Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

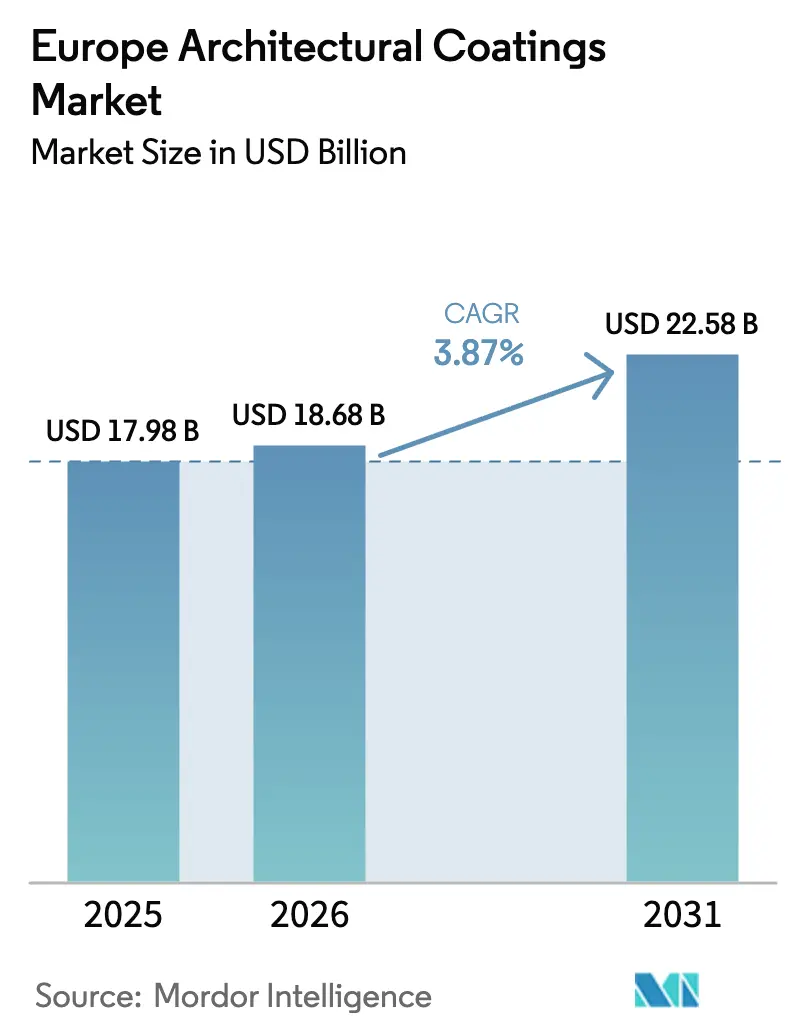

| Base Year Market Size (2025) | USD 17.98 Billion |

| Market Size (2026) | USD 18.68 Billion |

| Market Size (2031) | USD 22.58 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

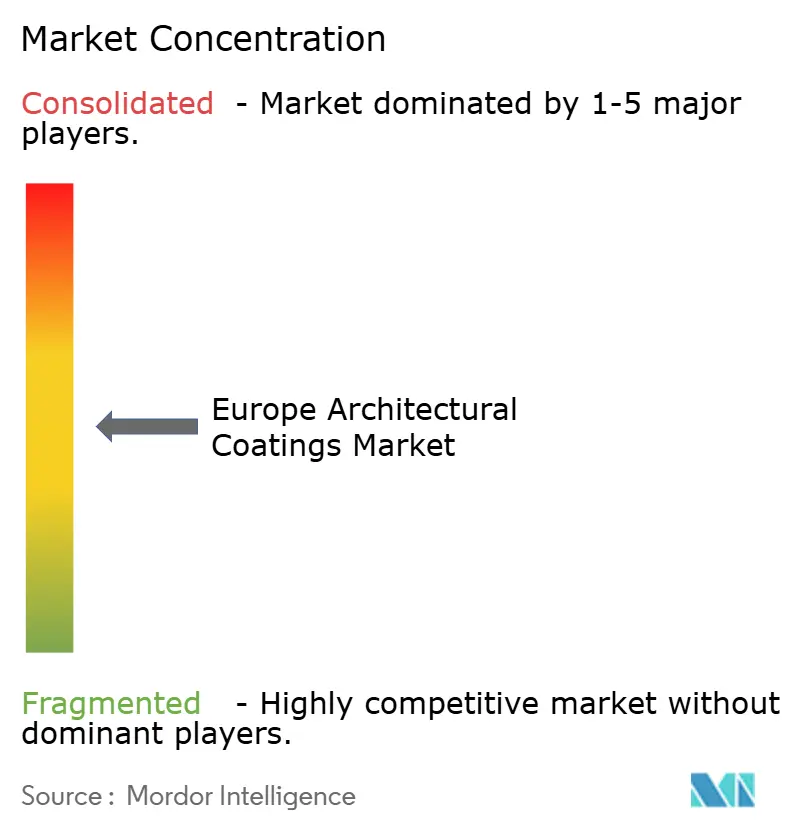

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Architectural Coatings Market Analysis by Mordor Intelligence

The Europe Architectural Coatings Market size is projected to grow from USD 17.98 billion in 2025 to USD 18.68 billion in 2026, and reach USD 22.58 billion by 2031, growing at a CAGR of 3.87% from 2026 to 2031. A measured pivot toward high-value, low-emission formulations has started to outweigh pure volume growth, as purchasers respond to tougher European Union VOC ceilings and a building stock whose average age now tops 50 years. Demand for waterborne systems already dominates because professional painters favor low-odor, easy-clean products, and retailers have delisted many solventborne lines to avoid compliance risk. Suppliers are also repositioning toward repair and refurbishment projects that promise steadier margins than new-build work, weakened by high borrowing costs. Consolidation among leading producers is accelerating in order to spread raw-material inflation, fund greener research and development pipelines, and strengthen go-to-market scale.

Key Report Takeaways

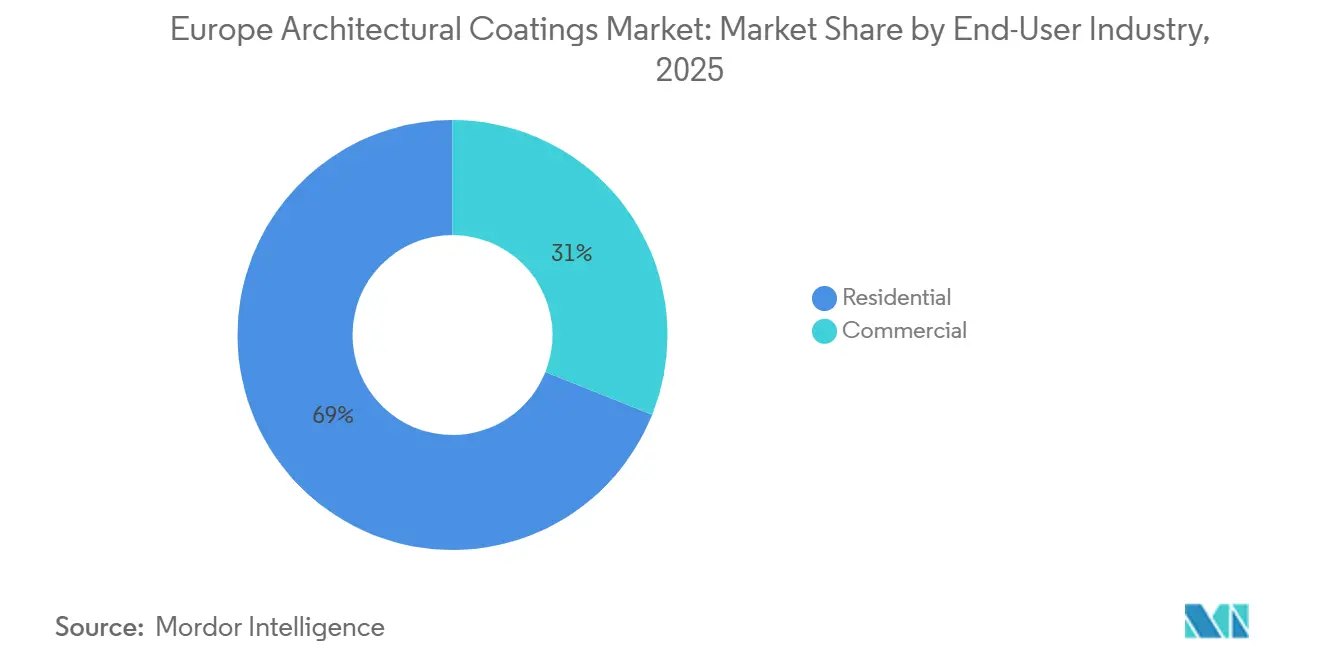

- By end-user industry, residential applications captured 68.96% of the Europe architectural coatings market size in 2025 and are expanding at a 4.04% CAGR to 2031.

- By technology, waterborne coatings led with 82.78% of the Europe architectural coatings market share in 2025 and are forecast to advance at a 4.24% CAGR through 2031.

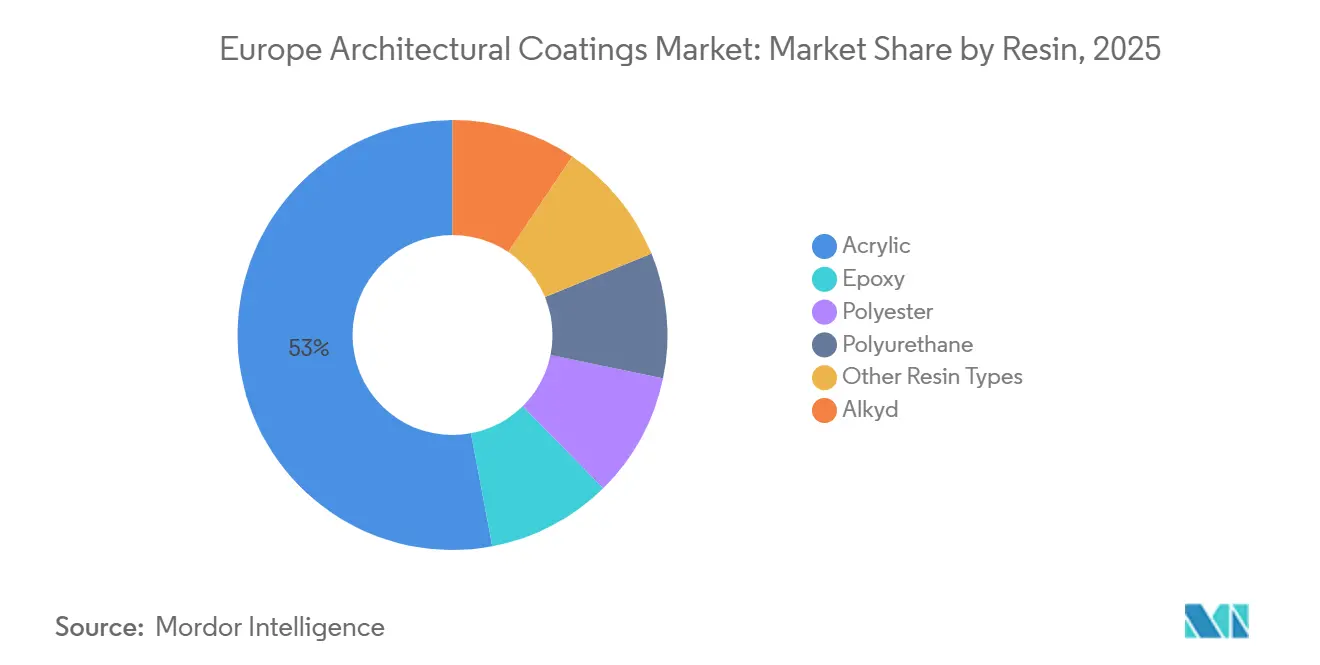

- By resin, acrylic platforms held 52.96% Europe architectural coatings market share in 2025 and are projected to grow at 4.17% to 2031.

- By geography, Russia accounted for 15.33% of regional revenue in 2025 while registering the fastest 4.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging housing-stock renovation boom | +1.2% | Western Europe (France, Germany, Italy, Spain, UK); Nordic countries | Medium term (2-4 years) |

| EU VOC regulations accelerating waterborne shift | +0.8% | EU27 plus UK (post-Brexit regulatory alignment); Norway, Switzerland | Long term (≥ 4 years) |

| Post-COVID rebound in commercial fit-outs | +0.5% | Urban centers (Paris, Berlin, Madrid, London); CEE capitals (Warsaw, Prague) | Short term (≤ 2 years) |

| Demand for energy-saving thermal-insulation paints | +0.6% | Northern Europe (Germany, Nordics, Poland); Southern Europe (Spain, Italy) | Medium term (2-4 years) |

| On-site tint-as-a-service platforms | +0.3% | Western Europe retail channels; expanding to CEE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Housing-Stock Renovation Boom

Europe counts more than 220 million dwellings built before 1990; many now require facade repair, moisture protection, and interior upgrades to meet modern health standards. Eurostat recorded EUR 310 billion spent on housing renovation in 2025, up 12% from the prior year[1]Directorate-General Environment, “Commission Decision Establishing EU Ecolabel Criteria for Paints and Varnishes,” ec.europa.eu. France, Germany, Italy, and Spain delivered 60% of that spending, with Italy alone surging 20% thanks to generous tax credits for energy-efficient coatings. The European Parliament wants to double annual renovation rates to 2% by 2030, lifting demand for durable acrylic and polyurethane finishes that extend repaint cycles from seven to twelve years. Consequently, the Europe architectural coatings market continues to rotate toward high-margin segments while sustaining steady headline growth.

EU VOC Regulations Accelerating Waterborne Shift

The European Commission updated EU Ecolabel rules in February 2026, lowering both VOC and SVOC caps and adding fitness-for-use tests that discourage binder dilution. Retailers quickly delisted non-compliant solventborne lines; by end-2025 waterborne products already formed 70% of decorative volume, up five points in five years[2]Staff Report, “European Decorative Coatings Shift Toward Waterborne,” coatingsworld.com. Pure acrylic emulsions now dominate interior walls, while styrene-acrylic blends migrate to budget exteriors. BASF, AkzoNobel, and Arkema validated bio-attributed resins that cut coating carbon footprints 40% during 2025 pilot runs. These moves confirm that tighter regulation not only accelerates waterborne uptake but also raises entry barriers for smaller formulators lacking research and development scale. As a result, the Europe architectural coatings market is tilting toward larger incumbents with science-based sustainability credentials.

Post-COVID Rebound in Commercial Fit-Outs

Office leasing across continental Europe climbed 8% in 2025, while hotel refurbishment orders jumped 15% in Mediterranean destinations. Owners refreshed interiors to entice hybrid workers and leisure travelers, demanding rapid-drying low-odor paints that allow overnight turnovers. Although overall commercial volumes still trail pre-pandemic highs, the mix has shifted toward premium ceiling and trim products specified for indoor-air-quality compliance. This niche favors suppliers offering zero-VOC, antibacterial, or formaldehyde-scavenging packages. Faster curing also helps contractors cope with scarce painter labor, a chronic issue in the Netherlands and Denmark. Hence, the commercial upswing, though modest in tonnage, delivers outsized value growth inside the Europe architectural coatings market.

Demand for Energy-Saving Thermal-Insulation Paints

Energy-price volatility has pushed property owners to seek passive efficiency upgrades. Thermal-insulation coatings using ceramic or aerogel fillers can lift wall R-values enough to cut HVAC bills 5-8% within three heating seasons. Germany’s KfW bank began reimbursing up to 20% of product cost for qualifying exterior systems in 2025, sparking strong adoption in pre-1990 buildings. Heritage sites embrace these thin-film solutions because conventional external insulation often violates preservation rules. Suppliers promoting quantifiable payback now secure specification in municipal retrofit tenders, broadening revenue streams. The trend is expected to carry a 0.6% positive swing for the Europe architectural coatings market CAGR through 2031.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Titanium-dioxide and petro-feedstock price volatility | -0.7% | Pan-European (all markets); acute in import-dependent Southern Europe | Short term (≤ 2 years) |

| High interest rates dampening new-build housing | -0.9% | Germany, UK, France, Nordic countries; limited impact in Poland, Spain | Medium term (2-4 years) |

| Professional painter labor shortages | -0.5% | Northern Europe (Netherlands, Denmark, Germany); emerging in France, Poland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Titanium-Dioxide and Petro-Feedstock Price Volatility

Spot TiO₂ hovered between EUR 2,800 and EUR 3,400 per ton in 2025, a 21% swing that squeezed gross margins for mass-market interior emulsions. Producers offset part of the spike with extender pigments and composite opacifiers, yet these substitutions risk reduced scrub resistance or color fidelity at higher tint levels. Simultaneously, acrylic-monomer costs tracked Brent crude, which ranged from USD 75 to USD 95 per barrel. Because EU duties keep cheap Chinese TiO₂ out of the bloc, local formulators face a persistently high cost floor relative to Asian rivals.

High Interest Rates Dampening New-Build Housing

European Central Bank rates peaked at 4.0% in mid-2024 and still sit at 3.5% in 2026, eroding mortgage eligibility for first-time buyers. Germany recorded a 12% year-on-year drop in housing completions during 2025, and the UK slipped 8%. Lower construction starts curb demand for economy-grade wall primers typically applied in new apartments. While renovation activity partly compensates, it favors lower-volume premium lines, muting total literage growth. Analysts expect a gentle rate-cut cycle from late 2026; until then, high borrowing costs shave almost one point off the underlying expansion of the Europe architectural coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Residential Activity Anchors Growth

Residential projects generated 68.96% of 2025 revenue and will climb at a 4.04% CAGR through 2031. Renovation dominates because owners must preserve asset value in an aging building stock, and national tax credits now reimburse up to 30% of energy-saving exterior paint costs. Italy led spending with a 20% uptick in 2025 after enhancing its Eco-Bonus scheme. Consumers increasingly specify low-odor paints carrying asthma-allergy labels, and anti-scuff interior emulsions advertised to last a decade between coats. That dynamic lifts average selling prices even as liters per dwelling shrink.

Commercial applications are also witnessing increasing demand for architectural coatings. Offices are adapting to hybrid work, which trims square footage requirements by roughly 15%. Yet hotel, healthcare, and education refurbishments have accelerated, each demanding fast-dry zero-VOC or antimicrobial coatings to minimize disruption. The segment relies on supply partners able to stage rapid weekend repaints, a service advantage mid-tier regional brands exploit. Nonetheless, volume recovery remains uneven across Europe; Spain posts double-digit hospitality gains, whereas Germany’s office pipeline stalls under financing constraints.

By Technology: Waterborne Dominance Strengthens

Waterborne systems accounted for 82.78%, or USD 14.89 billion, of the Europe architectural coatings market share in 2025 and are forecast to advance at a 4.24% CAGR to 2031. Updated ecolabel limits, together with retailer delisting, leave solventborne alkyds with shrinking niches. Meanwhile, advances in coalescent chemistry have closed adhesion gaps on porous masonry, enabling pure acrylic emulsions to promise 10-year exterior life. Suppliers also upgrade waterborne trim enamels with blocking and leveling agents to meet professional brushability standards, once monopolized by oil-based paints.

Solventborne volumes are still witnessing a considerable growth rate because certain metal priming and heritage-wood applications still require cross-link density unattainable in water. Innovation now centers on hybrid alkyd-in-water dispersions that retain traditional appearance while emitting under 30 g/L VOC. The outcome is a gradual fade rather than a rapid cliff, yet every year the solventborne slice thins, reinforcing the structural ascendancy of waterborne technology inside the Europe architectural coatings market.

By Resin: Acrylic Systems Extend Lead

Acrylic resins underpinned 52.96% of 2025 revenue, giving them more than half of the total Europe architectural coatings market share, and they are rising at 4.17% to 2031. Pure acrylic binders deliver flexibility, UV stability, and low-temperature film formation that suit both interior and exterior uses. As waterborne adoption expands, acrylic consumption climbs in lockstep. Premium masonry brands advertise 12-year warranties based on pure acrylic technology, enabling 20-30% price premiums relative to styrene-acrylic blends.

Alkyd volumes erode 1-2% annually as architects drop traditional gloss enamels in favor of waterborne urethane-modified alternatives. Polyurethane and epoxy resins, while expensive, gain share in high-traffic corridors and hospital floors where chemical resistance matters. EU-funded PERFECOAT and BIO4COAT projects proved bio-based acrylic feasibility above 25% renewable content in 2024 trials. Commercial scale-up expected by 2028 positions acrylic chemistry to retain leadership while meeting decarbonization targets, solidifying its central role in the Europe architectural coatings market.

Geography Analysis

Russia produced 15.33% of the 2025 turnover and is projected to expand at 4.38%, outpacing all European peers. Federal infrastructure budgets shielded its construction sector from broader Continental slowdowns, and import substitution policies favor domestic coating brands supplied by multinational joint ventures. Germany remains the largest national market but saw a 12% drop in new-build apartments during 2025. That contraction diverted demand toward refurbishment, which skews toward long-life exterior systems and higher-margin interior matte paints. France and Spain weathered rate hikes better because renovation incentives offset weaker mortgages; each logged 8-10% renovation spend growth.

The Nordic bloc, including Sweden, Denmark, Finland, and Norway, contributes a smaller volume yet commands some of the highest average prices thanks to strict ecolabel norms. Denmark reported 86.7% of contractors short on painters in 2025, spurring sales of single-coat high-hide products that reduce labor hours. Finland’s coastal climate also supports niche demand for ice-resistant facade coatings used on offshore infrastructure.

Central and Eastern Europe, including the Czech Republic, Slovakia, Romania, and the Western Balkans, offers white-space potential. Household purchasing power is climbing, yet value brands still dominate shelf space. Mid-tier Western suppliers are moving in with training academies and tint-center rollouts that introduce eco-label products at affordable price points. As these countries transpose updated EU building directives, demand will migrate toward compliant waterborne acrylics, enlarging the addressable base of the Europe architectural coatings market over the next five years.

Competitive Landscape

The Europe architectural coatings market is moderately consolidated. AkzoNobel’s proposed USD 25 billion merger with Axalta would create a scale player capable of negotiating titanium-dioxide contracts on near-integrated producer terms. Innovation themes converge on sustainability and productivity. BIO4COAT partners test bio-based polyurethanes and diamond-like carbon finishes to lower embodied carbon 20%. Hempel’s Crown Paints leverages Farrow & Ball’s color authority to trade consumers up into premium price tiers. With ESG due-diligence tight, larger groups consolidate to shoulder the compliance cost burden, while niche players win by addressing heritage restoration, antimicrobial interiors, or ultra-low-VOC categories that mainstream portfolios overlook.

Europe Architectural Coatings Industry Leaders

AkzoNobel N.V.

DAW SE

PPG Industries, Inc.

The Sherwin-Williams Company

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Evonik launched Protectosil ECO-TRETE ANTIGRAFFITI, a PFAS-alternative silane product for urban facades, showcased at EUROCOAT in Paris.

- February 2026: The European Commission issued updated EU Ecolabel criteria for paints and varnishes, adding stricter VOC and SVOC thresholds and new circularity rules.

Europe Architectural Coatings Market Report Scope

Architectural coatings are specialized products designed for application on residential and commercial buildings to deliver aesthetic appeal, weather resistance, and long-term durability. These coatings protect structures from moisture, UV radiation, and corrosion, while enhancing the visual appearance of both interior and exterior surfaces.

The Europe architectural coatings market is segmented by end-user industry, technology, resin, and geography. By end-user industry, the market is segmented into commercial and residential. By technology, the market is segmented into solventborne and waterborne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. The report also provides market sizing and forecasts for seven major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By End-User Industry

| Commercial |

| Residential |

By Technology

| Solventborne |

| Waterborne |

By Resin

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By Geography

| France |

| Germany |

| Italy |

| Nordic Countries |

| Poland |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By End-User Industry | Commercial |

| Residential | |

| By Technology | Solventborne |

| Waterborne | |

| By Resin | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By Geography | France |

| Germany | |

| Italy | |

| Nordic Countries | |

| Poland | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms