Global Intravenous Immunoglobulin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

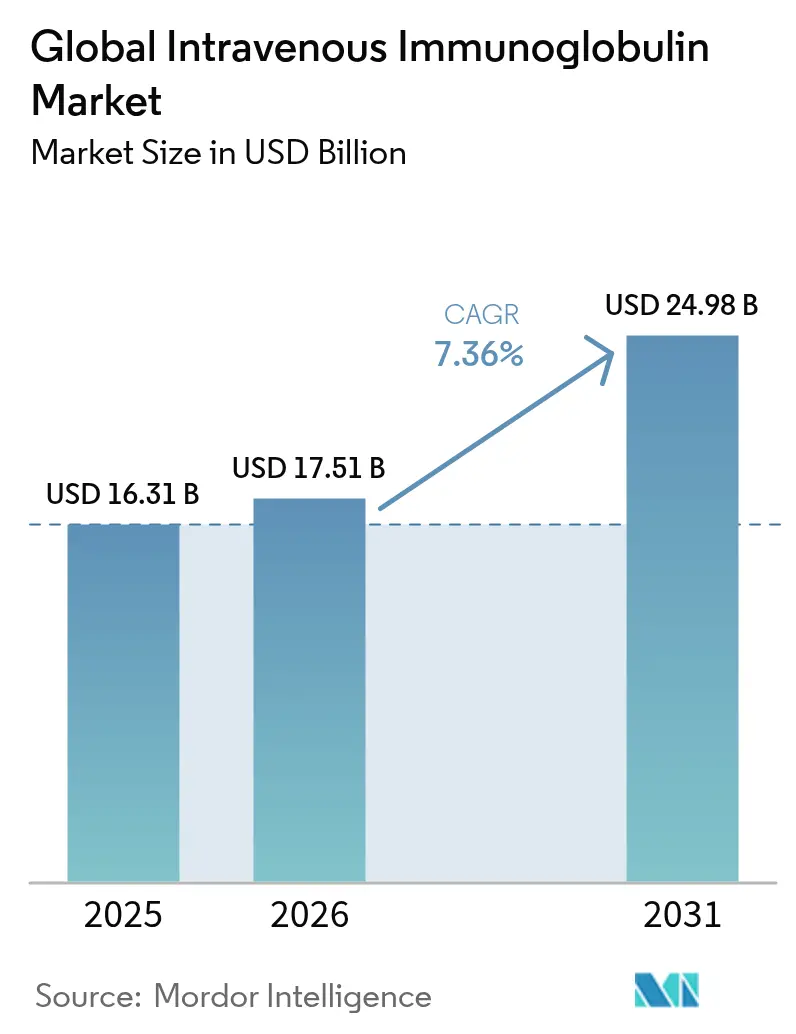

| Market Size (2026) | USD 17.51 Billion |

| Market Size (2031) | USD 24.98 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

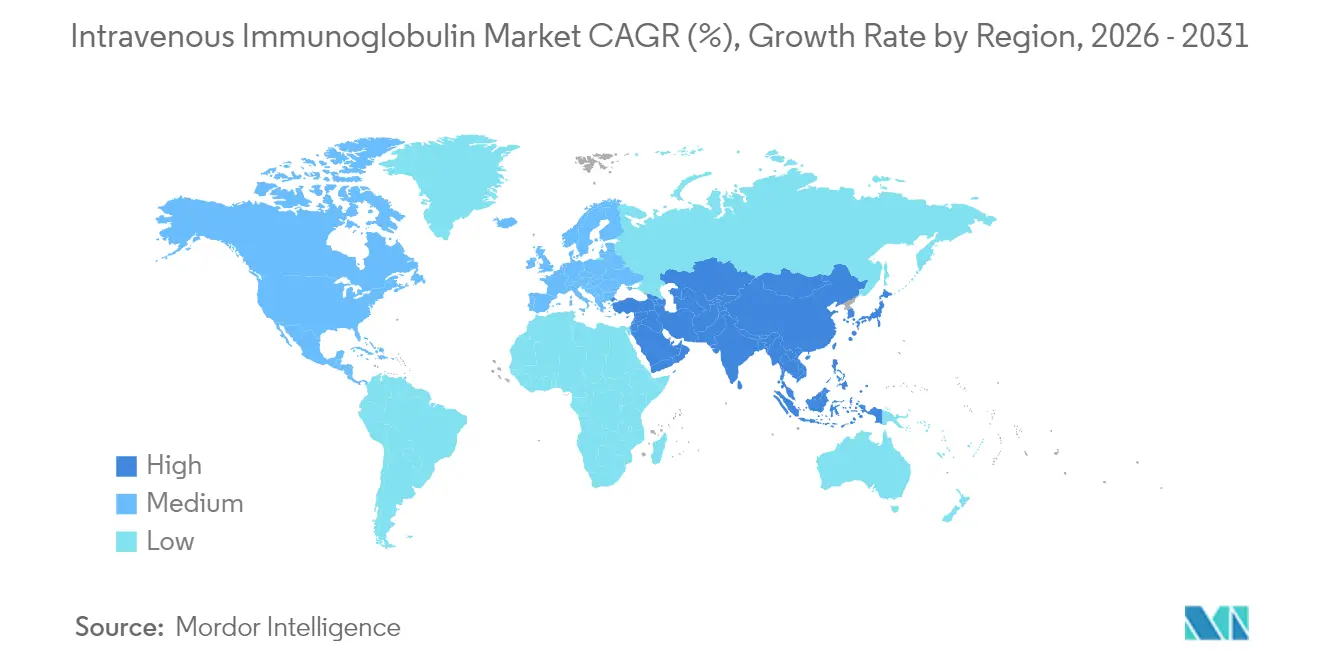

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Intravenous Immunoglobulin Market Analysis by Mordor Intelligence

The intravenous immunoglobulin market size is expected to grow from USD 16.31 billion in 2025 to USD 17.51 billion in 2026 and is forecast to reach USD 24.98 billion by 2031 at 7.36% CAGR over 2026-2031. Rising clinical use beyond primary immunodeficiency, demographic ageing, and sustained capacity investments by fractionators all reinforce demand fundamentals. North America leads the intravenous immunoglobulin market because of well-established reimbursement pathways and high per-capita spending, whereas rapid healthcare access gains and policy reform propel Asia-Pacific. IgG retains dominant status, and expanding neurological indications such as chronic inflammatory demyelinating polyneuropathy broaden the intravenous immunoglobulin market opportunity landscape[2]Octapharma USA, “IVIG Specialty Clinic Trends,” octapharmausa.com.

Key Report Takeaways

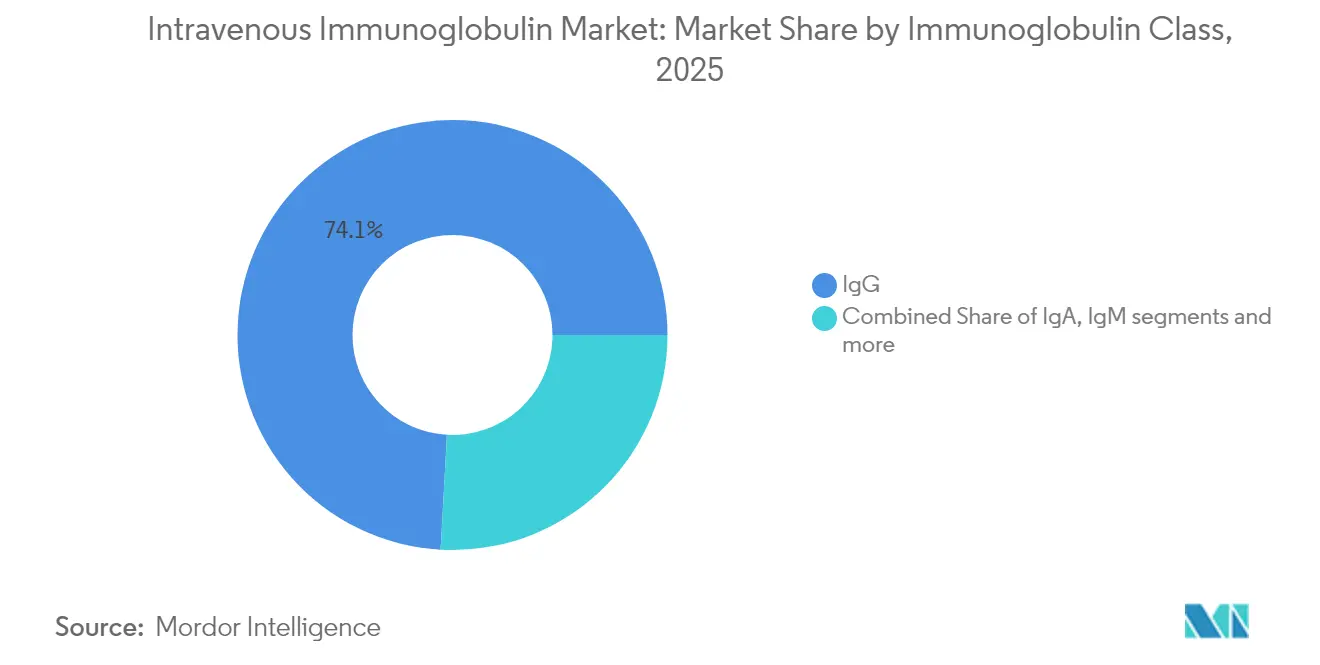

- By immunoglobulin class, IgG captured 74.12% of the intravenous immunoglobulin market share in 2025; it is also projected to expand at an 8.17% CAGR through 2031.

- By application, hypogammaglobulinemia accounted for 32.05% share of the intravenous immunoglobulin market size in 2025, while myasthenia gravis is advancing at an 7.89% CAGR to 2031.

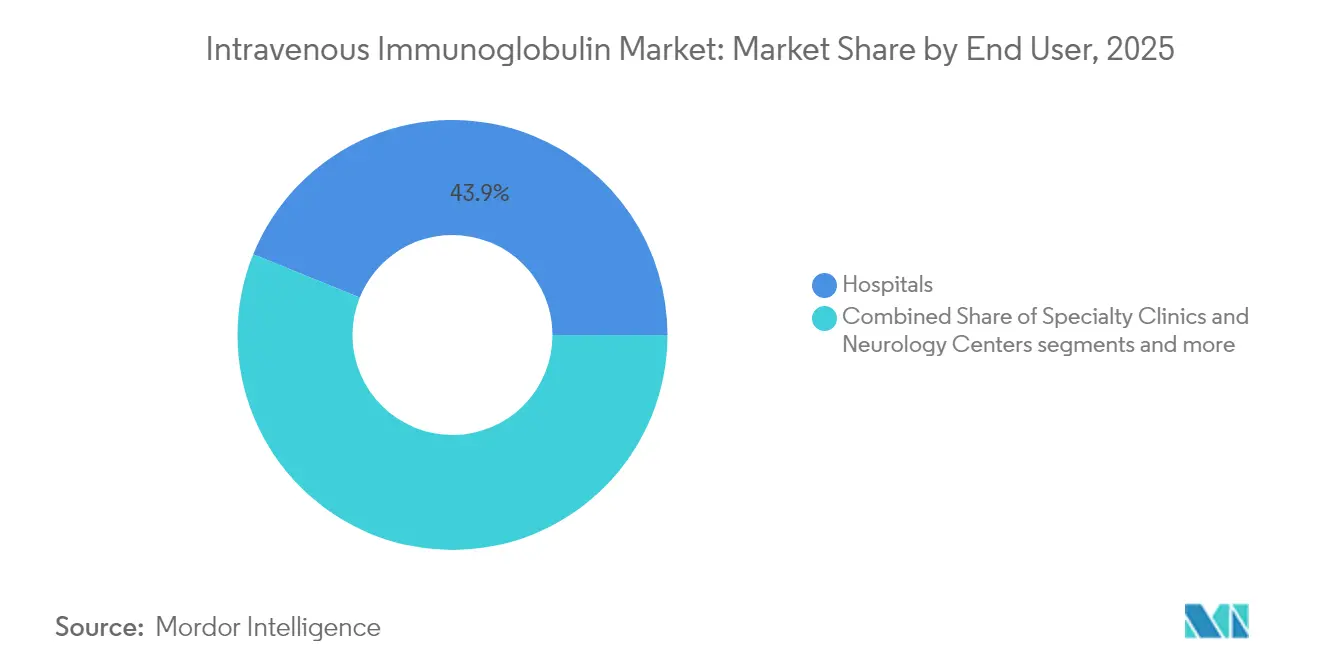

- By end user, hospitals held 43.88% revenue share in 2025; specialty clinics and neurology centers are forecast to grow fastest at an 8.12% CAGR through 2031.

- By geography, North America led with 41.92% revenue share in 2025, whereas Asia-Pacific is projected to accelerate at an 8.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Intravenous Immunoglobulin Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in geriatric population | +1.8% | Global, with highest impact in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Increased adoption of immunoglobulin therapy | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising prevalence of immunodeficiency & bleeding disorders | +1.2% | Global, with emerging market acceleration | Medium term (2-4 years) |

| Advancements in plasma-fractionation technology | +0.9% | North America & EU manufacturing hubs | Short term (≤ 2 years) |

| Off-label neurological use & relaxed reimbursement in Asia | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Regional plasma-collection hubs driving supply security | +0.6% | Global, with focus on US and EU collection centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Geriatric Population

Age-related immune decline increases susceptibility to infections and autoimmune disorders, which sustains long-term demand within the intravenous immunoglobulin market. Asia-Pacific feels the effect most, as rapid population ageing aligns with broader diagnostic reach and insurance coverage. The demographic trend also amplifies secondary immunodeficiencies linked with cancer therapies, further lifting usage. Japan’s medical technology spending trajectory underscores how ageing catalyzes specialty-therapy consumption. Together these factors form a predictable volume pipeline for fractionators over the next decade.

Increased Adoption of Immunoglobulin Therapy

Regulatory approvals such as Takeda’s GAMMAGARD LIQUID for chronic inflammatory demyelinating polyneuropathy have validated broader immunomodulatory utility and accelerated clinician acceptance. Emerging data in autoimmune encephalitis and sepsis reinforce confidence, encouraging off-label prescribing as reimbursement loosens in several high-income markets. The evidence base unlocks new patient pools and extends dosing durations, thereby raising overall consumption inside the intravenous immunoglobulin market.

Rising Prevalence of Immunodeficiency & Bleeding Disorders

Enhanced screening and heightened awareness uncover more primary and secondary immunodeficiency cases. In hematological malignancies, intravenous immunoglobulin therapy cut severe bacterial infection hospitalizations from 2.3 to 0.9 per person-year, illustrating clear clinical benefit. COVID-19 experience further spotlighted immunoglobulin for immunocompromised patients, solidifying its place in treatment algorithms and supporting repeat utilization patterns globally.

Advancements in Plasma-Fractionation Technology

Continuous chromatography, multicolumn systems, and automation shorten production cycles while raising yields, which expands effective supply without proportional increases in plasma collection volumes. Higher purity and better pathogen reduction also support premium positioning. Cost savings re-invested into new centers create a reinforcing loop that increases resilience of the intravenous immunoglobulin market supply chain.

Restraints Impact Analysis of Global Intravenous Immunoglobulin Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval & donor-screening norms | -1.1% | Global, with highest impact in EU and US | Long term (≥ 4 years) |

| High therapy & cold-chain costs | -0.9% | Global, with emerging market sensitivity | Medium term (2-4 years) |

| Shift toward subcutaneous Ig (SCIG) reducing IVIG volumes | -0.7% | North America & EU, spreading globally | Medium term (2-4 years) |

| ESG scrutiny of plasma sourcing raising compliance costs | -0.5% | Global, led by EU regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval & Donor-Screening Norms

Tight donor eligibility rules and exhaustive validation steps lengthen lead times and add overhead, especially in the European Union and United States, where regulatory scrutiny remains intense. Batch-release requirements and viral safety benchmarks impose capital and documentation burdens that may decelerate new-entrant progress inside the intravenous immunoglobulin market.

High Therapy & Cold-Chain Costs

A single IVIG course can run USD 5,000–10,000, and uninterrupted 2-8 °C logistics add financial weight, which restricts uptake in resource-constrained regions. Insurance prior authorization hurdles further delay initiation, keeping penetration below potential and trimming short-term volume growth projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Intravenous Immunoglobulin Market Segment Analysis

By Immunoglobulin Class:

IgG Dominance Drives InnovationIgG commanded 74.12% of the intravenous immunoglobulin market in 2025, and the segment is growing at an 8.17% CAGR to 2031, which underlines how indispensable IgG remains for both replacement and immunomodulation. Grifols’ purification process consistently delivers ≥98% IgG purity, strengthening brand differentiation. High-strength formulations now shorten infusion time, easing hospital scheduling pressures and improving patient comfort.

Manufacturers have prioritized continuous chromatography to boost yield and lower cost, which further bolsters margins across the intravenous immunoglobulin market. Regulatory clearances for new brands such as Yimmugo and ALYGLO increase competitive dynamics yet simultaneously assure broader supply security. IgA and IgM retain niche status focused on mucosal and complement-mediated disorders.

By Application:

Neurological Indications Accelerate GrowthHypogammaglobulinemia retained the largest share at 32.05% of the intravenous immunoglobulin market size in 2025, reflecting entrenched prescribing habits and clear guidelines. Nevertheless, myasthenia gravis is charting an 7.89% CAGR, the quickest among tracked indications, as neurologists adopt IVIG earlier in the disease course.

Chronic inflammatory demyelinating polyneuropathy and multifocal motor neuropathy also post solid gains, benefiting from recent label expansions. Off-label niches such as autoimmune encephalitis imply additional upside for the intravenous immunoglobulin market as clinical evidence accumulates and payers refine reimbursement conditions.

By End User:

Specialty Care TransformationHospitals delivered 43.88% of revenue in 2025, preserving leadership within the intravenous immunoglobulin market because most first infusions still happen in acute settings. However, specialty clinics and neurology centers are accelerating fastest, posting an 8.12% CAGR as payers and patients value dedicated infusion expertise.

Specialist sites streamline dosing adjustments, manage adverse events, and integrate electronic monitoring, which lifts adherence and outcome metrics. Home-care programs, while smaller, continue to emerge, encouraged by device advances and telehealth support that reduce facility visits and total cost of care.

Geography Analysis

North America Intravenous Immunoglobulin Market

North America kept 41.92% of the intravenous immunoglobulin market in 2025 due to long-standing insurer coverage and extensive plasma collection infrastructure. Medicare policies outline usage criteria that commercial payers largely mirror, facilitating predictable demand and rapid adoption of new formulations. Specialized infusion networks and maturing home-based services advance patient convenience and operational efficiency.

APAC Intravenous Immunoglobulin Market

Asia-Pacific is growing fastest at an 8.03% CAGR through 2031. China’s National Reimbursement Drug List negotiations produced average IVIG price reductions of 63% in 2024, opening therapy to previously unreachable cohorts. Japan’s revised health technology assessments uphold funding for innovative biologics, while India’s production-linked incentives stimulate local fractionation capacity, all of which enlarge the intravenous immunoglobulin market base.

Europe Intravenous Immunoglobulin Market

Europe shows stable progression, yet supply dependence on United States plasma highlights vulnerability. ESG-driven self-sufficiency policies and centralized procurement place pressure on manufacturers to diversify donor pools and enhance transparency. Gradual shifts toward outpatient infusions aim to reduce hospitalization costs and maintain quality benchmarks across the intravenous immunoglobulin market.

Competitive Landscape

The intravenous immunoglobulin market is moderately concentrated, as Takeda, CSL Behring, and Grifols control integrated collection-to-product chains that protect margins and secure supply. Each invests in continuous processing technology to lift yields and deploy digital twins for predictive maintenance. Strategic moves include CSL’s rollout of a novel nomogram-based plasma collection system that increases volume per donation by about 10% while maintaining safety[3]CSL Limited, “Rika Plasma Donation System,” csl.com.

Joint ventures broaden reach and hedge capacity risk. ICU Medical and Otsuka’s USD 200 million partnership builds one of the largest IV solutions plants in North America, supporting downstream bottling for immunoglobulins. Grifols seeks optionality through recombinant polyclonal platforms after winning BARDA funding, an approach that could Eventually reshape supply economics and lessen plasma reliance.

Emerging regional firms leverage government incentives to establish fractionation hubs close to high-growth patient pools. Nonetheless, high capital commitments, donor access hurdles, and complex regulatory files form substantial entry barriers, sustaining existing leadership within the intravenous immunoglobulin market.

Global Intravenous Immunoglobulin Industry Leaders

Biotest AG

Kedrion S.p.A

Grifols, S.A.

Bio Products Laboratory Limited

Takeda Pharmaceutical Company Limited

- *Disclaimer: Major Players sorted in no particular order

Global Intravenous Immunoglobulin Market Companies Covered in this Report

- Takeda Pharmaceutical Co.

- CSL Behring

- Grifols

- Octapharma

- Baxter

- Kedrion Biopharma

- Biotest

- Bio Products Laboratory

- LFB Group

- China Biologic Products Holdings

- Shanghai RAAS Blood Products

- Hualan Biological Engineering

- ADMA Biologics

- Emergent Bio Solutions

- Kamada Ltd

- GC Biopharma

- Intas Pharmaceuticals (Lonza Tie-up)

- BioTest Pharma (US)

- South African National Blood Service

- Sanquin Plasma Products

Read Analysis of Global Intravenous Immunoglobulin Companies

Recent Industry Developments in Global Intravenous Immunoglobulin Market

- November 2024: ICU Medical and Otsuka Pharmaceutical Factory formed a USD 200 million joint venture that targets annual output of 1.4 billion IV solution units to enhance supply resilience.

- October 2024: GigaGen secured a USD 135.2 million BARDA contract to advance recombinant polyclonal therapies against botulinum neurotoxins, signaling strategic expansion beyond plasma-derived products.

- July 2024: Grifols received FDA sign-off for expanded XEMBIFY labeling that allows treatment-naïve primary immunodeficiency patients to start with subcutaneous dosing.

- June 2024: Biotest obtained FDA approval for Yimmugo, its first US-market intravenous immunoglobulin, strengthening competitive diversity

Global Intravenous Immunoglobulin Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the intravenous immunoglobulin (IVIG) market as the worldwide revenue generated from licensed 5-10 % human IgG solutions delivered through hospital or home-based intravenous infusion for approved and widely adopted replacement or immunomodulatory indications, including primary immunodeficiency, CIDP, ITP, and select neuromuscular disorders.

Scope exclusion: investigational subcutaneous IgG products, hyperimmune specialty fractions, and veterinary preparations lie outside this analysis.

Segments Covered in This Report

- By Immunoglobulin Class

- IgG

- IgA

- IgM

- Others

- By Application

- Hypogammaglobulinemia

- Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- Primary Immunodeficiency Diseases (PID)

- Myasthenia Gravis

- Multifocal Motor Neuropathy

- Other Applications

- By End User

- Hospitals

- Specialty Clinics & Neurology Centers

- Home-Care Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Structured calls with plasma fractionators, neurology clinicians, and payer advisors across North America, Europe, and key Asia-Pacific nations validated treated-patient ratios, dose regimens in grams per kilogram, real-world ASP discounts, and likely reimbursement changes, ensuring that model levers mirror clinical practice rather than list-price assumptions.

Desk Research

Analysts first mapped the therapy universe through openly available sources such as the US FDA Biological Product Lot Release database, EMA EPARs, WHO Defined Daily Dose files, and annual plasma collection reports from PPTA. We blended these with epidemiology datasets from NIH Rare Diseases, Eurodis, and Japan's MHLW, plus import-export codes (HS 3002) extracted via Volza to frame addressable demand. Company 10-Ks and hospital purchase disclosures helped us spot typical average selling prices and recent volume shifts. Subscription assets like D&B Hoovers and Dow Jones Factiva supplied revenue splits that refined baseline shares. The sources named are illustrative; many additional publications were reviewed to corroborate figures, legal changes, and pricing nuances.

Market-Sizing & Forecasting

We reconstructed 2025 demand using a top-down prevalence-to-treated cohort build-up for core indications, multiplied by region-specific grams per patient and blended ASPs. Supplier roll-ups and channel checks offered bottom-up cross-tests that tightened variance to within three percent. Key variables like confirmed PID prevalence, CIDP incidence, plasma collection volumes, fractionation capacity additions, and regional reimbursement ceilings drive annual growth. A multivariate regression with these inputs, checked through three macro scenarios, underpins 2026-2030 forecasts. Outlier years are smoothed with exponential weighting.

Where distributor data proved patchy, missing nodes were bridged using nearest-neighbor averages vetted with experts.

Data Validation & Update Cycle

Every draft passes two analyst reviews, anomaly flags trigger source re-contact, and variance above five percent versus independent plasma supply or hospital purchase benchmarks is re-worked before sign-off. Reports refresh annually, with interim updates after material regulatory, epidemiological, or capacity events so clients always receive our most current view.

How Mordor Intelligence's Global Intravenous Immunoglobulin Market Size Compares to Other Published Estimates

Published estimates often differ because firms apply unlike product mixes, price points, and refresh cadences.

Key gap drivers include whether subcutaneous doses are co-reported, if list rather than realized prices are used, and how producers' fractionation bottlenecks are treated.

Mordor's scope focuses strictly on IV infusion, applies weighted ASPs derived from purchaser feedback, and updates the model each year, which limits inflation from unadjusted list prices and avoids over-counting emerging SCIG volumes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.31 B | Mordor Intelligence | - |

| USD 18.40 B | Global Consultancy A | Combines IV and SC products and relies on catalog prices, inflating value |

| USD 14.88 B | Industry Journal B | Uses historical shipment extrapolation without plasma-supply correction |

In sum, Mordor Intelligence delivers a balanced baseline grounded in clear scope choices, transparent variables, and repeatable steps, giving decision-makers a dependable figure against which to plan capacity, pricing, and investment.

Key Questions Answered in the Report

What is the current value of the intravenous immunoglobulin market?

The intravenous immunoglobulin market size is USD 17.51 billion in 2026 and is projected to reach USD 24.98 billion by 2031.

Which immunoglobulin class dominates sales?

IgG accounts for 74.12% of revenue because its pharmacology suits both replacement and immunomodulatory therapy.

Which region is growing fastest for IVIG?

Asia-Pacific posts the quickest growth at an 8.03% CAGR, driven by ageing populations, policy reform, and larger reimbursement pools.

Why are specialty clinics gaining share in IVIG delivery?

Clinics focused on neurology and immunology streamline infusion protocols, improve monitoring, and deliver better patient experience, supporting an 8.12% CAGR.

How does SCIG adoption affect IVIG demand?

Subcutaneous products offer convenience and fewer systemic side effects, which moderates IVIG volume growth, especially in North America and Europe.

What are key restraints for market expansion?

High therapy costs, cold-chain logistics, and stringent donor-screening rules increase operational overhead and can limit patient access in price-sensitive regions.

Page last updated on: