Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

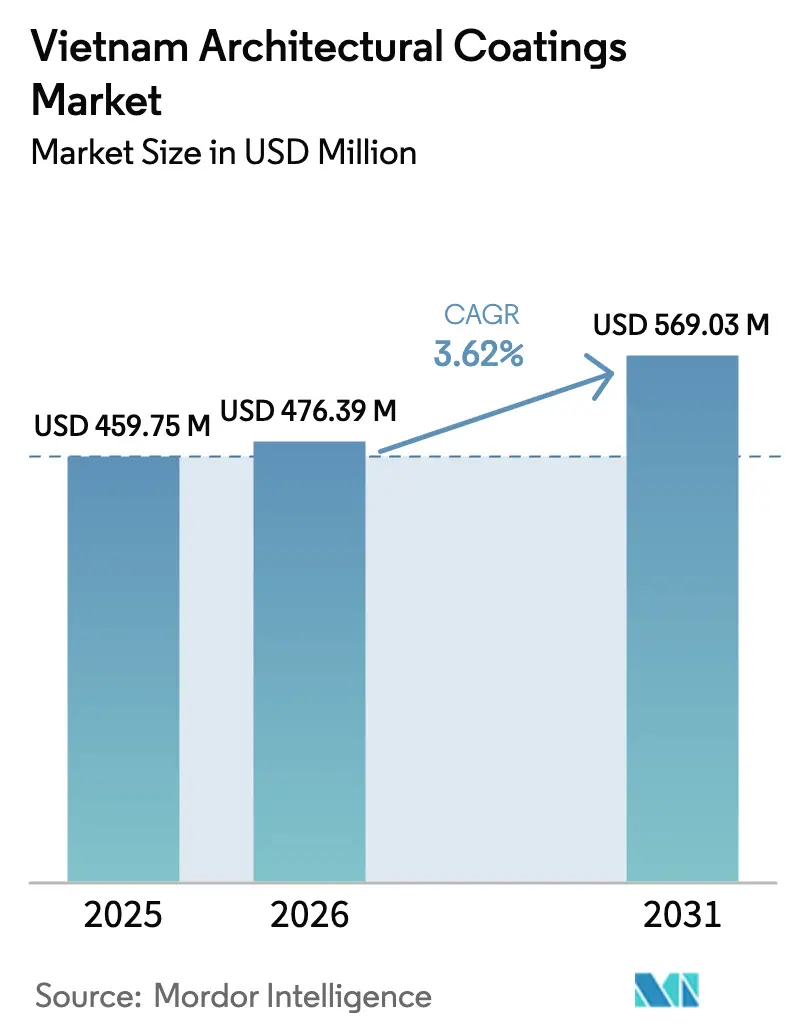

| Base Year Market Size (2025) | USD 459.75 Million |

| Market Size (2026) | USD 476.39 Million |

| Market Size (2031) | USD 569.03 Million |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Architectural Coatings Market Analysis by Mordor Intelligence

The Vietnam Architectural Coatings Market size in 2026 is estimated at USD 476.39 million, growing from 2025 value of USD 459.75 million with 2031 projections showing USD 569.03 million, growing at 3.62% CAGR over 2026-2031. Record foreign direct investment (FDI) of USD 25.35 billion in 2024 further underpins new starts across housing, retail, hospitality, and light manufacturing. Water-borne technology already commands nearly four-fifths of the Vietnam architectural coatings market thanks to tightening total volatile organic compound (TVOC) limits, yet solvent-borne systems still achieve the fastest expansion as developers specify high-performance finishes for weathered façades and intensive foot-traffic areas. Acrylic resins lead by volume, but polyurethane grades grow quickest as specifiers look for longer repaint cycles in the country’s tropical climate. Competitive intensity remains high, with AkzoNobel, Nippon Paint, PPG, and domestic champion KOVA Group all adding local capacity, embracing digital channels, and rolling out anti-counterfeiting safeguards to defend share in the price-sensitive Vietnam architectural coatings market.

Key Report Takeaways

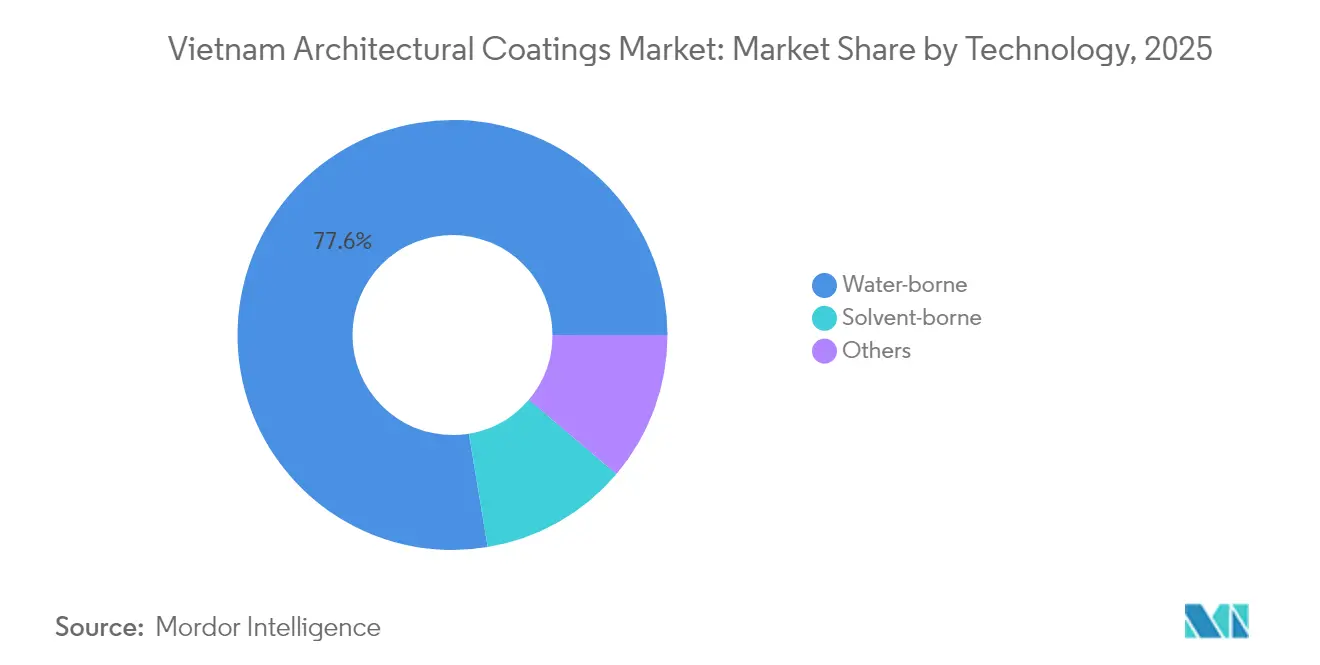

- By technology, water-borne formulations captured 77.62% of the Vietnam architectural coatings market share in 2025, whereas solvent-borne lines are projected to post a 3.92% CAGR through 2031.

- By resin type, acrylic systems held 41.88% of the Vietnam architectural coatings market size in 2025, while polyurethane grades are forecast to expand at a 4.05% CAGR to 2031.

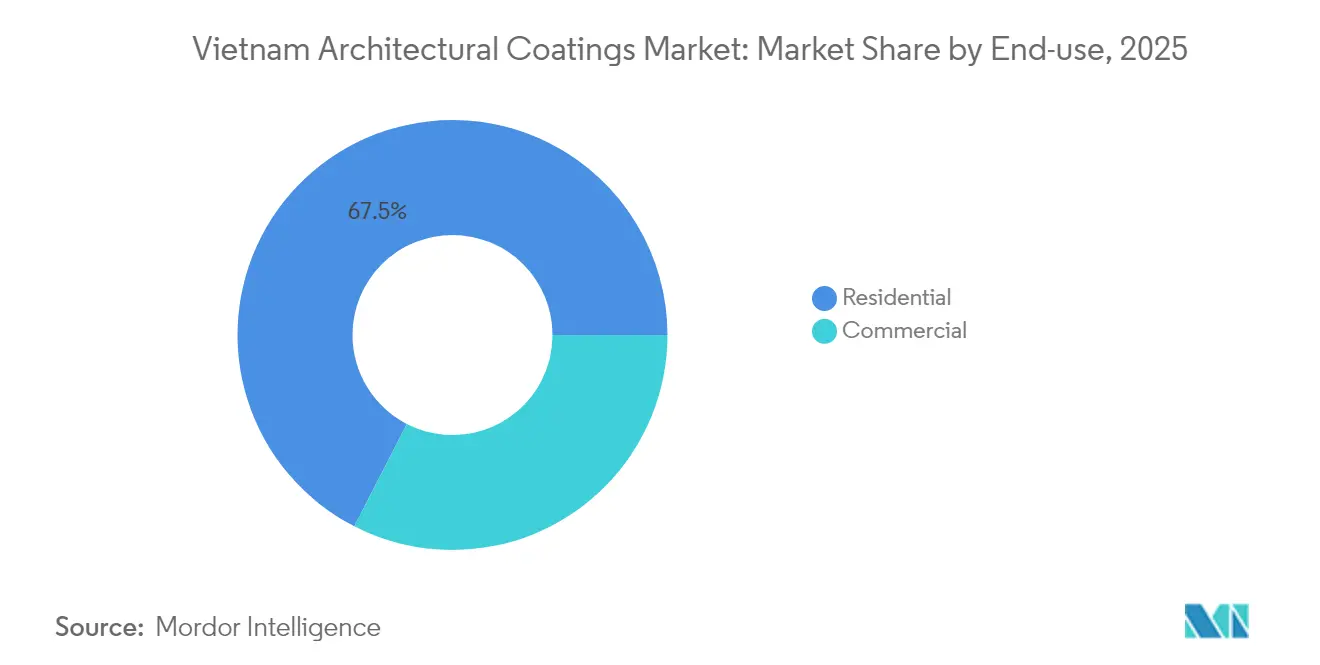

- By end-use, the residential segment accounted for 67.45% of the Vietnam architectural coatings market size in 2025; commercial construction is advancing at a 4.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming residential construction and urban housing demand | +1.2% | Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Government incentives for green and low-VOC buildings | +0.8% | Nationwide, major cities lead | Long term (≥ 4 years) |

| Rising disposable income driving remodeling and DIY paints | +0.6% | Tier-1 and Tier-2 urban centers | Short term (≤ 2 years) |

| FDI-led expansion of retail, hospitality and tourism assets | +0.9% | Economic zones nationwide | Medium term (2-4 years) |

| Digital D2C paint platforms shortening supply chains | +0.4% | Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming Residential Construction and Urban Housing Demand

Housing remains the single largest outlet for the Vietnam architectural coatings market. Ho Chi Minh City alone plans to release 50,000 new apartments in 2025 across 17 projects, while suburban provinces such as Binh Duong, Dong Nai, and Long An are absorbing mid-priced developments that widen the geographical footprint for mass-market interior and exterior paints. Premium apartments priced above USD 8,000 per m² in District 1 channel demand toward higher-end, stain-resistant, and colorfast coatings. The robust pipeline is backed by VND 661 trillion in executed public infrastructure during 2024, ensuring sustained coatings consumption for communal facilities, façades, and ancillary works.

Government Incentives for Green and Low-VOC Buildings

Vietnam’s 2050 net-zero pledge accelerates adoption of low-VOC formulations across the Vietnam architectural coatings market. More than 400 projects totaling 10 million m² have secured LEED, EDGE, Green Mark, or domestic Lotus certification—already far exceeding the national 2025 target of 80 buildings. The Ministry of Construction is drafting mandatory green-building specifications that will embed low-emission criteria into permits, giving an explicit advantage to water-borne and powder products. Demonstration cases such as Jotun’s LEED-Gold industrial complex, which achieved a 73.6% energy-cost reduction, offer proof of concept to developers weighing the return on sustainable finishes

Rising Disposable Income Driving Remodeling and DIY Paints

Home-improvement studies show coatings rank as the most frequently purchased category for interior upgrades, with purchase intent peaking in the 2024 holiday season[1]Home Improvement Research Institute, “2024 Consumer Spending Patterns,” hiri.org. Urban households increasingly favor low-odor, health-orientated formulations, aligning with water-borne acrylic and natural ingredient lines. Retailer Mr. DIY’s rapid rollout, five megastores opened inside one month, illustrates budding appetite for organized do-it-yourself retail, while omnichannel chains such as Paintmart combine digital color tools, click-and-collect, and home delivery that reduce friction for end users. Manufacturers capitalize through contractor-loyalty apps like Seamaster’s “Pro Painter,” further tightening the supply chain around the Vietnam architectural coatings market.

FDI-Led Expansion of Retail, Hospitality, and Tourism Assets

Record-high FDI, up 9.4% YoY in 2024, bankrolls premium malls, resorts, and manufacturing campuses that specify technologically advanced coatings. The USD 1.5 billion Trump Organization resort in Hung Yen Province targets five-star finishes across villas, hotels, and recreational structures for its 2027 launch. T&T Group’s VND 2,300 billion DoubleTree by Hilton in the Mekong Delta marks the first international five-star presence in the region, bringing high-performance, salt-spray-resistant exterior systems to a coastal climate[2]Thời Báo Tài Chính Việt Nam, “T&T Group khởi công xây dựng khách sạn 5 sao,” tbtco.vn. Retail complexes such as Vincom Mega Mall Grand Park in Ho Chi Minh City expand leasable area for decorative interior paints while sustaining after-hours foot traffic that necessitates abrasion-resistant flooring topcoats.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and resin prices squeezing margins | -0.7% | Global supply chain impacts, affecting all regions | Short term (≤ 2 years) |

| Stricter VOC caps adding compliance costs | -0.5% | National, industrial zones prioritized for enforcement | Medium term (2-4 years) |

| Counterfeit paints undermining premium brands | -0.3% | National, concentrated in secondary distribution channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC Caps Adding Compliance Costs

National regulation QCVN 19:2024/BTNMT enters force July 2025 and sets TVOC limits of 50–100 mg/Nm³ for spray-booth exhaust, obliging coating plants to install monitoring and possibly regenerative thermal oxidizers. Compliance expenses will squeeze margins for solvent lines and may accelerate a shift toward water-borne or powder offerings, especially where projects must file environmental-impact assessments. Existing plants enjoy grace periods, yet new facilities approved after September 2025 must meet thresholds on day one, shaping capital‐expenditure decisions for the Vietnam architectural coatings market.

Counterfeit Paints Undermining Premium Brands

Fakes siphon revenue from top-tier producers, dilute brand equity, and trigger costly warranty claims. Jotun now maintains an in-country brand-protection manager and litigated successfully against unauthorized distributors who refilled genuine buckets with lower-grade contents. Seamaster and KOVA deploy security holograms and scratch-code verification to reassure contractors. Despite crackdowns, counterfeit supply persists in rural outlets where price sensitivity is acute, introducing reputational risk that restrains premiumization across the Vietnam architectural coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Formulations Dominate Sustainability Transition

Water-borne coatings claimed 77.62% of the Vietnam architectural coatings market in 2025. Momentum stems from QCVN 19:2024/BTNMT’s emission ceilings, educational campaigns on indoor air quality, and multinational investments in local capacity. AkzoNobel injected EUR 18.5 million into its Bac Ninh site to add five powder lines and parallel water-borne modules, trimming import reliance and reducing lead times.

Solvent-borne products, though marginalized, post a healthy 3.92% CAGR as specifiers in marine, petrochemical, and high-traffic retail demand harder films and faster drying. Manufacturers mitigate emission penalties via high-solid and exempt-solvent technologies that stay below the regulatory cap yet preserve application properties. Powder coatings, still niche for façades and doors, gain mindshare through minimal waste and near-zero VOC, though adoption is slowed by the need for metal substrates and curing ovens. UV-curable paints remain confined to furniture makers exporting to North America and the European Union where migration limits are strict.

By Resin Type: Acrylic Leadership Faces Polyurethane Challenge

Acrylic families represented 41.88% of the Vietnam architectural coatings market size in 2025, supported by superior color retention and compatibility with water mediums. Domestic formulators leverage regionally sourced emulsions to offer cost-effective interior matt and exterior semigloss ranges. Technical standard TCVN 8653-4:2024 now prescribes scrub-resistance thresholds, incentivizing higher solids and crosslink density to extend life cycles.

Polyurethanes, albeit smaller, outpace rivals at 4.05% CAGR into 2031. KOVA’s KL‐5 flooring system demonstrates the segment’s traction in warehouses and hypermarkets where forklifts and shoppers impose severe abrasion. Hotels and resorts also migrate to two-component aliphatic PU clear coats for pool decks exposed to ultraviolet rays and chlorinated water. Alkyds continue in budget exteriors and rural venues but lose share as builders prioritize shorter project schedules incompatible with long dirt-pick times. Epoxies preserve a foothold for basements and chemical areas, while polyester resins serve architectural metalwork thanks to stable powder formulations.

By End-Use: Residential Dominance Yields to Commercial Acceleration

Housing absorbed 67.45% of the Vietnam architectural coatings market in 2025, a figure that tracks urbanization rates topping 41%. Local authorities channel land banks into mid-rise communities, spawning demand for primers, sealers, and color topcoats. Developers increasingly opt for factory-tinted systems to improve batch consistency, boosting tinting-paste and dispenser sales.

Commercial projects now advance at a 4.02% CAGR, narrowing the gap as FDI ushers in malls, offices, and logistics hubs. LEED-oriented retail clusters such as Central Premium Mall incorporate low-VOC guidelines into tender documents, pushing suppliers toward Environmental Product Declarations. Large hospitality builds adopt elastomeric exterior paints that bridge hairline cracks and resist coastal salt spray, notably along the Mekong Delta and central coast. Industrial end-users sustain steady pull for flooring and maintenance coatings amid electronics and apparel export growth, while institutional buyers, schools and hospitals, favor washable antimicrobial finishes aligned with public health directives.

Geography Analysis

The metropolis blends luxury apartments exceeding USD 8,000 per m² with expansive township developments, ensuring volume for both premium and economy grades in Southern Vietnam. Port proximity also simplifies inbound flows of titanium dioxide, resins, and additives, cutting freight for manufacturers based in nearby Dong Nai and Binh Duong provinces.

Infrastructure projects such as Ring Road 3’s completion by mid-2026 and Long Thanh International Airport’s final civil-works packages sustain steady protective-and-decorative consumption in Northern Vietnam. Industrial zones in Bac Ninh host the expanded AkzoNobel and PPG sites, improving just-in-time service to electronics assemblers and large-project contractors.

Central provinces boast the fastest incremental growth as policymakers lure investment with tax abatements. Saint-Gobain’s USD 9 million lightweight-panel plant in Quang Tri underscores the region’s push toward sustainable building components. Tourist corridors from Da Nang to Hoi An drive resort builds that demand weather-proof high-build elastomerics to withstand typhoon exposure. Regulatory geography also matters: emission-control zones cluster around major industrial parks, directing water-borne production inward while allowing powder units farther afield to exploit lower land costs.

Competitive Landscape

The Vietnam architectural coatings industry features consolidation amongts major players. Domestic champion KOVA leverages 100% Vietnamese ownership to tailor products to wet-season challenges, fielding over 1,000 shades certified for algae resistance. Joton and Seamaster focus on anti-counterfeit digital labels and painter-engagement apps that reward loyalty. Players increasingly differentiate through sustainability credentials, mobile color visualization, and end-to-end service bundles, surface inspection, substrate repair, and maintenance plans, that lock in repeat orders. Rural expansion offers whitespace; however, fragmented mom-and-pop outlets still command 60% of paint retail, challenging centralized marketing but offering growth runway for nimble players in the Vietnam architectural coatings market.

Vietnam Architectural Coatings Industry Leaders

Jotun

4Oranges Co., Ltd.

AkzoNobel N.V.

KOVA Group

Nippon Paint Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: PPG completed an expansion of its Yen Phong plant, adding automated spray booths and new water-borne lines to serve consumer-electronics customers in Southeast Asia.

- May 2024: Vietnam issued national standard TCVN 8653-4:2024 for emulsion wall paints, establishing scrub-resistance test methods and raising performance benchmarks.

Vietnam Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By End-Use

| Residential |

| Commercial |

| By Technology | Water-borne |

| Solvent-borne | |

| Others | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms