Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

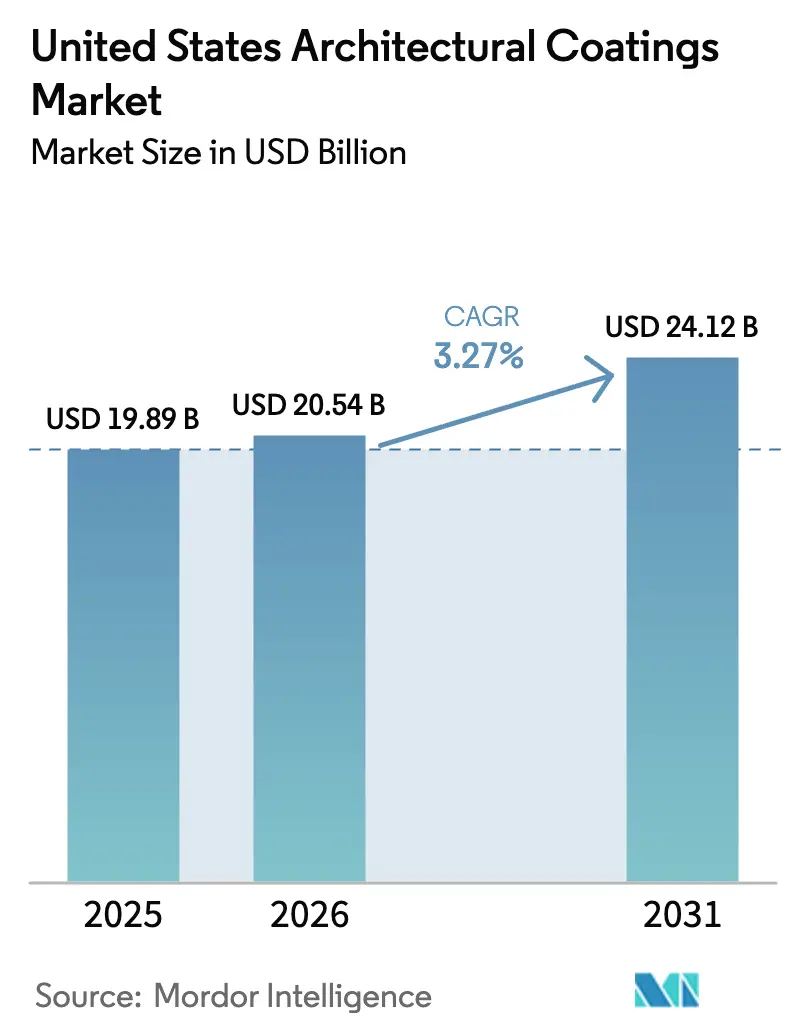

| Base Year Market Size (2025) | USD 19.89 Billion |

| Market Size (2026) | USD 20.54 Billion |

| Market Size (2031) | USD 24.12 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

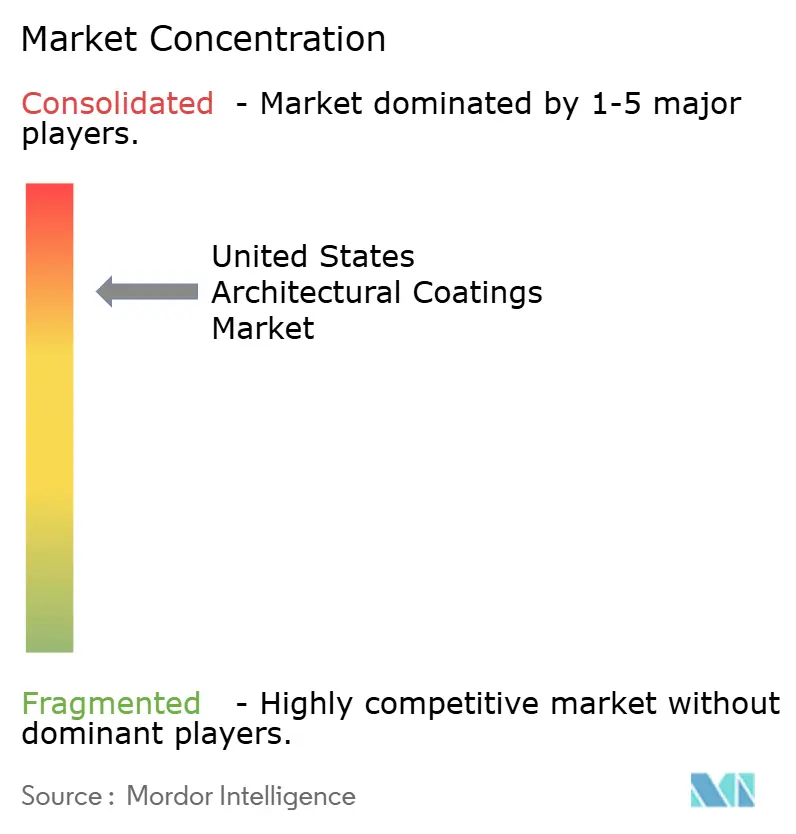

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Architectural Coatings Market Analysis by Mordor Intelligence

The United States Architectural Coatings Market size was valued at USD 19.89 billion in 2025 and estimated to grow from USD 20.54 billion in 2026 to reach USD 24.12 billion by 2031, at a CAGR of 3.27% during the forecast period (2026-2031). The mature but expanding demand profile stems from a large, aging housing inventory, tightening environmental regulations, and steady innovation in water-borne chemistries that match or exceed solvent-borne performance. Residential remodeling remains the backbone of the US architectural coatings market, supported by USD 509 billion in projected 2025 improvement spending that favors exterior repaint cycles and upgraded interior finishes[1]Abbe Will, “Improving America’s Housing 2025,” Harvard Joint Center for Housing Studies, jchs.harvard.edu. New single-family construction is stabilizing near 1.3 million annual starts, injecting incremental volume, particularly in Sun Belt states where larger floor plans increase per-unit coating consumption. Parallel regulatory momentum toward sub-50 g/L VOC ceilings is boosting the penetration of acrylic-based water systems, which already command the bulk of the US architectural coatings market. Ongoing raw-material volatility centered on titanium dioxide and petro-resins tempers margin expansion but continues to reinforce scale advantages for integrated suppliers.

Key Report Takeaways

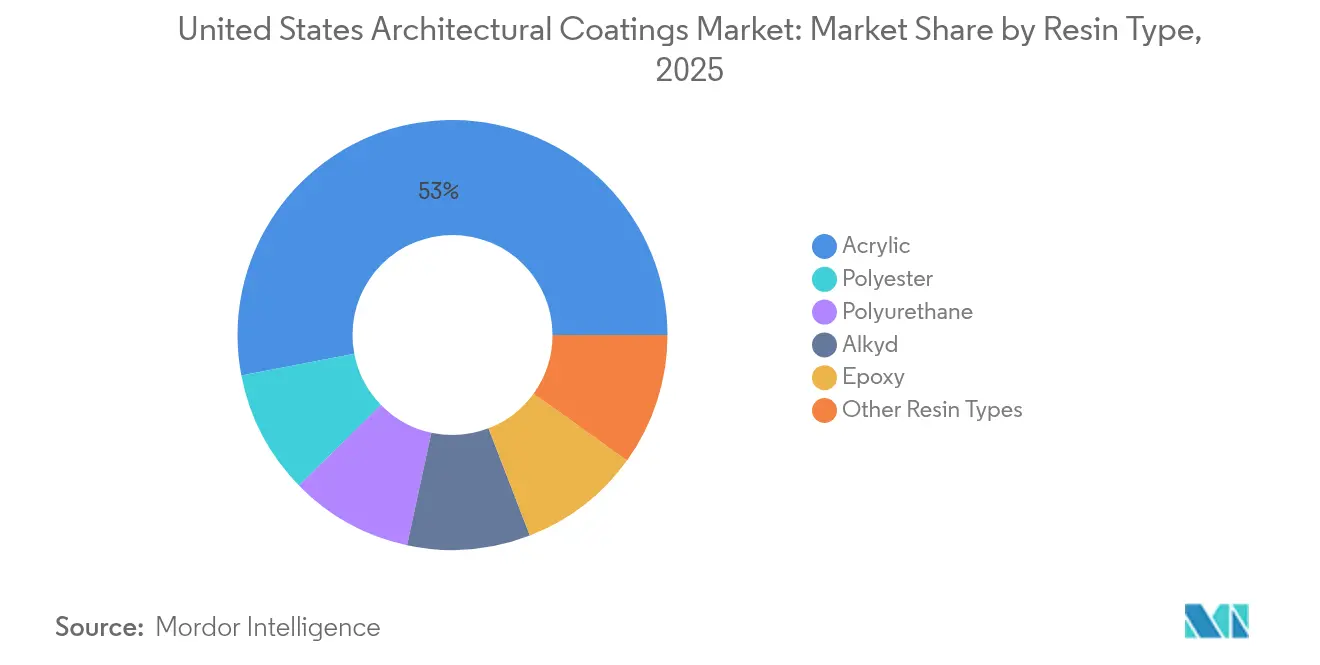

- By resin type, acrylic accounted for the largest revenue share of 53.02% in 2025 and is expected to grow at a CAGR of 3.78% during the forecast period (2026-2031).

- By technology, water-borne had a share of 86.74% in 2025, and this share is expected to increase with a CAGR of 3.48% during the forecast period (2026-2031).

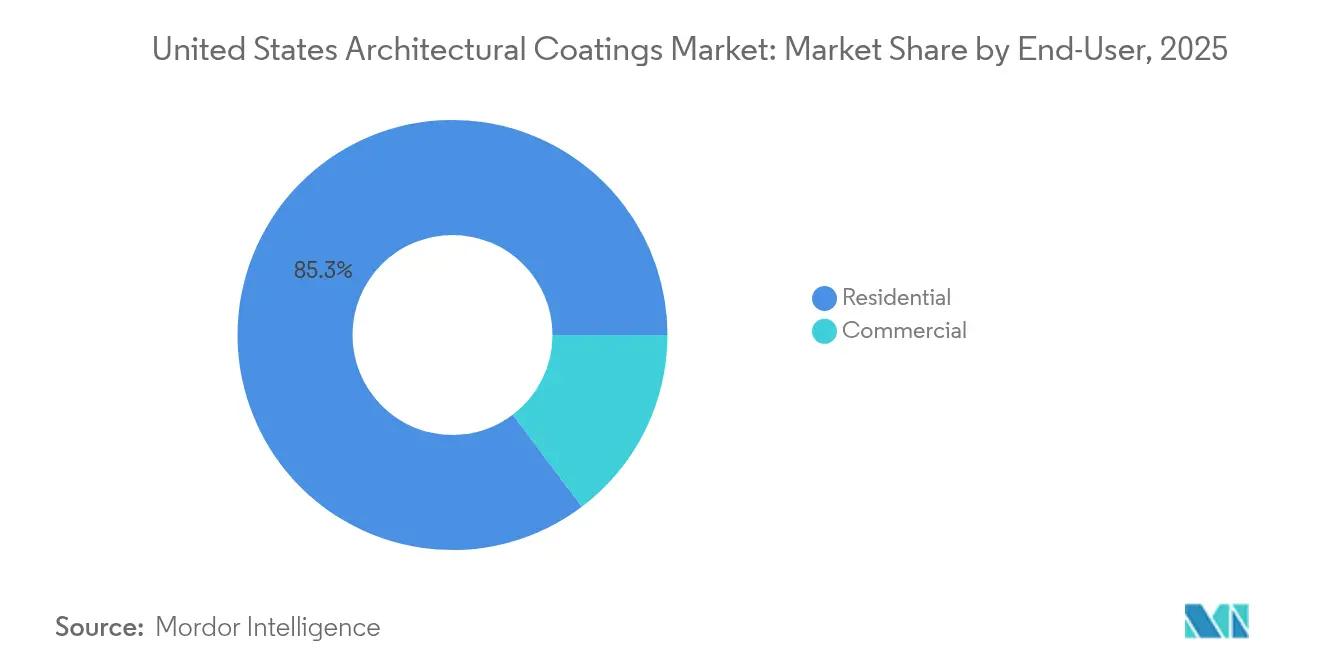

- By end-user, the market share of residential was the highest in 2025, of about 85.28%. Moreover, this share is anticipated to grow with the fastest CAGR of 3.4% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential remodeling surge from aging stock | +1.2% | Northeast, Midwest, national coverage | Long term (≥ 4 years) |

| Growth in new housing starts | +0.8% | Texas, Florida, Arizona, wider Sun Belt | Medium term (2-4 years) |

| Low-VOC water-borne adoption | +0.6% | California, Northeast, national spill-over | Long term (≥ 4 years) |

| Heat-reflective cool-coating uptake | +0.4% | Southwest, broader Sun Belt | Medium term (2-4 years) |

| OEM demand from off-site modular builds | +0.3% | Early uptake in Southeast, national scale-ups | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Residential Remodeling Surge from Aging Housing Stock

More than half of US owner-occupied dwellings are over 40 years old, anchoring a structural repaint cycle that shields the US architectural coatings market from sharp construction downturns. Harvard research estimates 2025 homeowner improvement expenditures at USD 509 billion, with exterior paint and stain work accounting for 8-12% of that spend. Older housing concentrations in the Northeast and Midwest result in higher per-capita paint consumption and a preference for premium products that promise longer repaint intervals. Professional painters report exterior projects now averaging 12-15 years between coats, a material extension from the past decade, thanks to advanced acrylic binders. The longevity imperative fosters demand for higher-margin, warranty-backed topcoats that underpin profitability for market leaders in the US architectural coatings market.

Growth in New Housing Starts

Single-family starts hovering at 1.3 million units annually underpin a gradual volume uplift for the US architectural coatings market, even as elevated interest rates cool multifamily development. Texas, Florida, and Arizona collectively account for roughly 35% of national starts, concentrating growth in hot-climate regions where heat-reflective and high-build moisture-barrier coatings carry premium price tags[2]U.S. Census Bureau, “New Residential Construction September 2025,” census.gov. New dwellings now average 2,400 square feet—approximately 30% larger than the existing stock—resulting in an expansion of surface-area demand per home. Larger footprints combined with design shifts toward open-plan interiors fuel incremental gallons per project and maintain a favorable outlook for the US architectural coatings market.

Adoption of Low-VOC Water-Borne Technologies

Regulators continue to ratchet down allowable VOC thresholds, with California’s Rule 1113 patterning the federal trajectory toward sub-50 g/L limits. Waterborne acrylic systems already comprise more than 86% of the US architectural coatings market, and accelerated uptake is expected as Northeast states follow California’s lead. Formulators now deliver waterborne products that survive accelerated weathering as well as, or better than, their solvent-borne predecessors, erasing historical performance hesitancy. Price premiums of 15-20% for zero-VOC interior lines encourage margin expansion, while reduced hazardous air pollutant reporting lowers compliance costs. These converging benefits keep water-borne innovation at the center of competitive positioning across the US architectural coatings market.

Heat-Reflective “Cool” Coatings for Sun Belt Compliance

Rising energy codes in the Sun Belt incentivize cool-roof and exterior wall technologies that can lower building skin temperatures by 30-40°F, resulting in 10-15% savings on HVAC energy. Utility rebate programs and LEED point structures further accelerate penetration in Texas, Florida, and California, where population inflows sustain robust new-build pipelines. Proprietary pigment packages engineered to reflect the infrared spectrum fetch significant price premiums and embed differentiation for early adopters in the US architectural coatings market. Mainstream builders are beginning to specify cool-roof options as standard upgrades, reinforcing a medium-term growth pocket.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.7% | Global supply dependency; amplified in US coatings | Short term (≤ 2 years) |

| Contractor labor shortages | -0.5% | Nationwide, most acute in high-growth Sun Belt | Medium term (2-4 years) |

| Shift toward composite siding & veneer | -0.3% | Premium segments, suburban infill and tear-downs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (TiO₂, Petro-Resins)

Titanium dioxide, which accounts for roughly one-third of the cost of high-quality white paint, remains exposed to Chinese export fluctuations that have produced 20-30% price spikes within a single calendar year. Petroleum-based binders introduce a second layer of volatility tied to crude oil swings, compressing gross margins and prompting mid-tier suppliers to consider implementing surcharge mechanisms. Integrated majors hedge through multi-year contracts and backward integration, but small and mid-sized brands in the US architectural coatings market face thinner buffers against spot surges, occasionally triggering price pass-throughs that dampen DIY demand.

Contractor Labor Shortages

Seventy-eight percent of general contractors report difficulty in recruiting painters, while 45% indicate that project delays are directly tied to labor scarcity. A tight supply inflates wage bills and extends job schedules, limiting throughput for both residential repaint cycles and new-build finishing stages. As Sun Belt migration strains local labor pools, some homeowners postpone elective projects, moderating the otherwise robust growth trajectory of the US architectural coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Durability Sets the Pace

Acrylic formulations held 53.02% of the total US architectural coatings market share in 2025, and this lead is projected to expand at a 3.78% CAGR through 2031 as property owners prioritize weatherability, color retention, and VOC compliance. The segment’s dominance is anchored in cross-linkable polymer chemistries that deliver fade resistance in high-UV geographies while enabling waterborne systems that are acceptable under tightening regulations. Alkyd products persist for specialty heritage restorations that require high gloss and flow, but encounter slowing demand as solvent restrictions take effect. Polyurethane and epoxy variants carve out niche positions in commercial kitchens, hospitals, and parking decks, where abrasion resistance and chemical tolerance take precedence over aesthetics.

Hybrid chemistries combining acrylic backbones with silicone or fluoropolymer modifiers illustrate the next evolution in premium wall and roof offerings, commanding price premiums and extending service intervals beyond 15 years. Producers leveraging proprietary latex particle engineering reinforce brand equity and secure shelf space at pro-paint centers, a channel that constitutes roughly 60% of value sales across the US architectural coatings market.

By Technology: Water-Borne System Supremacy

Water-based lines represented 86.74% of 2025 unit volume and will capture further share as commercial builders chase LEED credits and occupants demand healthier indoor air. Federal and state VOC caps have rendered solvent-borne formulations effectively niche, relegated mostly to cold-weather touch-up work and select metal primers. The US architectural coatings market size for water-borne grades across interior and exterior applications is projected to post a 3.48% CAGR, underpinned by continual resin innovation that mimics alkyd flow without odor or flammability hazards.

Manufacturing efficiencies also promote adoption; water systems eliminate the need for costly explosion-proof infrastructure and simplify wastewater management. Market leaders in the US architectural coatings market incorporate antimicrobial agents and scuff-resistant particles during dispersion, catering to end-user preferences for hygienic, low-maintenance surfaces in schools and healthcare facilities.

By End-User: Residential Still Reigns

The residential channel accounted for 85.28% of the US architectural coatings market volume in 2025 and is expected to continue expanding at a 3.4% CAGR through 2031, driven by aging stock renovations and consistent aesthetic refresh cycles. DIYers remain active, but professionals now capture a growing share as homeowners opt for time savings and longer-lasting finishes. Premium interior eggshell and exterior satin sheens outsell economy flat finishes, reflecting a consumer preference for durability and cleanability.

Commercial demand is diversifying beyond traditional office buildings into advanced manufacturing facilities, logistics hubs, and institutional campuses. These projects specify higher solids and color-stable finishes to reduce maintenance overhead, supporting incremental gains even as remote work impacts new office start approvals. Sustainability mandates in hospitals and universities favor zero-VOC lines, reinforcing technology leadership aspirations for suppliers entrenched in the US architectural coatings market.

Geography Analysis

Legacy housing concentrations in the Northeast and Midwest underpin a high-value repaint cycle, characterized by older, wood-clad homes that require frequent exterior upkeep. Premium elastomeric wall coatings that bridge hairline cracks have gained share, as owners of century-old stock prioritize weather armor over initial cost. Regional dealer networks tailor assortments to these climate stresses, underscoring the localized service model still prevalent across the US architectural coatings market.

Pacific Coast jurisdictions led by California impose the nation’s tightest VOC ceilings, catalyzing manufacturer R&D investment in ultra-low-emission resins. Oregon and Washington adopt similar thresholds, hastening a regional migration toward bio-based binders derived from soy and castor oils. While such products currently represent a single-digit share, early-adopter consumers in high-income metropolitan areas like San Francisco and Seattle help validate commercial pathways that could subsequently scale across the broader US architectural coatings market.

Competitive Landscape

The United States Architectural Coatings market is concentrated. Sherwin-Williams anchors its advantage through more than 4,800 company-owned stores that embed loyalty among professional painters, while PPG leverages scale in raw-material procurement to buffer margin swings. Benjamin Moore differentiates through a premium independent dealer network, emphasizing color accuracy and upscale branding. Differentiation is shifting toward service-plus-solution ecosystems, rather than focusing on price, which sustains healthy margins across the upper tier of the market.

United States Architectural Coatings Industry Leaders

Benjamin Moore & Co.

Masco Corporation

PPG Industries, Inc.

RPM International Inc.

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Rodda Paint Company, based in Oregon, in partnership with the Cloverdale Group, based in Surrey, Canada, announced the acquisition of Miller Paint Company, a manufacturer of architectural coatings in the United States. This will increase the company's overall revenue and product portfolio.

- December 2024: PPG Industries, Inc. completed the sale of 100% of its architectural coatings business in the United States (US) and Canada at a transaction value of USD 550 million to American Industrial Partners (AIP), an industrials investor.

United States Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms