Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

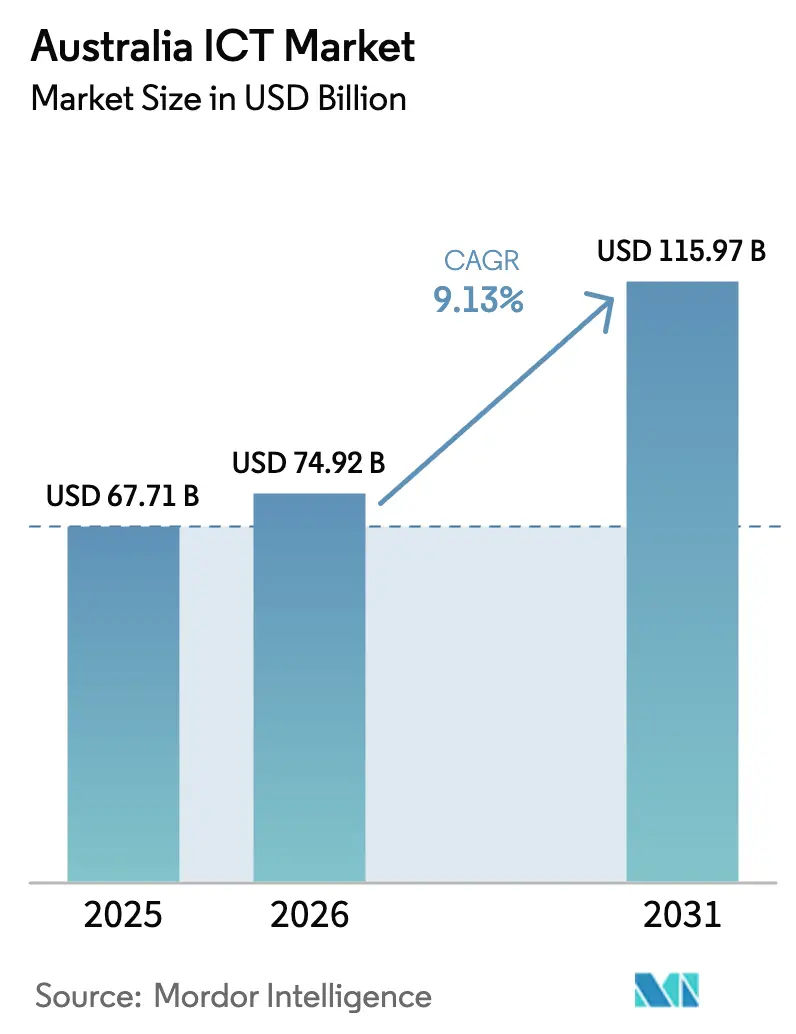

| Base Year Market Size (2025) | USD 67.71 Billion |

| Market Size (2026) | USD 74.92 Billion |

| Market Size (2031) | USD 115.97 Billion |

| Growth Rate (2026 - 2031) | 9.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia ICT Market Analysis by Mordor Intelligence

The Australia ICT Market size was valued at USD 67.71 billion in 2025 and is estimated to grow from USD 74.92 billion in 2026 to reach USD 115.97 billion by 2031, at a CAGR of 9.13% during the forecast period (2026-2031). Robust public-sector digital mandates, sovereign-cloud requirements, and expanding hyperscale footprints are reinforcing domestic data-center builds and accelerating cloud migration. Enterprise spending is further buoyed by the intensified Notifiable Data Breaches regime, which has redirected budgets toward managed security and zero-trust architectures. Telco 5G stand-alone cores now enable network slicing, unlocking edge-computing use cases in mining, logistics, and healthcare. In parallel, the Moon to Mars initiative is driving demand for high-performance computing that ripples through storage and networking suppliers. Counterbalancing these tailwinds, a widening talent gap and regional broadband inequalities threaten to slow project delivery and cloud-based collaboration.

Key Report Takeaways

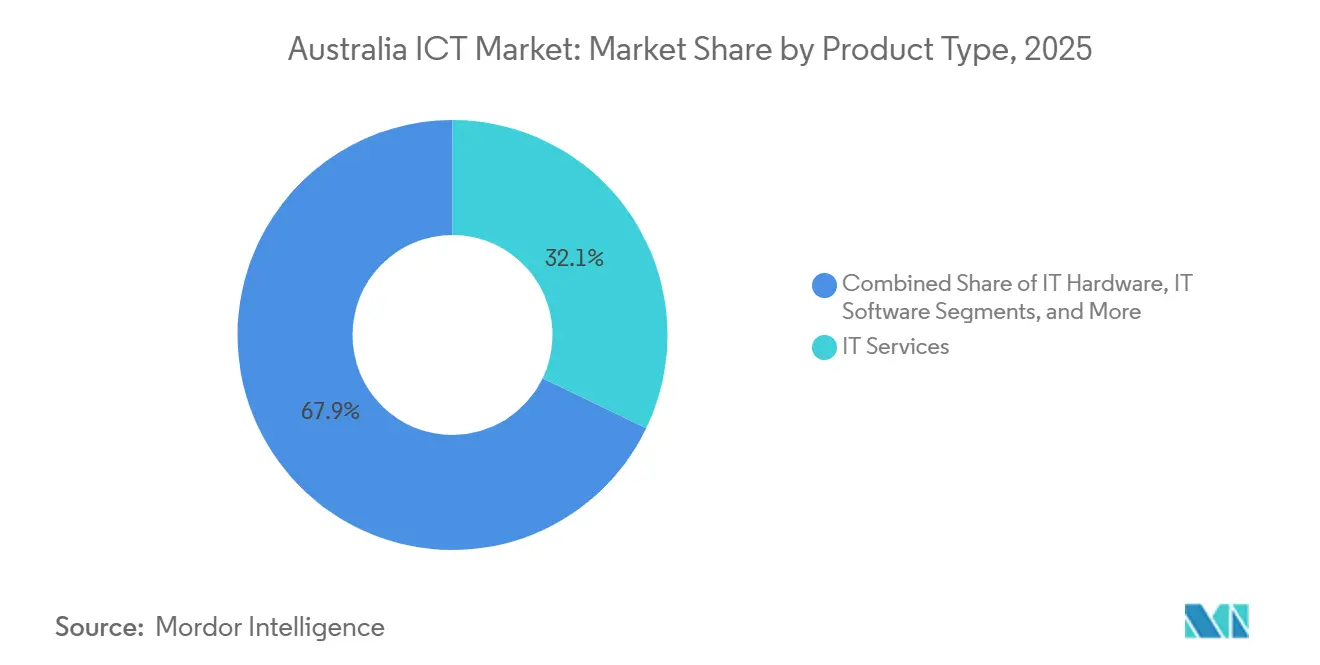

- By product type, IT Services led with 32.13% revenue share in 2025, while Cloud and Platform Services is advancing at a 10.74% CAGR through 2031.

- By enterprise size, Large Enterprises held 57.46% of the Australia ICT market share in 2025, whereas SMEs are set to grow at 10.11% annually to 2031.

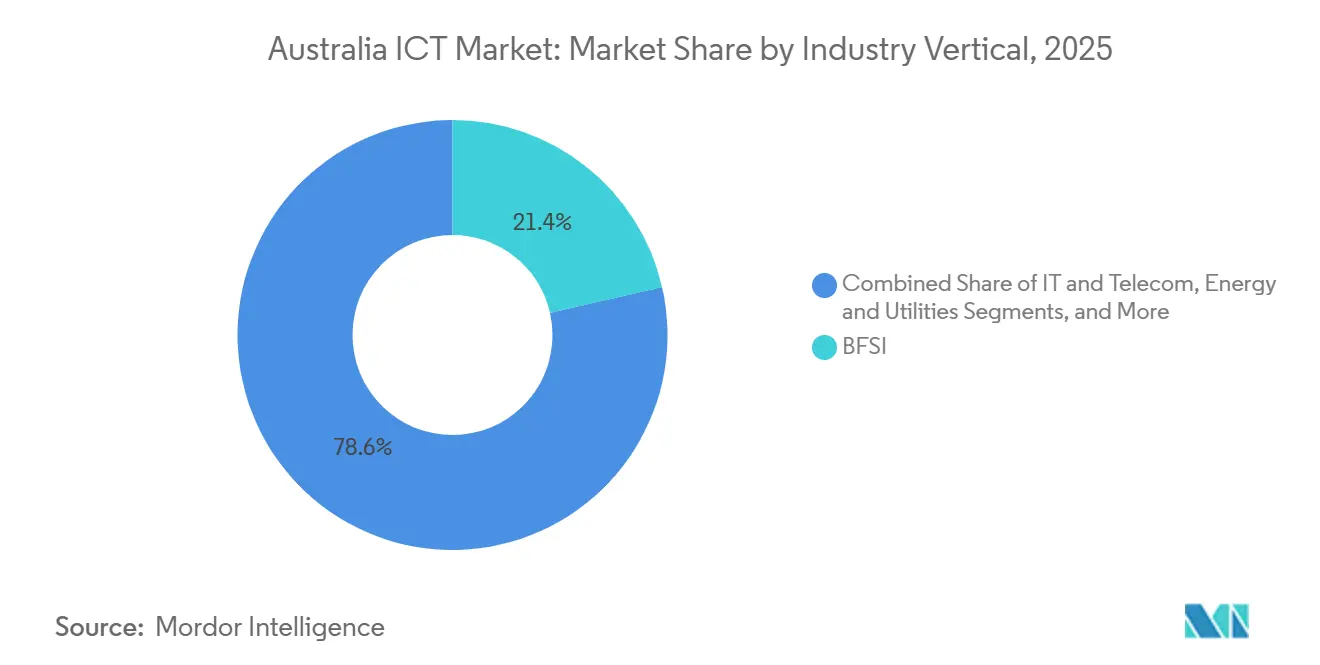

- By industry vertical, BFSI captured 21.43% of 2025 spend, but Healthcare and Life Sciences is expanding at a 10.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Government Digital Transformation Programs | +2.1% | National, concentrated in Australian Capital Territory, New South Wales, Victoria | Medium term (2-4 years) |

| Rapid Cloud Computing Adoption Across Enterprises | +2.4% | National, with early gains in Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Expansion of 5G Networks Enabling Next-Gen Applications | +1.8% | National, urban centers in New South Wales, Victoria, Queensland leading | Medium term (2-4 years) |

| Rising Cybersecurity Threats Boosting Security Spend | +1.6% | National, heightened focus in BFSI and Government sectors | Short term (≤ 2 years) |

| Australia's Emerging Space Industry Driving HPC Demand | +0.7% | South Australia, Australian Capital Territory, Western Australia | Long term (≥ 4 years) |

| Data Sovereignty Mandates Fueling Local Data Center Investment | +1.5% | National, concentrated in New South Wales, Victoria, Australian Capital Territory | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Government Digital Transformation Programs

Whole-of-government targets require 80% of unclassified workloads to operate in IRAP-assessed clouds by June 2027, channeling AUD 1.2 billion (USD 809 million) toward SaaS licenses and API gateways in the 2025-26 federal budget.[1] Federal and state agencies are consolidating 147 procurement contracts into a single framework that favors ISO 27001-certified vendors, thereby elongating multi-year transformation pipelines. Services Australia’s myGov re-platforming exemplifies identity federation spanning 32 portals, and state-level digital restart funds replicate this model for land-title and court systems. The result is sustained demand for change-management consultants and UX designers, roles historically under-resourced in public projects.

Rapid Cloud Computing Adoption Across Enterprises

APRA’s revised CPS 234 compels quarterly penetration tests and seven-year log retention, encouraging FSIs to shift core apps into multi-AZ cloud patterns. AWS added 50 MW in its fourth Sydney zone in 2025, while Google Cloud committed AUD 2 billion (USD 1.35 billion) to Melbourne data halls powered entirely by wind energy. Mid-market adoption is visible; 62% of manufacturers with 50-500 employees had at least one cloud ERP module live in 2025, up from 41% in 2023, citing faster time-to-value. Yet identity management across AWS, Azure, and Google now absorbs up to 40% of cloud-ops budgets, making policy automation a new spending hotspot.

Expansion of 5G Networks Enabling Next-Gen Applications

Telstra finalized its 5G stand-alone core in June 2025, unlocking network slicing for mining and logistics, where latency-sensitive control loops govern autonomous haul trucks. Optus followed with millimeter-wave cells in Sydney’s CBD, enabling 4.5 Gbps peaks for AR retail showcases. ACMA’s 26 GHz spectrum auction spurred private 5G builds; BHP’s Olympic Dam network integrated 1,200 IoT sensors and cut downtime 18% within six months. Edge partnerships, such as AWS Wavelength in Telstra cores, now deliver sub-10 ms latency for gaming and telemedicine.

Rising Cybersecurity Threats Boosting Security Spend

Cybercrime reports hit 94,000 in FY 2024-25, up 23% year-on-year, and new privacy penalties rise to the greater of USD 33.7 million or 30% of turnover. Managed security contracts rose 34% for NTT Ltd., underscoring a pivot from product to service-led defense. The ASD partnership program now exchanges classified indicators for vendor telemetry, tightening patch cycles. Zero-trust adoption accelerated 47% of ASX 200 firms using microsegmentation in 2025, up from 29% in 2023, reflecting board-level prioritization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage of Advanced IT Talent | -1.4% | National, most severe in cybersecurity and cloud architecture roles | Short term (≤ 2 years) |

| Legacy Infrastructure Complexity in Large Enterprises | -0.9% | National, concentrated in BFSI, Government, Energy sectors | Medium term (2-4 years) |

| High Broadband Costs in Remote Regions | -0.5% | Northern Territory, Western Australia, Queensland regional areas | Long term (≥ 4 years) |

| Stringent E-waste Regulations Increasing Compliance Cost | -0.3% | National, affecting IT Hardware and Infrastructure segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Advanced IT Talent

ICT unemployment stood at 1.8% in December 2025, well below the national rate of 3.9%, highlighting structural scarcity.[2]Australian Bureau of Statistics, “Labour Force Survey December 2025,” abs.gov.au Cybersecurity analysts earn a median AUD 135,000 (USD 91,000), yet roles remain vacant for 14 weeks on average. Visa backlogs hinder offshore recruitment, and although universities are scaling cybersecurity cohorts by 40%, graduations will not bridge the gap before 2028. Cost escalation and project delays are already evident as integrators over-commit on delivery timelines.

Legacy Infrastructure Complexity in Large Enterprises

Mainframe estates with COBOL codebases exceeding 10 million lines still process billions of transactions monthly, exemplified by Commonwealth Bank’s z/OS core. Regulatory stress-test mandates discourage rip-and-replace migrations, funneling budgets into middleware for incremental modernization. Hybrid integration raises licensing costs and adds failure points, complicating root-cause analysis during outages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Anchor Spend, Cloud Platforms Drive Momentum

IT Services captured a 32.13% slice of 2025 spending as enterprises leaned on integrators for multi-cloud navigation and regulatory alignment. Within IT Services, managed security and business process outsourcing are converging, with providers knitting threat intelligence into HR and finance workflows, elevating stickiness among mid-market clients. IT Services are forecast to post the fastest CAGR of 10.74% to 2031, driven by cloud and platform services fueled by consumption-based economics and a maturing ecosystem of PaaS abstractions that trim infrastructure overhead. Selective hardware refresh persists when performance gains are material, such as Cisco’s silicon photonics switches that reduce power by 40%, yet overall hardware budgets flatten as device-as-a-service shifts capex to opex.

Hyperconverged infrastructure now dominates new storage procurement, with Dell reporting 38% of Australian storage revenue in fiscal 2025 derived from VxRail and PowerFlex. Security spend remains the outlier, outpacing overall Australia ICT market size growth as essential-eight compliance drives upgrades to EDR and SIEM platforms.[3]Dell Technologies, “Australia VxRail Revenue Share,” dell.com Communication services revenue is migrating from voice to SD-WAN and unified comms, and telcos are bundling these with sovereign-cloud connectivity to defend margins. Consulting benches stay busy with generative-AI pilots, yet routine integration is commoditizing under AI-assisted tooling.

By Enterprise Size: Large Enterprises Command Budgets, SMEs Accelerate Adoption

Large Enterprises accounted for 57.46% of 2025 outlays, with investment focused on governance, master data management, and robust API gateways. Their complex estates elevate demand for Australia ICT market size-linked integration budgets and professional services retainer models. SMEs, aided by 50% migration subsidies, are projected to compound at 10.11% annually to 2031. Turnkey SaaS bundles cloud accounting, inventory, and payroll, lower entry barriers, and vendors like Xero report double-digit subscriber growth as average revenue per user rises with module attach.

Security postures diverge sharply; large firms allocate 8-12% of ICT budgets to cybersecurity, often staffing internal SOCs, whereas SMEs lean on managed detection and response subscriptions priced under AUD 15,000 (USD 10,110) per month. Telstra’s Essential Cyber package exemplifies security subscriptions tailored for SMEs. 34% of ASX 200 companies piloted large-language-model assistance in 2025, versus 9% of SMEs, but falling model-training costs should narrow this divide.

By Industry Vertical: BFSI Still Dominant, Healthcare Surges

BFSI retained 21.43% of 2025 spend for mandatory compliance tooling, fraud analytics, and mobile-banking upgrades. Yet Healthcare and Life Sciences is the standout growth area, expanding at a 10.92% CAGR under the My Health Record interoperability mandate, which requires FHIR-compliant APIs by December 2026. In mining-centric states, energy and utilities channel funds into grid digitization and distributed energy resource management, aligning with the Integrated System Plan. Retail and logistics sectors adopt warehouse robotics and AI-driven last-mile routing, curbing labor costs and boosting delivery predictability.

Manufacturing’s Industry 4.0 shift embeds IoT sensors and predictive analytics across production lines, cutting unplanned downtime and sharpening maintenance cycles. Government workloads constitute high-value demand for identity assurance and case-management systems, while oil and gas players deploy digital twins to optimize offshore production. These varied but convergent vertical demands ensure the Australia ICT market remains resilient against cyclical shocks.

Geography Analysis

New South Wales led national spend in 2025, powered by Sydney’s finance headquarters, hyperscale data-centers, and dense startup corridor. The state’s AUD 1.5 billion (USD 1.06 billion) Digital Restart Fund funds mainframe replacement and microservice adoption, catalyzing long-tail opportunities for local integrators. Victoria follows closely; Melbourne hosts sovereign-cloud regions for AWS, Microsoft, and Google, and combined hyperscale investment topped AUD 7 billion (USD 4.92 billion) from 2024-2026. Victoria’s green power commitments help firms meet net-zero targets without purchasing offsets.

Queensland harnesses the 2032 Brisbane Olympics as a springboard for smart-city infrastructure and 5G-enabled public transport. Western Australia’s mining automation drives roughly 40% of the state's ICT outlays, focusing on private 5G and edge analytics to support autonomous haulage. South Australia is emerging as a space-tech hub, anchored by the Australian Space Agency, attracting HPC vendors and communications startups. Tasmania leverages its cool climate and renewable energy to attract data center operators such as CDC to Hobart for low-PUE colocation.

Australian Capital Territory’s spend is government-centric, consolidated through DTA’s cloud framework that favors IRAP-Protected suppliers. Northern Territory trails due to sparse fiber, yet Darwin’s subsea-cable landing stations tighten latency to Southeast Asia, enabling real-time replication for disaster recovery. Despite progress, regional connectivity gaps remain, NBN’s fixed-wireless tier delivers median 48 Mbps to 1.2 million premises, limiting cloud-CAD and high-definition video. The government’s Regional Connectivity Program funds fiber to 400 towns, yet timelines extend to 2028, prolonging the digital divide.

Competitive Landscape

The Australia ICT market is moderately concentrated; the top 10 players command a major share of revenue, leaving a vibrant tail of niche vendors. Telstra combines ubiquitous connectivity with managed cloud and security services, leveraging its Digicel Pacific acquisition to bundle subsea capacity with edge nodes, yet margin pressure grows as hyperscalers negotiate direct peering. AWS, Microsoft, and Google compete on sovereign-cloud credibility; Microsoft’s pledge to store government data exclusively in IRAP zones forces rivals to match residency and compliance assurances.

Indian integrators Infosys, Wipro, and Tata Consultancy Services undercut on price while embedding AI co-pilots in modernization projects, compressing delivery timelines but commoditizing integration labor. Incumbents such as Accenture and DXC counter with industry-specific playbooks and change-management depth. Edge computing, private 5G, and quantum-safe cryptography surface as white-space segments; ASD’s 2025 quantum-resistant roadmap sparks early consulting engagements as agencies prepare algorithm migrations.

Telstra bought Versent to deepen professional services, NTT acquired Nexon for security scale, and Cisco-Accenture co-develop SD-WAN patterns for retail. Vertical SaaS specialists achieve 60-70% gross margins by fusing workflow expertise with narrow domains livestock management or hospital rostering that hyperscalers overlook. Collectively, these dynamics ensure sustained innovation and price competition across the Australia ICT market.

Australia ICT Industry Leaders

Telstra Corporation Limited

Microsoft Corporation

IBM Corporation

Amazon Web Services Inc.

Alphabet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft began phase-one construction of three new Azure availability zones, with completion slated for Q4 2027, and launched a national AI-skills academy targeting 300,000 participants by 2028.

- November 2025: Amazon Web Services activated Local Zones in Perth, adding 20 MW of renewable-powered capacity for latency-sensitive workloads.

- October 2025: Telstra finalized nationwide 5G stand-alone core, enabling sub-10 ms slices for industrial IoT.

- September 2025: Optus completed millimeter-wave rollout across Sydney CBD, achieving 4.5 Gbps peaks for AR retail pilots.

Australia ICT Market Report Scope

The Australia ICT Market Report is Segmented by Product Type (IT Hardware [Computer Hardware, Networking Equipment, and Peripherals]. IT Software (IT Services [IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, and Cloud and Platform Services] IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), and Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

What is the projected value of the Australia ICT market in 2031?

The market is forecast to reach USD 115.97 billion by 2031, growing at a 9.13% CAGR from 2026.

Which segment shows the fastest growth within national ICT spending?

Cloud and Platform Services lead with a 10.74% CAGR forecast through 2031.

Why are SMEs increasing their ICT budgets more rapidly than large enterprises?

Government co-investment grants subsidize up to 50% of cloud migration costs, accelerating SME adoption of SaaS and security subscriptions.

How does 5G deployment influence enterprise technology strategies in Australia?

Stand-alone 5G cores and millimeter-wave rollouts enable low-latency edge applications, prompting investments in private networks for mining, logistics, and AR retail.

What are the primary challenges restraining ICT growth across Australia?

A shortage of advanced IT talent and the complexity of legacy mainframe infrastructures slow transformation timelines and raise project costs.

Which state currently accounts for the largest share of ICT expenditure?

New South Wales holds the largest share, underpinned by Sydney’s financial services and dense hyperscale data-center footprint.

Page last updated on: