Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

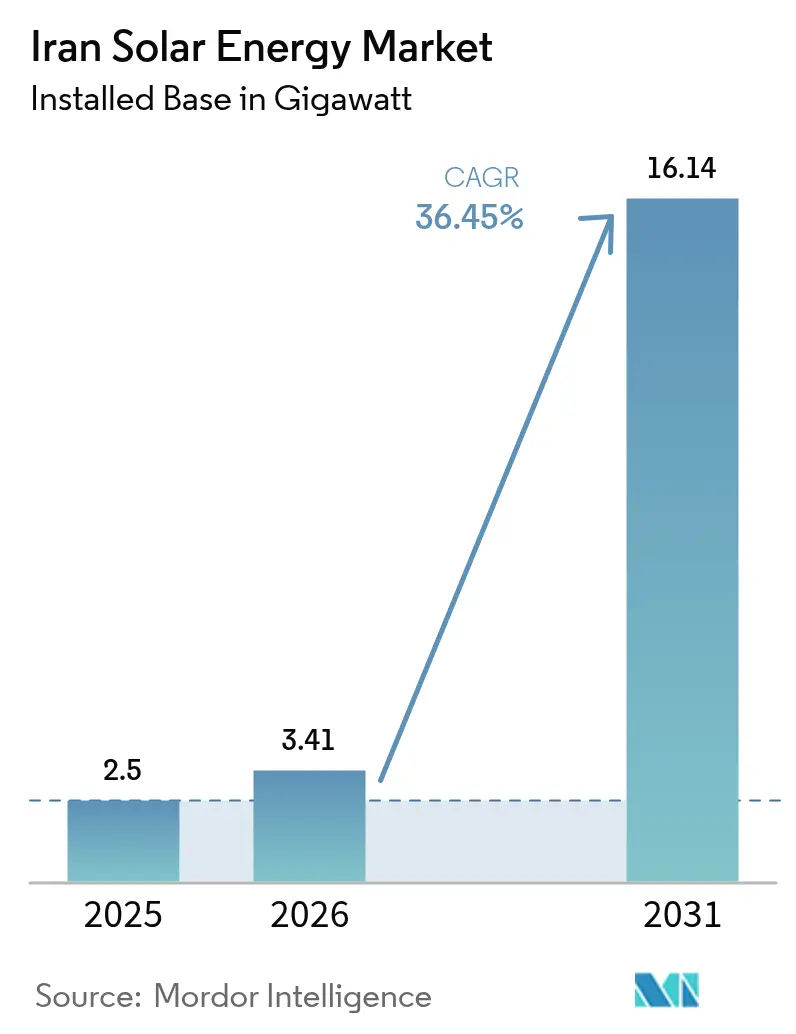

| Base Year Market Size (2025) | 2.5 gigawatt |

| Market Volume (2026) | 3.41 gigawatt |

| Market Volume (2031) | 16.14 gigawatt |

| Growth Rate (2026 - 2031) | 36.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Solar Energy Market Analysis by Mordor Intelligence

The Iran Solar Energy Market size in terms of installed base was valued at 2.5 gigawatt in 2025 and estimated to grow from 3.41 gigawatt in 2026 to reach 16.14 gigawatt by 2031, at a CAGR of 36.45% during the forecast period (2026-2031).

This growth surge is driven by a 15 GW national target, 300 sunny days per year, and an average solar irradiance of over 2,200 kWh per square meter. The SATBA feed-in tariff (FiT) revival offers 20-year, foreign-exchange-indexed contracts that restore bankability for private developers, while the 10 GW industrial captive-solar exemption from load shedding anchors demand from energy-intensive plants. Import-duty waivers on bifacial modules and trackers, together with localization mandates that seed joint-venture factories, are further accelerating capacity build-out. Foreign-exchange constraints and fossil-fuel subsidies still temper residential adoption, but rail freight from China and domestic assembly lines provide viable workarounds.

Key Report Takeaways

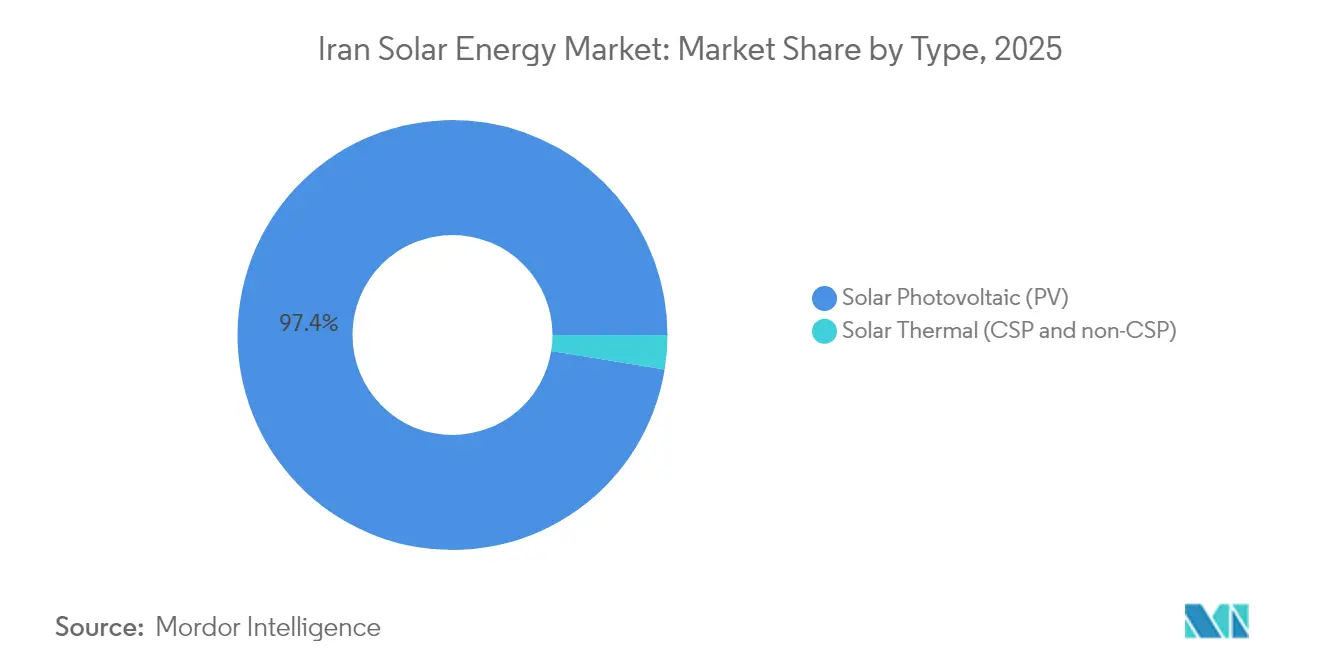

- By technology, solar photovoltaic (PV) accounted for 97.43% of Iran's solar energy market share in 2025 and is projected to grow at a 36.12% CAGR through 2031.

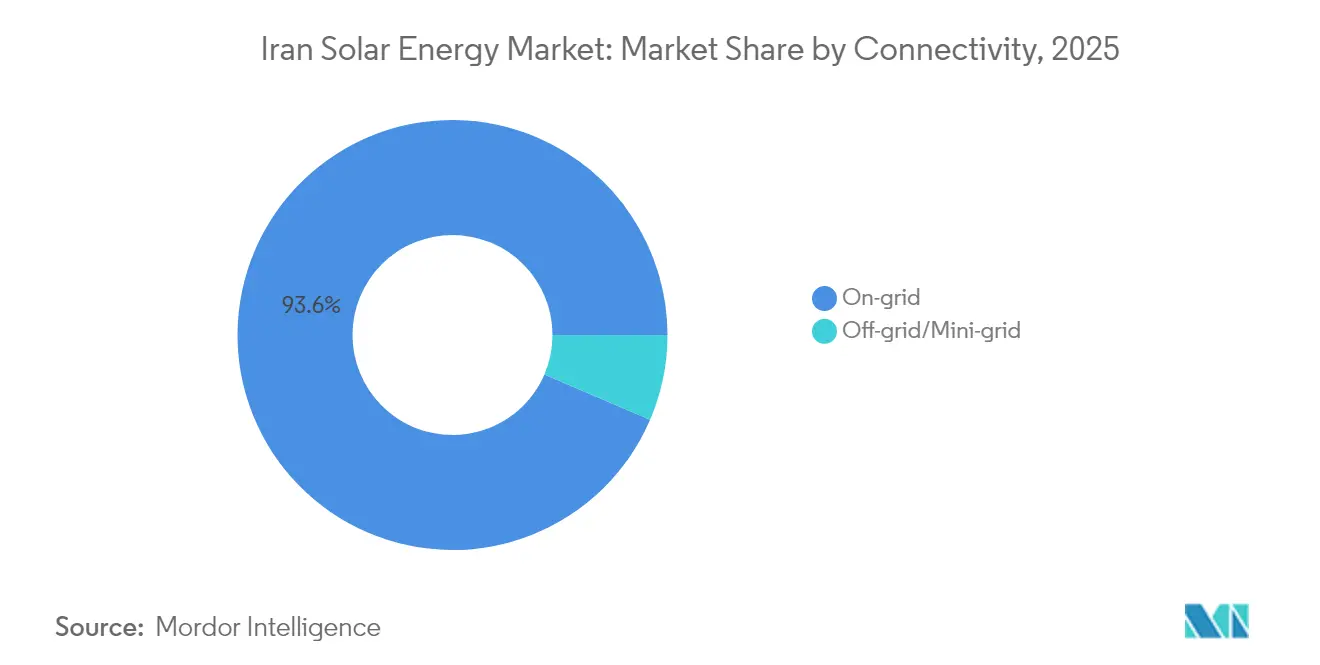

- By grid type, on-grid systems held a 93.55% share of the Iranian solar energy market in 2025; off-grid registered the fastest growth at a 40.25% CAGR.

- By end-user, utility-scale installations secured 74.62% of Iran's solar energy market share in 2025, while commercial and industrial systems led growth at a 41.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iran Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SATBA feed-in-tariff revival boosts bankability | +8.5% | National, with early gains in Isfahan, Kerman, Yazd | Medium term (2-4 years) |

| 10 GW industrial captive-solar exemption from load-shedding | +7.2% | Industrial corridors, concentrated in Tehran, Isfahan, Khuzestan | Short term (≤ 2 years) |

| Nomad & rural mini-grid roll-out (28,000 kits by 2024) | +5.8% | Rural and nomadic regions nationwide | Long term (≥ 4 years) |

| Import-duty waiver on bifacial modules & trackers | +4.9% | National, with spillover to neighboring markets | Medium term (2-4 years) |

| Localization mandate spurs JV manufacturing capacity | +4.1% | Manufacturing hubs in Tehran, Isfahan, with export potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SATBA Feed-in Tariff Revival Boosts Bankability

The restored 20-year FiT, indexed to foreign-exchange rates, removes off-taker risk and shields returns from devaluation. Solar projects that once stalled at 3% of annual capacity targets now progress as SATBA has granted permits exceeding 29 GW, creating a substantial development pipeline. Domestic pension funds welcome inflation-protected yields, and preliminary talks on rial-denominated green bonds indicate emerging depth in the capital market. Early grid-synchronized projects validate cash flows, encouraging follow-on investment, and the multiplier effect accelerates the Iranian solar energy market beyond official forecasts.

10 GW Industrial Captive-Solar Exemption from Load-Shedding

Guaranteed grid access for self-generation provides energy-intensive plants with a clear arbitrage: replacing blackout downtime, which cuts summer output by up to 40%, with a predictable solar supply. The 600 MW Aftab-e-Sharq complex, co-developed by Mobarakeh Steel, demonstrates how captive solar reduces operational volatility and cuts CO₂ emissions by 2.5 million tons annually.[1]MAPNA Group Communications, “Aftab-e-Sharq 600 MW Solar Project Update,” mapnagroup.com Spatial clustering around industrial corridors reduces infrastructure costs per MW and fosters shared maintenance ecosystems, thereby deepening solar’s competitiveness in manufacturing value chains.

Nomad & Rural Mini-Grid Roll-Out (28,000 Kits)

Portable systems, offered at 10% of the cost, have electrified 10% of Iran’s 252,000 nomadic households, demonstrating a scalable off-grid model that bypasses the need for expensive transmission extensions. High reliability in harsh climates encourages sedentary rural communities to adopt similar solutions, and government subsidy precedents pave the way for solar-powered irrigation and cold-storage schemes that enhance food security. The three-year deployment window showcases institutional agility that could be redeployed for larger rural energy programs.

Import-Duty Waiver on Bifacial Modules & Trackers

Removing duties aligns policy with energy-yield economics: bifacial panels deliver up to 30% more output in high-albedo deserts while single-axis trackers add 15-25% generation gains.[2]Wiley Editorial Board, “Performance Uplift of Bifacial Modules in High-Albedo Terrains,” Wiley, onlinelibrary.wiley.com Higher harvests raise tax receipts, making the waiver fiscally neutral and position Iran to benefit from global bifacial cost curves expected to dominate installations post-2030. The measure also signals a pragmatic balance between access to technology and domestic manufacturing incentives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Subsidised fossil-fuel tariffs undercut solar LCOE | -3.8% | National, with higher impact in gas-rich regions | Long term (≥ 4 years) | |

| FX liquidity crunch for imported PV components | -2.9% | National, with acute effects in import-dependent regions | Short term (≤ 2 years) | |

| Grid-congestion & curtailment in Yazd-Kerman solar belt | -2.4% | Yazd-Kerman corridor, with spillover to central provinces | Medium term (2-4 years) | |

| Sanctions-linked financing bottlenecks | -2.1% | National, with higher impact on large-scale projects | Medium term (2-4 years) | |

| Source: Mordor Intelligence | ||||

Subsidized Fossil-Fuel Tariffs Undercut Solar LCOE

Electricity priced near USD 0.04/kWh distorts economics, keeping solar LCOE at a premium, especially for residential customers. Subsidy reform is politically sensitive, yet gradual industrial tariff rises signal an implicit recognition that the fiscal burden is unsustainable. Differential price adjustments now encourage corporates to adopt renewables, but household uptake lags until broader subsidy rationalization narrows the gap.

FX Liquidity Crunch for Imported Components

Sanctions-induced banking curbs prompt developers to turn to informal currency markets, which offer exchange rates 20-30% higher, thereby inflating capital expenditures for inverters and trackers. Rail shipments from China to Aprin dry port offer an alternative logistics option; however, currency volatility necessitates contingency buffers in project budgets. Localization is a long-term hedge, although advanced component production still relies on imported precursor materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Achieves Complete Market Dominance

Solar PV accounted for 97.43% of Iran's solar energy market share in 2025, as every new megawatt added since late 2023 has used crystalline-silicon modules. The Iranian solar energy market size devoted to PV is projected to grow at a 36.12% CAGR through 2031, as policymakers have eliminated regulatory pathways for water-intensive CSP, opting instead for a single-technology platform that standardizes engineering, O&M, and grid-code compliance. Iran's 300 sunny days and direct normal irradiance above 2,200 kWh/m² raise PV capacity factors to 23% in southeastern deserts, keeping levelized costs below subsidized gas peaker plants over 20-year FiT contracts.

Technology consolidation further trims soft costs as EPC firms reuse design templates, procurement contracts, and workforce training modules. Duty-free access to bifacial panels and single-axis trackers enables developers to increase yield by up to 30% at flat capital expenditure, locking in superior economics for the Iran solar energy market size earmarked for utility projects. The absence of rival technologies also simplifies supply-chain localization, enabling Tehran and Isfahan factories to scale module assembly lines without splitting volume across multiple process flows. Continued global price declines for mono-PERC and TOPCon wafers, therefore, directly feed into domestic capex savings, sustaining PV's market share through 2031.

By Grid Type: On-Grid Dominates While Off-Grid Accelerates

On-grid assets represented 93.55% of Iran's solar energy market share in 2025 because SATBA's 20-year, FX-indexed power-purchase agreements guarantee bankable cash flows for utility plants. This grid-linked slice of the Iranian solar energy market size grows steadily as developers rush to plug a 14 GW summer deficit; yet, off-grid and mini-grid systems register a sharper 40.25% CAGR through 2031, driven by 28,000 subsidized nomadic kits and village micro-grids that leapfrog transmission bottlenecks.

Curtailment in the congested Yazd-Kerman corridor is now pushing some sponsors toward storage-coupled off-grid farms, creating a feedback loop that accelerates decentralized adoption. Net-metering and one-stop interconnection desks cut paperwork for rooftop projects feeding urban feeders, while standalone arrays power pumps, telecom towers, and agro-clusters beyond the reach of the high-voltage backbone. Taken together, on-grid expansion and off-grid acceleration create a twin-track build-out that enhances both bulk supply and last-mile access.

By End-User: Utility-Scale Leads While C&I Surges

Utility plants larger than 5 MW commanded 74.62% of Iran's solar energy market share in 2025, reflecting a state strategy that prioritizes high-impact projects capable of offsetting a projected 30% generation shortfall. The Iran solar energy market size for these grid-anchored parks grows steadily, but commercial and industrial (C&I) systems post a faster 41.12% CAGR as manufacturers secure blackout immunity under a 10 GW captive-solar exemption.

Mobarakeh Steel's off-take from the 600 MW Aftab-e-Sharq complex exemplifies how C&I demand underwrites utility economics while delivering 2.5 million t annual CO₂ cuts. Subsidized household tariffs of around USD 0.04/kWh still hinder residential adoption, yet rising industrial rates and ESG reporting rules are propelling factory rooftops and brownfield carports into financial viability. As fiscal pressures prompt the government to consider broader tariff reform, the C&I surge is likely to intensify, gradually balancing today's utility-heavy project pipeline.

Geography Analysis

Southern and central provinces form the nucleus of the Iranian solar energy market. The Yazd-Kerman belt, blessed with 2,200 kWh/m² of irradiation, hosts landmark projects such as the 600 MW Aftab-e-Sharq park, which demonstrates industrial-utility collaboration. Grid congestion in the corridor prompts parallel investment in 400-kV lines and battery systems to stave off curtailment risks.

The northern coastal provinces of Gilan and Mazandaran show promise for rooftop potential in densely populated areas. Although irradiance is lower, proximity to demand nodes and robust urban grids offset production differentials. Pilot “solar settlements” are already paving streets with PV canopies that double as shading and power generation.

Western regions such as Khuzestan and Kermanshah present emerging opportunities tied to oil-gas infrastructure that offers strong grid backbones and industrial offtakers. Resource assessments identify Abadan and Aghajari as high-yield sites with minimal land-use conflicts. Further east, Semnan Province is earmarked for a high-tech solar hub backed by Chinese capital, creating export corridors into Central Asia once sanctions constraints ease.

Competitive Landscape

Market concentration is moderate, with MAPNA Group spearheading development and vertically integrated joint ventures strengthening local supply chains. MAPNA’s renewable arm synchronised the first 20 MW of Aftab-e-Sharq in October 2024 and targets full completion of 600 MW before 2027, showcasing its turnkey EPC capability. Chinese majors, JinkoSolar, Trina Solar, and Longi, sustain equipment dominance through cell and wafer supply, but opt for licensing rather than direct ownership to navigate sanctions.

Strategically, top domestic firms pursue localization to lock in FiT premium eligibility and hedge currency exposure. Target segments include floating PV on reservoirs, combining evaporation control with generation; agro-PV in water-scarce farms; and grid-stabilizing battery hybrids that can unlock curtailed capacity. Barriers to new entrants remain high due to financing hurdles and the complexity of navigating policies, yet the scale of upcoming tenders ensures room for specialized EPC, O&M, and digital monitoring players.

Iran Solar Energy Industry Leaders

Mapna Renewable Energy

SATBA-backed Ghadir Solar

JinkoSolar

KPV Solar GmbH

Carlo Maresca SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Iran earmarked USD 1.5 billion for solar panel installations. On May 24, Iran's Supreme Council for Economic Coordination (SCEC) mandated banks to provide a USD 1.5 billion loan to the Ministry of Energy, contingent on Central Bank approval. These funds are designated for importing crucial equipment to build a 7,000 MW solar power plant.

- May 2025: Rail freight from China delivered a full cargo of PV panels to Aprin dry port in Iran, demonstrating the resilience of logistics against sanctions.

- January 2025: Iran's Small Industries and Industrial Parks Organisation (ISIPO) greenlit 24 specialized industrial parks focused on solar energy, with four parks already operational and leasing land to investors.

- December 2024: Iran, in collaboration with Tavanir and under the supervision of the Ministry of Energy, has launched a program. This initiative provides portable solar panels to all nomadic households across the country, requiring participants to cover just 10 percent of the cost.

Iran Solar Energy Market Report Scope

Solar energy refers to the energy that is harnessed from the sun's light and heat. The sun is a natural source of energy that emits electromagnetic radiation, which can be captured and converted into usable energy using various technologies such as solar panels, solar cells, and solar thermal collectors.

The solar energy market is segmented by type. By type, the market is segmented into solar photovoltaic (PV) and solar thermal. For each segment, market sizing and forecasts have been done based on installed capacity (MW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the Iran solar energy market in 2026?

Installed capacity reached 3.41 GW in 2026 and is projected to hit 16.14 GW by 2031.

What annual growth rate is forecast for Iranian solar installations?

Capacity is set to advance at a 36.45% CAGR from 2026 to 2031.

Which segment leads solar deployment in Iran?

Utility-scale plants above 5 MW held 74.62% share of installed capacity in 2025.

What share does solar PV hold in Iran’s technology mix?

Solar PV commands 97.43% of installations and continues to grow due to favorable economics.

How does the FiT scheme support project finance?

SATBA offers 20-year, FX-indexed purchase agreements that eliminate offtaker risk for grid-connected projects.

What impact do localization mandates have on supply chains?

Joint-venture factories assembling modules and inverters reduce foreign-exchange exposure and create skilled jobs in Tehran and Isfahan.

Page last updated on: