Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

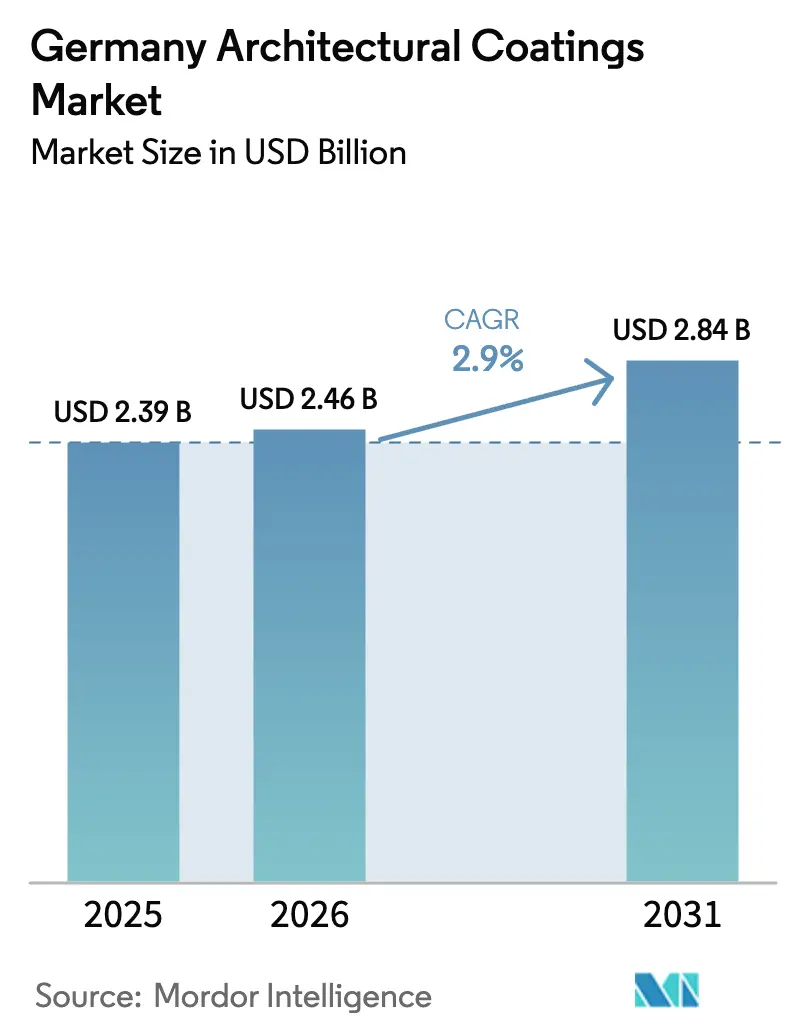

| Base Year Market Size (2025) | USD 2.39 Billion |

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 2.84 Billion |

| Growth Rate (2026 - 2031) | 2.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Architectural Coatings Market Analysis by Mordor Intelligence

The Germany Architectural Coatings market size is expected to grow from USD 2.39 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 2.84 billion by 2031 at 2.90% CAGR over 2026-2031. This steady trajectory reflects a maturing business landscape shaped by strict volatile-organic-compound limits, sustained renovation subsidies, and a decisive shift toward water-borne technology. Water-borne systems continue to outpace solvent-borne alternatives as professional applicators favor low-odor, quick-drying products that comply with the 2024 Construction Products Regulation. Subsidy programs such as BEG grants and KfW loans maintain paint demand even when new-build permits falter, while cost-competitive acrylic resins strengthen their hold on premium exterior and interior uses. Persistent swings in raw-material costs, notably for titanium dioxide, keep pricing strategies in flux; yet, larger producers defend their margins with purchasing scale and formulation agility. Competition intensifies as domestic leaders upgrade automation and as global multinationals broaden low-emission portfolios, ensuring the Germany Architectural Coatings market remains highly dynamic.

Key Report Takeaways

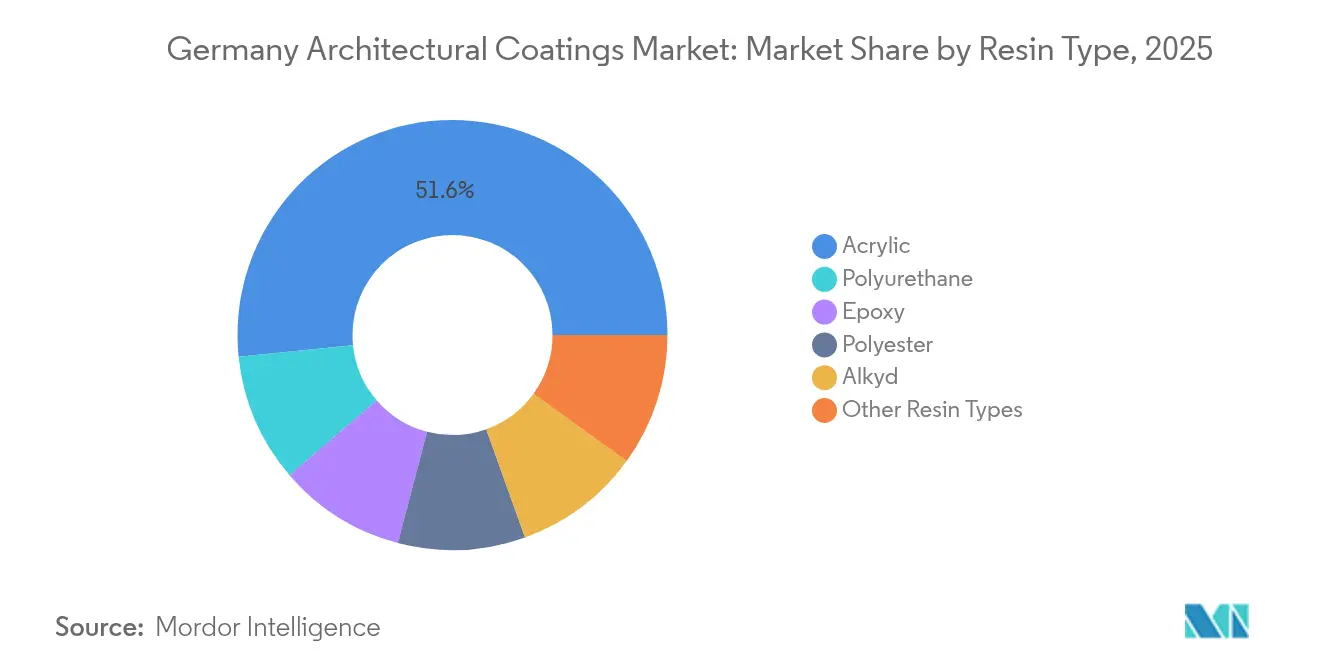

- By resin type, acrylic systems held a 51.62% share of the Germany Architectural Coatings market size in 2025 and are projected to expand at a 3.19% CAGR through 2031.

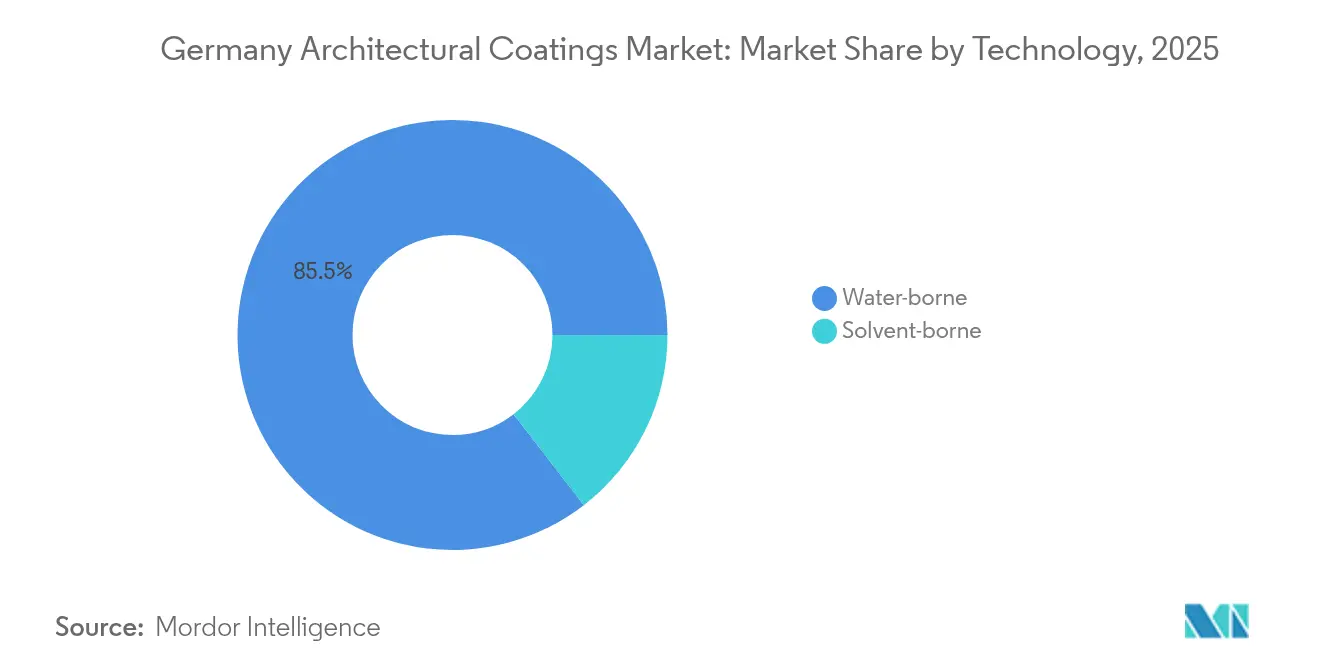

- By technology, water-borne products captured an 85.46% share of the Germany Architectural Coatings market in 2025, while the segment records the highest forecast CAGR at 3.12% to 2031.

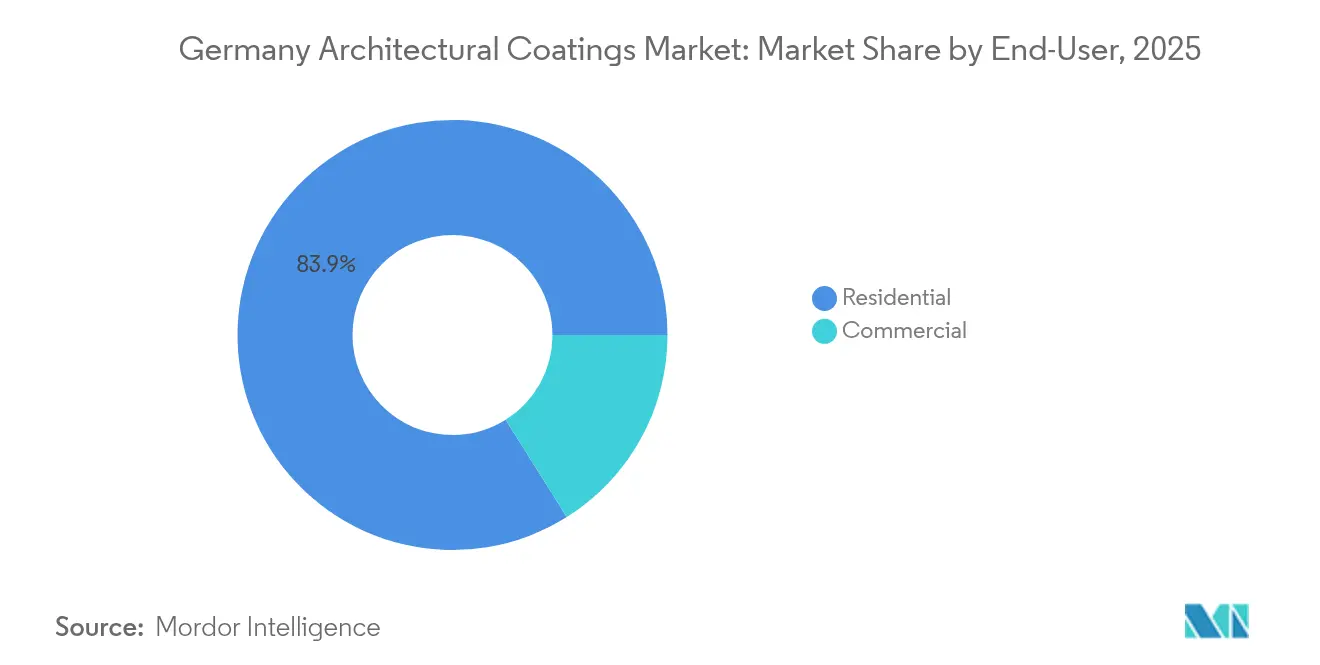

- By end-user, residential applications accounted for 83.92% of the Germany Architectural Coatings market share in 2025; the same segment advances at a 3.09% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-borne transition propelled by stricter VOC regulations | +1.2% | Germany nationwide, strongest in industrial regions | Medium term (2-4 years) |

| Renovation-wave incentives (BEG & KfW programs) | +0.8% | Germany nationwide, concentrated in residential markets | Short term (≤ 2 years) |

| Post-pandemic rebound in commercial fit-outs | +0.4% | Urban centers, commercial districts | Short term (≤ 2 years) |

| Acrylic resin durability & cost advantage | +0.6% | Germany nationwide, professional and DIY segments | Long term (≥ 4 years) |

| Rise of online DIY paint platforms & D2C brands | +0.3% | Germany nationwide, consumer-focused regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water-borne Transition Propelled by Stricter VOC Regulations

The 2024 Construction Products Regulation imposes lower VOC ceilings, which are expected to accelerate the adoption of water-borne products beyond the current 85.23% share. Professional painters increasingly specify compliant coatings because reduced emissions support safe job-site conditions and simplify waste-handling requirements. Manufacturers respond with formulation upgrades, Blue Angel certifications, and extensive Environmental Product Declarations, which help distributors showcase their environmental credentials. Acrylic chemistry underpins most innovations, as it pairs regulatory compliance with proven color stability, which explains its 52.15% share and the fastest expansion rate. These factors collectively underpin the Germany architectural coatings market as policymakers intensify enforcement[1]Bundesministerium für Umwelt, Naturschutz, nukleare Sicherheit und Verbraucherschutz, “Verordnung 2024/3110 Bauprodukte VOC-Grenzwerte,” BMUV, bmuv.de.

Renovation-Wave Incentives (BEG & KfW Programs)

BEG grants cover up to 40% of eligible retrofit costs, while KfW offers soft-rate loans that lower financing hurdles for energy upgrades. The two instruments directed EUR 2.1 billion to building refurbishments in 2024, offsetting a decline in new housing permits. Eligible projects frequently involve external-wall insulation and high-build facade paints, creating resilient demand in the residential category. Water-borne acrylic facades meet both energy performance and VOC regulations, enhancing product pull-through in hardware retail and professional dealer channels. Renovation projects now incorporate efficiency measures in roughly 60% of cases, a shift that stabilizes volume while improving mix toward premium coatings.

Post-Pandemic Rebound in Commercial Fit-outs

Commercial interiors, which were previously delayed by work-from-home uncertainty, returned to growth in 2024 as office owners reconfigured floor space for hybrid occupancy. Office refurbishments increased by 15% year-over-year, and facilities in healthcare, hospitality, and logistics also resumed expansion. These settings specify antimicrobial, stain-resistant, and easy-clean paints that command higher price points and require multi-coat systems, thereby elevating the liters-per-square-meter ratios compared to standard residential work. The commercial rebound boosts professional volumes and supports distributor sell-through in metro regions, despite lingering weaknesses in new construction[2]Bundesministerium für Wohnen, Stadtentwicklung und Bauwesen, “Baugenehmigungen Jahresreport 2024,” BMWSB, bmwsb.bund.de .

Acrylic Resin Durability and Cost Advantage

Acrylic chemistries offer weather-fastness and color retention unmatched by older alkyd solutions, yet remain price competitive because global monomer supply has stabilized. Their broad formulation latitude allows producers to tailor products for interior matte finishes, exterior elastomeric facades, and direct-to-metal primers, supplying every value tier from budget DIY to industrial maintenance. German formulators utilize acrylic backbones to reduce solvent content without compromising hide or scrub resistance, thereby directly addressing the regulatory context and consumer safety expectations. Cost resilience during feedstock swings further shields margin when titanium dioxide quotations fluctuate, reinforcing acrylic’s ascendancy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ & petrochemical feedstock prices | -0.9% | Germany nationwide, affecting all manufacturers | Short term (≤ 2 years) |

| Slump in new-build permits amid high interest rates | -0.7% | Germany nationwide, concentrated in residential markets | Medium term (2-4 years) |

| EU Biocide Regulation escalating in-can preservative costs | -0.4% | Germany nationwide, water-borne segment impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Petrochemical Feedstock Prices

Titanium dioxide spot prices displayed 25% swings in 2024, forcing repeated surcharge notices from major suppliers and squeezing smaller producers with limited hedging capacity. Resin raw materials tied to propylene and butadiene posted similar volatility, complicating cost-plus pricing models in the do-it-yourself channel where shoppers resist rapid list-price adjustments. To protect their margins, larger companies negotiated volume rebates, diversified their pigment purchasing, and reformulated their products toward lower TiO₂ levels where hiding power was still effective. The volatility threatens sustained R&D investment among mid-tier participants and may accelerate consolidation if access to capital becomes tighter.

Slump in New-Build Permits Amid High Interest Rates

Building permits for dwellings decreased by 4.1% in 2024, as mortgage rates rose and labor shortages persisted. New-build work typically consumes 40% to 60% more coating per unit than repaint cycles, as virgin surfaces require primers and multiple finishing coats. The decline, therefore, exerts outsized pressure on professional painting crews, leading to increased competitive bidding and eroded service margins. The Federal Ministry for Housing forecasts a gradual recovery of the construction sector from 2025, aided by rate stabilization and energy-efficient prefabricated components that reduce site time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Systems Drive Performance Innovation

Acrylic resins owned 51.62% of the Germany Architectural Coatings market in 2025 and are growing at a 3.19% CAGR through 2031. Their widespread use in both interior and exterior products positions them as the technology of choice for projects that require weathering resistance, colorfastness, and VOC compliance. Formulators exploit acrylic’s broad molecular weight range to tailor viscosity, sheen, and film strength, which supports niche offerings such as crack-bridging elastomeric facades and low-tension heritage coatings. In cost-sensitive DIY products, styrene-acrylic blends increase solids content while maintaining tint acceptance, thereby protecting shelf appeal during raw material inflation cycles.

Alkyd resins retain their legacy niches in wood preservation and metal primer systems, but face gradual displacement as low-solvent regulations tighten. Polyurethane crosslinking enhances scrub resistance and impact hardness in premium interior enamels, increasing unit price but limiting volume due to isocyanate safety regulations. Epoxy and polysiloxane hybrids serve high-traffic floors, garages, and commercial kitchens that require chemical resistance, a niche market that remains small yet profitable. Collectively, these dynamics confirm that acrylic technology will account for an even larger slice of the Germany architectural coatings market size by 2030 as environmental rules and performance demands converge on its attribute set.

By Technology: Water-Borne Dominance Accelerates

Water-borne products constituted 85.46% of the Germany Architectural Coatings market in 2025 and are forecast to advance at a 3.12% CAGR, effectively solidifying near-total market control. Regulatory ceilings for VOCs, end-user expectations for low odors, and property owner preferences for quick re-occupancy all reinforce demand. Technical progress, such as latex-shielded particles, coalescing solvent optimization, and wet-edge extenders, means that modern waterborne enamels now rival historical alkyd gloss levels. Training initiatives by trade associations teach applicators how to manage changed open times and tool cleaning, closing skill gaps that once slowed adoption.

Solvent-borne systems persist where substrate adhesion or cold-weather drying is critical, but unit share continues to retreat as water-borne chemistries improve. Some industrial maintenance paints still rely on solvent carriers for corrosion inhibition; however, crosslinkable waterborne polysiloxanes now offer similar protection with fewer hazardous air pollutants. The acceleration toward water-borne therefore appears irreversible, cementing the technology as the backbone of the Germany Architectural Coatings market over the next decade.

By End-User: Residential Renovation Sustains Growth

Residential applications commanded 83.92% of the Germany Architectural Coatings market in 2025 and should expand at a 3.09% CAGR through 2031. Government incentives covering insulation, window upgrades, and heat-pump installation lead households to schedule full-envelope refurbishments that inevitably include facade repaint and interior redecoration. Do-it-yourself volumes dipped in 2024 amid rising living costs, yet consumer sentiment surveys signal renewed project intent as borrowing conditions stabilize. Meanwhile, professional contractors are pivoting toward renovation service bundles that combine energy audits, scaffold logistics, and warranty coverage, thereby lifting average ticket values.

Commercial demand still lags 2019 peaks but shows clear rebound patterns in office modernization, health-care expansions, and hotel upgrades. Product specifications in these segments emphasize antimicrobial surfaces, stain resistance, and long repaint cycles, which raise liter-per-unit prices. Industrial and infrastructure niches—such as parking decks, tunnels, and rail stations—consume specialized high-build systems that add incremental tonnage, albeit at slower growth rates. Together, these patterns keep residential work the volume backbone while commercial refits drive specification innovation and margin in the Germany Architectural Coatings market.

Geography Analysis

The Germany Architectural Coatings market concentrates demand along the populous western and southern Länder where construction activity remains highest. North Rhine-Westphalia stands out due to its dense urban clusters, such as Cologne, Düsseldorf, and Essen, which generate constant renovation cycles in both multifamily housing and commercial real estate. The region’s manufacturing base also anchors multiple production plants, ensuring prompt supply to professional wholesalers and retail chains. Bavaria and Baden-Württemberg exhibit above-average disposable incomes, which encourage the uptake of premium products and greater acceptance of sustainability labeling. These states further benefit from active state-level subsidy supplements that stack on top of federal BEG grants, amplifying demand for façade refurbishment and insulation coatings.

In eastern Germany, structural funds and renewed infrastructure budgets are driving public building repaint projects, while new logistics hubs along the Berlin-Leipzig corridor support warehouse construction that requires protective floor and roof coatings. Construction sector data indicate a 3% nationwide rebound in 2025, with the strongest early momentum visible in Saxony and Brandenburg, where industrial project pipelines are firming. Northern ports such as Hamburg spur marine maintenance coatings for adjacent dock facilities, yet the bulk of architectural volumes still flows to housing stock enhancements rather than heavy industrial use. Uniform VOC rules and Blue Angel adoption create a common regulatory baseline across Länder, but local labor availability and municipal tender schedules produce distinct quarterly volume swings. Ultimately, the Germany architectural coatings market grows at a measured pace nationwide, with regional subsidy uptake and urbanization patterns dictating short-term variances.

Competitive Landscape

The Germany Architectural Coatings market is moderately consolidated. Continuous margin tension forces every participant to automate production, digitize color matching, and shorten supply lead times. Caparol’s Paint Buddy robot sprayer pilots on live building sites, and MAPEI’s digital support hub provides BIM-ready specification downloads, accelerating contractor workflow. Sustainability disclosures shift from a marketing claim to a market entry ticket. These moves keep competition vigorous yet increasingly service-oriented, ensuring innovation remains a key currency in the market.

Germany Architectural Coatings Industry Leaders

Brillux GmbH & Co. KG

DAW SE

PPG Industries, Inc.

Sto SE & Co. KGaA

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: German multinational Keimfarben GmbH (KEIM) announced a strategic partnership with India’s Zydex Industries. Under the partnership, KEIM’s silicate paint technology will be available for India’s architectural and infrastructure projects. This will increase the revenue of Keimfarben GmbH (KEIM) in the future.

- November 2024: AURO Pflanzenchemie AG, a pioneer in ecological natural architectural paints and wood care products, was named the winner of the 17th German Sustainability Award (DNP) in the Companies, Construction and Real Estate sector, Coatings and Paints category.

Germany Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms