UAE Architectural Paints And Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

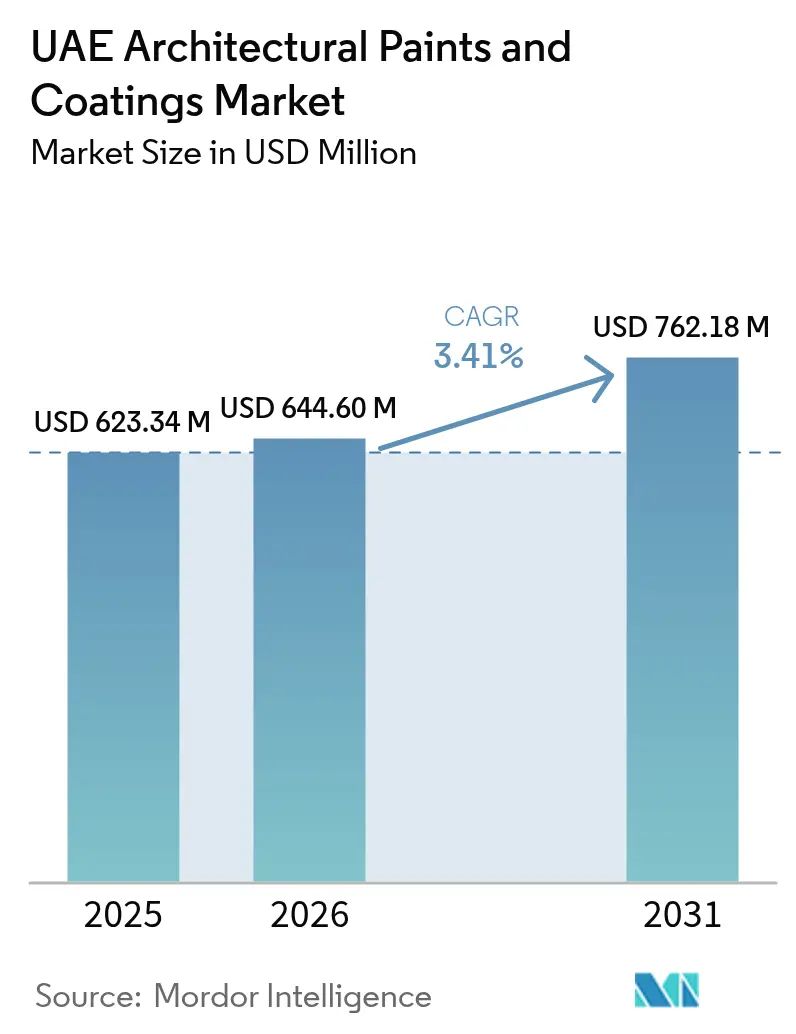

| Base Year Market Size (2025) | USD 623.34 Million |

| Market Size (2026) | USD 644.6 Million |

| Market Size (2031) | USD 762.18 Million |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

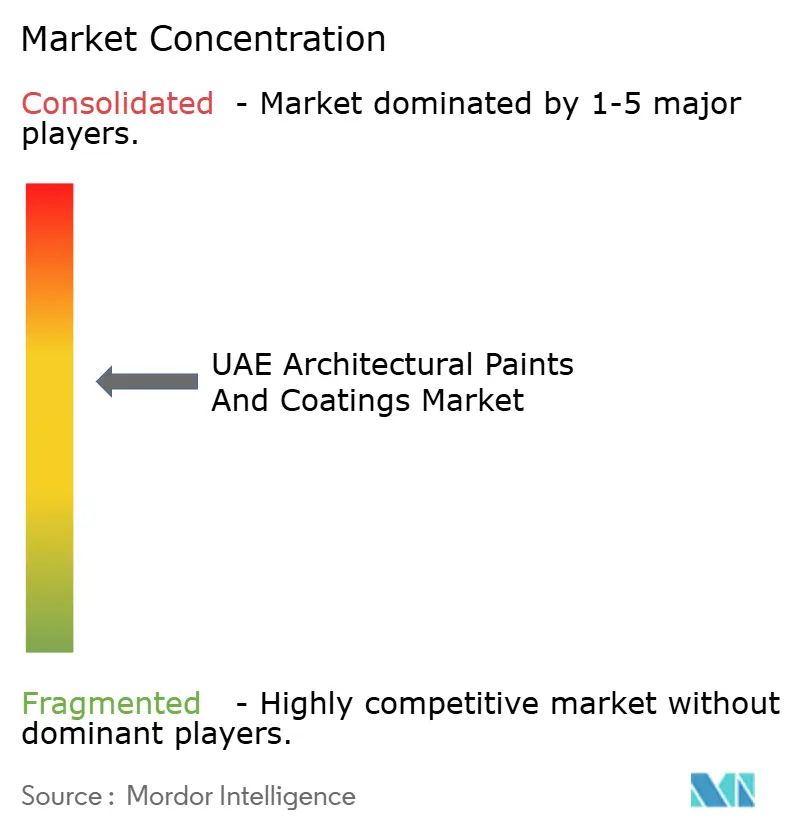

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Architectural Paints And Coatings Market Analysis by Mordor Intelligence

The UAE Architectural Paints and Coatings Market size is expected to grow from USD 623.34 million in 2025 to USD 644.6 million in 2026 and is forecast to reach USD 762.18 million by 2031 at 3.41% CAGR over 2026-2031. This moderated growth pace mirrors a maturing construction sector that now favors premium, compliance-ready formulations over commodity products. Architectural demand remains anchored in Dubai’s mixed-use and residential pipeline, while Abu Dhabi’s retrofit agenda sustains protective and specialty demand despite cyclical slowdowns in new government awards. Waterborne technology continues to expand on the back of stringent indoor-air-quality rules, and acrylic resins dominate due to their UV resistance and alignment with emirate-level VOC limits. Competitive intensity is shifting away from price toward regulatory compliance, local testing infrastructure, and technical service capabilities, giving established regional manufacturers and multinational incumbents a structural advantage.

Key Report Takeaways

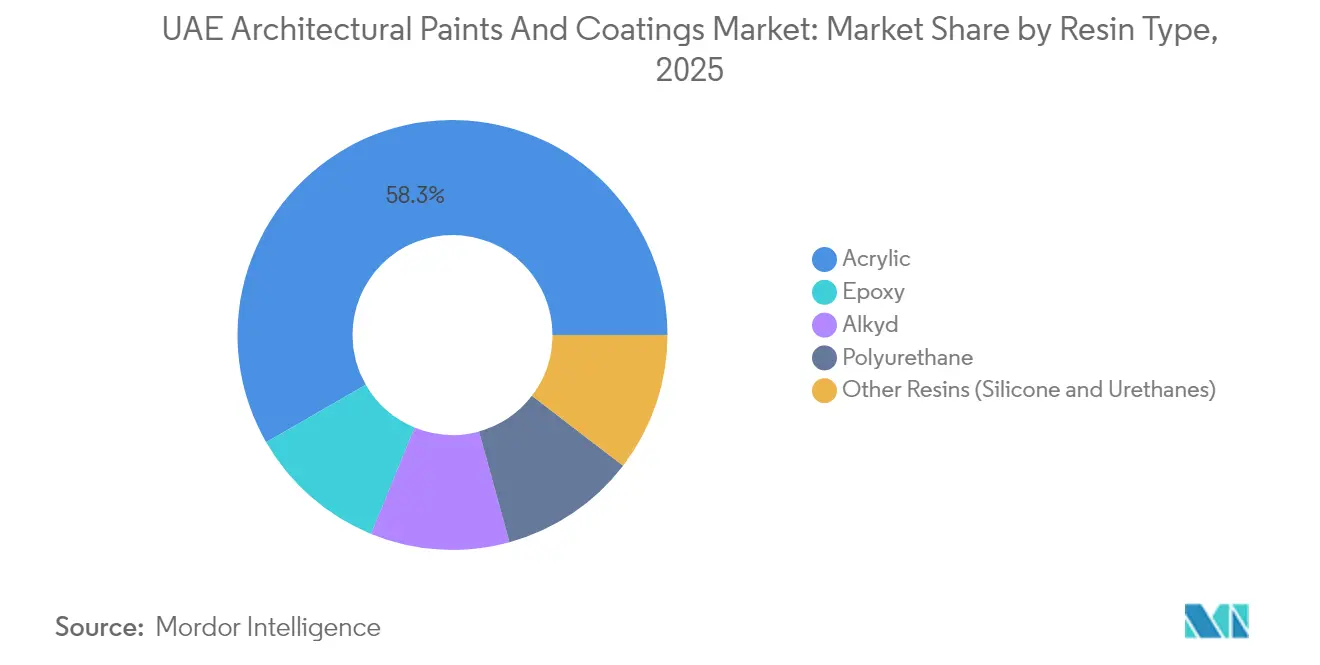

- By resin type, acrylics captured 58.31% of the UAE paints and coatings market share in 2025. Moreover, the share of acrylics is expected to increase with a CAGR of 3.78% during the forecast period (2026-2031).

- By technology, waterborne systems accounted for 71.55% of the UAE paints and coatings market size in 2025 and are projected to grow at a 4.02% CAGR through 2031.

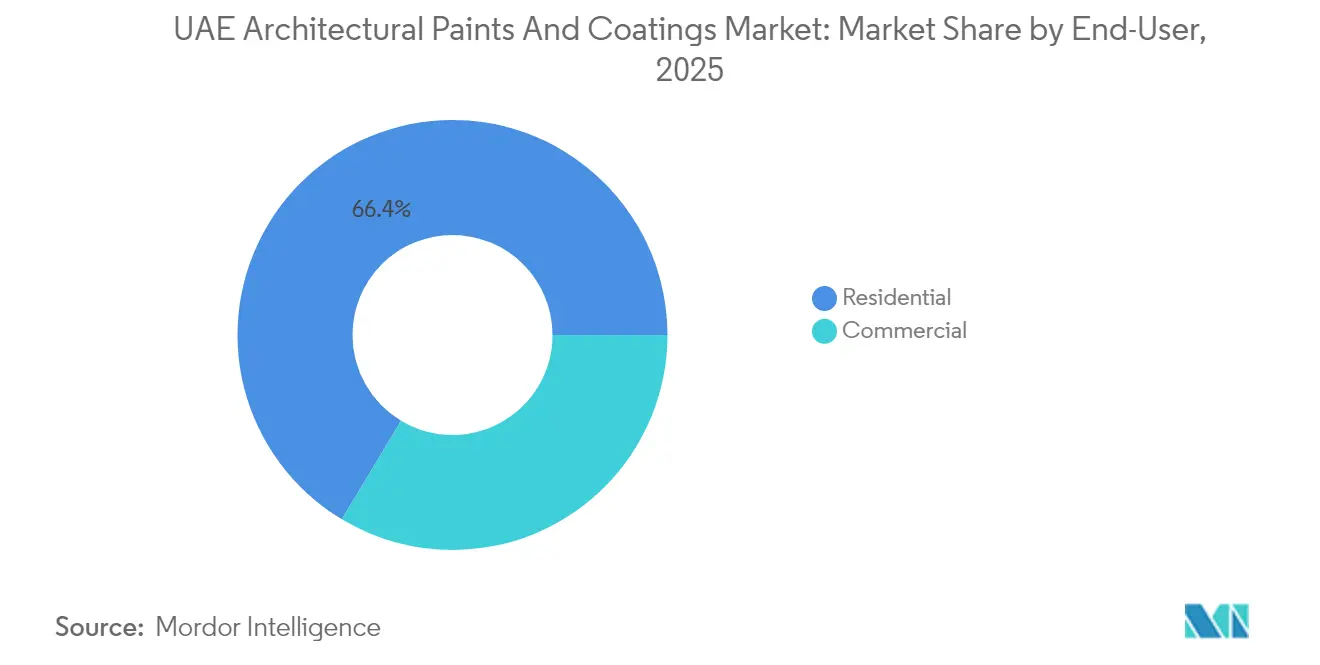

- By end-user, the residential segment led with a 66.40% revenue share of the UAE paints and coatings market size in 2025, while commercial applications are expected to advance at a 3.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Architectural Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential construction boom in Dubai and Northern Emirates | +1.2% | Dubai, Sharjah, Ajman, Ras Al Khaimah | Medium term (2-4 years) |

| Tourism-led demand for hospitality refurbishments | +0.8% | Dubai, Abu Dhabi coastal areas | Short term (≤ 2 years) |

| Mandatory green-building codes driving low-VOC paints | +0.9% | UAE-wide, strongest in Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Smart-city initiatives fuelling demand for heat-reflective coatings | +0.4% | Dubai, Abu Dhabi urban cores | Medium term (2-4 years) |

| Rise of design-build contracts accelerating specification of premium finishes | +0.6% | UAE-wide, concentrated in major projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Residential Construction Boom in Dubai and Northern Emirates

Dubai handed over 10,000 housing units in Q1 2024, with an additional 25,000 units slated by year-end, pushing the emirate’s stock toward 754,000 units[1]Jones Lang LaSalle, “Dubai Residential Market Q1 2024,” JLL, jll.com. Similar momentum in Sharjah, Ajman, and Ras Al Khaimah stems from affordability programs and population-growth incentives that sustain multisegment demand for interior and exterior finishes. Consistent handover schedules foster predictable coating procurement cycles, favoring suppliers with robust regional distribution. Rising indoor-air-quality testing requirements are steering developers toward water-borne acrylics, reinforcing the segment’s dominance within the UAE paints and coatings market. Turner & Townsend projects a tender-price inflation rate of 3.3% for 2025, supporting the uptake of premium specifications despite material-cost pressures.

Tourism-Led Demand for Hospitality Refurbishments

Dubai added 5,000 hotel keys in 2024, primarily in the five-star category, while Abu Dhabi added 500 keys, intensifying refurbishment cycles that require rapid-cure interior coatings and marine-grade exterior systems. International brands are mandating low-emission certifications, which in turn elevates demand for waterborne and specialty finishes. Caparol’s 35% year-over-year regional sales surge in 2024, driven by projects such as Rove Hotels and Six Senses The Palm, illustrates how premium, compliance-ready paints gain market traction.

Mandatory Green-Building Codes Driving Low-VOC Paints

Dubai’s Al Sa’fat system caps VOC content at 30 g/L for interior matt finishes, while Abu Dhabi’s Trustmark demands ISO 9001 compliance and bans heavy metals, effectively elevating entry barriers. Federal convergence is underway under the UAE National Air Quality Agenda 2031, signaling tighter future ceilings and reinforcing a shift toward water-borne formulations. Field studies report that oil-based coatings emit 30-times higher TVOC levels than water-based alternatives in UAE climates, strengthening the regulatory case for aqueous systems.

Smart-City Initiatives Fuelling Demand for Heat-Reflective Coatings

Abu Dhabi’s retrofit program has upgraded 8,000 buildings toward a 2030 target of 30,000, with cool roofs delivering 3.85% energy savings. Meanwhile, Dubai’s pilot pavements underscore the municipality's interest in reflective surfaces. The Dubai Building Code 2021 establishes Solar Reflectance Index thresholds that encourage developers to adopt high-performance reflective coatings. As the UAE targets net-zero emissions by 2050, thermally efficient paints move from an optional upgrade to a baseline material within the UAE paints and coatings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and isocyanate limits | -0.7% | UAE-wide, chiefly Dubai and Abu Dhabi | Medium term (2-4 years) |

| Volatile titanium-dioxide prices | -0.9% | UAE-wide | Short term (≤ 2 years) |

| Cyclical slowdown in Abu Dhabi awards | -0.5% | Abu Dhabi and spillover emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and Isocyanate Limits Increasing Compliance Costs

Federal Law No. 33/2021 mandates robust hazardous-substance controls, while Dubai requires EC Directive-aligned VOC caps and bans certain biocides, raising formulation, testing, and certification costs[2]Dubai Municipality, “Technical Guidelines for Paints and Varnishes,” dm.gov.ae. Annual surveillance testing and Dubai Central Laboratory audits can exceed AED 15,000 per product line, disproportionately impacting SMEs. As emirate-level rules converge under a federal framework, additional reformulation cycles loom, trimming margins for solvent-borne players within the UAE paints and coatings market.

Volatile Titanium-Dioxide Prices Squeezing Margins

TiO₂ price swings persisted through 2024 amid global supply disruptions, while freight costs more than doubled year-over-year, eroding profitability for UAE manufacturers that depend on imported pigments. Raw materials already account for roughly 60% of baseline construction costs, and fixed-price contract commitments limit the pass-through capacity. The concentration of global TiO₂ suppliers forces local producers to carry high inventories to ensure continuity, inflating working-capital requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Resins Sustain Leadership

Acrylic resins held a 58.31% share of the UAE paints and coatings market in 2025, driven by their superior UV resistance, rapid cure, and compliance with Dubai’s VOC thresholds of 30–100 g/L for interior work. The segment is projected to track a 3.78% CAGR to 2031, outpacing the overall UAE paints and coatings market. Alkyds remain relevant for exterior durability, while epoxies gain traction in Abu Dhabi’s industrial corridors where chemical resistance supersedes VOC concerns. National Paints expanded its acrylic lineup in 2024 with the introduction of the National Shield Travertine and Touchstone ranges, and the company published an Environmental Product Declaration for powder coatings, signaling a sector-wide emphasis on lifecycle transparency.

Premium acrylic systems also dominate high-rise façade refurbishments, where severe salt-spray exposure and temperature cycling are present. Silicone-modified variants and specialty urethanes retain niche status for coastal landmarks, but premium pricing limits penetration. Strategic investments in R&D by regional players such as Caparol and Asian Paints reinforce acrylic optimization for local climatic stresses, ensuring the resin’s continued leadership within the UAE paints and coatings market.

By Technology: Water-Borne Systems Accelerate on Compliance

Water-borne technology accounted for 71.55% of the UAE paints and coatings market in 2025 and is forecast to grow at a 4.02% CAGR through 2031. Interior projects favor these formulations to meet indoor-air-quality targets of ≤ 300 µg/m³ TVOCs and ≤ 0.08 ppm formaldehyde. A landmark residential study confirmed that water-borne paints release 30 times fewer emissions than oil-based analogs in local climates, cementing their dominance.

Beyond compliance, water-borne systems enable faster re-coat cycles, lower worker safety risks, and simplified waste treatment processes, aligning with federal HSE laws. Caparol’s solvent-free range, launched in 2024, contributed significantly to its 35% surge in Middle East sales. Solvent-borne coatings persist in niche exterior and industrial situations where Dubai permits up to 430 g/L VOC, but the trajectory remains downward as the UAE paints and coatings market moves toward consolidated emission ceilings by 2031.

By End User: Commercial Segment Outpaces Residential Growth

Residential demand accounted for 66.40% of the UAE paints and coatings market size in 2025, underpinned by the consistent delivery of approximately 35,000 housing units per year across Dubai and Abu Dhabi. Yet, commercial activity is growing at a faster rate, with a 3.71% CAGR through 2031, buoyed by hospitality refurbishments, office pipeline additions, and smart-city retrofits. Abu Dhabi’s plan to retrofit 30,000 buildings by 2030 is already 26% complete, driving sustained uptake of reflective and energy-saving coatings.

Five-star hotel upgrades in Dubai demand odor-free, quick-turnaround interior finishes and marine-grade exteriors, while office developers specify low-VOC systems to achieve WELL and LEED ratings. Smart-city requirements for Solar Reflectance Index compliance further expand demand for functional coatings within the UAE paints and coatings market. Suppliers offering bundled product-and-service models, including application training and performance warranties, are poised to capture incremental share from this value-rich segment.

Geography Analysis

Dubai and Abu Dhabi jointly account for most of the awarded contract value since 2020, cementing their status as prime demand centers in the UAE paints and coatings market. Dubai supports architectural demand through a USD 232 billion mixed-use pipeline and USD 125 billion residential backlog, while population targets of 5.8 million by 2040 expand long-term housing requirements. Abu Dhabi complements industrial and petrochemical projects, including ADNOC expansions, which sustain demand for protective and marine coatings even during periods of public spending pauses.

The Northern Emirates—comprising Sharjah, Ajman, and Ras Al Khaimah—are emerging as cost-sensitive yet high-volume zones. Sharjah’s manufacturing base hosts National Paints’ flagship facility and Jotun’s expanding retail network, ensuring close supply for regional contractors. Affordable housing drives, paired with incentives such as long-term visas, maintain a steady residential flow that bolsters baseline decorative volumes across the UAE paints and coatings market.

Fujairah and Umm Al Quwain are positioning themselves as manufacturing nodes. Dubai Industrial City’s 97% occupancy and recent AED 410 million land expansion confirm policy-led localization, reducing import reliance and enhancing supply-chain resilience throughout the UAE paints and coatings market.

Competitive Landscape

The UAE architectural paints and coatings market is moderately consolidated, with multinational giants and large regional firms sharing the field. Compliance capability and local test infrastructure outweigh mere pricing in bid evaluations, given Dubai Central Laboratory and Abu Dhabi Trustmark mandates. AkzoNobel leverages partnerships with the Kanoo Group to navigate the complexities of distribution and regulation. National Paints counters with a broad acrylic catalog and published EPDs, reinforcing sustainability credentials, while Caparol differentiates through solvent-free innovations and a robust technical-service network.

UAE Architectural Paints And Coatings Industry Leaders

Jotun

Hempel A/S

Caparol Paints

AkzoNobel N.V.

NATIONAL PAINTS FACTORIES CO. LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Jotun Paints UAE celebrated its 50th anniversary and launched its latest retail concept, ‘Unlock the Future,’ marking a new era in retail shopping, with interactive experiences and tailored advice.

- April 2025: AL PAINTURA Global Paint Services LLC, a key player in the premium paint sector, inaugurated its latest PROFITEC Paint Showroom in Dubai's Al Quoz Industrial Area 2. The showroom debut highlights PROFITEC Paint's distinguished lineup of premium German paints.

UAE Architectural Paints And Coatings Market Report Scope

Architectural paints and coatings include paints and coatings used for commercial purposes, such as office buildings, warehouses, retail convenience stores, shopping malls, and residential buildings. It also includes the coatings used in the new construction and remodeling of old houses.

The UAE architectural paints and coatings market is segmented by resin type, technology, end-user industry, and geography. By resin type, the market is segmented into acrylic, alkyl, polyurethane, epoxy, polyester, and other resin types (urethanes, etc.). By technology, the market is segmented into water-borne and solvent-borne. By end-user industry, the market is segmented into residential and commercial. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Other Resins (Silicone, Urethanes) |

| Water-borne |

| Solvent-borne |

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Other Resins (Silicone, Urethanes) | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Key Questions Answered in the Report

How large is the UAE paints and coatings market in 2026?

The UAE paints and coatings market size is USD 644.6 million in 2026.

What is the expected CAGR for UAE coatings to 2031?

The market is projected to log a 3.41% CAGR through 2031.

Which resin type holds the biggest share in UAE coatings?

Acrylic resins lead with 58.31% market share in 2025.

Why are water-borne coatings gaining ground in the Emirates?

Strict VOC and indoor-air-quality rules favor water-borne systems that emit far lower TVOCs.

Which end-user segment is expanding fastest?

Commercial applications, including hotels and smart-city retrofits, are growing at a 3.71% CAGR through 2031.

Page last updated on: