Intrusion Detection And Prevention Systems (IDPS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

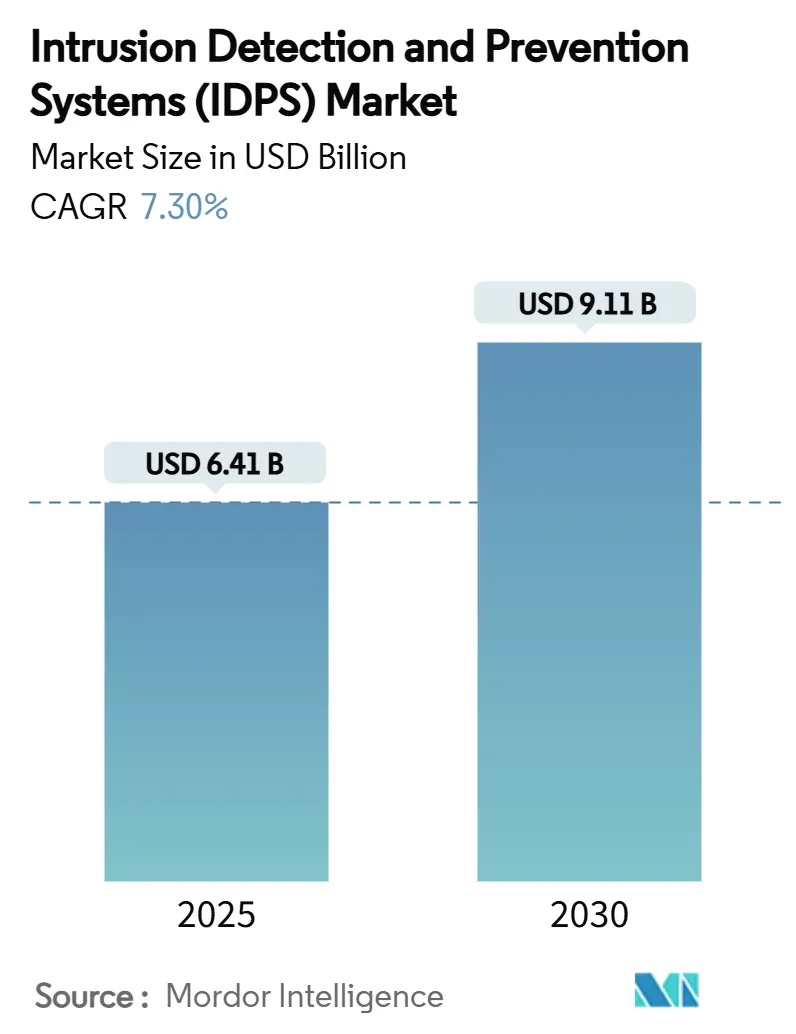

| Market Size (2025) | USD 6.41 Billion |

| Market Size (2030) | USD 9.11 Billion |

| Growth Rate (2025 - 2030) | 7.30% CAGR |

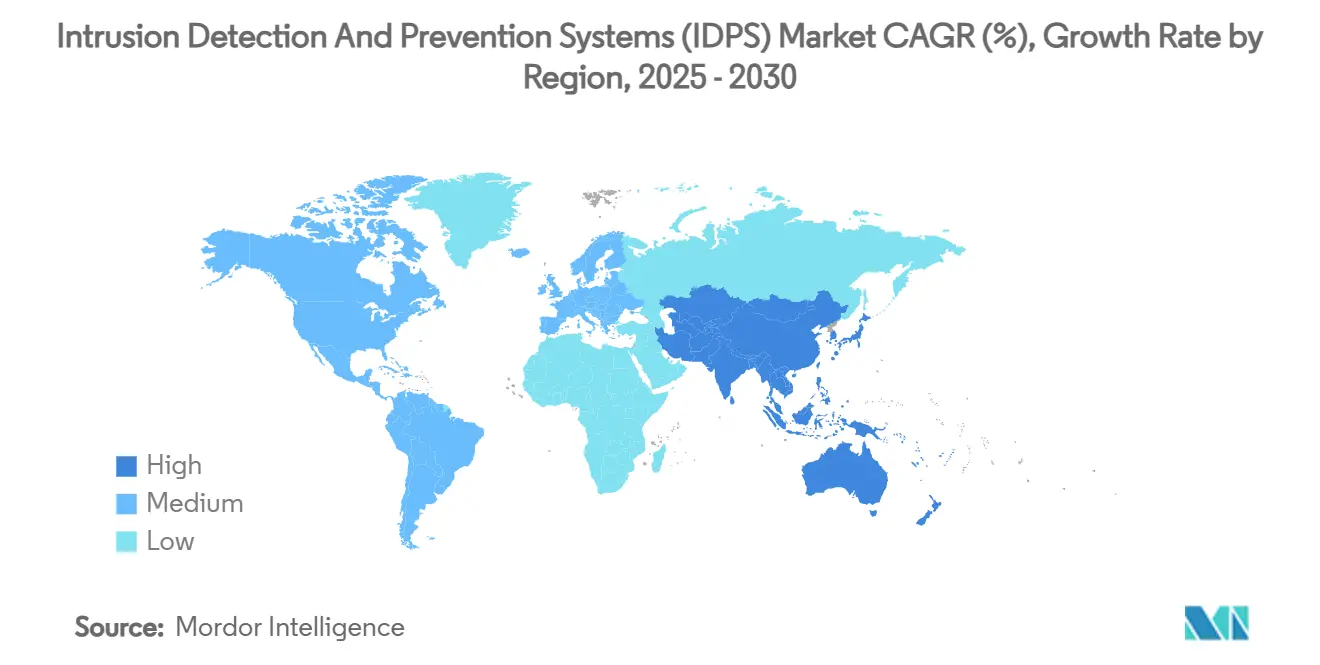

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

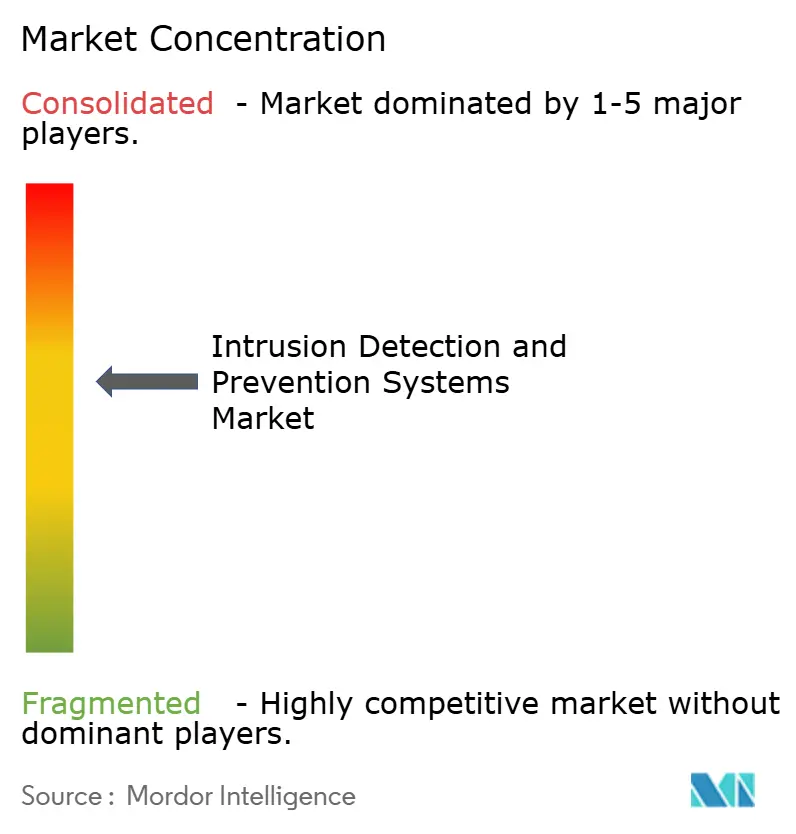

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intrusion Detection And Prevention Systems (IDPS) Market Analysis by Mordor Intelligence

The Intrusion Detection and Prevention Systems Market size is estimated at USD 6.41 billion in 2025, and is expected to reach USD 9.11 billion by 2030, at a CAGR of 7.30% during the forecast period (2025-2030). Heightened volumes of AI-enabled attacks, expanding cloud-native architectures, and mandatory compliance requirements are pushing enterprises to adopt real-time behavioral analytics and Zero Trust–aligned IDPS frameworks. [1]Federal Energy Regulatory Commission, “Critical Infrastructure Protection Reliability Standard CIP-015-1—Cyber Security—Internal Network Security Monitoring,” federalregister.gov Vendors that integrate cloud-based orchestration, threat-intelligence feeds, and automated response engines gain a clear competitive advantage as enterprises prioritize resilience and lower false-positive rates. The cybersecurity skills gap, estimated at 3.5 million unfilled roles, is accelerating demand for managed detection and response services that wrap around core IDPS technology. North America retains spending leadership on the back of NERC CIP-015-1 and NYDFS mandates, yet Asia-Pacific is expanding fastest as India, China, and Southeast Asia scale 5G and IoT programs.

Key Report Takeaways

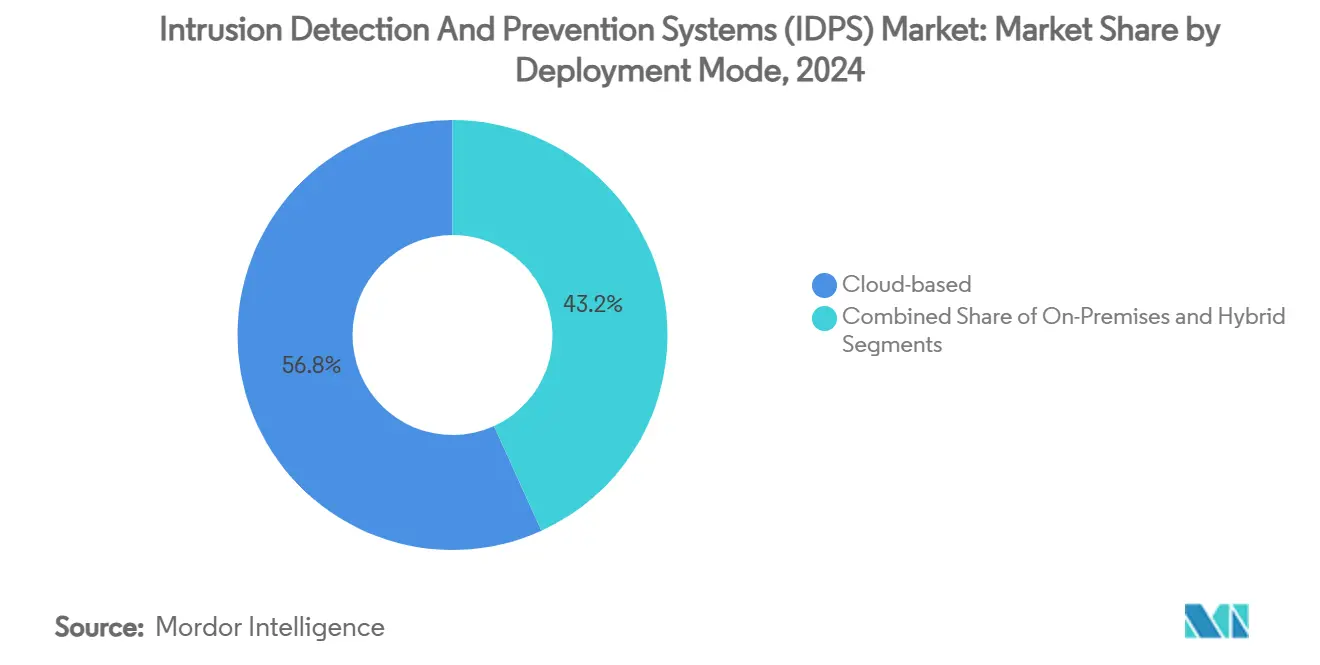

- By deployment mode, cloud-based deployment modes captured 56.8% of the intrusion detection and prevention systems market share in 2024, while hybrid configurations are advancing at an 8.7% CAGR through 2030.

- By component, software and platform components held 50.3% of the intrusion detection and prevention systems market size, whereas services represent the fastest-growing vector at an 8.4% CAGR as organizations outsource 24/7 threat hunting.

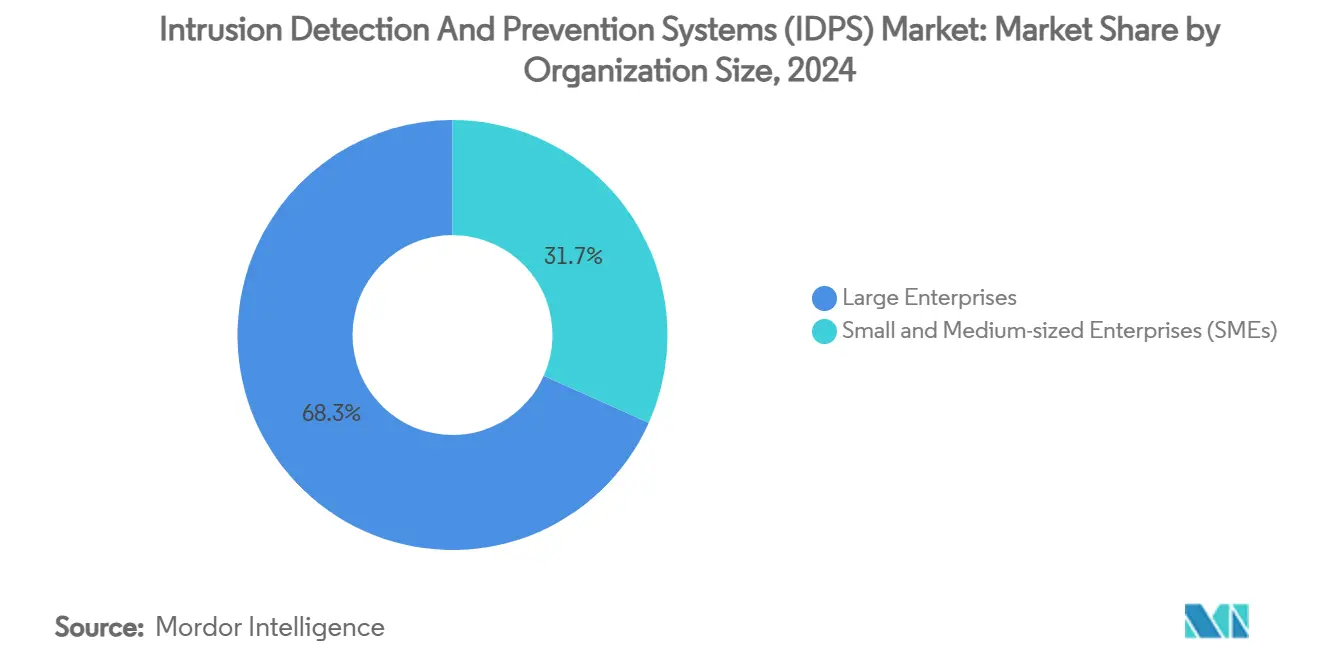

- By organization size, large enterprises controlled 68.3% revenue in 2024; however, small and medium-sized enterprises are on track for a 9.0% CAGR owing to cloud-delivered security models that remove heavy capital costs.

- By type, network-based IDS/IPS systems led with 46.1% of intrusion detection and prevention systems market share in 2024, but wireless IDS/IPS is accelerating at an 8.5% CAGR as 5G network slicing expands attack surfaces.

- By end-user industry, BFSI accounted for 29.1% revenue in 2024; IT-and-telecom is the fastest-advancing end-user group at an 8.3% CAGR due to complex multi-cloud environments.

- By geography, North America generated 38.3% of global revenue in 2024; Asia-Pacific is forecast to rise at an 8.4% CAGR driven by surging national cybersecurity budgets and domestic startups.

Global Intrusion Detection And Prevention Systems (IDPS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in sophisticated cyber-attacks | +1.5% | Global, high in North America and EU | Short term (≤ 2 years) |

| Regulatory mandates for real-time detection | +1.2% | EU primary, North America secondary | Medium term (2-4 years) |

| Cloud and hybrid workload migration | +0.8% | Global, led by North America and APAC | Medium term (2-4 years) |

| Expanding BYOD and IoT footprints | +1.1% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| IDPS-to-Zero-Trust integration | +0.9% | North America and EU growing into APAC | Medium term (2-4 years) |

| AI-driven analytics lowering OPEX | +0.6% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Sophisticated Cyber-Attacks Targeting Enterprise Networks

Enterprise networks now face polymorphic malware, AI-scripted phishing, and supply-chain infiltration that routinely sidestep legacy signature-based defenses. The U.S. Department of Homeland Security highlights how 5G vulnerabilities can disrupt critical infrastructure, prompting organizations to embed distributed IDPS sensors that correlate threats in real time. [2]U.S. Department of Homeland Security, “5G Impacts to Vehicles and Highway Infrastructure,” dhs.gov High-profile semiconductor attacks have proven that lateral movement can cripple production without continuous internal monitoring. Enterprises, therefore, combine behavioral baselines with curated threat-intelligence feeds to transform reactive operations into predictive security postures.

Regulatory Mandates for Real-Time Threat Detection (GDPR, NIS2)

The European Commission’s Delegated Regulation 2024/1774 compels financial entities to monitor anomalous ICT activity continuously, aligning with NERC CIP-015-1 obligations for utilities in North America. [3]European Commission, “Delegated Regulation 2024/1774,” europa.eu NYDFS amendments likewise require detection of unauthorized access within 30 days, pushing banks and insurers to integrate automated IDPS alerts into incident-response playbooks. As compliance audits intensify, cloud-hosted IDPS services that auto-generate reports and store evidence centrally gain preferred-vendor status among resource-constrained security teams.

Rapid Migration of Workloads to Cloud and Hybrid Environments

Multi-cloud strategies and containerized microservices produce east-west traffic volumes that overwhelm traditional appliances. Integrations such as Google Cloud and Palo Alto Networks showcase how cloud-native IDPS engines secure ephemeral workloads without manual rule updates. Financial institutions moving core banking platforms off-site retain on-prem transaction monitoring for compliance while leveraging cloud analytics to flag fraud across channels, illustrating why hybrid IDPS designs are gaining traction.

Growing BYOD and IoT Footprints Expanding Attack Surface

Cisco projects 14.7 billion IoT connections by 2025, with DDoS incidents expected to double, underscoring the urgency for device-aware IDPS capable of protocol-specific anomaly detection. Healthcare deployments ranging from infusion pumps to imaging systems require passive monitoring that identifies malicious traffic without interrupting patient care, as reflected in upcoming HIPAA Security Rule revisions. Manufacturing and energy operators similarly need OT-savvy analytics that preserve uptime while blocking cyber-physical threats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and legacy complexity | -0.7% | Global, high in emerging markets | Short term (≤ 2 years) |

| Scarcity of skilled cyber-security talent | -0.5% | Global, acute in North America and EU | Medium term (2-4 years) |

| Performance overhead on high-throughput nets | -0.4% | Global, critical for telecom and finance | Medium term (2-4 years) |

| Encrypted-by-default traffic visibility gap | -0.3% | Global, growing with privacy regulation adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Complexity in Legacy Infrastructures

Organizations that run monolithic data centers often lack the capital or expertise to retrofit modern IDPS appliances and centralized policy managers. Small firms gravitate toward open-source tools like Snort or Suricata, yet still require advanced tuning to control false positives, an exercise that inflates the overall cost of ownership. Complex mesh networks in manufacturing or utilities demand bespoke integrations that stretch limited budgets and delay roll-outs.

Shortage of Skilled Cyber-Security Professionals

With 3.5 million open roles worldwide, many enterprises cannot staff round-the-clock SOC teams to operate advanced IDPS suites. Optiv reports that firms without trained analysts incur USD 1.76 million more per breach, heightening interest in managed services that offload detection, triage, and containment workflows. Automation features that push plain-language alerts to IT generalists thus remain a critical buying criterion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Configurations Drive Enterprise Adoption

Hybrid deployments captured a rapidly accelerating 8.7% CAGR while cloud solutions maintained 56.8% of the intrusion detection and prevention systems market in 2024. Financial institutions keep sensitive customer data on-prem yet stream telemetry to cloud engines for AI enrichment, preserving compliance and latency performance. The intrusion detection and prevention systems market size attributed to hybrid subscriptions is forecast to hit USD 3.65 billion by 2030, reflecting enterprises’ need for simultaneous control and elasticity. On-prem appliances retain steady adoption in defense and government, where air-gapped infrastructures remain non-negotiable, but the integration layer increasingly mirrors cloud-native design patterns.

Edge computing is knitting together remote factories, retail branches, and 5G base stations, and hybrid IDPS architectures now push lightweight sensors to those endpoints while normalizing logs in central data lakes. Vendors offering single-pane policy orchestration across locations are therefore expanding wallet share, and this capability has become table stakes in competitive evaluations.

By Component: Services Acceleration Reflects Talent Shortage

Software and platform offerings held 50.3% of the intrusion detection and prevention systems market share in 2024, yet managed and professional services are climbing at an 8.4% CAGR. Outsourcing IDPS tuning, threat-hunting, and incident response addresses the acute labor deficit that hampers internal deployments. Services-driven revenue will represent USD 2.4 billion of the overall intrusion detection and prevention systems market size by 2030, encouraged by subscription models that convert capital outlays into operational spending.

Hardware appliance revenue is flattening as customers embrace virtualized form factors that fit into software-defined data centers. Platform vendors are enriching portals with AI explainability dashboards that help generalist IT staff understand anomalous patterns, a step that mitigates the operational drag caused by under-resourced SOCs.

By Organization Size: SME Growth Driven by Cloud Accessibility

Large enterprises held 68.3% revenue in 2024; however, SME uptake is pacing a 9.0% CAGR because cloud marketplaces let smaller firms license enterprise-grade capabilities on demand. Open-source stacks like Wazuh attract cost-sensitive adopters, but managed cloud wrappers dominate production roll-outs because they shield non-experts from rule-set maintenance. The intrusion detection and prevention systems market size tied to SMEs is forecast to double from USD 1.1 billion in 2025 to USD 2.2 billion by 2030, proving that consumption-based pricing is democratizing security.

Enterprise customers continue investing in cross-domain analytics that join endpoint, network, and cloud telemetry, reinforcing vendor lock-in for full-stack suites. Their focus has pivoted from greenfield expansion to optimization of alert fidelity and analyst productivity.

By Type: Wireless IDS/IPS Expansion Reflects 5G Security Imperatives

Network-based systems held 46.1% revenue in 2024, yet wireless IDS/IPS is accelerating at 8.5% CAGR because 5G introduces slice-specific threat vectors. Telecom operators require visibility into massive machine-type communications and ultra-reliable low-latency applications, demanding protocol-aware analytics to uphold service-level agreements. Host-based sensors complement network views, especially for insider-threat detection on laptops and servers. Meanwhile, Network Behavior Analysis engines, infused with machine learning, are essential for spotting zero-day exploits that signature finds miss.

Industrial operators installing private 5G adopt wireless IDPS nodes that integrate with OT firewalls, extending blueprint security without degrading real-time control-loop performance. Vendors fluent in 3GPP and industrial protocols thus secure a premium valuation.

By End-user Industry: IT and Telecom Sector Leads Digital-Transformation Security

Financial services organizations commanded 29.1% spending in 2024, spurred by PCI DSS 4.0 and anti-fraud mandates. Yet IT-and-telecom companies are rising fastest at an 8.3% CAGR, as hyperscale clouds, SaaS providers, and telcos embed IDPS into platform fabric to protect multi-tenant workloads. The intrusion detection and prevention systems market size allocated to IT and telecom will eclipse USD 1.9 billion by 2030.

Healthcare adoption is intensifying, given HIPAA 2025 updates that require continuous risk assessment. Energy and utilities invest in industrial-grade analytics compliant with NERC CIP obligations. Retailers prioritize high-throughput, low-latency appliances that guard cardholder data during seasonal peaks.

Geography Analysis

North America generated 38.3% of 2024 revenue as regulatory pressure and mature vendor ecosystems foster continued refresh cycles. Electric utilities deploy internal network security monitoring to satisfy NERC CIP-015-1, and major banks embed automated reporting to align with NYDFS breach-notification windows. [4]Industrial Defender, “Emerging NERC CIP Requirements for Internal Network Security Monitoring,” industrialdefender.com Growth in the region is steady, with enterprises now channeling budgets toward lowering alert fatigue rather than expanding sensor footprints.

Asia-Pacific is the fastest-growing region at an 8.4% CAGR, fueled by India’s USD 3.3 billion cybersecurity outlay in 2025 and a surge of 124 regional startups that elevate threat-intelligence sophistication. Governments across ASEAN are launching national CSIRT programs that recommend IDPS as a first-line defense in smart-city roll-outs. China’s data-localization rules spur domestic vendors to deliver sovereign analytics stacks, whereas Japan and South Korea center on 5G slice security.

Europe experiences measured expansion as GDPR and the NIS2 directive codify real-time detection for critical sectors. Delegated Regulation 2024/1774 standardizes ICT risk frameworks for financial entities, driving IDPS substitution away from legacy point solutions toward unified analytics. Germany’s automotive and machinery exporters favor industrial-ready platforms that blend IT and OT telemetry, while the United Kingdom’s fintech clusters gravitate toward SaaS-delivered IDPS with PCI automation.

Competitive Landscape

The market shows moderate concentration, with Cisco, Palo Alto Networks, and Fortinet controlling roughly 45% combined share while niche innovators deliver AI-driven differentiation. Cisco leverages installed network hardware to insert IDPS capabilities at line rate, and its 2024 threat-intelligence upgrade deepens contextual detection. Palo Alto Networks’ acquisition of IBM QRadar SaaS assets expands its SIEM-IDPS convergence strategy, aligning with Google Cloud and T-Mobile managed offerings to extend reach.

Fortinet’s 2025 purchase of Lacework augments its behavior analytics prowess, and the company’s AI workplace security suite unifies endpoint and network telemetry for automated containment. Check Point and Juniper Networks differentiate through cloud marketplaces and performance-optimized ASICs, while Trend Micro and WatchGuard court industrial and SME buyers with simplified consoles.

Vendors increasingly bundle data-loss prevention, application-layer firewalls, and security-service-edge features, eroding clear category boundaries. Consolidation is expected to persist as hyperscalers partner or acquire niche players for integrated threat pipelines.

Intrusion Detection And Prevention Systems (IDPS) Industry Leaders

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

Check Point Software Technologies Ltd.

Juniper Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Palo Alto Networks closed the acquisition of IBM QRadar SaaS assets, bolstering threat-correlation depth and automated response.

- March 2025: Google Cloud and Palo Alto Networks launched a joint firewall-IDPS service for hybrid deployments.

- February 2025: T-Mobile unveiled a managed SASE offering with integrated IDPS functions.

- January 2025: Fortinet acquired Lacework for USD 4.5 billion, adding cloud behavior analytics.

- December 2024: CrowdStrike allied with Fortinet to merge endpoint and network visibility.

- November 2024: Cisco released real-time IOC ingestion for its IDPS platform.

Global Intrusion Detection And Prevention Systems (IDPS) Market Report Scope

| On-Premises |

| Cloud-based |

| Hybrid |

| Hardware | |

| Software/Platform | |

| Services | Professional Services |

| Managed Services |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Network-based IDS/IPS |

| Host-based IDS/IPS |

| Wireless IDS/IPS |

| Network Behavior Analysis IDS/IPS |

| BFSI |

| IT and Telecom |

| Government and Defense |

| Healthcare |

| Retail and E-Commerce |

| Energy and Utilities |

| Manufacturing |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | On-Premises | ||

| Cloud-based | |||

| Hybrid | |||

| By Component | Hardware | ||

| Software/Platform | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Type | Network-based IDS/IPS | ||

| Host-based IDS/IPS | |||

| Wireless IDS/IPS | |||

| Network Behavior Analysis IDS/IPS | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Government and Defense | |||

| Healthcare | |||

| Retail and E-Commerce | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the intrusion detection and prevention systems market?

The market is valued at USD 6.41 billion in 2025 and is projected to hit USD 9.11 billion by 2030.

Which deployment model is growing fastest?

Hybrid IDPS configurations are expanding at an 8.7% CAGR as firms balance on-prem compliance with cloud scalability.

Why are services outpacing hardware growth?

A global shortage of 3.5 million cybersecurity professionals is driving enterprises to outsource threat monitoring and response.

Which region offers the largest growth opportunity?

Asia-Pacific, projected at an 8.4% CAGR, benefits from surging 5G roll-outs, IoT adoption, and government spending.

How will 5G influence IDPS technology requirements?

5G network slicing and ultra-low-latency applications demand protocol-aware wireless IDS/IPS capable of real-time threat detection.

What factors should SMEs consider when selecting an IDPS?

Cost-effective cloud delivery, automated rule management, and managed services that offset limited in-house security expertise.

Page last updated on: