Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

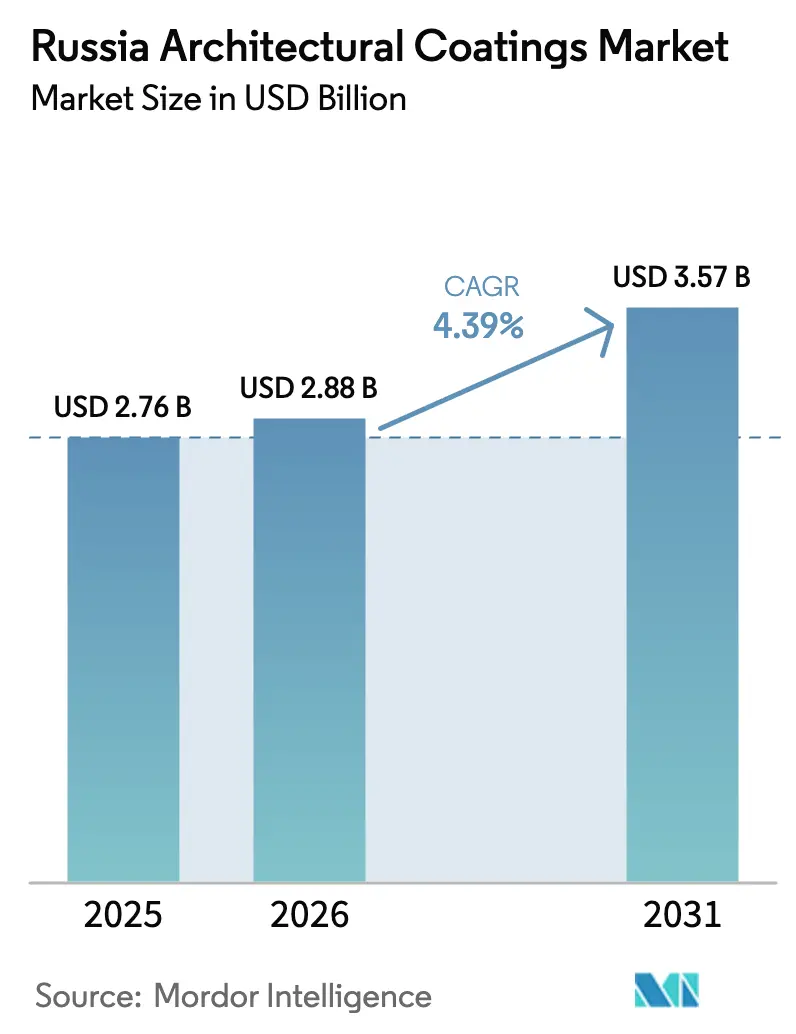

| Base Year Market Size (2025) | USD 2.76 Billion |

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 3.57 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Architectural Coatings Market Analysis by Mordor Intelligence

The Russia Architectural Coatings Market size is expected to increase from USD 2.76 billion in 2025 to USD 2.88 billion in 2026 and reach USD 3.57 billion by 2031, growing at a CAGR of 4.39% over 2026-2031. The headline growth figure hides an industry pivot driven by import substitution after Western exits, accelerated housing modernization, and the rollout of overlapping green-building codes. Domestic formulators are scaling polyacrylic, acrylic-polyurethane, and epoxy acrylate capacity to replace lost volumes from PPG/Tikkurila and Jotun, while distributors tighten private-label procurement to hedge currency swings. Demand remains firmly anchored in residential renovation, especially Moscow’s fast-tracked program, and in new multiplex housing that now requires Class A energy efficiency and certified low-VOC materials. Yet, persistent ruble volatility, titanium-dioxide dependency, and a 40% jump in painter wages squeeze margins, prompting value-engineering, thinner film builds, and growing interest in omnichannel fulfillment. E-commerce powerhouses Vseinstrumenti.ru, Ozon, and Wildberries already bundle coatings with turnkey tools, reshaping route-to-market economics and favoring suppliers offering digital shade-matching and site-based tech service.

Key Report Takeaways

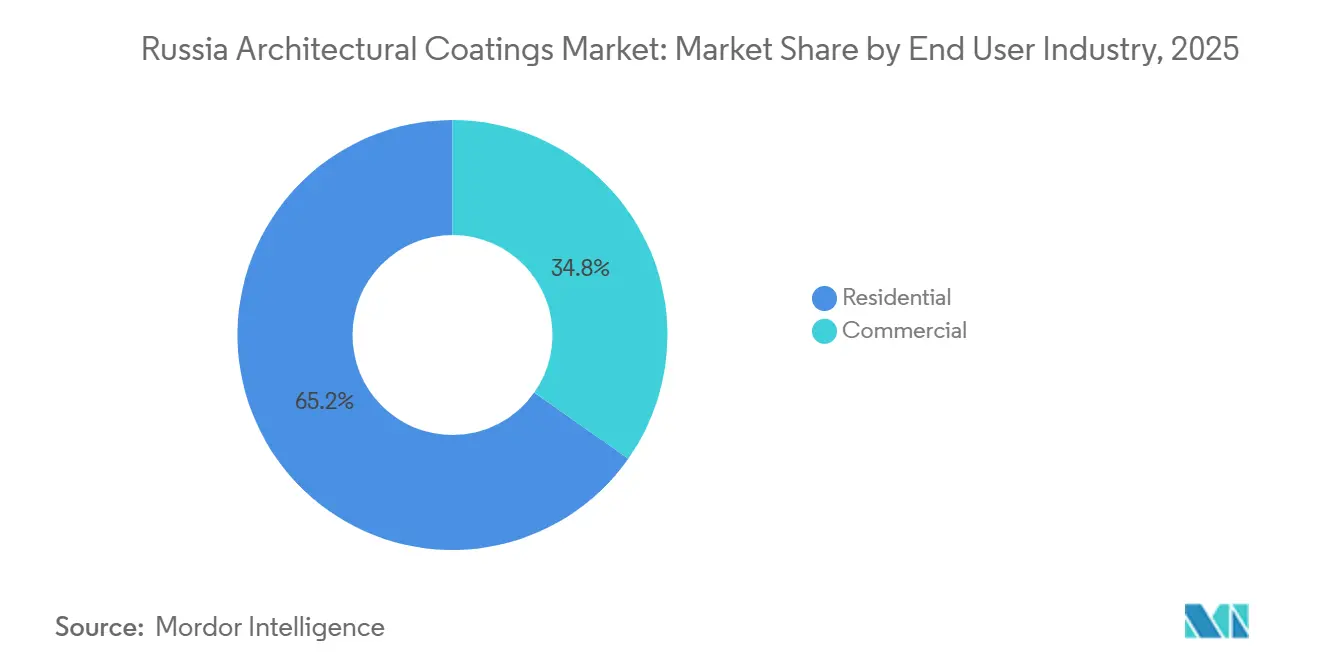

- By end-user industry, residential led with 65.23% of Russia architectural coatings market share in 2025 and is forecast to advance at a 4.67% CAGR through 2031.

- By technology, waterborne products commanded 78.89% of the Russia architectural coatings market size in 2025; the segment is projected to grow at 4.55% CAGR over 2026-2031.

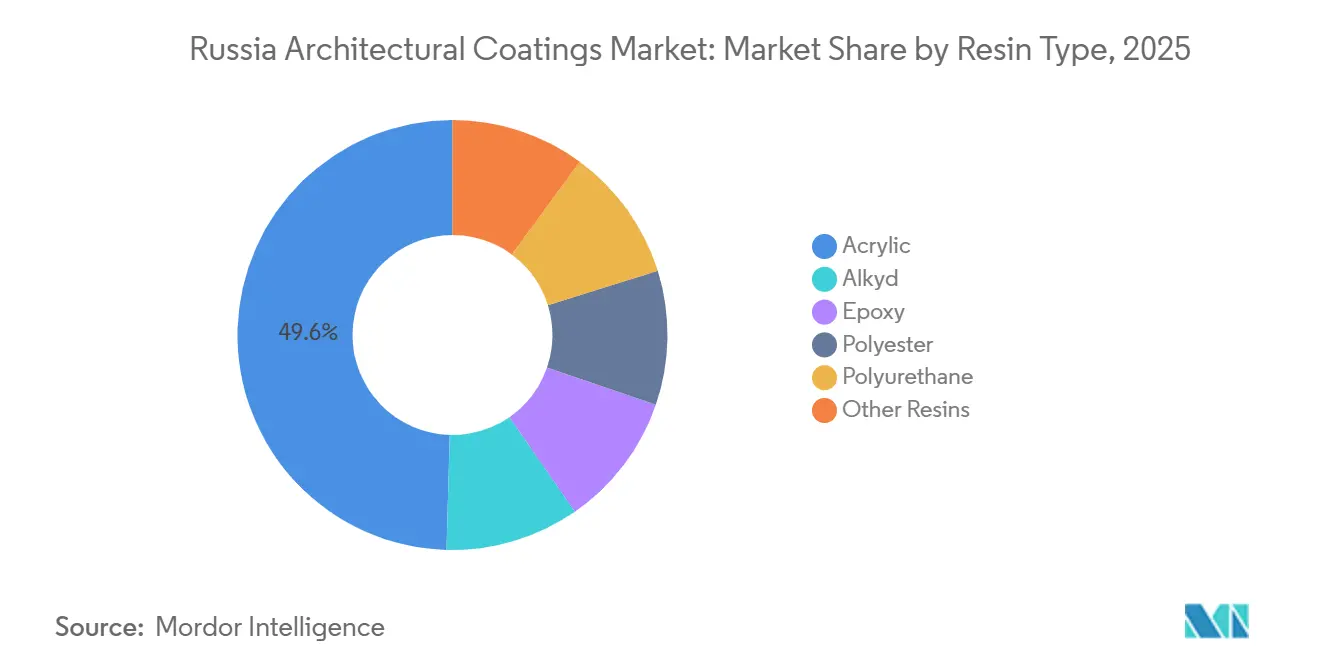

- By resin type, acrylic systems captured 49.56% share of the Russia architectural coatings market size in 2025 and are expected to expand at a 4.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-building codes and low-VOC mandates | +0.8% | National, with concentration in Moscow, St. Petersburg, and regional capitals adopting GOST R 71468-2024 | Medium term (2–4 years) |

| Post-war reconstruction and housing modernization wave | +1.2% | National, with highest intensity in Moscow (7.9M sqm renovated since 2017), Central FD, and newly integrated territories | Long term (≥4 years) |

| DIY retail expansion into secondary Russian cities | +0.5% | Regional cities in Volga, Siberian, and Ural Federal Districts; secondary markets beyond Moscow/St. Petersburg | Medium term (2–4 years) |

| Rapid shift to e-commerce paint sales | +0.4% | National, led by Moscow and St. Petersburg; B2B online strongest in professional contractor segments | Short term (≤2 years) |

| Emergence of bio-based binders from domestic chemical start-ups | +0.3% | Tomsk, Lipetsk, and industrial clusters in Central FD; early-stage localized impact | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Green-Building Codes and Low-VOC Mandates

Two overlapping standards, GOST R 71468-2024 (in force since January 2025) and the new interstate green code effective July 2026, now oblige developers to achieve Class A energy efficiency, certify up to 50% of installed materials, and demonstrate 30-60% reductions in heating demand[1]ZA-STROY.RF, “Interstate Green Standard for Multi-Apartment Buildings,” za-stroy.rf. Buildings that earn Bronze, Silver, or Gold ratings gain preferential escrow finance, adding financial ballast to environmental compliance. Multiplex developers have already registered 226 qualifying projects, lifting demand for waterborne acrylic and acrylic-polyurethane coatings that meet VOC-chamber criteria. The modular-construction-specific GOST R 72520-2026 further requires ISO 16000-9 testing and digital eco-passports, nudging factory finishers toward low-odor systems compatible with off-line tinting. Legacy alkyd and solventborne lines now lose shelf space in DIY chains as buyers migrate to green-label SKUs.

Post-War Reconstruction and Housing Modernization Wave

Deputy Prime Minister Marat Khusnullin confirmed an ambition to renovate one-third of Russia’s aging housing within six years while erecting 663 million sqm of new dwellings. Moscow alone delivered 2.3 million sqm in 2025 and 7.9 million sqm cumulatively since 2017, using modular blocks that cut build cycles to six months[2]IZVESTIA.RU, “Moscow Renovation Program Accelerates,” izvestia.ru. A parallel RUB 4.5 trillion communal-infrastructure plan spans 18,000 utility assets and 140,000 km of networks, unlocking coatings spend on both exterior envelopes and buried pipelines. However, Soviet-era apartment blocks that have exceeded their design life are often slated for demolition under economic-feasibility rules, focusing paint demand on replacement housing rather than deep interior retrofits.

DIY Retail Expansion into Secondary Russian Cities

Lemana PRO rebranded its 112 superstores and raised domestic‐sourced assortment to 72%, pursuing 18-20% private-label turnover by end-2026. Lenta’s buyout of OBI’s 25 formats adds 263,000 sqm of retail floor and heralds hybrid hypermarket/DIY concepts in regions such as Samara and Perm. Regional chains Petrovich and Baucenter scale project-oriented “ready-solution” bundles, combining coatings with design consult and on-site application. The resulting channel reach gives mid-tier domestic producers like VGT and Yaroslavskie Kraski a direct pipeline beyond Moscow, but it also intensifies price wars as store brands import alternative resins and pigments from China and Türkiye.

Rapid Shift to E-Commerce Paint Sales

Online DIY turnover climbed 7.7% year-on-year to RUB 144.3 billion in H1 2025, accounting for an estimated 14% of decorative-paint retail value. Vseinstrumenti.ru registered RUB 86.8 billion revenue with a 73.7% B2B mix, underscoring contractors’ growing appetite for click-and-collect tinting and bulk shipment. Marketplaces Ozon and Wildberries posted 43.1% and 57.6% revenue surges, respectively, but maintain razor-thin margins that push suppliers to distinguish via technical chatbots, consumption calculators, and five-hour urban delivery. For manufacturers, API-based catalog syndication and BIM object libraries evolve from nice-to-have to license-to-operate capabilities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported TiO₂ price volatility and rouble swings | -0.6% | National; acute in import-dependent producers lacking vertical integration or long-term supply contracts | Short term (≤2 years) |

| Skilled-labour shortage for professional applicators | -0.4% | National, most severe in Moscow, St. Petersburg, and fast-growing regional centers; exacerbated by migrant-labor reduction | Medium term (2–4 years) |

| Cold-climate curing challenges for waterborne formulas | -0.2% | Northern regions, Siberia, Far East; seasonal impact October–April | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Imported TiO₂ Price Volatility and Ruble Swings

With imports forming up to 80% of input costs, a falling ruble translates into immediate pigment inflation; titanium-dioxide prices alone helped push 2024 finishing-material costs up 12.9%. Russian receipts for HS 3208/3209 coatings collapsed from USD 536.6 million in 2021 to USD 106.4 million in 2023 under sanctions pressure, leaving formulators exposed to spot cargoes from Asia at unpredictable dollar quotes. Downstream, DIY retailers resist full cost passthrough, compressing producer margins and discouraging green-field investment outside vertically integrated giants such as Ruschem.

Skilled-Labor Shortage for Professional Applicators

Average painter wages leapt 40% year-on-year to RUB 118,400 per month in 2025 as migrant labor dwindled and domestic trade schools failed to backfill vacancies. Developers now face delivery delays and budget resets, often trimming finishing scopes or shifting to pre-coated panels. For paint suppliers, labor scarcity reinforces demand for high-build single-coat systems, spray-applied polyurethanes, and manufacturer-led training academies that help contractors reduce four-coat cycles to two, without sacrificing warranty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Residential Renovation Commands Majority Volume

The residential slice of the Russia architectural coatings market held a 65.23% revenue share in 2025, propelled by rapid relocation programs and 63.5 million sqm of individual housing (IZhS) completions that year. Commercial commissioning surged primarily in warehouses and mid-tier offices, yet an authorized pipeline of 186.2 million sqm flags possible oversupply and softer coatings offtake post-2027. Builders pursuing fixed-price contracts consequently favor competitively priced acrylic-alkyd hybrid interiors that deliver acceptable scrub resistance at lower dry-film thickness.

The segment outlook remains skewed toward dwellings, with residential coatings predicted to grow at 4.67% CAGR to 2031. Mortgage subsidies backing more than 80% of originations, plus a widening DIY footprint in secondary cities, ensure baseline demand. Conversely, warehouse completions are forecast to slow once marketplace logistics centers normalize inventory, curbing epoxy floor-coating volume by late-decade.

By Technology: Waterborne Dominance Continues Despite Winter Curing Hurdles

Waterborne products accounted for 78.89% of 2025 sales and should lift marginally as GOST-linked public procurement insists on Type I ecolabels. The segment is anticipated to register a CAGR of 4.55% during the forecast period 2026-2031. Solventborne systems still dominate exterior work in Siberia and the Arctic, where application down to −25 °C is routine; grades like Bronya Winter, which require orthoxylene dilution, illustrate the residual role of VOCs for sub-zero jobs.

Forward-looking builders adopt engineered latexes with tertiary polyamines that expand coalescence windows to −5 °C without excess amines, but such binders remain licensed technology not yet copied by local monomer plants. The result is a dual-track trajectory: mainstream Class B and C residential projects convert fully to waterborne acrylics, while industrial hangars, pipelines, and arctic exploration camps retain solventborne polyurethanes and epoxies.

By Resin Type: Acrylic Retains Leadership While Epoxy Gains Niche Share

Acrylic resins secured 49.56% of the 2025 market revenue and are anticipated to grow with 4.60% CAGR through 2031, owing to upcoming domestic polyacrylic lines in Lipetsk and expanded PVC-E feedstock from Bashkir Soda.

Epoxy volumes, while smaller, climb on logistics warehouse construction and hospital flooring renewals, areas where 2-component systems promise 30-year lifecycles. Alkyd units edge down as oil-price-linked phthalic anhydride inflates raw-material spend, making hybrid acrylic-alkyd chemistries the mid-price alternative. Polyurethane and polyester capture niche applications such as wood façades and powder-coated railings, but remain capacity-lagged given the limited di-isocyanate supply.

Geography Analysis

Moscow and the broader Central Federal District together consumed a significant Russia architectural coatings market demand in 2025, buoyed by a further 2.3 million sqm of renovated stock and aggressive office completions. The Volga and Southern Federal Districts trail but still represent a combined 23%, amplified by Lenta-OBI banner conversions that add 60,000 sqm of incremental paint shelf space.

The Ural region posted a blistering growth in non-residential commissioning, and its metals hub in Sverdlovsk creates a captive market for corrosion-resistant floor epoxies. Siberia’s split-season climate cramps exterior paint days to five summer months; however, state-subsidized Arctic infrastructure funnels defense-grade polyurethanes and thermal-insulating ceramics for year-round energy depots.

Retail penetration mirrors macro disparity: Moscow averages one organized DIY outlet per 110,000 residents versus one per 480,000 in Krasnoyarsk. E-commerce bridges some of that gap, yet high-latitude delivery still tops RUB 140/kg, encouraging local tint plants in Novosibirsk and Yakutsk to formulate short-life pastel shades on demand. Across all regions, the Russia architectural coatings market continues to bifurcate into service-led premium hubs and cost-sensitive rural corridors.

Competitive Landscape

The Russia architectural coatings market is moderately consolidated. Foreign departures have re-sorted the field. Jotun’s assets went to Atomstroykomplex in 2022, while PPG’s Tikkurila unit transferred to Smart Business Group and relaunched as Tikkivala in Q1 2025, after PPG booked a USD 146 million impairment. AkzoNobel scaled to a maintenance presence, leaving domestic makers VGT, Yaroslavskie Kraski, and Lakra Sintez to jostle for shelf space.

VGT operates two plants, supplies more than 200 SKUs, and claims coverage in 73 Russian regions; its Moscow site will add a third automatic tint line in 2027. Yaroslavskie Kraski leverages ISO 9001 and IATF 16949 credentials to win automotive fillers and now rolls out decorative latex produced on the same high-solids line, enhancing plant utilization. Lakra Sintez doubles down on regional DIY private-label supply, guaranteeing 72-hour cross-dock refill to Lemana PRO’s dark stores.

Russia Architectural Coatings Industry Leaders

AkzoNobel N.V.

PPG Industries, Inc.

Lakra Sintez

Russian Paints Company

Eskaro Group AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Russia ratified a new interstate green standard for multi-apartment buildings, effective July 2026, embedding Class A energy criteria and ecolabel mandates.

- February 2025: PPG and Finnish Tikkurila finalized their Russian exit; Smart Business Group rebranded the acquired assets as Tikkivala from Q1 2025.

Russia Architectural Coatings Market Report Scope

Architectural coatings are specialized products designed for application on residential and commercial buildings to deliver aesthetic appeal, weather resistance, and long-term durability. These coatings protect structures from moisture, UV radiation, and corrosion, while enhancing the visual appearance of both interior and exterior surfaces.

The Russia architectural coatings market is segmented by end-user industry, technology, and resin type. By end-user industry, the market is segmented into commercial and residential. By technology, the market is segmented into solventborne and waterborne. By resin type, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By End User Industry

| Commercial |

| Residential |

By Technology

| Solventborne |

| Waterborne |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resins |

| By End User Industry | Commercial |

| Residential | |

| By Technology | Solventborne |

| Waterborne | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resins |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms