring that cuts inspection labour. Providers capable of mapping statutory tasks to digital workflows gain a competitive edge and mitigate regulatory exposure for occupiers.

Technology-led integrated FM (IoT, BMS, AI-based predictive maintenance)

Irish pilot projects show IoT retrofits delivering 61% energy savings in combined heat-and-power units and 39% reductions in domestic hot-water loads, underscoring the payback potential of data-driven maintenance. The PHOENIX platform applies machine-learning algorithms to legacy plant, shifting loads to off-peak tariffs and forecasting component failures weeks ahead. Dublin’s tech-savvy occupiers now request asset-health dashboards alongside cleaning scorecards, pushing FM firms toward in-house analytics teams and API-integrated CAFM systems. Under outcome-based contracts, providers guarantee uptime and energy-intensity targets rather than prescriptive task lists, aligning incentives with landlord ESG goals. Capital-expenditure hurdles remain for smaller vendors, yet partnership models with sensor makers and energy-service companies lower entry barriers. Over time, predictive analytics will re-set price baselines as reactive call-outs decline and planned interventions dominate workloads.

ESG-compliant FM solutions demand

Mandatory ESG disclosure under CSRD applies from 2024, compelling large Irish corporates to publish building-level energy, waste and carbon data. Parallel EPBD targets mandate net-zero new builds by 2030 and staged retrofits for 16% of existing commercial stock by the same year. FM providers respond by bundling traditional hard services with carbon accounting, renewable procurement and green-lease advisory. Nearly Zero Energy Building standards already require 60% performance improvement over 2008 baselines for non-domestic assets, placing HVAC optimisation and envelope upgrades high on maintenance agendas. Institutional landlords track certification scores such as LEED and BREEAM, prompting FM partners to coordinate audits and verify meter data integrity. Early movers capable of translating sensor outputs into investor-grade ESG reports secure longer tenures and premium rates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce participation | -0.9% | National; acute in Dublin & Cork | Short term (≤ 2 years) |

| Competitive rivalry intensity | -0.6% | Dublin core; moderate elsewhere | Medium term (2-4 years) |

| Skilled-labour shortage & wage inflation | -0.8% | National; premium in metros | Short term (≤ 2 years) |

| Fragmented legacy building stock | -0.5% | Dublin & Cork CBDs | Long term (≥ 4 years) |

Source: Mordor Intelligence

Workforce indicators – labor participation

A quarter of Irish employers struggle to fill roles, with structural deficits most acute in skilled trades crucial to FM, such as electricians and HVAC technicians. Construction workforce numbers hover around 177,800, yet ESRI estimates 50,000 additional workers are needed to meet housing and infrastructure goals. Emigration during the previous downturn and declining STEM enrolment compound shortages, pushing agencies to import talent under critical-skills permits. FM contractors face schedule slippage when subcontractor pools are thin, forcing premium overtime pay and longer mobilisations. Apprenticeship backlog funding helps, but practical training takes years, dampening near-term labour supply.

Fragmented legacy building stock increasing integration complexity

Ireland’s commercial estate contains disparate vintages and control systems, complicating IoT retrofits and predictive models. Older properties lack as-built drawings, forcing FM teams to invest in surveys before implementing BMS upgrades. Integration costs deter some landlords from full-stack solutions, restricting providers to piecemeal deployments that dilute energy-saving potential. Long-term, digital twin adoption and modular sensor kits may cut retrofit hassle, but near-term complexity slows project roll-outs and tempers market growth.

Segment Analysis

By Service Type: Hard services underpin compliance as soft services outpace on growth

The hard-services segment generated 59.73% of 2024 revenue for the Ireland facility management market, anchored by mandatory maintenance of mechanical, electrical and life-safety systems under the Safety, Health and Welfare at Work Act 2005. Within that basket, MEP and HVAC tasks dominate given NZEB rules that demand 60% performance improvement, pushing landlords to invest in high-efficiency chillers, pumps and controls. Asset-management sub-services increasingly rely on IoT sensors that predict part failures, delivering the headline 61% CHP-energy-saving example cited in Irish pilots. The Ireland facility management market size tied to hard services is forecast to expand steadily, aided by continuous safety reforms and deeper ESG audits.

Soft services, while representing the smaller share, are projected to record a 4.93% CAGR to 2030, the fastest within the portfolio. Hybrid workplaces elevate requirements for dynamic cleaning, agile security rosters and event-oriented catering that adjust to fluctuating daily headcounts. As a result, the Ireland facility management market increasingly values concierge-style support that boosts tenant satisfaction scores. Technology overlays, such as app-based helpdesks and real-time feedback kiosks, couple with data-driven staffing models, further differentiating providers and raising barriers to entry.

By Offering Type: Outsourcing cements majority as integration drives premiums

Outsourced contracts contributed 67.41% of the Ireland facility management market in 2024 thanks to clients offloading compliance risk and talent acquisition challenges. The Ireland facility management market size for outsourced work is forecast to climb at 4.84% CAGR as CSRD reporting pushes firms toward vendors fluent in ESG metrics. Integrated-FM bundles show the quickest uptake: Sodexo’s EUR 250 million higher-education PPP exemplifies multi-year, multi-service wins that centralise cleaning, grounds, HVAC and helpdesk under one SLA.

In-house delivery remains important for organisations guarding strategic control, yet its 32.59% share is expected to erode gradually. Digital retrofits and AI-enabled predictive tools exceed the investment appetite of most occupiers, reinforcing outsourcing’s value proposition. Hybrid arrangements emerge where landlords retain energy-strategy oversight but outsource on-site execution to tech-enabled specialists, reflecting a co-sourced evolution rather than a binary choice.

By End-user Industry: Institutional momentum outruns commercial dominance

Commercial offices retained 37.29% revenue share of the Ireland facility management market in 2024, buoyed by multinational tenants clustering in Dublin Docklands. The Ireland facility management market share within this segment remains stable as a “flight to quality” sees occupiers trade up to energy-efficient Grade-A assets even while optimising desk counts. Tech and telecom clients pioneer AI-based maintenance and air-quality monitoring, setting new service benchmarks.

Institutional and public infrastructure emerges as the quickest-growing customer base with a forecast 5.01% CAGR, powered by SEAI grants funding deep retrofits in education and healthcare. Hospitals require stringent infection-control protocols with round-the-clock engineering cover, driving higher-margin contracts. Transport nodes and government campuses increasingly sign outcome-based energy-performance deals, guaranteeing carbon-emission thresholds and uptime standards for critical plant. With policy support locked in until 2030, this vertical will steadily capture a larger slice of Ireland facility management market size.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Dublin and its commuter belt dominate spend, representing about a quarter of national commercial floor area and attracting the lion’s share of multinational leases. Vacancy stood at 12% in Q4 2024 against a 14.5% national reading, enabling premium FM pricing that runs 15-20% above provincial averages . Tech-centric occupiers cluster in Docklands and Sandyford, demanding integrated packages covering energy dashboards, smart security and hospitality-grade soft services. Skilled-labour scarcity is acutest here, inflating wage bills yet also encouraging automation investment.

Cork and the wider Munster region form the second pillar of demand, fuelled by pharmaceutical and life-science manufacturing plus port-linked logistics. Facilities require GMP-compliant cleaning, validated HVAC and specialist electrical maintenance, all of which carry premium rates. The city’s growing fintech presence further diversifies requirements, prompting FM firms to establish satellite control centres to balance travel times and response SLA obligations.

Galway, Limerick and the western seaboard show rising need for biotechnology, medical-device and higher-education FM support. Regional vacancy peaks above 18% in parts of Galway and 20% in Sligo and Donegal provide openings for providers offering space-repurposing and energy-retrofit programmes. Meanwhile, the M1 corridor between Dublin and Belfast develops as a co-working cluster, with flexible-space operators outsourcing concierge-style FM to vendors adept at experience-centric metrics. Government retrofit grants apply nationally, so even dispersed local-authority offices in rural counties become attractive for energy-performance contracting as bandwidth opens among major players.

Competitive Landscape

Ireland facility management market competition remains moderate but consolidating as regulatory complexity and technology capex raise entry thresholds. International incumbents like Sodexo, Mitie and Kier leverage global purchasing power and proprietary digital platforms to secure multi-service PPP contracts worth hundreds of millions of euro. Domestic challenger Sensori, launched by John Sisk & Son, differentiates through data-analytics overlays that convert building telemetry into actionable asset-life plans.

Talent scarcity amplifies the advantage of firms with structured apprenticeships and branded graduate routes. Larger providers offset wage inflation via productivity-boosting mobile apps and AI-driven dispatch algorithms, while smaller outfits struggle to fund similar upgrades. CSRD and EPBD requirements compel investment in meter-data verification, carbon accounting software and third-party assurance, further widening the capability gap.

Strategic moves include Sodexo’s 2024 EUR 250 million higher-education PPP win, Mitie’s HMRC five-year FM contract extending United Kingdom public-sector credentials into Ireland, and an early-2025 acquisition that added 1,100 employees to a global player’s local footprint. Kier Group’s 17% revenue growth in 2024, buoyed by infrastructure, signals cross-selling potential into FM lifecycle services. Emerging niche players focus on AI-enabled predictive offerings, but integration hurdles with heterogeneous legacy systems tilt scale and client trust toward established brands.

Ireland Facility Management Industry Leaders

-

CBRE Group Inc

-

Sodexo Group

-

Kier Group PLC

-

Sensori Facilities Management

-

Cushman & Wakefield PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: A global facilities-management group acquired an Irish operator, adding more than 1,100 employees to its portfolio.

- November 2024: Mitie won a five-year HMRC facilities-management contract, signalling expansion of UK providers into Irish public-sector work.

- September 2024: Kier Group plc reported 17% revenue growth to GBP 3.97 billion, with a GBP 10.8 billion order book supporting future FM-service cross-sell opportunities.

- May 2024: Sodexo secured a EUR 250 million contract covering facilities management and technical services across Dublin, Cork, Kerry and Westmeath as part of a higher-education PPP project.

Ireland Facility Management Market Report Scope

By integrating people, place, process, and technology, facility management confines multiple disciplines to ensure any building's functionality, comfort, safety, and efficiency. At the same time, complex services include physical and structural services like fire alarm systems, lifts, etc. Soft services include cleaning, landscaping, security, and similar human-sourced services, providing solutions to end-user industries. The Ireland facility management market is defined based on the revenues generated from the services used in various end-user applications nationwide.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from the various types used in various end-user industries across Ireland. In addition, the study provides the Ireland facility management market trends, along with key vendor profiles. The study further analyses the overall impact of COVID-19 on the ecosystem.

The Ireland facility management market is segmented by type (inhouse facility management and outsourced facility management [single FM, bundled FM, and integrated FM]), by offering type (hard FM and soft FM), and by end-user (commercial, institutional, public/ infrastructure, industrial, and other end-users). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Service Type | Hard Services | Asset Management | |

| MEP and HVAC Services | |||

| Fire Systems and Safety | |||

| Other Hard FM Services | |||

| Soft Services | Office Support and Security | ||

| Cleaning Services | |||

| Catering Services | |||

| Other Soft FM Services | |||

| By Offering Type | In-house | ||

| Outsourced | Single FM | ||

| Bundled FM | |||

| Integrated FM | |||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | ||

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | |||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | |||

| Healthcare (Public and Private Facilities) | |||

| Industrial and Process (Manufacturing, Energy, Mining) | |||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | |||

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current market value of the Ireland facility management market?

The market is valued at USD 2.05 billion in 2025 with a projected rise to USD 2.58 billion by 2030.

Which service type holds the largest share?

Hard services dominate with 59.73% share, driven by mandatory maintenance of mechanical and life-safety systems.

Why is outsourcing prevalent among Irish occupiers?

Acute labour shortages and complex ESG reporting push organisations to rely on specialised providers that can supply skilled staff and compliance technology.

Which end-user segment is growing the fastest?

Institutional and public-infrastructure clients, supported by SEAI retrofit grants, are forecast to grow at 5.01% CAGR through 2030.

How are technology trends reshaping FM contracts?

IoT sensors, AI-based predictive maintenance and outcome-based KPIs allow providers to guarantee uptime and energy-intensity targets instead of delivering prescriptive task lists.

What regulatory changes most influence FM demand?

Implementation of CSRD and the recast EPBD require detailed ESG disclosures and net-zero upgrades, stimulating demand for integrated sustainability-focused FM solutions.

Page last updated on: February 26, 2025