Iraq Architectural Coatings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 124.91 Million |

| Market Size (2030) | USD 158.12 Million |

| Growth Rate (2025 - 2030) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq Architectural Coatings Market Analysis by Mordor Intelligence

The Iraq Architectural Coatings Market size is estimated at USD 124.91 million in 2025, and is expected to reach USD 158.12 million by 2030, at a CAGR of 4.83% during the forecast period (2025-2030). Rapid reconstruction activity, the USD 250 billion public‐investment pipeline, and a rising preference for low-VOC paint systems underpin steady demand expansion. Large-scale housing programs, foreign-financed commercial megaprojects, and climate-driven product specifications are reshaping procurement patterns, while local manufacturing scale-ups are starting to reduce their reliance on imported finishes. Competitive intensity remains moderate because project-based buying fragments market power across governorates; however, firms offering climate-adapted, waterborne solutions gain a clear edge. The Iraq architectural coatings market is also benefiting from regulatory incentives that favor cool-roof and insulating products, a trend likely to accelerate as energy-efficiency codes tighten nationwide.

Key Report Takeaways

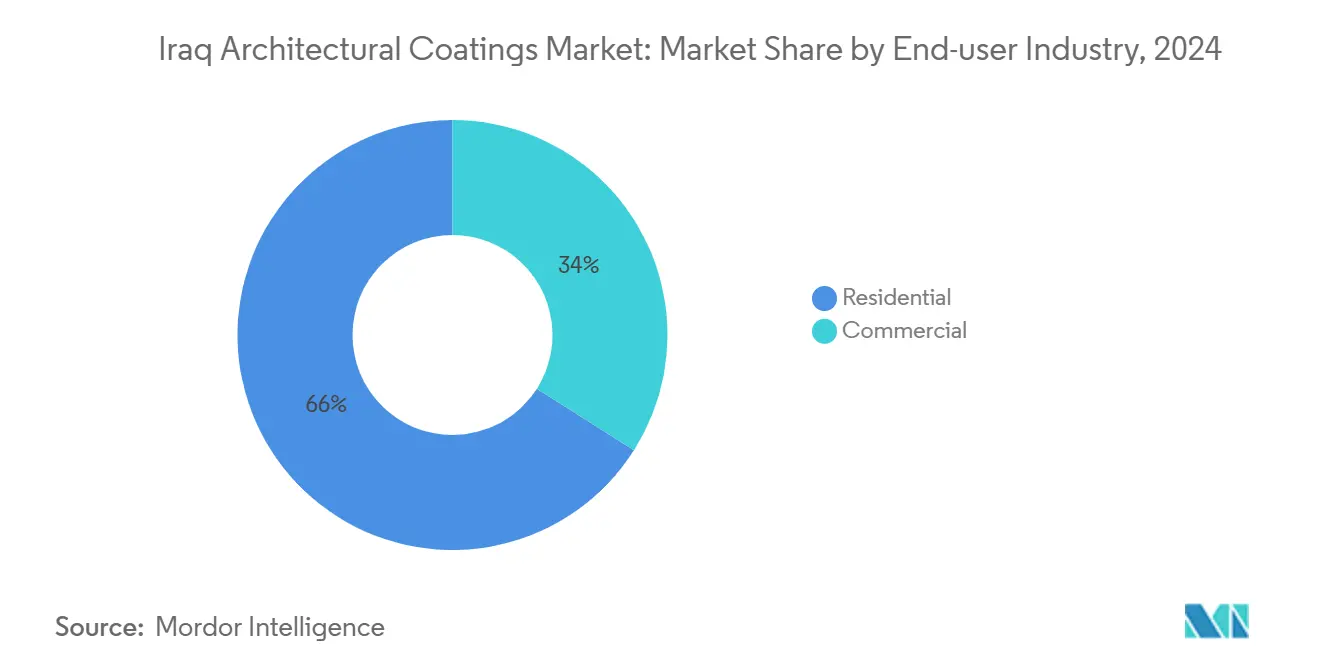

- By end-user industry, residential construction accounted for 65.99% of the Iraq Architectural Coatings market share in 2024; this segment is projected to expand at a 5.32% CAGR through 2030.

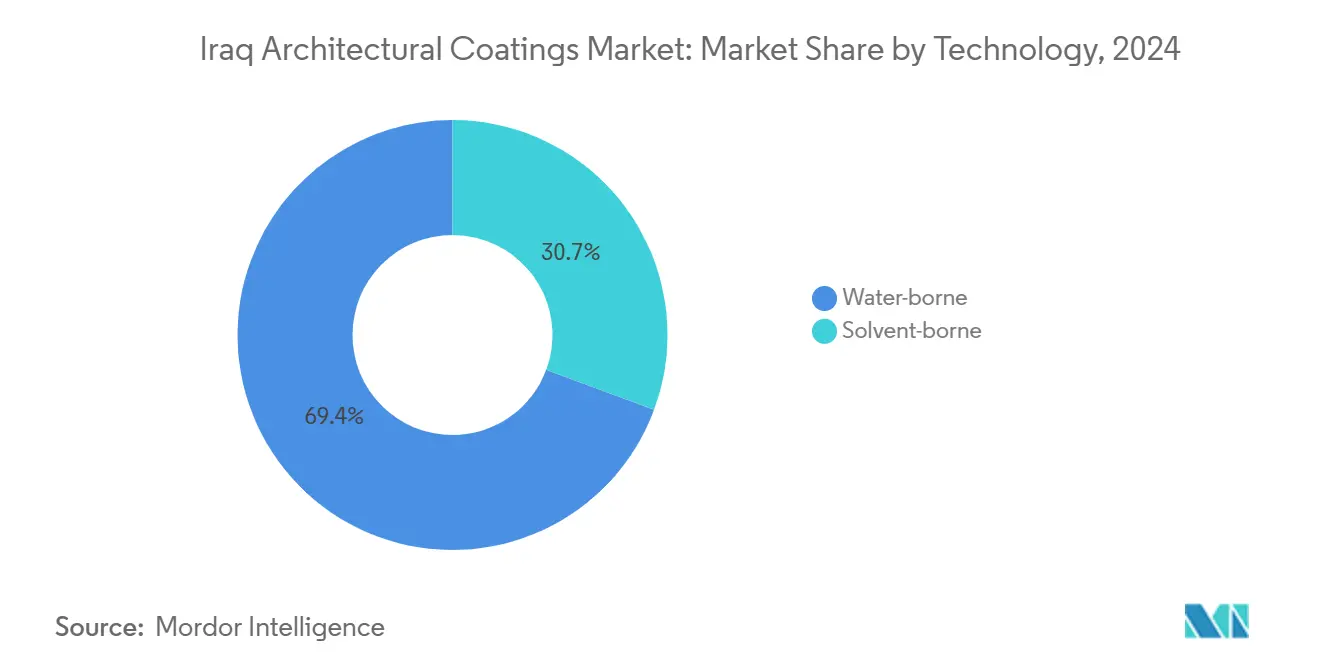

- By technology, water-borne coatings dominated the market with a 69.35% revenue share in 2024, and are expected to post a 5.62% CAGR through 2030.

- By resin type, acrylic formulations accounted for 39.60% of the Iraq Architectural Coatings market size in 2024 and are forecast to grow at a 5.60% CAGR over 2025-2030.

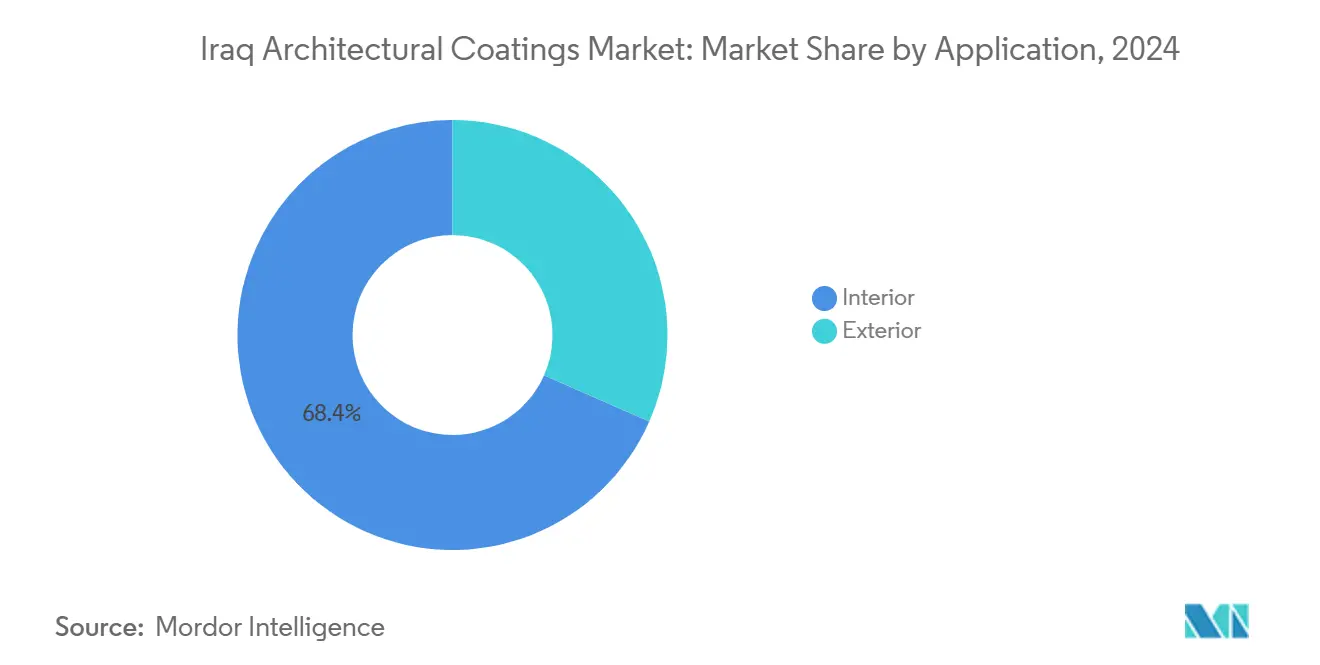

- By application, interior finishes captured 68.40% share of the Iraq Architectural Coatings market size in 2024, whereas exterior coatings are expected to grow at a 5.87% CAGR to 2030.

Iraq Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-war reconstruction and infrastructure boom | +1.8% | Baghdad–Basra–Mosul corridors | Medium term (2-4 years) |

| Housing-finance-fuelled residential demand | +1.5% | Nationwide, focus on Baghdad & Kurdistan | Long term (≥4 years) |

| Foreign-funded commercial megaprojects pipeline | +1.2% | Development Road & Grand Faw corridors | Medium term (2-4 years) |

| Government subsidy on energy-efficient coatings | +0.8% | National pilot programs | Long term (≥4 years) |

| Modular-construction factories preferring factory-applied paints | +0.5% | Industrial zones in Baghdad, Erbil, Duhok | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Post-war reconstruction and infrastructure boom accelerates market expansion

Government allocations of USD 250 billion for infrastructure over 2024-2026 continue to drive demand for coatings across rail, highway, and port assets. The USD 17 billion Development Road—1,200 km of combined rail and highway—needs large volumes of traffic marking and corrosion-resistant systems. The restarted public works, worth USD 18 billion, highlight the official resolve to complete stalled projects, unlocking backorders for primers, sealers, and topcoats. Marine coatings prospects are buoyed by the Grand Faw Port build-out, where 99 berths enter phased delivery from 2025. Suppliers with certified protective systems suited to hot-dry and hot-humid climatic zones are likely to gain recurring business as the Iraq Architectural Coatings market consolidates around megaproject specifications.

Housing-finance-fuelled residential demand drives volume growth

A 3.5 million-unit national housing deficit underpins strong volumes in interior and exterior decorative paints. The National Investment Commission’s program for 1 million standardized units across 15 governorates provides coatings producers with predictable, high-volume call-offs[1]National Investment Commission, “One Million Housing Units Initiative,” investpromo.gov.iq. Massive schemes, such as Al-Rashid New City and the 70,000 dwellings in Sadr City, add further pull for mid-tier acrylic emulsions. Climate-adaptive, low-VOC lineups appeal to the EU-supported BEIT initiative, which specifies reflective roof coatings and elastomeric wall finishes for affordability and energy savings. As mortgages for middle-income buyers expand, interior repaint cycles shorten, sustaining growth momentum for the Iraq architectural coatings market.

Foreign-funded commercial megaprojects pipeline expands market scope

Chinese-backed industrial parks and IFC-financed cement expansions inject specialized demand for solvent-resistant, heavy-duty coatings. The USD 2 billion industrial city, anchored by San Jian, requires high-performance epoxy and polyurethane systems for its chemical, steel, and logistics facilities. IFC’s USD 130 million loan to Al-Douh Cement adds 1 million tpa capacity, indirectly boosting coatings uptake via downstream ready-mix and precast plants. Sustainability clauses in new economic-city charters elevate the share of water-borne and low-VOC products, broadening the Iraq architectural coatings market beyond residential repaint cycles.

Government subsidy on energy-efficient coatings promotes technology adoption

The National Strategy for Environmental Protection and Improvement (2024-2030) opens fiscal incentives for reflective and insulating paints. Pilot programs in Baghdad reimburse part of the incremental cost of cool-roof coatings that reduce rooftop temperatures by 4.5°C and curb cooling loads by nearly 29%. UNDP-funded code-development projects introduce compliance levers, accelerating the adoption of water-borne and solar-reflective technologies. Domestic distributors report a 12% uptick in cool-roof SKU sales during 2025’s peak summer months, signaling traction for the Iraq architectural coatings market as energy tariffs climb.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political/security instability and project stoppages | −1.2% | Disputed territories | Short term (≤2 years) |

| Import-dependent raw-material cost volatility | −0.8% | Nationwide | Medium term (2-4 years) |

| Shortage of trained applicators causing coating failures | −0.5% | Rural governorates | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Political/security instability and project stoppages constrain market growth

Intermittent unrest disrupts site access and investor confidence, leading to schedule overruns and idle inventories. Although 490 stalled projects restarted in 2024, historical backlogs of 1,400 schemes worth USD 18 billion continue to underscore operational risk. Security premiums increase the total installed cost of coatings in high-risk zones, prompting contractors to favor shorter warranty periods and lower-specification finishes. Uneven market activity means the Iraq architectural coatings market advances more quickly in Kurdistan and south-central corridors than in contested northern districts.

Import-dependent raw-material cost volatility pressures profit margins

Pigments, resins, and specialty additives sourced from Asia and Europe still dominate local formulations. Freight spikes and currency swings widen landed-cost variability, compressing margins for both importers and nascent domestic producers. HS 320649 customs data confirm persistent reliance on imported pigment dispersions, even as new plants like Kalekim’s Duhok unit ramp up. With roughly 60% of Development Road materials expected to be imported, coatings feedstocks remain vulnerable to global price shocks, posing a challenge to cost planning for the Iraqi architectural coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Residential dominance reflects housing priorities

Residential construction contributed 65.99% of 2024 revenue, leveraging large-scale city projects and standardized unit specifications. The Iraq architectural coatings market size for residential applications is set to rise at a 5.32% CAGR as mortgage access and public housing budgets expand. Sustained interior repaint cycles of three to four years maintain baseline demand, while climate-resilient exterior systems provide incremental volume. Commercial and industrial users follow, propelled by foreign capital and diversification efforts, yet they still make up a smaller slice by value. Industrial city ventures along the Development Road incorporate stringent environmental clauses, creating a future pull for specialty, low-VOC, and high-durability coatings.

Project-based procurement provides larger paint companies with an opportunity to bundle primers, topcoats, and sealants, thereby capturing market share through turnkey supply contracts. Smaller local firms cater to the price-sensitive do-it-yourself channel, particularly in peri-urban governorates where self-build activity remains high. As Iraq’s public–private partnership law matures, developers increasingly incorporate performance-based painting schedules that reward longer-life systems, favoring multinational brands with proven warranty records. That shift positions residential spend growth as the bellwether for overall momentum in the Iraq architectural coatings market.

By Technology: Water-borne solutions lead market transformation

Water-borne coatings commanded 69.35% of the revenue in 2024 and are projected to expand at a 5.62% CAGR, driven by tightening environmental regulations and increased awareness of indoor air quality. Products bearing EN 13300 scrubbability certification gain preference among property developers and municipal project owners. Government energy-efficiency subsidies further tilt specifications toward cool-roof elastomeric systems and low-VOC interior emulsions. In contrast, solvent-borne products play a niche role in petrochemical and heavy-industrial settings, where chemical and abrasion resistance take precedence over emissions considerations.

The transition is also economic: domestic producers avoid import tariffs on water-based acrylic emulsions by using regionally sourced latex binders, thereby trimming costs and delivery times. Training programs run by multinational suppliers demonstrate brush, roller, and spray techniques tailored to high summer temperatures, reducing application defects. Cumulatively, these factors cement water-borne leadership and anchor the Iraq architectural coatings market’s environmental pivot.

By Resin: Acrylic leadership reflects climate adaptation

Acrylic systems retained a 39.60% share in 2024, thanks to superior UV stability and color retention at ambient highs exceeding 50°C. The Iraq architectural coatings market share for acrylics is tied to growing exterior repaint work, local tests indicating 18-month gloss retention versus 12 months for economy alkyds. Research confirms the energy-saving potential of acrylic topcoats that incorporate reflective pigments, adding measurable value to residential roofs and façades[2]Editorial Board, “Reflective Pigments Improve Roof Energy Savings,” frontiersin.org. Alkyds still serve budget-sensitive interiors, while polyurethane and epoxy variants satisfy industrial warehouses, bridges, and port facilities that demand chemical resistance and high film build.

Acrylic innovation continues to converge with green mandates as bio-based binders arrive from regional polymer units. Pilot lots with 20% plant-oil-derived content are being tested on walls in the Basra Trade Zone, indicating a longer-term shift toward sustainable feedstocks within the Iraqi architectural coatings market.

By Application: Interior focus drives volume growth

Interior coatings represented 68.40% of the 2024 volume, as multi-room apartments and office projects typically require multiple finish coats per unit. Standardized procurement under the national housing program directs demand toward mid-sheen acrylic emulsions that strike a balance between cost and performance. Supply chains optimized around 18-liter pails deliver scale efficiencies for paint makers.

Exterior specifications, however, are growing at the fastest rate, with a 5.87% CAGR, as developers prioritize building-envelope performance to reduce cooling loads. Field studies in Baghdad document a 35% reduction in roof heat transfer when cool-roof coatings are reapplied annually. High albedo façades are gaining traction across airport-city projects in Karbala and Mosul, widening the product mix and boosting the size of the Iraq architectural coatings market for exterior formulations.

Geography Analysis

Baghdad leads regional demand, absorbing the lion’s share of public works and private developments. The metro system, high-rise clusters, and government complexes collectively secure long-term contracts for protective and decorative segments. Kurdistan ranks second, aided by consistent security and USD 2.8 billion worth of ongoing construction projects, although 65% of its building materials still arrive from Turkish suppliers. Southern hubs, such as Basra, experience rising coatings consumption tied to Grand Faw Port and associated industrial estates, which require marine-grade epoxy systems to withstand the salt-laden air.

Central governorates capitalize on rail and highway upgrades that specify pavement-marking and anti-carbonation paints, creating steady throughput for bulk suppliers. Northern governorates experience intermittent spikes in activity as stability allows work on energy and mining infrastructure to resume. Local distribution networks, exemplified by Mass Iraq’s 300 agents, reduce lead times and win community repaint projects that larger multinational importers often overlook. Regional regulatory checks diverge between federal Iraq and the Kurdistan Regional Government; however, both now reference EN 13300 and ISO 12944 in their bidding documents, standardizing quality thresholds nationwide. Collectively, these dynamics reinforce the geographically diverse yet opportunity-rich landscape of the Iraq architectural coatings market.

Competitive Landscape

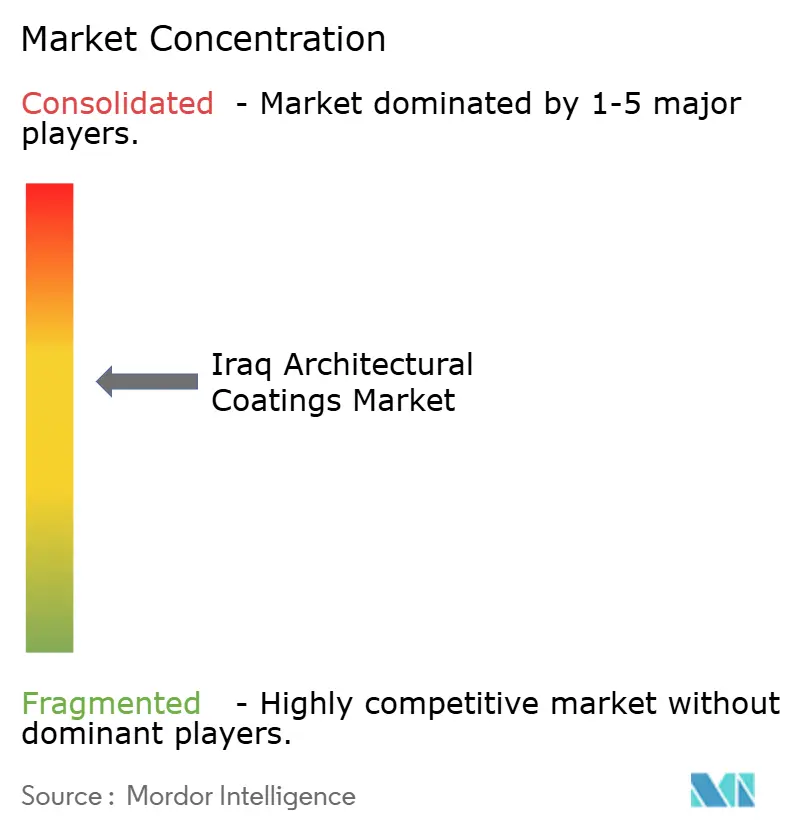

The Iraq Architectural Coatings market is moderately concentrated. Technology transfer emerges in joint ventures under the Iraq Development Fund’s eco-city scheme with ELSEWEDY ELECTRIC, channeling R&D into reflective and insulating coatings. Competitive differentiation is increasingly centered on climate performance data, supply reliability, and training services, rather than low price alone, steering the Iraq Architectural Coatings market toward a higher quality equilibrium.

Iraq Architectural Coatings Industry Leaders

Jotun

Caparol Paints

Akzo Nobel N.V.

Hempel A/S

Jazeera Paints

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Government of Iraq, supported by the European Union (EU) and the United Nations Human Settlements Programme (UN-Habitat), launched the National Housing Policy (NHP) 2025–2030 to address housing sector challenges, potentially increasing demand for architectural coatings.

- August 2025: Kalekim, a prominent player in the construction chemicals sector, which also ventures into architectural coatings, concluded Q2 2025 on target, buoyed by robust investment moves. The company initiated trial production at its Iraqi facility and expanded production capacity with new investments in Mersin and Diyarbakır.

Iraq Architectural Coatings Market Report Scope

| Residential |

| Commercial |

| Water-borne |

| Solvent-borne |

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

| Interior |

| Exterior |

| By End-user Industry | Residential |

| Commercial | |

| By Technology | Water-borne |

| Solvent-borne | |

| By Resin | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Application | Interior |

| Exterior |

Key Questions Answered in the Report

What is the current value of the Iraq architectural coatings market?

The sector was worth USD 124.91 million in 2025 and is forecast to reach USD 158.12 million by 2030.

Which segment holds the largest share of coating demand in Iraq?

Residential construction leads with 65.99% market share, reflecting ongoing large-scale housing initiatives.

Why are water-borne paints gaining ground in Iraq?

Tightening environmental regulations and increased awareness of indoor air quality have driven waterborne solutions to account for 69.35% of 2024 revenue.

Which resin type is most popular in Iraq’s hot climate?

Acrylic resins dominate because they maintain color and film integrity under temperatures above 50°C.

How will the Development Road project affect coatings demand?

The USD 17 billion, 1,200 km infrastructure plan requires vast quantities of protective and traffic-marking coatings, boosting near-term volumes.

Page last updated on: