Iran ICT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 24.91 Billion |

| Market Size (2030) | USD 30.18 Billion |

| Growth Rate (2025 - 2030) | 3.91% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Iran ICT Market Analysis by Mordor Intelligence

The Iran ICT market size stands at USD 24.91 billion in 2025 and is forecast to reach USD 30.18 billion by 2030, expanding at a 3.91% CAGR over the period. Persistent currency weakness, sanctions, and power-supply constraints continue to challenge operators, yet the sector’s overall trajectory remains positive thanks to accelerated 5G deployment, state-backed cloud projects, and rising small-business demand. Government funding of USD 115 million for a ten-year national AI program, coupled with spectrum auctions that favor domestic suppliers, illustrates Tehran’s push for technological self-reliance. In parallel, a 25% jump in national-internet spending to USD 300 million during 2024 reduced reliance on foreign bandwidth and underpinned local cloud uptake. Major operators such as MTN Irancell have begun rolling out fiber-to-the-home in 61 cities, creating new backhaul capacity for data-hungry services.

Key Report Takeaways

- By type, Communication Services held 33.41% of Iran ICT market share in 2024.

- By enterprise size, SMEs accounted for 56.63% of the Iran ICT market size in 2024 and are projected to grow at a 4.02% CAGR through 2030.

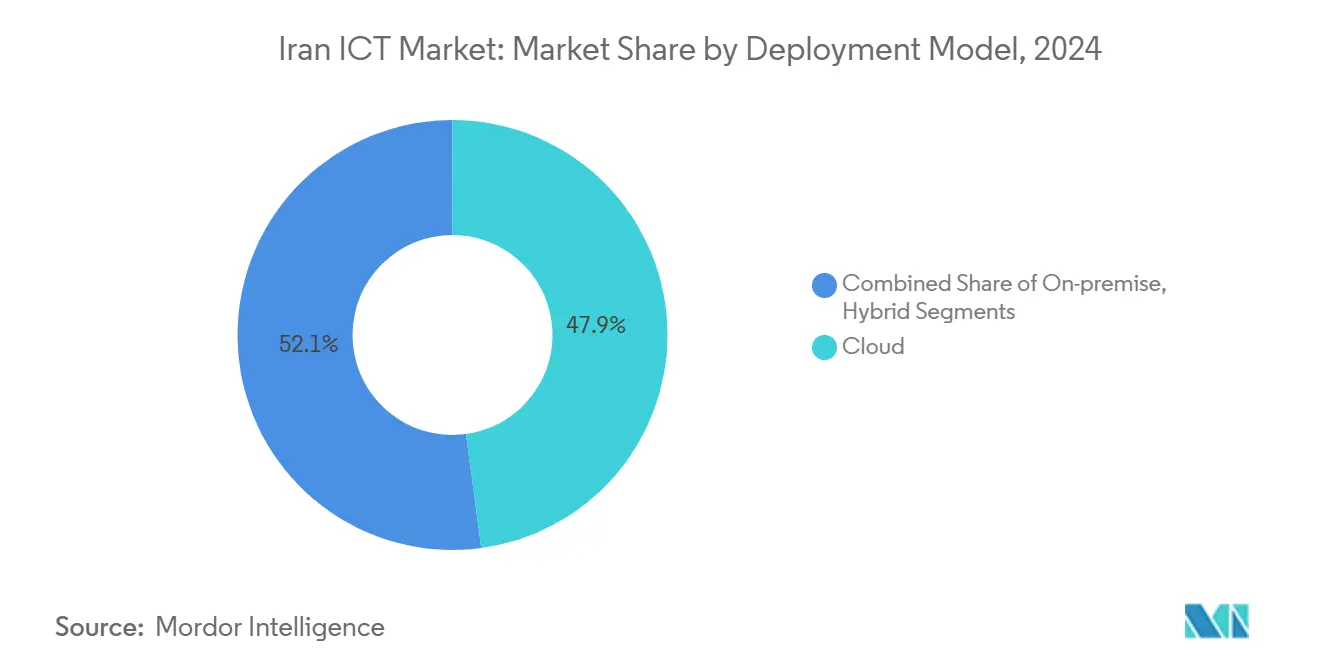

- By deployment model, cloud solutions captured 47.86% of 2024 revenue and are set to post a 4.13% CAGR between 2025 and 2030.

- By end user, Gaming and Esports leads with a 4.74% CAGR to 2030.

Iran ICT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-out backed by government spectrum auctions | +1.20% | Tehran, Kish | Medium term (2-4 years) |

| Emergence of nation-wide cloud datacenter projects | +0.90% | Major cities | Long term (≥4 years) |

| Surge in e-commerce and digital payment penetration | +0.80% | Urban centers | Short term (≤2 years) |

| Increase in ICT spend by oil-and-gas modernization programs | +0.70% | Khuzestan, Persian Gulf | Medium term (2-4 years) |

| Re-export of refurbished hardware via free-trade zones | +0.40% | Kish, Chabahar | Short term (≤2 years) |

| Growth of Persian-language SaaS tools for SMEs | +0.30% | Tehran, Isfahan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G roll-out backed by government spectrum auctions

About 650 commercial 5G sites are now live alongside 16,800 4G locations, anchored by operator commitments to national coverage. Protected auctions restrict foreign participation, ensuring domestic vendors win spectrum blocks, share technology, and localize equipment. Kish Free Zone serves as a testbed where gigabit speeds underpin smart-tourism and connected-logistics pilots. The expanding footprint boosts mobile broadband capacity, lowers latency for cloud workloads, and accelerates use cases such as remote maintenance in energy fields.

Emergence of nation-wide cloud datacenter projects

Tehran’s USD 300 million allotment for the National Information Network in 2024 fostered hyperscale facilities run by ArvanCloud, DigiCloud and AsiaTech. Domestic hosting sidesteps sanctions, keeps data onshore, and offers businesses pay-as-you-go elasticity absent in imported servers. Operators, however, face a 25 GW power-generation shortfall and must install diesel gensets, driving operating expenditures. Long-term agreements with the Energy Ministry are in discussion to guarantee stable electricity for tier-III and tier-IV halls.

Surge in e-commerce and digital payment penetration

Local gateway Asan Pardakht reported 36.83% revenue growth in 2025 after banks were cut off from SWIFT, prompting merchants to adopt domestic rails. [1]EMIS, “Asan Pardakht Persian Company Profile,” emis.com Although 2022-2024 internet curbs depressed transaction counts by up to 60%, volumes rebounded once restrictions lifted thanks to resilient switching networks. The Smart Government Services Window logged 60 million users, creating a single sign-on environment that smooths checkout for retail marketplaces.

Increase in ICT spend by oil-and-gas modernization programs

The National Iranian Oil Company has begun AI-enabled digitalization of wellheads to recover 15 million m³ of flared gas by end-2025. A USD 17 billion domestic vendor package for South Pars pressure-boosting embeds predictive analytics, edge sensors, and private-LTE networks. Local systems integrators tap this funding pool to supply ruggedized hardware and bespoke machine-learning models, elevating industrial demand for cyber-secure telecom links.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. sanctions limiting access to global vendors | -1.80% | Countrywide | Long term (≥4 years) |

| Local currency volatility affecting CapEx cycles | -1.10% | Import-heavy sectors | Medium term (2-4 years) |

| Brain-drain of senior ICT talent to Gulf countries | -0.70% | Tech hubs | Long term (≥4 years) |

| Electricity rationing impacting data-center uptime | -0.50% | Tehran, industrial centers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

U.S. sanctions limiting access to global vendors

Wide-ranging export controls keep advanced chipsets, network optics, and licensed software out of Iran, forcing domestic developers to reverse-engineer or source from East-Asian grey channels. The April 2025 Russia–Iran pact adds joint R&D labs and a shared satellite backbone that partially offsets Western blockade effects. [2]Tadviser, “Russia and Iran Conclude Large-Scale ICT Treaty,” tadviser.com Still, compliance burdens and shipping delays stretch project timelines, lift costs, and pare back feature upgrades for enterprise customers.

Electricity rationing impacting data-center uptime

A 25 GW generation gap has triggered rotating blackouts that downed connectivity across Tehran in February 2025. Data-center operators rely on diesel gensets that add 10%-15% to opex and complicate service-level guarantees. The grid deficit derives from under-funded thermal plants and gas-supply curbs. Without new capacity, power-hungry GPU clusters for AI training may stay capped, limiting high-performance-compute workloads within the Iran ICT market.

Segment Analysis

By Type: Communication Services Drive Market Evolution

Communication Services contributed 33.41% of the Iran ICT market in 2024 on the back of MTN Irancell’s fiber roll-out and nationwide 5G coverage. Cloud Services follow as the fastest-growing with a 4.31% CAGR, reflecting enterprise migration to domestic infrastructure supported by USD 300 million in state funding. IT Hardware imports remain constrained and volatile, whereas IT Software benefits from Persian-language ERP and SaaS adoption.

Extensive mobile-broadband reach lets operators bundle fintech gateways, video streaming, and edge-cloud offerings, transforming telcos into platform providers. Capital intensity shifts toward backhaul fiber and datacenter colocation rather than copper replacements. Domestic vendors capture spend via localized security stacks that meet compliance mandates. As a result, Communication Services will stay a cornerstone yet cede incremental share to cloud and managed-service lines as enterprises embrace asset-light operations aligned with sanctions-era realities within the Iran ICT market.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SMEs Accelerate Digital Adoption

SMEs accounted for 56.63% of 2024 demand, underscoring accessibility of cloud POS, accounting, and HR applications through subscription pricing. The segment is forecast to expand at 4.02% CAGR, aided by government e-invoicing mandates and simplified tax filing inside the Smart Government Services Window.

Large enterprises still drive ticket-size projects, especially in energy and banking where full-stack modernization, private 5G, and AI require multi-year budgets. Yet pricing pressure and local content rules push Tier-1 suppliers to modularize offerings to fit SME budgets. SaaS marketplaces list over 3,000 Persian-language apps, from CRM to data-visualization, lowering switch costs and fueling broader Iran ICT market penetration among smaller firms.

By Deployment Model: Cloud Infrastructure Gains Momentum

Cloud captured 47.86% revenue in 2024 and remains the growth frontrunner at 4.13% CAGR. Pay-as-you-go access sidesteps cash-flow limits imposed by currency swings, while built-in redundancy mitigates power-outage risk. The Iran ICT market size linked to cloud solutions for SMEs is projected to account for nearly half of incremental spending over 2025-2030.

On-premise systems persist for ministries and critical-sector clients that demand air-gapped environments. Hybrid adoption grows as banks deploy local Kubernetes clusters backed up to ArvanCloud zones in Kerman and Tabriz. Sovereign-cloud certifications released in 2025 require all personal-data workloads to stay inside national borders, a rule that funnels more migration toward domestic facilities.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry Vertical: Retail and Gaming Lead Growth

Retail, e-commerce, and logistics led with 18.21% of 2024 revenue, riding a surge in mobile payments once international rails closed. Digikala’s demand for same-day fulfillment has spurred last-mile tech such as route-optimization AI and smart lockers.

Gaming and Esports remains the fastest-growing vertical at 4.74% CAGR as 5G low latency and cheaper GPUs spawn local studios and competitive leagues. Energy and utilities accelerate digital twins to curb gas flaring, while BFSI invests in blockchain-based trade finance to bypass currency bottlenecks. Healthcare adopts tele-diagnostics, building resilience learned during pandemic-era restrictions, further expanding opportunities across the Iran ICT market.

Geography Analysis

Domestic demand clusters around Tehran, which houses most datacenters, vendor HQs, and regulatory bodies. The capital’s 20-million-household fiber plan, slated for completion in March 2026, promises gigabit access that feeds cloud service uptake and AI training nodes. Universities such as Sharif and Tehran Polytechnic supply constant engineering talent to these hubs.

Secondary cities including Isfahan, Mashhad, and Shiraz nurture growing tech parks and micro-electronics clusters that diversify regional supply chains. Local governments co-fund incubators, easing the path for SaaS startups targeting provincial manufacturing SMEs. Mobile operators extend 5G small cells along intercity highways, opening IoT corridors for fleet telematics and cold-chain monitoring in agriculture, reinforcing depth across the Iran ICT market.

Free-trade zones in Kish and Chabahar offer duty-free imports, 20-year tax holidays, and 100% foreign ownership, attracting data-assembly and refurbishment ventures. [3]Najma Tejareh, “Chabahar Free Zone Trade,” najma-tejareh.com Kish’s smart-city blueprint showcases connected-tourism pilots, while Chabahar positions itself as a redundancy landing point on the Asia-Europe terrestrial fiber route. Joint backbone projects with Russia add northern capacity, integrating Iran into emerging Eurasian digital corridors and broadening geographic diversification inside the Iran ICT market.

Competitive Landscape

Iran’s ICT arena is moderately concentrated in connectivity but fragmented in software and services. MTN Irancell, MCI, and Rightel account for the majority of mobile subscribers, allowing scale economies in 5G and fiber roll-outs. System Group, Iran’s first listed IT firm, posted 54.71% revenue growth in 2025 by bundling ERP, BI, and RPA solutions for more than 60 industry verticals.

Strategic moves emphasize vertical integration and local sourcing. FANAP Infrastructure deploys private-LTE rigs and edge-cloud nodes for manufacturing clients, complementing its fintech unit that processes micro-loans for ride-hailing fleets. MTN Irancell’s April 2025 fiber program commits 525 billion IRR in Andisheh and 200 billion IRR in Bandar Dayyer, tying residential broadband to smart-home bundles.

Emergent challengers-many spun out of university labs-specialize in AI acceleration, low-code platforms, and Persian-language NLP, areas underserved by global giants due to sanctions. The talent pipeline, however, faces ongoing outflows to Gulf employers that offer higher pay in stable currencies, compelling firms to deploy ESOPs and remote-work policies to retain engineers within the Iran ICT market.

Iran ICT Industry Leaders

-

Microsoft Corporation

-

Alphabet Inc.

-

Cisco Systems Inc.

-

SAP SE

-

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Russia and Iran ratified a strategic ICT pact that covers joint satellites, traffic-routing, and secure-Internet initiatives.

- April 2025: Irancell began FTTH works in Andisheh and Bandar Dayyer worth 725 billion IRR combined.

- February 2025: MCI unveiled a new brand reflecting a pivot toward AI, IoT, and XR services.

- January 2025: Tehran budgeted USD 115 million for a National AI Organization with a ten-year road map.

Iran ICT Market Report Scope

Information and communication technologies or ICT is a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form. The revenue tracks the product offerings provided by the companies.

The Iranian ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprises (small and medium enterprises and large enterprises), and industry verticals (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

How large is the Iran ICT market in 2025?

It is valued at USD 24.91 billion and projected to hit USD 30.18 billion by 2030.

What CAGR is expected for Iran’s cloud segment?

Cloud revenue is forecast to rise at a 4.13% CAGR between 2025 and 2030.

Which customer group spends the most on ICT solutions?

SMEs represent 56.63% of 2024 demand and show the fastest growth pace.

Why is 5G important for Iranian businesses?

Rapid 5G roll-out adds low-latency capacity that underpins IoT, mobile commerce, and edge-cloud services.

How are sanctions shaping technology procurement?

Restrictions push firms toward domestically built hardware, localized SaaS, and regional alliances with Russia to secure advanced capabilities.

Page last updated on: