Intravenous Iron Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

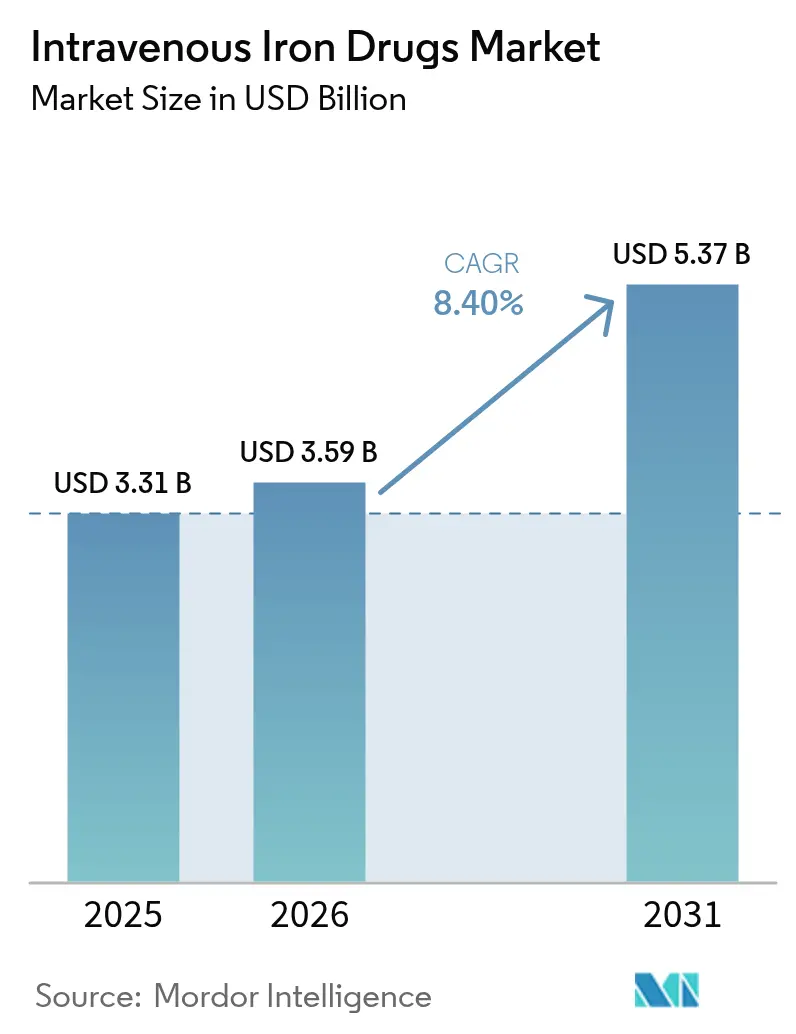

| Market Size (2026) | USD 3.59 Billion |

| Market Size (2031) | USD 5.37 Billion |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

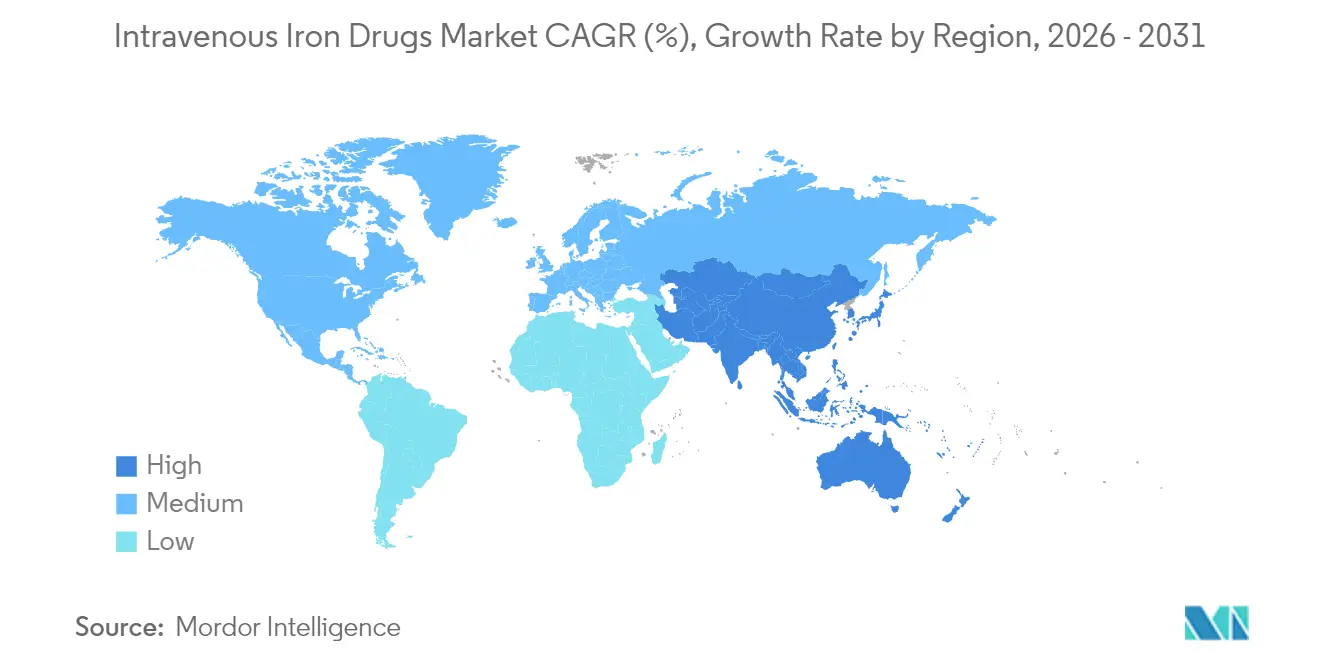

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intravenous Iron Drugs Market Analysis by Mordor Intelligence

The intravenous iron drugs market size is expected to grow from USD 3.31 billion in 2025 to USD 3.59 billion in 2026 and is forecast to reach USD 5.37 billion by 2031 at 8.40% CAGR over 2026-2031. The growth is mainly driven by robust clinical data favoring parenteral formulations, the sector is transitioning from episodic anemia correction toward proactive iron repletion in chronic kidney disease (CKD), heart failure (HF), inflammatory bowel disease (IBD) and oncology. Physicians increasingly prescribe high-dose, rapid-infusion complexes that limit chair time, while home-based infusion and telehealth models broaden patient access. Intensifying guideline support, notably from KDIGO and the Heart Failure Society of America, reinforces first-line use of IV iron, and expanding outpatient infrastructure underpins sustained demand. The growth trajectory is tempered by vigilance around hypophosphatemia and by payer-mandated step-edit protocols that favor lower-priced generics.

Key Report Takeaways

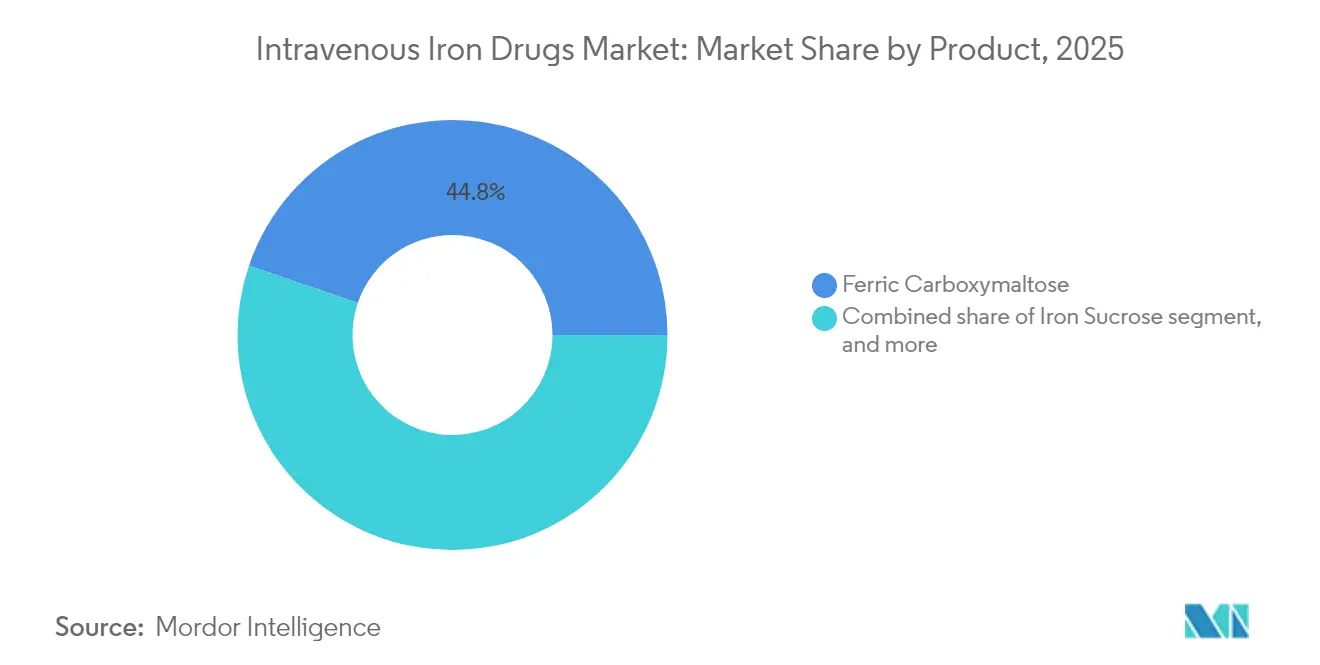

- By product type, ferric carboxymaltose led with 44.78% revenue share in 2025; iron isomaltoside is projected to grow at a 10.14% CAGR to 2031.

- By indication, CKD held 51.62% of the intravenous iron drugs market share in 2025, while HF with iron deficiency is set to expand at a 10.02% CAGR through 2031.

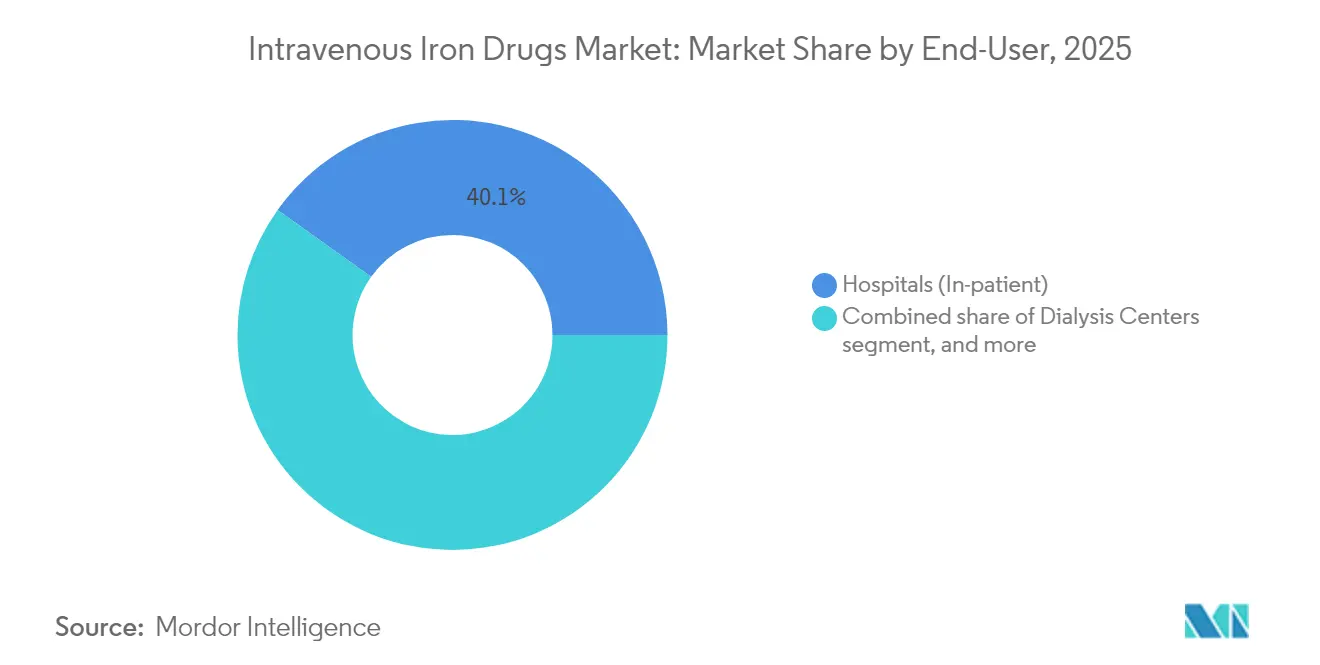

- By end-user, hospitals accounted for 40.12% of the intravenous iron drugs market size in 2025, whereas home infusion and telehealth services will rise at an 10.96% CAGR between 2026-2031.

- By distribution channel, hospital pharmacies contributed 42.08% share in 2025; online & specialty pharmacies are anticipated to advance at an 11.05% CAGR over the forecast period.

- By geography, North America commanded 42.05% of 2025 revenues; Asia-Pacific is expected to register the fastest 9.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intravenous Iron Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global iron-deficiency anemia burden across CKD, IBD, oncology & HF populations | +2.1% | Global; North America & Europe core | Long term (≥ 4 years) |

| Growing clinical preference for intravenous iron to overcome poor oral absorption & adherence | +1.8% | Global; developed markets | Medium term (2–4 years) |

| Rapid expansion of out-patient infusion centers and dialysis networks worldwide | +1.5% | North America & Asia-Pacific | Medium term (2–4 years) |

| Updated international guidelines endorsing IV iron as first-line therapy in CKD and heart failure | +1.3% | Global; early uptake in North America & Europe | Short term (≤ 2 years) |

| Introduction of high-dose, rapid-infusion complexes reducing treatment visits & costs | +1.0% | Developed markets; expanding to emerging economies | Medium term (2–4 years) |

| Rising healthcare expenditure in emerging markets improving access to parenteral therapies | +0.8% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Iron-Deficiency Anemia Burden Across CKD, IBD, Oncology & HF Populations

Clinical audits show iron deficiency in 37-61% of HF patients, and meta-analysis confirms that IV iron lowers cardiovascular mortality by 13% compared with placebo[1]R. Smith, “Intravenous iron in heart failure reduces mortality,” Nature Medicine, nature.com. Renal guidelines mandate regular iron supplementation for 92% of dialysis recipients, while CKD prevalence growth sustains baseline demand. China still reports 79.6 million iron-deficient adults even after a 40.86% fall in dietary deficiency rates since 1990. Functional deficiency in cancer adds incremental volume because inflammation blocks gut absorption. Collectively, these disease pools secure long-run volume growth across nephrology, cardiology and oncology clinics.

Growing Clinical Preference for Intravenous Iron to Overcome Poor Oral Absorption & Adherence

Consensus statements published in 2024 indicate that oral ferrous salts often fail to normalize ferritin or improve 6-minute-walk distance in HF with reduced ejection fraction. The IRONMAN trial showed the greatest benefit among patients with transferrin saturation below 20%. Real-world Japanese data in 632,200 cases reported a 3.20 g/dL hemoglobin rise with ferric carboxymaltose versus 1.70 g/dL for oral iron at week 12. High discontinuation rates tied to gastrointestinal intolerance further tilt prescribers toward parenteral therapy, cementing demand across chronic disease cohorts.

Rapid Expansion of Outpatient Infusion Centers and Dialysis Networks Worldwide

Alternate-site infusion revenue is projected at USD 142 billion by 2027, and 50% of new FDA approvals require an injectable route. CMS raised ESRD facility reimbursement by 2.7% for 2025, allocating USD 6.6 billion to 7,700 centers[2]CMS, “ESRD Prospective Payment System 2025 Final Rule,” cms.gov. During pandemic adaptations, 190 ferric carboxymaltose home infusions produced no grade ≥3 adverse events. These data validate safety of decentralized administration, shorten patient travel, and ease hospital capacity strain, catalyzing further distribution away from inpatient wards.

Updated International Guidelines Endorsing IV Iron as First-Line Therapy in CKD And Heart Failure

The Heart Failure Society of America’s 2024 update positions IV iron as standard care for symptomatic HF with iron deficiency. Asian expert panels released operational roadmaps to overcome cost and facility barriers. KDIGO’s 2025 revision advocates proactive iron correction before anemia manifests, enlarging the eligible patient base. Regulatory interest is also evident: the European Commission continues to scrutinize anticompetitive messaging in the sector, supporting broader product choice.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns (hypersensitivity, hypophosphatemia) limiting uptake of high-dose formulations | −1.2% | Global; developed markets with advanced pharmacovigilance | Short term (≤ 2 years) |

| Intensifying generic competition driving price erosion in mature molecules | −0.9% | North America & Europe; expanding to emerging markets | Medium term (2–4 years) |

| Reimbursement uncertainties for non-dialysis indications in major markets | −0.7% | North America & Europe | Medium term (2–4 years) |

| Cold-chain & infusion infrastructure gaps in low-resource regions | −0.6% | Sub-Saharan Africa; parts of Asia & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns (Hypersensitivity, Hypophosphatemia) Limiting Uptake of High-Dose Formulations

Ferric carboxymaltose triggers hypophosphatemia in more than 70% of recipients within five weeks by elevating FGF-23, risking cardiac dysfunction and fractures[3]Oncology Nursing Society, “Hypophosphatemia after ferric carboxymaltose,” ons.org. Dutch cohort data in 2,468 courses documented insufficient replacement dosing and persistent anemia in 65% of cases, hinting that clinicians sometimes under-dose to mitigate adverse events. FDA guidance requires 30-minute post-infusion observation across the class, slowing clinic workflow. Collectively, these safety flags push some prescribers toward lower-dose or alternative complexes, capping near-term adoption of the highest-strength SKUs.

Intensifying Generic Competition Driving Price Erosion in Mature Molecules

Independence Blue Cross introduced a 2025 policy compelling use of two generics before branded Injectafer or Monoferric access. Public price sheets show 3-fold cost gaps between branded ferric carboxymaltose and generic ferumoxytol. CSL Vifor cited “dampened” outlook amid bundling pressure in renal drugs. While derisomaltose retains patent life into the 2030s, most legacy complexes confront margin compression, moderating nominal market expansion despite rising unit volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Persistent Ferric Carboxymaltose Leadership Amid Isomaltoside Acceleration

Ferric carboxymaltose held 44.78% of 2025 sales, securing the largest intravenous iron drugs market share on the back of extensive evidence across CKD and HF protocols. However, the intravenous iron drugs market size for iron isomaltoside is forecast to post a 10.14% CAGR to 2031 as prescribers value its lower hypophosphatemia risk profile. The PHOSPHARE-IBD study estimated that derisomaltose cuts infusion visits by 1.64 over a five-year horizon, translating into NOK 9,707 cost savings per patient.

Momentum toward safety-led selection continues. Sucrose enjoys embedded use in dialysis bundles, whereas sodium ferric gluconate fills niche hypersensitivity cases. Ferumoxytol’s generic entry exerts pricing leverage across the class, triggering formulary shifts. Overall, differentiated safety, dosing convenience and cost shape the competitive axis more than simple brand tenure.

By Indication: CKD Supremacy Challenged by Heart Failure Surge

CKD accounted for 51.62% of revenue in 2025, underpinned by obligatory iron needs within hemodialysis protocols. Yet the intravenous iron drugs market will increasingly pivot toward HF, where the indication’s 10.02% CAGR reflects landmark trials showing 18% reductions in composite cardiovascular endpoints. Reimbursement updates in Europe now cover outpatient HF infusions, widening addressability.

Oncology, IBD and obstetric segments deliver incremental volume through recognition of functional iron deficiency unresponsive to oral therapy. Precision screening of transferrin saturation in bariatric surgery further elevates demand. The indication mix continues to diversify, distributing growth more evenly beyond traditional nephrology silos.

By End-User: Hospitals Still Dominant as Home-Based Models Rise

Hospitals collected 40.12% of 2025 revenue, reflecting centralized infusion infrastructure. Nevertheless, home infusion recorded an 10.96% CAGR outlook, driven by payer preference for lower-cost sites of care and positive pandemic-era safety audits. The intravenous iron drugs market size for outpatient settings is projected to overtake inpatient channels in post-2030 scenarios if virtual monitoring tech matures.

Dialysis centers remain structurally important; CMS’s USD 6.6 billion allocation to ESRD facilities underpins continued integration of IV iron in routine sessions. Specialty clinics and ambulatory surgery centers complement the mix, reflecting fragmentation in service delivery.

By Distribution Channel: Institutional Tenders Confront Specialty Pharmacy Expansion

Institutional tenders dominate procurement owing to volume rebates and formulary standardization. Yet specialty pharmacy networks and e-commerce platforms are capturing share by synchronizing drug delivery with home-infusion nursing. Vertically integrated dialysis groups wield supply control advantages and negotiate aggressively on molecule price. With payer incentives favoring lower acquisition cost, channel power is redistributing toward entities that can document adherence, safety and real-world outcomes.

Geography Analysis

North America contributed 42.05% of global turnover in 2025, sustained by guideline-driven uptake and broad reimbursement of parenteral iron. Independence Blue Cross’s step-edit rules exemplify mounting cost oversight, yet CMS’s reimbursement increase secures dialysis channel volume. Mature infrastructure supports stable demand, though unit growth is flattening as eligible CKD cohorts approach full penetration.

Asia-Pacific is forecast to record the fastest 9.42% CAGR through 2031, led by China’s volume-linked procurement that cut prices 42% while lifting usage 49%. Joint ventures such as CSL Vifor–Fresenius target more than 2,000 tier-3 hospitals, and India’s Anemia Mukt Bharat program seeks to narrow diagnostic gaps. Affordability remains a ceiling, yet economic expansion and insurance coverage gains support rising uptake.

Europe benefits from entrenched nephrology protocols and HF guideline alignment. However, high generic penetration and HTA scrutiny constrain price growth. Regulatory attention to fair competition—illustrated by the EU probe into disparagement claims—ensures diversified molecule availability. Middle East & Africa and South America show nascent but accelerating adoption as private insurers and public health funds recognize the productivity gains of rapid anemia correction.

Competitive Landscape

The intravenous iron drugs market displays moderate concentration. CSL Vifor, Pharmacosmos, Fresenius Kabi and Daiichi Sankyo collectively generate just under half of worldwide revenue, yielding no dominant single-player lockout. CSL Vifor’s leadership is challenged by EU antitrust inquiries and U.S. reimbursement bundling, prompting portfolio rationalization toward higher-value complexes. Pharmacosmos leverages derisomaltose’s safety narrative, while Fresenius Kabi exploits cost-utility data and integrated biosimilar offerings.

Generic suppliers escalate price competition, especially in ferumoxytol and sucrose formulations, pushing innovators to defend share through real-world evidence and patient-reported outcomes. Companies invest in digital adherence platforms and at-home infusion kits to capture shifting service models.

Pipeline innovation spans microneedle patches and magnetic nanoparticle targeting, although commercialization is unlikely before 2030. Overall rivalry is shaped by safety differentiation, care-site migration strategies and payer-driven formulary negotiations rather than classical detailing.

Intravenous Iron Drugs Industry Leaders

AbbVie (Allergan)

Covis Pharma GmbH (AMAG Pharmaceuticals, Inc)

CSL Limited (Vifor Pharma Management Ltd.)

Sanofi S.A.

Pharmacosmos A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CSL Vifor opened Multicube manufacturing site in Switzerland featuring heat recovery and solar power to boost iron therapy capacity.

- May 2025: Akebia Therapeutics reported Q1 revenue of USD 12.0 million for Vafseo and announced Phase 3 VALOR trial in non-dialysis CKD.

- March 2025: Fresenius Kabi launched Otulfi (ustekinumab-aauz) IV-SC biosimilar for autoimmune diseases in the U.S.

- January 2025: Independence Blue Cross implemented step-edit protocols requiring two generic IV iron trials before access to Injectafer and Monoferric.

- November 2024: CMS finalized the 2025 ESRD PPS rule, allocating USD 6.6 billion to 7,700 facilities with a 2.7% payment rise.

Global Intravenous Iron Drugs Market Report Scope

As per the scope of the report, intravenous iron drugs are iron supplement that is given through the intravenous route to compensate for iron losses in the blood in a certain clinical condition such as Chronic Kidney Disease (CKD), Intestinal Bowel Disease (IBD), cancer, among others to treat iron deficiency anemia. Intravenous iron drugs play a key role in treating diseases in nephrology, gastroenterology, oncology, critical care, gynecology, and others. The intravenous iron drugs market is segmented by Product Type (Ferric Carboxy maltose, Iron Sucrose, Iron Dextran, and Others), Applications (Chronic Kidney Disease, Irritable Bowel Syndrome, Cancer, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Ferric Carboxymaltose |

| Iron Sucrose |

| Intravenous Ferumoxytol |

| Sodium Ferric Gluconate Complex |

| Iron Isomaltoside 1000 |

| Other Product Type |

| Chronic Kidney Disease (Dialysis & Non-Dialysis) |

| Inflammatory Bowel Disease |

| Cancer- & Chemotherapy-Induced Anemia |

| Obstetrics & Gynecology (Pregnancy-Related Anemia) |

| Heart Failure with Iron Deficiency |

| Bariatric & Gastrointestinal Surgery |

| Other Indications |

| Hospitals (In-patient) |

| Out-patient Infusion & Oncology Centers |

| Dialysis Centers |

| Other End-Users |

| Direct Tenders / Institutional Sales |

| Hospital Pharmacies |

| Online & Specialty Pharmacies |

| Captive Dialysis Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Ferric Carboxymaltose | |

| Iron Sucrose | ||

| Intravenous Ferumoxytol | ||

| Sodium Ferric Gluconate Complex | ||

| Iron Isomaltoside 1000 | ||

| Other Product Type | ||

| By Indication | Chronic Kidney Disease (Dialysis & Non-Dialysis) | |

| Inflammatory Bowel Disease | ||

| Cancer- & Chemotherapy-Induced Anemia | ||

| Obstetrics & Gynecology (Pregnancy-Related Anemia) | ||

| Heart Failure with Iron Deficiency | ||

| Bariatric & Gastrointestinal Surgery | ||

| Other Indications | ||

| By End-User | Hospitals (In-patient) | |

| Out-patient Infusion & Oncology Centers | ||

| Dialysis Centers | ||

| Other End-Users | ||

| By Distribution Channel | Direct Tenders / Institutional Sales | |

| Hospital Pharmacies | ||

| Online & Specialty Pharmacies | ||

| Captive Dialysis Service Providers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the intravenous iron drugs market by 2031?

The market is expected to reach USD 5.37 billion by 2031, growing at an 8.40% CAGR during 2026-2031.

Which therapeutic area will grow fastest within this market?

Heart failure with iron deficiency is forecast to post the highest 10.02% CAGR through 2031, reflecting strong clinical-outcome data.

Why are outpatient and home infusion channels expanding so quickly?

Payer incentives, patient convenience and CMS reimbursement increases support alternate-site care, while remote monitoring confirms safety equivalence to hospital administration.

How does hypophosphatemia affect prescribing patterns?

High rates of post-infusion hypophosphatemia with ferric carboxymaltose prompt closer phosphate monitoring and encourage uptake of lower-risk formulations such as iron isomaltoside.

Which region offers the greatest growth potential?

Asia-Pacific, led by China’s procurement reforms and expanding insurance coverage, is set to register the fastest 9.42% CAGR through 2031.

How significant is generic competition?

Generic ferumoxytol and other off-patent complexes create price gaps up to 3-fold against brands, leading payers to impose step-edit policies that favor lower-cost options before premium agents are approved.

Page last updated on: