Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

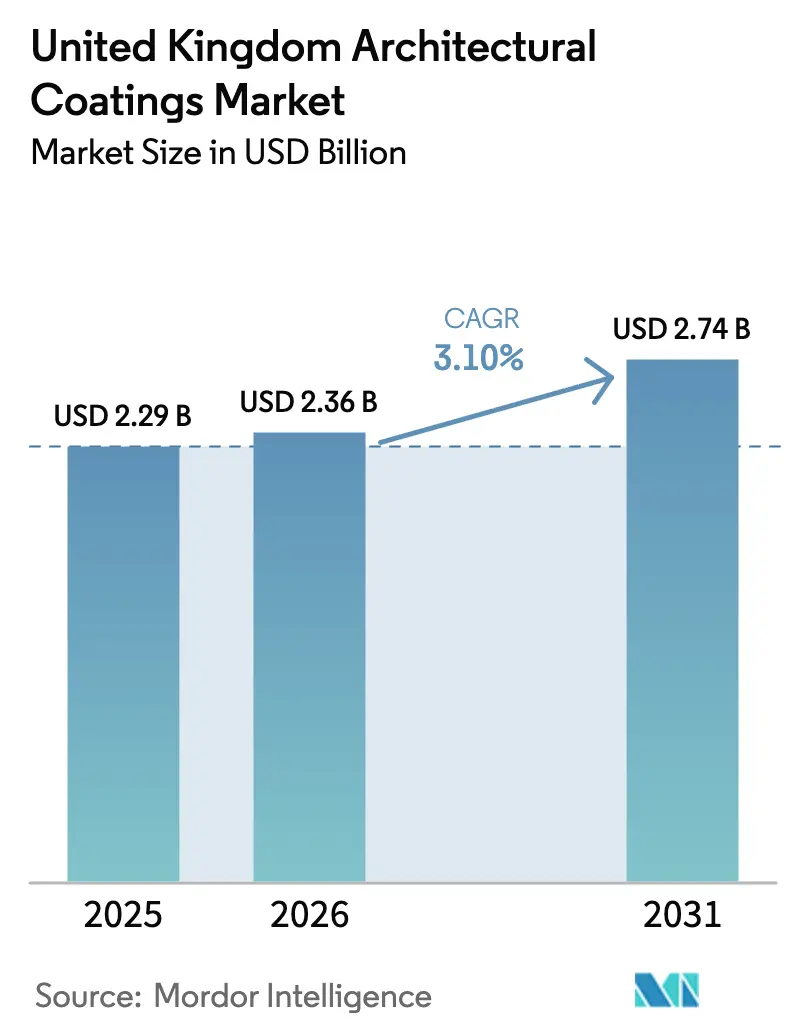

| Base Year Market Size (2025) | USD 2.29 Billion |

| Market Size (2026) | USD 2.36 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 3.10% CAGR |

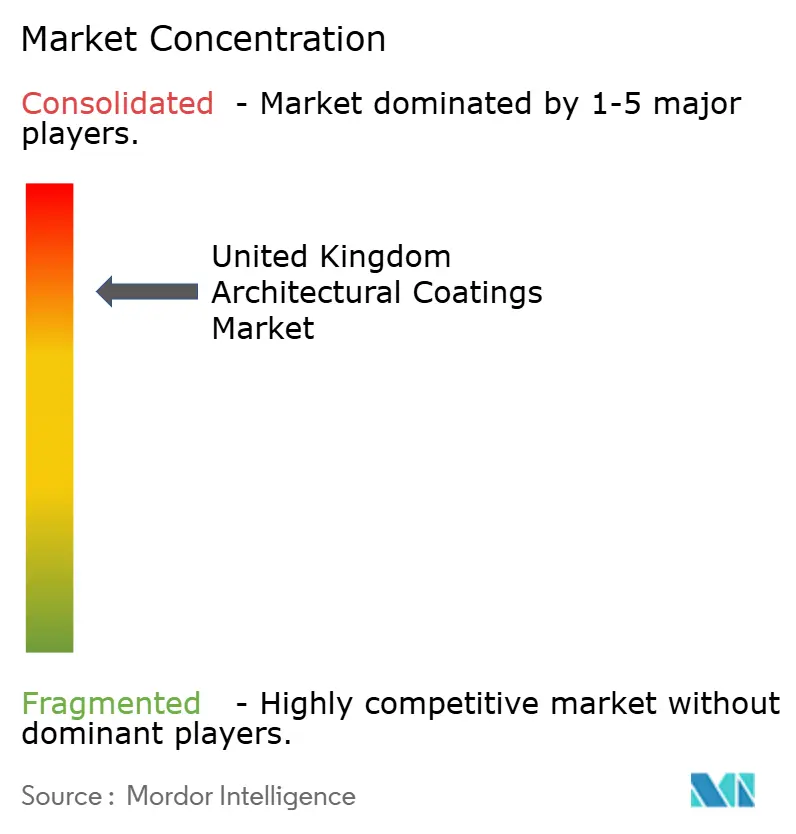

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Architectural Coatings Market Analysis by Mordor Intelligence

The United Kingdom Architectural Coatings Market size is expected to grow from USD 2.29 billion in 2025 to USD 2.36 billion in 2026 and is forecast to reach USD 2.74 billion by 2031 at 3.10% CAGR over 2026-2031. Demand is anchored in steady renovation activity, a resilient repair and maintenance subsector, and a widening preference for low-odor, quick-drying finishes. At the same time, raw-material cost swings—especially in titanium dioxide—compress margins, pushing large manufacturers toward vertical integration or multi-year supply contracts. Shortages of skilled applicators restrict throughput on commercial projects yet inadvertently boost DIY retail sales as households take on tasks once handled by professionals. Competitive focus, therefore, centers on improving water-based durability, simplifying application for non-professionals, and embedding verified carbon-reduction attributes to meet tightening green-building criteria.

Key Report Takeaways

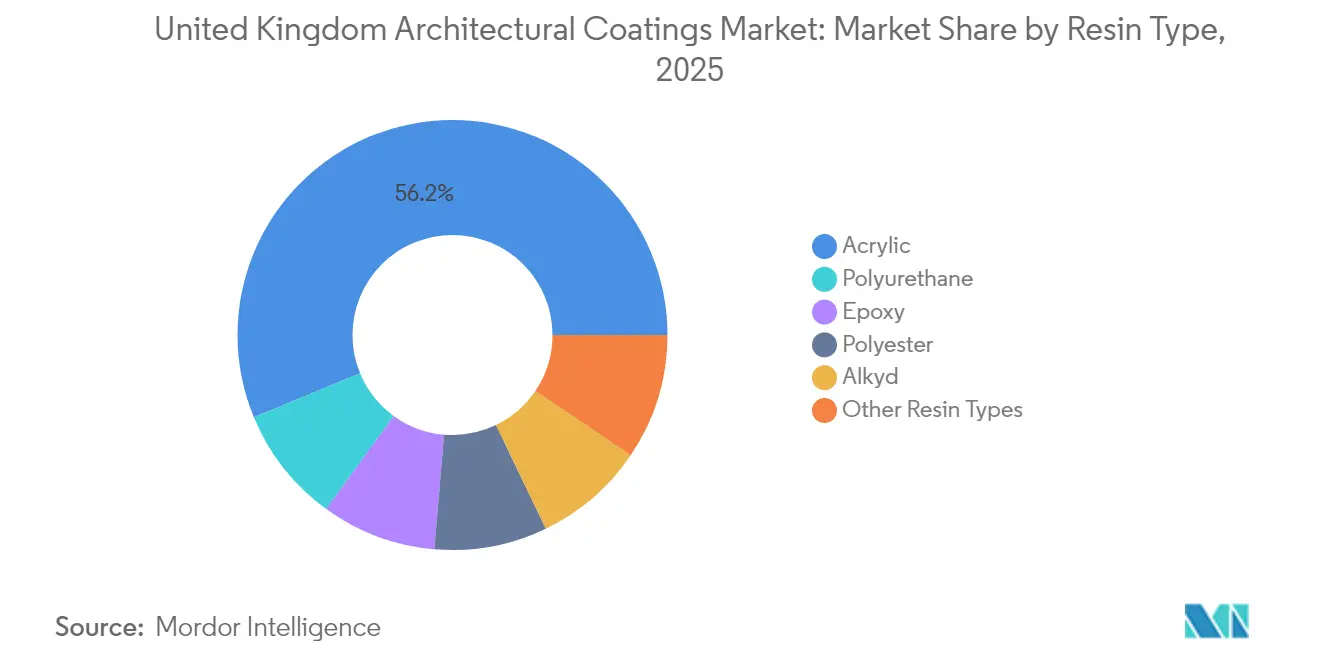

- By resin type, acrylic captured 56.25% of value in 2025 while recording the fastest 3.70% CAGR outlook to 2031.

- By technology, water-borne systems held 86.70% share in 2025, expanding at a 3.35% CAGR over the forecast horizon.

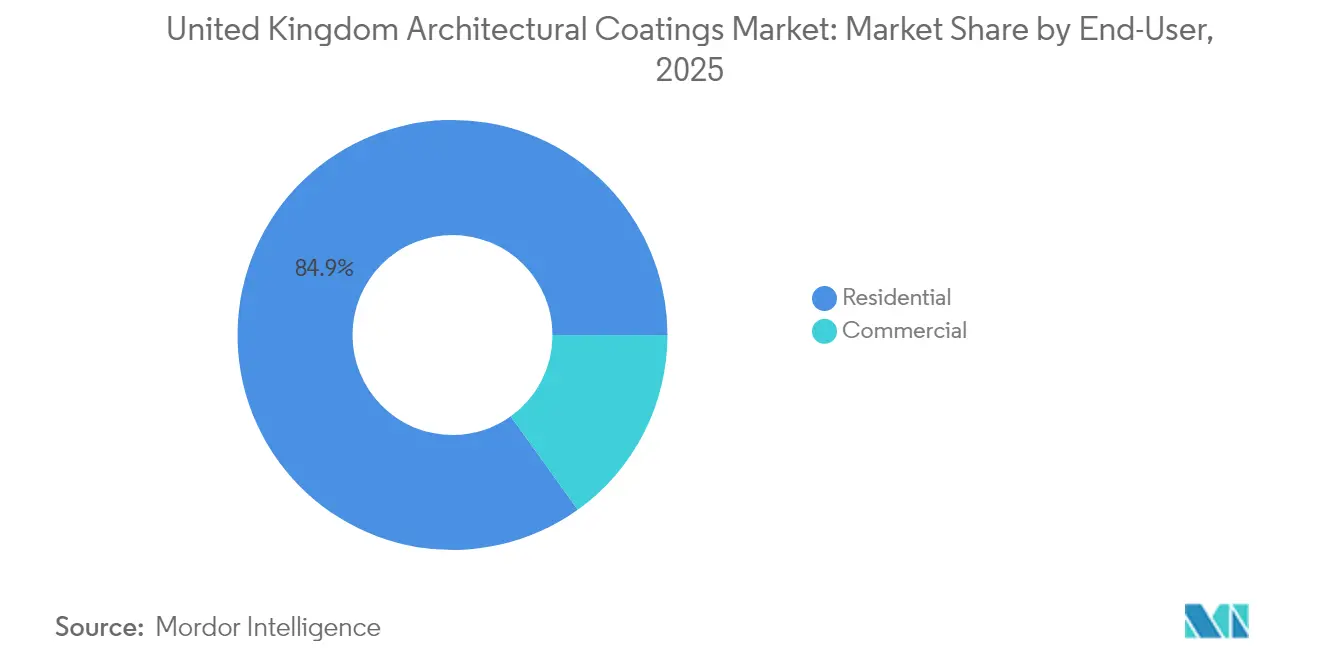

- By end-user, residential applications represented 84.90% of demand in 2025 and are projected to advance at a 3.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push toward water-/low-VOC systems | +0.8% | National; strongest in urban areas | Long term (≥ 4 years) |

| Post-pandemic DIY and renovation boom | +0.6% | National; higher in suburban regions | Medium term (2-4 years) |

| Net-zero/green-building incentives | +0.5% | National; early gains in London, Manchester, Edinburgh | Long term (≥ 4 years) |

| Heritage-property demand for mineral paints | +0.3% | Historic city centers | Medium term (2-4 years) |

| Off-site modular construction adoption | +0.4% | Scotland and Northern England | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push Toward Water-/Low-VOC Systems

The Building Safety Act 2022 enforcement has made compliance with the 2012 VOC regulations non-negotiable, propelling waterborne technology to 87.28% of the volume[1]UK Government, “The Volatile Organic Compounds in Paints, Varnishes and Vehicle Refinishing Products Regulations 2012,” legislation.gov.uk . Companies now invest roughly GBP 150,000 per year to retrofit lines, update testing protocols, and verify performance under lower solvent thresholds. Because the United Kingdom architectural coatings market must still align with EU chemical standards to preserve export access, non-compliant imports face costly re-testing at the border, deterring low-cost entrants. Advanced acrylic emulsions achieve VOC levels below 30 g/L, letting brands charge premium prices to contractors seeking BREEAM credits. As BREEAM Version 7 pushes stricter indoor-air benchmarks, manufacturers emphasizing verified M1 emission classifications enjoy priority listing on large commercial specifications.

Post-Pandemic DIY and Renovation Boom

Households spent more on home improvement in 2024, with decorative paints the leading retail item. Remote work has become permanent for many white-collar staff, creating ongoing demand for refreshed interiors rather than one-off pandemic fixes. DIY outlets reported an increase in waterborne sales, thanks to low-odor attributes and short re-occupancy times. Skilled applicator shortages have unintentionally led consumers to opt for self-application, resulting in increased demand for easy-roll and drip-resistant finishes. Government retrofit schemes, such as the GBP 500 million Warm Homes Local Grant, accelerate the use of specialty topcoats for insulated façades, reinforcing upward momentum in the United Kingdom's architectural coatings market.

Net-Zero/Green-Building Incentives

The 2050 net-zero pledge cascades down to building codes, with local authorities already imposing carbon targets that exceed Part L minimums. BREEAM points tied to Environmental Product Declarations reward coatings that disclose cradle-to-grave emissions, nudging specifiers toward suppliers with mature LCA capabilities. The GBP 3.8 billion Social Housing Decarbonisation Fund directs retrofit spending at external wall systems that require breathable yet weather-resistant finishes. This shift kindles interest in bio-based resins; a few formulations now integrate 25% plant-derived monomers while still meeting abrasion and scrub-resistance benchmarks. Manufacturers able to pair verified low-carbon footprints with proven durability stand to capture the fastest-growing niches within the United Kingdom architectural coatings market.

Heritage-Property Restoration Demand for Breathable Mineral Paints

Roughly 374,000 listed buildings depend on coatings that allow masonry to “breathe” without trapping moisture[2]Historic England, “Listed Buildings Statistical Report 2024,” historicengland.org.uk . Projects in 10,000 designated conservation areas, therefore specify lime-based or silicate paints that achieve permeability rates above 200 g/m²/24 h. The GBP 95 million Heritage Action Zones program funnels public money into high-street regeneration, clustering demand for traditional pastel palettes and matte finishes. Coating producers that bundle product training with supply can cement loyalty in this protection-heavy segment of the United Kingdom architectural coatings market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (TiO₂, resins) | -0.9% | National; higher impact on SMEs | Short term (≤ 2 years) |

| Tightening VOC and biocide rules | -0.4% | Specialty segments nationwide | Medium term (2-4 years) |

| Skilled-applicator shortage | -0.6% | London and South East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (TiO₂, Resins)

Titanium dioxide is squeezing gross margins by as much as 400 basis points for firms lacking multi-year supply deals. Acrylic resin outlays rose in the same period, driven by energy shocks and logistical bottlenecks. Because raw inputs account for up to 70% of the cost of goods sold, every 5% price swing directly impacts operating profit. Brexit-driven customs paperwork adds a further 3-5% burden to imported resins, hitting small and mid-size enterprises hardest. The result is aggressive portfolio rationalization and surcharges across the United Kingdom architectural coatings market until pricing stabilizes.

Tightening VOC and Biocide Rules Raise Compliance Cost

Regulators are phasing in tougher indoor-air thresholds and stricter limits on in-can preservatives. Reformulation runs parallel with expensive analytical testing, lengthening time-to-market for niche lines. Specialty coatings that once relied on higher solvent content must now find water-based replacements, sometimes compromising unique aesthetic or performance traits. Smaller brand owners either exit these categories or partner with toll manufacturers, altering the competitive landscape of the United Kingdom architectural coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Drives Innovation

Acrylic commanded 56.25% of the United Kingdom architectural coatings market share in 2025 and is projected to expand at a 3.70% CAGR to 2031. The United Kingdom architectural coatings market size tied to acrylic systems, therefore, climbs steadily as contractors and homeowners embrace their low-odor, fast-drying nature. Innovation centers on coalescent-efficient emulsions that deliver less than 30 g/L VOCs without sacrificing block resistance.

Alkyd shares continue to decline as modern water-based hybrids rival the traditional gloss of solvent-rich enamels. Polyurethane maintains its foothold in kitchens and healthcare spaces, while epoxy remains confined to heavy-duty flooring due to hurdles associated with amine-linked labeling. Bio-based acrylics feature up to 25% renewable content, enabling brands to highlight carbon reductions without compromising performance. Resin selection is increasingly influenced by REACH compliance costs, prompting formulators to opt for chemistries with lower regulatory burdens.

By Technology: Water-Borne Systems Reshape Market Dynamics

Water-borne products captured 86.70% of revenue in 2025, backed by a 3.35% CAGR outlook that sustains their overwhelming lead. This share translates into the largest slice of the United Kingdom architectural coatings market size, forcing even niche players to prioritize aqueous development pipelines.

Early water sensitivity once dogged these coatings, but advances in ambient-temperature film formation and early block resistance now allow contractors to re-coat within hours, a boon on fast-track projects. Solvent-borne offerings survive mainly in specialist roles: extreme facades, tannin-rich substrates, or heritage gloss enamels. The Building Safety Act’s indoor-air clauses will likely push those applications further into water-reducible territory, cementing the segment’s dominance.

By End-User: Residential Segment Sustains Market Leadership

Residential applications accounted for 84.90% of the 2025 value and are expected to continue at a 3.28% CAGR through 2031, underscoring their pivotal role in the United Kingdom architectural coatings market. Remote work keeps focus on home interiors, where repeat painting of living and office nooks drives volume.

DIY retail now captures a larger slice as consumers compensate for applicator shortages. Commercial new-build projects lag muted office absorption, but hospitality remodeling provides pockets of growth. Retrofit programs in social housing channel demand toward breathable yet weatherproof exterior solutions, offering a steady volume even when discretionary spending cools.

Geography Analysis

London and the South East account for a major part of the United Kingdom's architectural coatings market in 2024, reflecting a dense housing stock, high refurbishment budgets, and a concentration of commercial fit-outs. Premium brands prosper here thanks to homeowners willing to pay for low-odor, designer-color lines that minimize downtime in occupied dwellings. Yet, the same region bears the brunt of the applicator shortfall, which extends lead times and raises project costs.

Demand in Scotland is driven by a commitment to deliver 110,000 affordable homes by 2032 and a policy shift toward off-site manufacturing, which favors factory-applied finishes. Apprenticeship schemes seed a rising talent pool of painters, alleviating labor bottlenecks seen in England’s south. Northern England gains momentum from urban-regeneration grants, where heritage façades demand mineral paints tailored to high-permeability masonry.

Wales advances in tourism-led infrastructure upgrades and rural housing developments that require robust exterior coatings capable of withstanding the harsh coastal weather conditions. Sustainability mandates echo the national push, encouraging the adoption of water-borne formulations even in traditionally solvent-leaning marine resorts. Northern Ireland, meanwhile, benefits from smoother trade flows post-Windsor Framework, enabling competitive pricing through cross-border supply chains despite lingering customs complexity.

Competitive Landscape

The United Kingdom architectural coatings industry is consolidated. Multinationals possess brand equity, nationwide distribution, and substantial research and development budgets, whereas regional specialists specialize in niche markets such as heritage or custom colors. Volatile raw-material costs prompt larger firms to secure multi-year titanium dioxide contracts or explore backward integration. Innovation pipelines focus on bio-based resins, low-temperature cure powders, and digital color-matching platforms that reduce client approval cycles. Private-equity funds are eyeing mid-tier players that can bridge the consumer and trade channels, anticipating value creation through operational upgrades and e-commerce expansion. Despite margin compression, sustained renovation demand and regulatory tailwinds are expected to keep the United Kingdom architectural coatings market on a stable growth path.

United Kingdom Architectural Coatings Industry Leaders

Akzo Nobel N.V.

Hempel A/S

PPG Industries, Inc.

DAW SE

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Akzo Nobel N.V., Arkema, and BASF cut the carbon footprint of Interpon D architectural powder coatings by 40%, leveraging bio-attributed inputs and supplier-specific product carbon footprint (PCF) data.

- March 2025: Hempel unveiled Hempafire Extreme 550, a solvent-free epoxy passive fire protection (PFP) coating that delivers up to 4-hour fire resistance with a 40% lower CO₂ output.

United Kingdom Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms