Cloud Supply Chain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

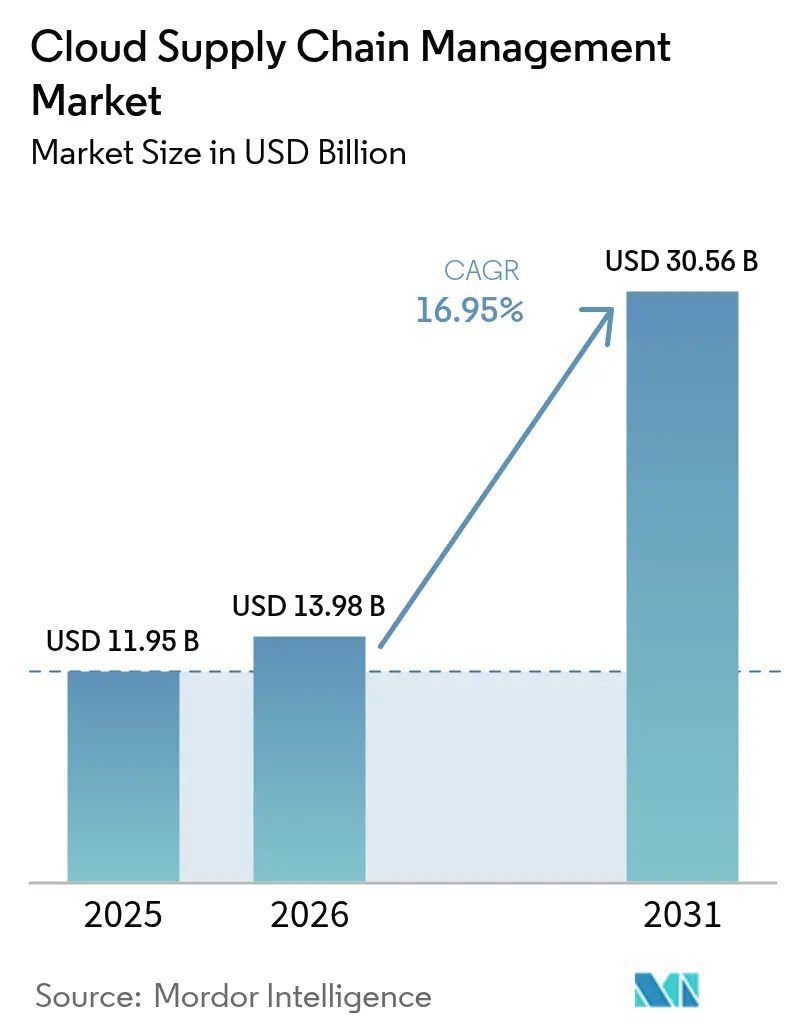

| Market Size (2026) | USD 13.98 Billion |

| Market Size (2031) | USD 30.56 Billion |

| Growth Rate (2026 - 2031) | 16.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Supply Chain Management Market Analysis by Mordor Intelligence

The cloud supply chain management market size is expected to grow from USD 11.95 billion in 2025 to USD 13.98 billion in 2026 and is forecast to reach USD 30.56 billion by 2031 at 16.95% CAGR over 2026-2031. Rapid migration from capital-intensive on-premise suites to consumption-based SaaS platforms, coupled with the demand for real-time visibility, is the primary catalyst. Large enterprises continue to drive core spending, yet small and medium enterprises are accelerating adoption as subscription pricing removes upfront license barriers. Transportation and logistics users prioritize end-to-end freight tracking, while digital twin planning and carbon-accounting modules are unlocking new use cases. Competitive intensity remains moderate, as no single vendor holds more than a 15% market share in cloud supply chain management, creating opportunities for niche specialists.

Key Report Takeaways

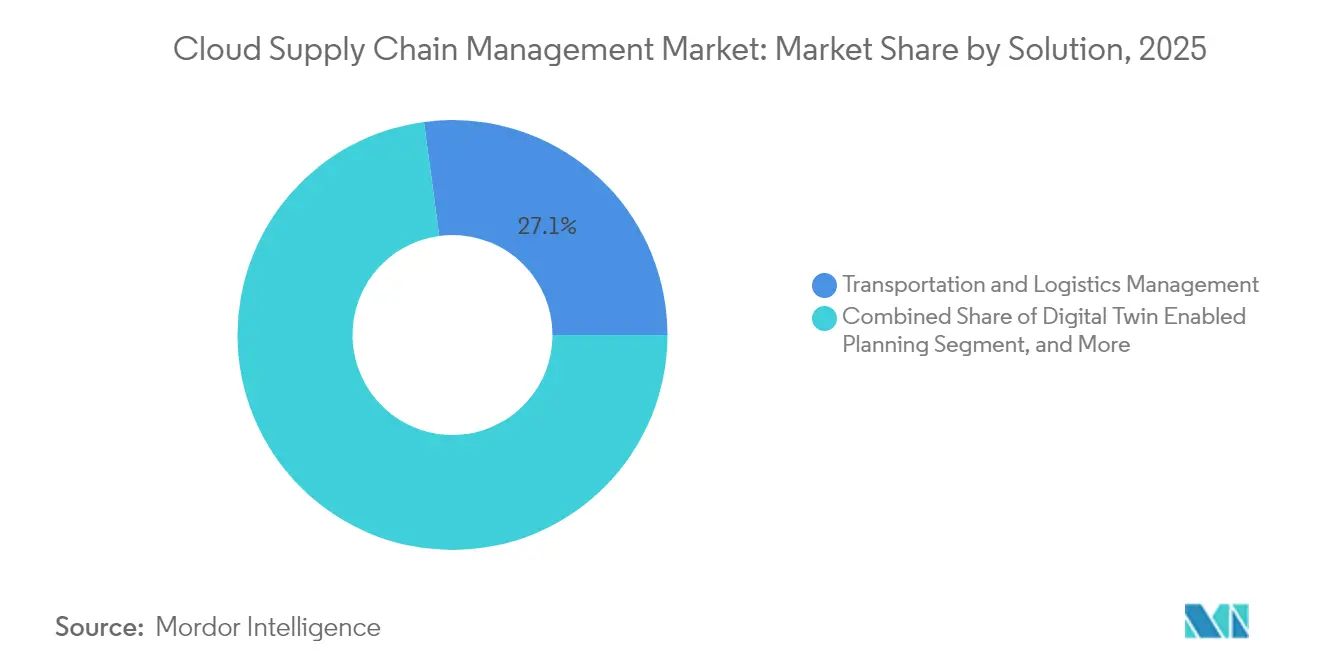

- By solution, Transportation and Logistics Management led with a 27.12% cloud supply chain management market share in 2025, while Digital Twin Enabled Planning is forecast to grow at 21.25% CAGR to 2031.

- By deployment type, Public Cloud captured 60.58% of the revenue in 2025; Hybrid Cloud is expected to expand at a 19.05% CAGR through 2031.

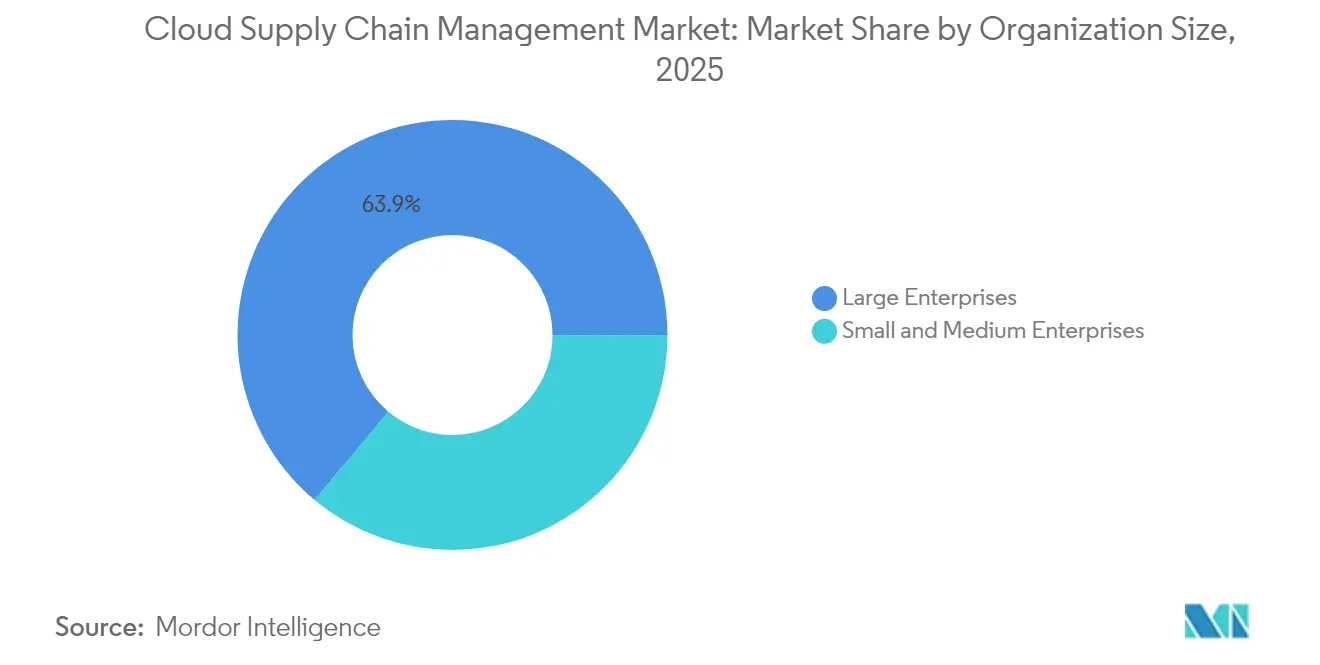

- By organization size, large enterprises held a 63.92% share in 2025, whereas Small and Medium Enterprises are advancing at a 19.60% CAGR to 2031.

- By end-user industry, the Retail Sector led with a 22.98% revenue share in 2025; the healthcare sector is projected to post a 21.60% CAGR from 2025 to 2031.

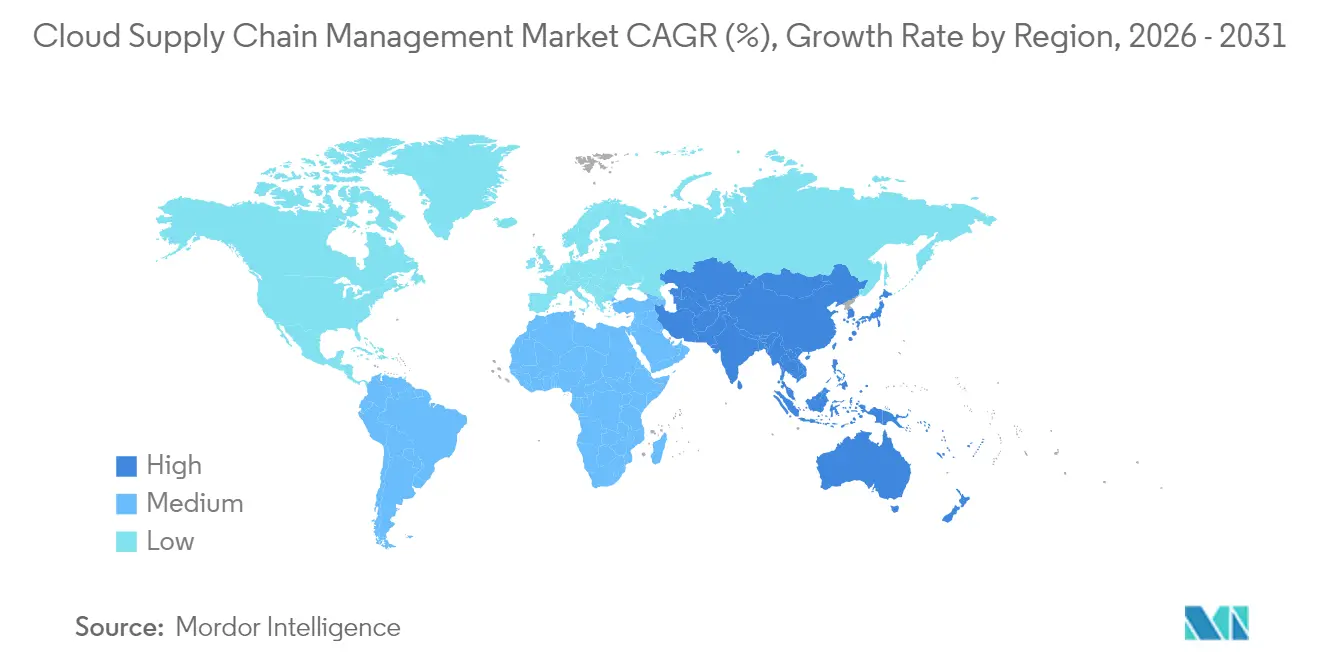

- By geography, North America accounted for 34.41% of 2025 revenue, and the Asia Pacific is anticipated to record an 18.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Supply Chain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Based Solutions for Demand Planning | +3.2% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of E Commerce Requiring Agile Supply Networks | +2.8% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| Cost Efficiency and Scalability Driving Migration from On-Premise SCM | +3.5% | Global, particularly strong in Small and Medium Enterprises across all regions | Medium term (2-4 years) |

| Integration of Digital Twins for Real-Time Supply Chain Simulation | +2.4% | North America and Europe core, expanding to the Asia Pacific manufacturing hubs | Long term (≥ 4 years) |

| Rising Carbon Accounting Mandates Promoting Cloud Visibility Platforms | +1.9% | Europe is primary, North America is secondary, and the Asia Pacific is emerging. | Medium term (2-4 years) |

| Vendor Transition to Composable Microservices: Accelerating Upgrades | +2.1% | Global, with early adoption in the technology and retail sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based Solutions for Demand Planning

Organizations replacing spreadsheets with cloud-native forecasting gain hourly demand-signal refreshes, fed by point-of-sale feeds, weather APIs, and social media sentiment. Generative AI now lets planners interrogate forecasts in natural language and simulate promotional lifts. Even minor accuracy gains cut safety stock by double-digit percentages, releasing working capital. Retail and consumer-goods leaders paved the way, but adoption is broadening as cloud data lakes support a secure, tenant-isolated model for machine learning and training.[1]SAP, “SAP Integrated Business Planning,” sap.com

Expansion of E Commerce Requiring Agile Supply Networks

With e-commerce penetration expected to reach 21% of retail sales by 2024, brands must orchestrate distributed inventory to meet same-day commitments. Cloud supply chain management market platforms route orders to the closest node, minimizing split shipments. Pre-built connectors link fulfillment centers, parcel carriers, and customs brokers, automating landed-cost calculations and returns processing across dozens of jurisdictions. The capability is critical for cross-border sellers managing baskets under USD 50.

Cost Efficiency and Scalability Driving Migration from On-Premise SCM

On-premise suites command license fees that can exceed USD 5 million plus annual maintenance. Subscription pricing converts capex to opex at USD 100-500 per user per month, while seasonal compute bursts are handled elastically. Blue Yonder reported 78% of 2024 bookings were subscription-based, up from 52% in 2020.[2]Blue Yonder, “Annual Report 2024,” blueyonder.com SMEs, in particular, leverage shared-tenant economics to tap into functions once reserved for Fortune 500 companies.

Integration of Digital Twins for Real-Time Supply Chain Simulation

Digital twins mirror multi-echelon networks, ingesting live IoT sensor data, port congestion indices, and supplier transactions. Siemens modeled 12,000 suppliers and 300 distribution centers to stress-test semiconductor shortages in 2024.[3]Siemens, “Digital Twin for Supply Chain Management,” siemens.com The practice reduces expedited freight, maintains service levels, and prevents line stoppages in aerospace and automotive production. Cloud infrastructure supplies the compute cycles needed for hourly Monte Carlo runs that on-premise servers cannot match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Security and Data Privacy Concerns | -1.8% | Global, with acute sensitivity in Europe and the Asia Pacific | Short term (≤ 2 years) |

| Complex Legacy Systems Hindering Cloud Migration | -2.3% | North America and Europe, particularly in the manufacturing and oil and gas sectors | Medium term (2-4 years) |

| Shortage of Cloud Native Supply Chain Talent | -1.5% | Global, most severe in North America and Europe | Long term (≥ 4 years) |

| Increasing Sovereign Cloud Requirements: Fragmenting Deployments | -1.2% | Europe, China, the Middle East, with emerging requirements in India and Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Security and Data Privacy Concerns

Multi-tenant architectures concentrate sensitive pricing, forecast, and shipment data. A 2024 breach at a logistics software provider exposed manifests for 40,000 customers, elevating scrutiny on encryption, access controls, and data-residency compliance. The European Union's GDPR and China’s Personal Information Protection Law complicate cross-border transfers, prompting some firms to opt for private regions or customer-managed keys. Added controls increase vendor costs and can slow the deployment of cloud supply chain management.[4]European Union, “General Data Protection Regulation,” gdpr.eu

Complex Legacy Systems Hindering Cloud Migration

Enterprises often run 8-12 bespoke supply chain applications lacking modern APIs. Cleansing master data, re-engineering workflows, and validating regulated processes extend project timelines and inflate budgets. A Deloitte survey found that 64% of migrations were missed by six months or more. Life-science and aerospace firms face additional validation requirements from regulators such as the U.S. FDA, which can double or triple total migration costs relative to annual subscription outlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Transportation Visibility Sustains Leadership

Transportation and Logistics Management contributed the largest slice of the cloud supply chain management market, holding 27.12% of the revenue in 2025. Shippers rely on real-time estimated arrival times, dynamic route optimization, and carrier performance dashboards to optimize their operations. Electronic logging device mandates in North America and tachograph rules in Europe feed telematics data that elevates predictive ETAs. Digital freight marketplaces interface through open APIs, letting planners benchmark rates across modes without manual tenders. Demand Planning and forecasting are on the rise as retailers integrate external variables, such as weather and social sentiment, to minimize excess stock. Inventory and Warehouse Management now embeds computer vision for cycle counting, reducing labor in high-velocity DCs. Product Lifecycle Management (PLM) modules have expanded into process industries, linking recipe revisions to compliance records. Sales and Operations Planning integrates finance links, allowing volume and revenue forecasts to be reconciled in a single cockpit. Procurement modules inject supplier risk scores that mix financial health, ESG ratings, and geopolitical exposure. Order Management engines orchestrate multichannel fulfillment using fill-rate, margin, and delivery-promise logic. Product Master Data Management increasingly leverages blockchain to build immutable provenance chains.

Digital Twin Enabled Planning, advancing at a 21.25% CAGR, is the fastest-growing solution subsegment. Pharmaceutical, semiconductor, and heavy-industrial firms construct network graphs that simulate disruptions across multi-tier bills of material. Planners can test alternate sourcing or buffer stock moves virtually before committing inventory. Graph databases spotlight single-point-of-failure suppliers, while cloud compute executes thousands of Monte Carlo scenarios hourly. The capability gained prominence after 2024 component shortages halted assembly lines worldwide, prompting firms to adopt scenario-driven operating models.

By Deployment Type: Public Cloud Dominates, Hybrid Accelerates

Public Cloud held 60.58% of the cloud supply chain management market in 2025. Organizations prize the vendor-managed infrastructure and speed of activation, avoiding 6-12 month on-premise projects. Regional data centers spread across more than 30 countries ensure data residency and sub-10 ms latency for operational workflows. Private Cloud persists among defense and energy firms, protecting classified diagrams or seismic data. These environments utilize hypervisor or OpenStack layers to simulate elastic scaling within corporate firewalls.

Hybrid Cloud, projected to grow 19.05% CAGR, balances governance and agility. Pharmaceutical companies store clinical trial protocols and patient data on private nodes validated under Good Clinical Practice, while offloading analytics workloads to public tenants during quarterly S&OP cycles. Offerings such as AWS Outposts and Azure Stack extend managed services on-premise, enabling consistent tooling. The model depends on event-stream integration to synchronize master data without stale reads. Certified controls under ISO 27001 and SOC 2 underpin audit readiness and influence deployment choices.

By Organization Size: SMEs Close the Gap

Large Enterprises represented 63.92% of the 2025 value as they harmonize global networks spanning thousands of suppliers. Automotive OEMs deploy multi-tier control towers, feeding component availability into production scheduling weeks ahead of freeze dates. Enterprise-grade SLAs with 99.9% uptime and outage compensation remain mandatory. Functional depth, such as hazardous-material routing or serialization for biologics, often dictates vendor shortlists.

Small and Medium Enterprises are forecast to expand at a rate of 19.60% annually, narrowing the functionality gap. Entry packages bundle best-practice workflows and pre-built ERP connectors, cutting consulting spend. API marketplaces let Shopify or WooCommerce merchants plug in route optimization and inventory sync without coding. Democratization means regional distributors can provide shipment visibility that matches that of large rivals. Community forums and self-service documentation address the scarcity of dedicated IT staff. For many SMEs, cloud supply chain management market adoption now coincides with the introduction of the first professional inventory system, rather than a replacement of legacy tools.

By End-User Industry: Retail Holds Lead, Healthcare Surges

Retail commanded a 22.98% share in 2025. Omnichannel fulfillment requires SKU-level visibility across stores, DCs, and supplier hubs to present accurate promise dates at checkout. Fashion players leverage allocation algorithms to minimize markdowns by throttling replenishment on slow-moving variants. Grocery chains utilize machine-learning-driven fresh food replenishment, tailored to spoilage curves, thereby curbing waste.

Healthcare is the fastest climber with a 21.60% CAGR to 2031. Serialization mandates under the U.S. Drug Supply Chain Security Act demand unit-level traceability, and cloud platforms scan barcodes at every hand-off. Temperature-controlled biologics rely on IoT sensors that feed cloud dashboards, triggering alerts for excursions. Hospital group purchasing organizations adopt cloud procurement to aggregate volume, reduce maverick buys, and enforce formulary compliance. Cold-chain trends intensify technology requirements, prompting pharmaceutical and vaccine manufacturers to adopt real-time lane monitoring.

Geography Analysis

North America delivered 34.41% of 2025 revenue. U.S. Customs and Border Protection’s Automated Commercial Environment APIs automate customs entry creation, lowering brokerage costs for importers. Early hyperscaler buildouts ensure low-latency access for time-sensitive control towers and freight visibility dashboards. Canada’s Safe Food for Canadians Regulations push agri-food exporters to establish farm-to-fork traceability, spurring cloud investments. Mexico’s near-shoring trend has electronics and auto assemblers digitizing supplier collaboration to bypass Pacific shipping risks.

The Asia Pacific is poised for the fastest regional growth, with an 18.05% CAGR. Contract manufacturers in China, India, and Vietnam digitize tier-2 and tier-3 partners to meet just-in-time milestones set by global brands. China’s Belt and Road rail corridors heighten the need for multi-modal route optimization. India’s fully digital Goods and Services Tax e-invoicing feeds cloud systems that reconcile tax liabilities in real time. Japan’s aging driver population fuels the adoption of AI-powered route consolidation, while Australia’s commodity exporters automate export documentation to speed vessel bookings.

Europe maintains a significant uptake, owing to the GDPR and the Corporate Sustainability Reporting Directive, which embeds compliance functionality into vendor RFPs. Germany’s automotive sector employs constraint-based planning to manage multi-tier capacity. The United Kingdom’s post-Brexit rules accelerate the adoption of automated tariff classification. France’s luxury segment relies on short seasonal calendars and uses demand sensing to slash markdowns. Russia’s data-localization law remains a barrier, steering companies to domestic cloud alternatives that add latency for global partners.

Competitive Landscape

The cloud supply chain management industry remains moderately fragmented, with no provider holding a significant share. Incumbent ERP vendors, SAP, Oracle, and Infor, cross-sell cloud modules into their established customer bases, bundling contracts to defend their market share. Pure-play specialists, including Blue Yonder, Manhattan Associates, and Kinaxis, compete through algorithmic depth in demand sensing, warehouse slotting, and concurrent planning. Emerging players, such as o9 Solutions and Verusen, embed machine learning for automatic forecast tuning and material risk scoring, differentiating themselves with faster time to value.

Platform ecosystems are a defining trend. Vendors curate marketplaces for ocean booking, trade compliance, or carbon calculators, letting buyers assemble best-of-breed stacks without custom code. Blue Yonder’s 2024 partnership with Microsoft Azure delivered retail and manufacturing data models pre-mapped to Azure data services. Kinaxis patented concurrent scenario editing, which allows multiple planners to adjust plans in real-time, thereby solving versioning pain points.

Regional expansion strategies intensify competition. Pure-plays chase Southeast Asia and Latin America by adding language packs, local tax logic, and regionally hosted nodes to meet data-sovereignty laws. Defensive moves include SAP extending its hyperscaler footprint in Saudi Arabia and Brazil, and Oracle acquiring Cleo for faster EDI onboarding of mid-market manufacturers. Mergers continue as larger suites buy logistics specialists to fill gaps quickly, exemplified by E2open’s 2025 purchase of Blume Global.

Cloud Supply Chain Management Industry Leaders

SAP SE

Oracle Corporation

Infor Inc

Descartes Systems Group Inc

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Körber Supply Chain Software opened a research and development center in Bangalore, India, to develop artificial intelligence-driven warehouse optimization algorithms.

- October 2025: Project44 expanded its real-time freight visibility network to include over 1,200 ocean carriers and 500 air cargo operators.

- September 2025: Logility launched a demand planning module optimized for small and medium enterprises, priced at USD 150 per user per month.

- August 2025: Tecsys received ISO 27001 certification for its cloud-based healthcare supply chain platform.

Global Cloud Supply Chain Management Market Report Scope

The Cloud Supply Chain Management Industry Report is Segmented by Solution (Demand Planning and Forecasting, Inventory and Warehouse Management, Product Lifecycle Management, Transportation and Logistics Management, Sales and Operations Planning, Procurement and Sourcing, Order Management, Product Master Data Management), Deployment Type (Hybrid Cloud, Public Cloud, Private Cloud), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (Retail, Food and Beverage, Manufacturing, Automotive, Oil and Gas, Healthcare, Consumer Electronics, Aerospace and Defense, Pharmaceuticals), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Demand Planning and Forecasting |

| Inventory and Warehouse Management |

| Product Lifecycle Management |

| Transportation and Logistics Management |

| Sales and Operations Planning |

| Procurement and Sourcing |

| Order Management |

| Product Master Data Management |

| Hybrid Cloud |

| Public Cloud |

| Private Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Retail |

| Food and Beverage |

| Manufacturing |

| Automotive |

| Oil and Gas |

| Healthcare |

| Consumer Electronics |

| Aerospace and Defense |

| Pharmaceuticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Solution | Demand Planning and Forecasting | |

| Inventory and Warehouse Management | ||

| Product Lifecycle Management | ||

| Transportation and Logistics Management | ||

| Sales and Operations Planning | ||

| Procurement and Sourcing | ||

| Order Management | ||

| Product Master Data Management | ||

| By Deployment Type | Hybrid Cloud | |

| Public Cloud | ||

| Private Cloud | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-User Industry | Retail | |

| Food and Beverage | ||

| Manufacturing | ||

| Automotive | ||

| Oil and Gas | ||

| Healthcare | ||

| Consumer Electronics | ||

| Aerospace and Defense | ||

| Pharmaceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the cloud supply chain management market?

The market generated USD 13.98 billion in 2026 and is forecast to climb to USD 30.56 billion by 2031.

Which deployment model dominates cloud supply chain systems?

Public Cloud leads with 60.58% 2025 revenue, favored for rapid activation and vendor-managed infrastructure.

Which industry segment will grow fastest through 2031?

Healthcare is projected to post a 21.60% CAGR through 2031 due to serialization mandates and cold-chain traceability needs.

Why are digital twins important in supply chains?

Digital twins simulate network disruptions, allowing planners to preempt delays and reduce expedited freight costs, driving a 21.25% CAGR for this solution type.

How fragmented is vendor competition?

No provider holds more than 15% share, and the top five control roughly 30%, indicating moderate fragmentation.

Page last updated on: