Intravenous Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.27 Billion |

| Market Size (2031) | USD 18.28 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

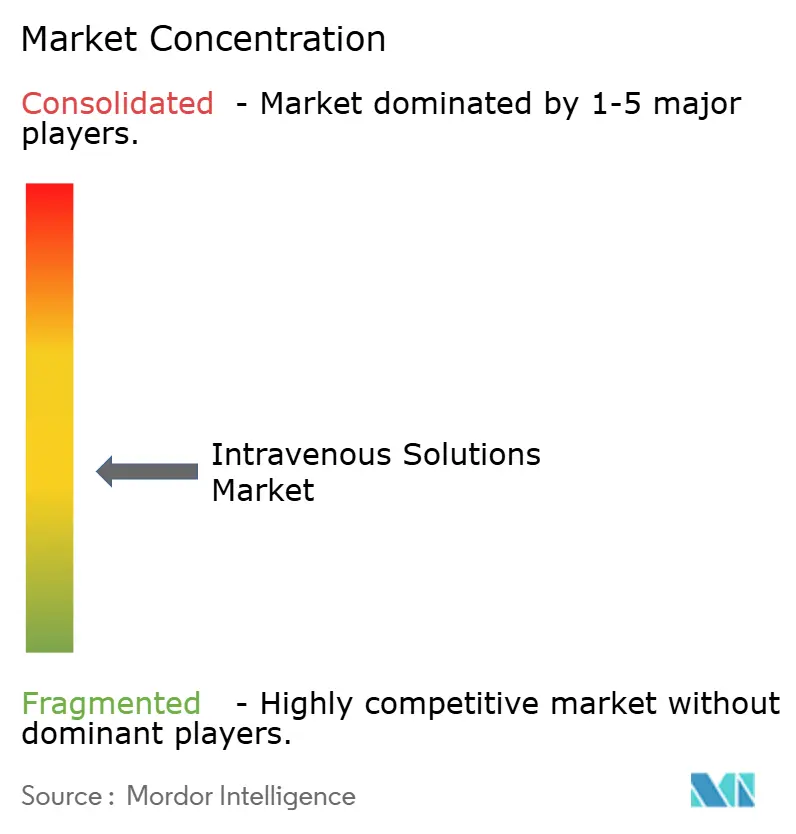

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intravenous Solutions Market Analysis by Mordor Intelligence

The Intravenous Solutions Market size was valued at USD 13.58 billion in 2025 and estimated to grow from USD 14.27 billion in 2026 to reach USD 18.28 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Growth stems from an accelerating shift toward precision-engineered formulations driven by artificial-intelligence dosing tools, rising surgical volumes, and a chronic-disease burden that intensifies demand for reliable parenteral therapies. Environmental legislation is hastening a transition away from PVC packaging, while government-backed onshoring initiatives seek to protect domestic supply after recent disaster-linked shortages. Leaders in the intravenous solutions market are therefore investing in vertically integrated manufacturing, AI-enabled nutritional platforms, and resilient logistics networks that can withstand climate and geopolitical shocks.

Key Report Takeaways

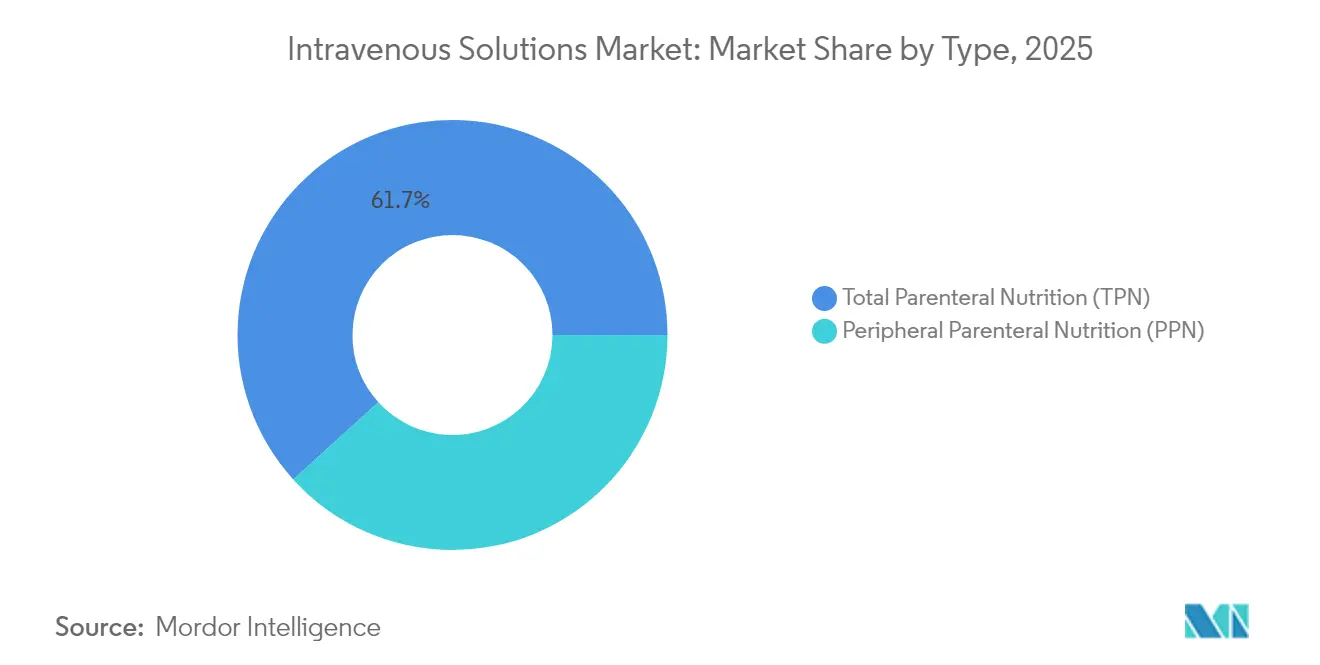

- By type, total parenteral nutrition (TPN) led with 61.72% of intravenous solutions market share in 2025, yet peripheral parenteral nutrition (PPN) is expanding at an 8.26% CAGR to 2031.

- By solution composition, saline solutions captured 52.60% of the intravenous solutions market in 2025, while lipid emulsions record the fastest 9.02% CAGR through 2031.

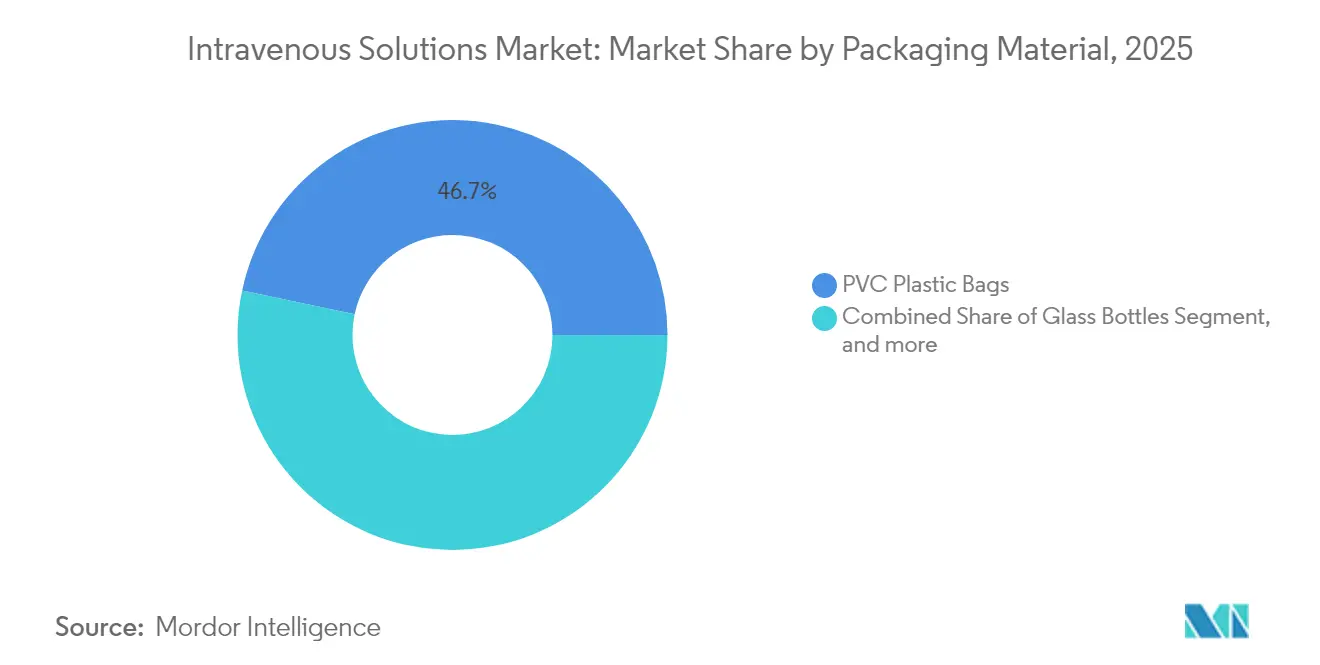

- By packaging material, non-PVC polyolefin formats are advancing at a 9.41% CAGR, whereas PVC bags still held 46.68% share of the intravenous solutions market in 2025.

- By end user, hospitals and clinics accounted for 68.55% revenue share in 2025; home-care settings show the highest 7.62% CAGR to 2031.

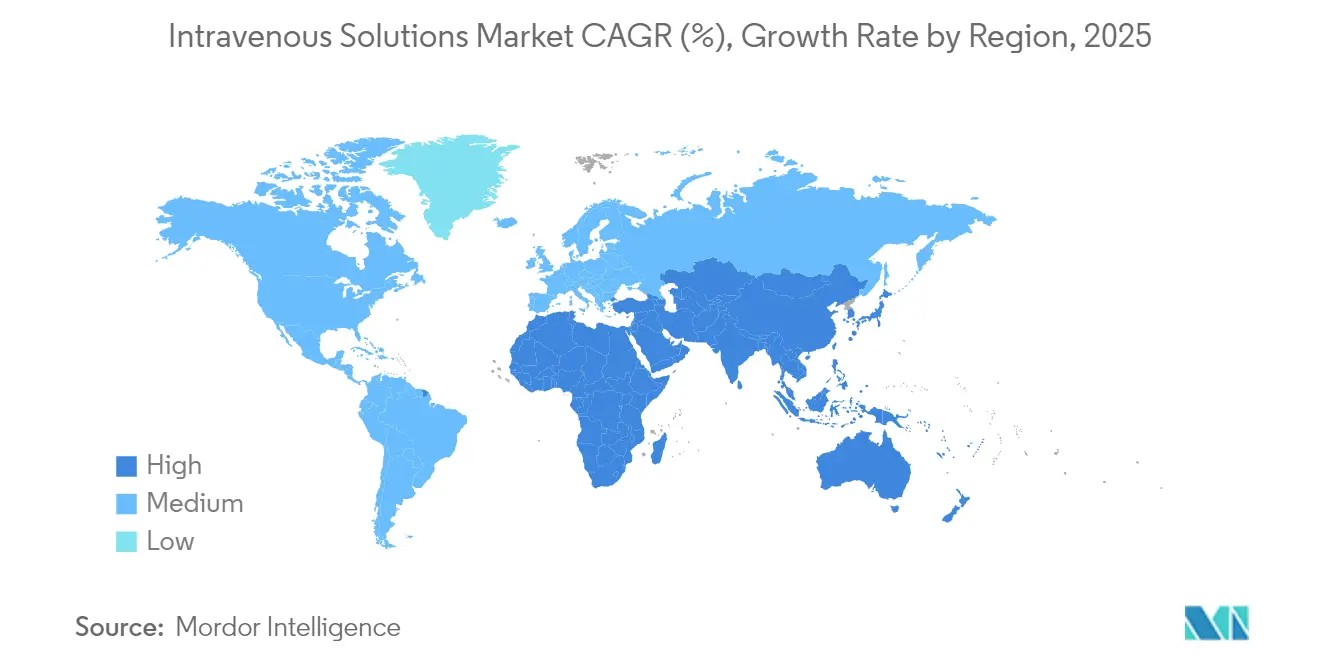

- By geography, North America commanded 39.35% share in 2025, but Asia-Pacific is forecast to grow at 6.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intravenous Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of AI-enabled, personalized parenteral nutrition protocols | +1.2% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Steady rise in chronic disease prevalence | +0.8% | Global, pronounced in APAC | Long term (≥ 4 years) |

| Rapid growth of home-based and ambulatory care models | +0.9% | North America & EU leading, expanding to APAC | Short term (≤ 2 years) |

| Ageing population coupled with higher surgical volumes | +0.7% | Global, greatest in developed markets | Long term (≥ 4 years) |

| Emergence of stability-optimized large-volume parenterals | +0.6% | Global | Medium term (2-4 years) |

| Government-backed onshoring initiatives | +0.5% | North America, similar trends in EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of AI-Enabled, Personalized Parenteral Nutrition Protocols

AI-driven software now matches expert TPN orders with 94% concordance, while cutting dosing-error rates by 54%.[1]Katherine Lee, “Deep-Learning Tool Achieves 94% Agreement With Neonatal Nutrition Experts,” nature.com Hospitals processing tens of thousands of nutrition prescriptions annually save minutes per preparation, freeing pharmacy labor and lowering cost. Standardized yet individualized regimens enhance evidence-based compliance and safeguard metabolic outcomes across neonatal and adult ICUs. Scalability makes the approach attractive for resource-limited centers that lack full-time nutritionists. Consequently, clinical protocols are shifting from manual calculations toward algorithm-guided prescriptions, reinforcing demand for formulation flexibility in the intravenous solutions market.

Steady Rise in Chronic Disease Prevalence

In 2024, 76.4% of US adults reported at least one chronic ailment, driving recurrent hospitalizations that depend on parenteral hydration and nutrition.[2]Centers for Disease Control and Prevention, “National Center for Health Statistics: Chronic Disease Indicators,” cdc.gov Younger patients increasingly present with multimorbidity, extending lifetime exposure to IV therapy. Surgeons anticipate thoracolumbar fusion procedures to rise to 297,994 cases by 2040, creating larger perioperative fluid needs.[3]A. Smith et al., “Forecast Trends in Thoracolumbar Fusion Surgery,” worldneurosurgery.org Hospitals therefore favor broad-spectrum IV platforms capable of supporting multi-drug regimens, a trend that reinforces baseline growth in the intravenous solutions market.

Rapid Growth of Home-Based and Ambulatory Care Models

Portable pumps, remote monitoring, and longer-shelf-life bags allow chemotherapy, antibiotics, and nutrition to shift outside hospitals. Pandemic experience validated clinical safety while reducing nosocomial infection risk. Manufacturers now formulate solutions for ambient stability and easy-to-use connectors, expanding addressable volumes within the intravenous solutions market. Payers also endorse the transition as it trims bed-day costs without sacrificing outcomes.

Ageing Population Coupled with Increased Surgical Volumes

Valve replacement, orthopedic, and oncologic procedures climb as median ages rise. Older patients with comorbidities require electrolyte-balanced, energy-dense fluids to expedite recovery and avoid renal stress. Forecasts indicate most candidates for major surgery will exhibit elevated BMI by 2030, complicating fluid distribution and necessitating customized macronutrient ratios. Precision blends positioned for geriatric physiology therefore secure heightened relevance, further broadening the intravenous solutions industry footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High compliance burden associated with GMP | -0.4% | Global, varying intensity | Medium term (2-4 years) |

| Ongoing supply-chain constraints | -0.3% | Global, acute in North America | Short term (≤ 2 years) |

| Environmental scrutiny of single-use IV plastics | -0.2% | North America & EU, expanding worldwide | Medium term (2-4 years) |

| Clinical shift toward subcutaneous and enteral routes | -0.3% | Global, faster in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Compliance Burden Associated With GMP

Revised EU Annex 1 now requires full contamination-control strategies and extensive barrier technology, raising capital thresholds for smaller firms. Validation of ready-to-use containers prolongs launch timelines by as much as 18 months, and documentation can consume 20% of development budgets. In emerging regions, diverging national rules oblige parallel audits, draining regulatory resources. These burdens deter new entrants and limit price competition, moderating growth in the intravenous solutions market.

Ongoing Supply-Chain Constraints

The Baxter North Cove shutdown proved that a single factory outage can force nationwide conservation protocols. Dependence on API imports from Asia leaves firms vulnerable to port closures and export bans. Stockpiles are difficult because typical shelf life remains below two years. Manufacturers therefore hold redundant inventory, inflating working capital, while hospitals scramble for substitutes that may not match formulation profiles. Such instability dampens short-term expansion in the intravenous solutions industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: TPN Sustains Leadership While PPN Gains Momentum

Total parenteral nutrition generated the largest revenue, equal to 61.72% of intravenous solutions market share in 2025. AI-guided calculators now tailor amino-acid, lipid, and electrolyte loads to metabolic markers, transforming TPN into a precision tool rather than a static recipe. Demand remains entrenched in neonatal and oncologic wards where gut function is compromised.

Peripheral Parenteral Nutrition, although accounting for a smaller base, is forecast to post the leading 8.26% CAGR. Home infusion programs favor PPN because peripheral lines avoid central-catheter infection risk and simplify nursing care. Multi-chamber PPN bags cut compounding errors, and stability-enhanced formulations extend hang times, supporting out-of-hospital uptake. The result is a steady re-balancing of volumes inside the intravenous solutions market as clinicians weigh risk, cost, and patient comfort.

By Solution Composition: Lipid Emulsions Accelerate Beyond Saline Staples

Saline maintained a 52.60% revenue share in 2025, underscoring its ubiquity in resuscitation and dilution tasks. Nevertheless, omega-3 enriched lipid emulsions are advancing at 9.02% CAGR between 2026 and 2031. Composite products such as SMOFlipid curb hepatotoxicity and modulate inflammation, creating measurable survival benefits in ICU cohorts.

Protein hydrolysates, carbohydrate blends, and trace-element cocktails enjoy niche growth as evidence supports tighter nutrient control during sepsis and trauma recovery. Research into heat-stable protein carriers that remain bioactive after pasteurization may soon eliminate cold-chain dependence, opening frontier markets and reinforcing geographical diversity of the intravenous solutions market.

By Packaging Material: Non-PVC Formats Push Sustainability Agenda

PVC bags still dominate on a unit basis with market share of 46.68% in 2025, but non-PVC polyolefin containers are recording the highest 9.41% CAGR. California’s phase-out deadlines have already diverted USD 1.2 billion of capital toward re-tooling, and European tenders increasingly demand DEHP-free products.

Glass bottles and multilayer polypropylene vials cater to niche segments involving cytotoxics and biologics where material compatibility is paramount. Barrier-coated polyolefin films that slash water-vapor transmission extend shelf life for amino-acid solutions, adding resilience to the intravenous solutions market supply chain.

By End User: Home Care Outpaces Institutional Settings

Hospitals and clinics secured 68.55% revenue share in 2025, reflecting entrenched inpatient protocols. Yet the home-care sub-segment is expanding 7.62% annually, powered by payer incentives and patient preference for familiar surroundings. Portable smart pumps transmit data to telehealth centers, allowing real-time dose adjustment.

Ambulatory infusion suites occupy the middle ground by offering specialist staff without costly overnight stays. These hybrid models sustain broader access and propel the intravenous solutions market into community settings previously dominated by oral therapies.

Geography Analysis

North America retained the largest regional stake with 39.35% of 2025 revenue, backed by advanced hospital networks and early uptake of AI dosing software. Executive Order 14293 and parallel state incentives are now underwriting new sterile-fill facilities in the Midwest, dispersing risk away from hurricane-prone regions. High insurance penetration also supports premium pricing for innovative non-PVC bags, further boosting the region’s intravenous solutions market performance.

Asia-Pacific displays the strongest momentum with a forecast 6.93% CAGR through 2031. China’s provincial tenders favor local capacity additions, while India leverages low-cost fill-finish labor for export contracts. Japan channels R&D subsidies into emulsions enriched with long-chain fatty acids that meet stringent geriatrics guidelines. Rising prevalence of diabetes and obesity in Southeast Asia likewise elevates demand for electrolyte-controlled solutions, making the region a critical growth engine for the intravenous solutions market.

Europe shows steady expansion anchored in stringent quality rules that reward GMP compliance. Hospitals prioritize DEHP-free sourcing, accelerating non-PVC conversion and opening premium niches. Meanwhile, Eastern European contract manufacturers bid for supplemental production to backstop Western shortages. Collectively, these dynamics keep the intravenous solutions industry resilient despite environmental taxes and evolving pharmacopoeia standards.

Mordor Intelligence provides coverage of the intravenous solutions market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The three largest suppliers Baxter International, Fresenius Kabi, and B. Braun collectively command high share of global revenue, reflecting moderate concentration. Baxter couples IV fluids with infusion pumps to lock in system sales, while its 2024 rollout of 10 new injectables expanded hospital wallet share. Fresenius Kabi’s EUR 600 (USD 708.2) million biosimilar franchise lets it bundle biologics with supportive parenterals, differentiating its catalog. B. Braun’s USD 1.2 billion investment in non-DEHP production strengthens its appeal in sustainability-focused tenders.

Mid-tier players pursue partnerships to scale, exemplified by ICU Medical’s USD 200 million joint venture with Otsuka that yields 1.4 billion bags annually. Start-ups aim at AI-guided compounding services, seeking licensing deals with hospital pharmacies. Regulatory initiatives such as the FDA Advanced Manufacturing Technologies program further encourage continuous-manufacturing prototypes that promise shorter lead times and fewer sterility interventions. Competitive rivalry therefore hinges on capacity, compliance agility, and digital-health integration as firms contest share in the intravenous solutions market.

Intravenous Solutions Industry Leaders

B. Braun SE

ICU Medical Inc.

Ajinomoto Co., Inc.

Baxter International Inc.

Grifols S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mallinckrodt and Endo announced a merger to create a diversified pharmaceuticals leader with pro forma revenue of USD 3.6 billion and Adjusted EBITDA of USD 1.2 billion, integrating their sterile injectables and generics businesses to enhance manufacturing infrastructure and generate substantial operating synergies.

- February 2025: Baxter International completed the sale of its Kidney Care business as part of strategic transformation, enabling focus on core IV solutions and infusion therapy segments while anticipating operational sales growth of 4-5% annually post-sale.

- October 2024: B. Braun Medical announced the plan to ramp up production of intravenous (IV) saline fluids by 20% at its plants in Irvine, California, and Daytona Beach, Florida.

- July 2024: Amneal Pharmaceuticals, Inc. received U.S. Food and Drug Administration (FDA) approval for a new formulation of potassium phosphates in 0.9% sodium chloride injection, available in ready-to-use intravenous (IV) bags. This sterile presentation streamlines the administration process by minimizing the compounding steps typically clinicians require.

Global Intravenous Solutions Market Report Scope

As per the report's scope, intravenous solutions are chemically prepared fluids administered in the body through venous circulation to maintain or replace the level of lost body fluid. The intravenous solutions market is segmented by type, solution composition, end-user, and geography. The type segment is further bifurcated into total and peripheral parenteral solutions. The solution composition is further divided into saline, carbohydrates, vitamins and minerals, and other solution compositions. The end-user segment is further segmented into hospitals and clinics, ambulatory centers, and home care settings. The geography segment is divided into North America, Europe, Asia-Pacific, Middle East, and Africa. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

| Total Parenteral Nutrition (TPN) |

| Peripheral Parenteral Nutrition (PPN) |

| Saline |

| Carbohydrates |

| Amino-acid & Protein Hydrolysates |

| Lipid Emulsions |

| Electrolytes, Vitamins & Trace Elements |

| Glass Bottles |

| PVC Plastic Bags |

| Non-PVC/Polyolefin Bags |

| Hospitals & Clinics |

| Ambulatory Surgery & Infusion Centres |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Total Parenteral Nutrition (TPN) | |

| Peripheral Parenteral Nutrition (PPN) | ||

| By Solution Composition | Saline | |

| Carbohydrates | ||

| Amino-acid & Protein Hydrolysates | ||

| Lipid Emulsions | ||

| Electrolytes, Vitamins & Trace Elements | ||

| By Packaging Material | Glass Bottles | |

| PVC Plastic Bags | ||

| Non-PVC/Polyolefin Bags | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgery & Infusion Centres | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the intravenous solutions market?

The market stands at USD 14.27 billion in 2026 and is set to reach USD 18.28 billion by 2031.

Which product type dominates the intravenous solutions market?

Total Parenteral Nutrition leads with 61.72% market share, although Peripheral Parenteral Nutrition is growing faster at 8.26% CAGR.

Why are non-PVC containers gaining traction?

Environmental regulations such as California’s Toxic-Free Medical Devices Act are phasing out DEHP-containing PVC, driving 9.41% CAGR growth for polyolefin bags.

How is artificial intelligence influencing IV-solution demand?

AI platforms like Stanford’s TPN2.0 standardize individualized dosing, cutting error rates and boosting hospital efficiency, thereby increasing demand for customizable formulations.

Which region is expected to show the fastest growth?

Asia-Pacific is forecast to expand at 6.93% CAGR through 2031, propelled by healthcare infrastructure upgrades and a rising chronic-disease burden.

Page last updated on: