Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

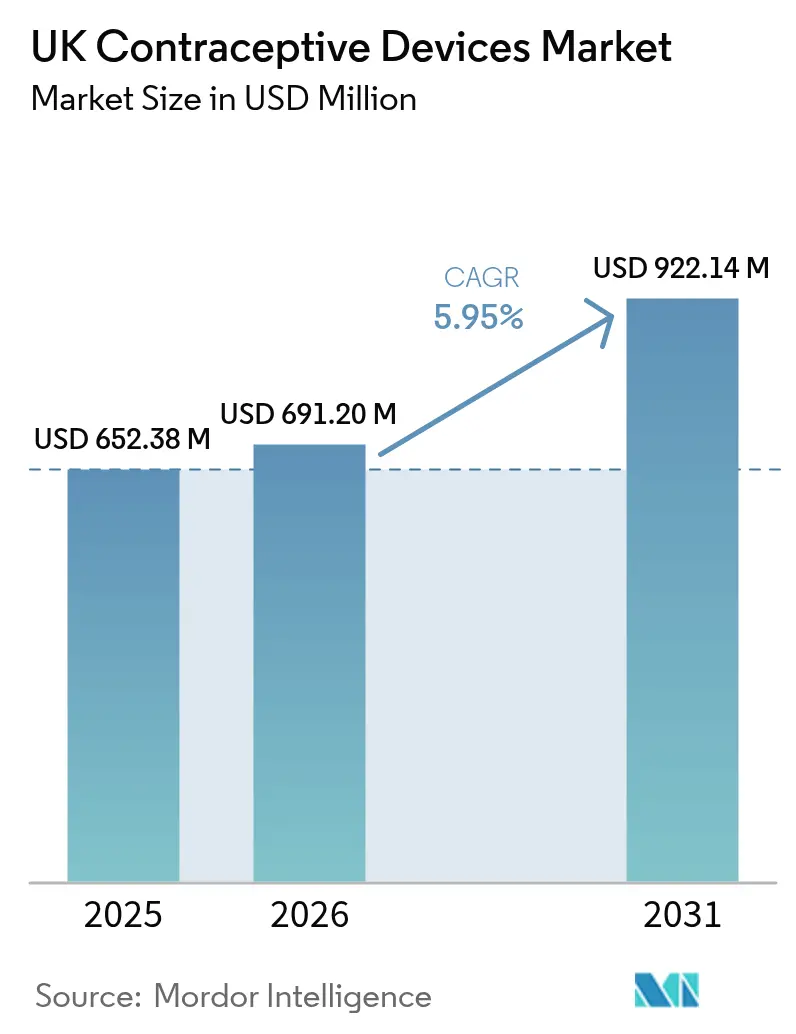

| Base Year Market Size (2025) | USD 652.38 Million |

| Market Size (2026) | USD 691.2 Million |

| Market Size (2031) | USD 922.14 Million |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Contraceptive Devices Market Analysis by Mordor Intelligence

UK contraceptive devices market size in 2026 is estimated at USD 691.2 million, growing from 2025 value of USD 652.38 million with 2031 projections showing USD 922.14 million, growing at 5.95% CAGR over 2026-2031. This expansion reflects the National Health Service’s (NHS) preventive-care emphasis, a regulatory climate that rewards product safety, and persistent demographic trends that sustain demand for reliable birth-control technologies. Rising sexually transmitted infection (STI) rates, notably the 85,223 gonorrhoea diagnoses recorded in 2023, keep dual-protection methods such as condoms squarely in focus.[1]UK Health Security Agency, “Quarterly Report on Diagnoses of Syphilis and Gonorrhoea,” gov.ukThe Medicines and Healthcare products Regulatory Agency (MHRA) intensified post-market surveillance rules in 2024, raising entry barriers yet reinforcing end-user confidence in device quality. Meanwhile, the January 2024 policy that allows pharmacists to dispense oral contraceptives without a general-practitioner consultation has accelerated over-the-counter (OTC) and online sales channels. Together, these forces position the UK contraceptive devices market for steady medium-term growth despite public-sector budget constraints and periodic supply bottlenecks.

Key Report Takeaways

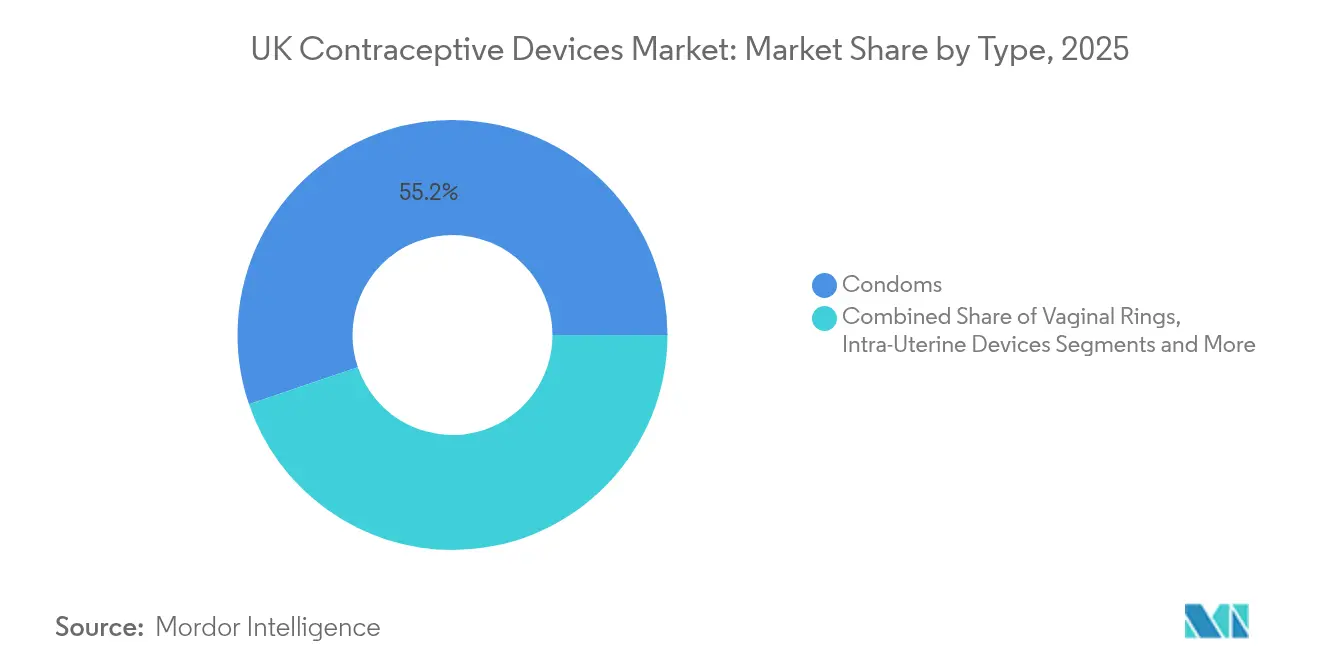

- By product type, condoms led with 55.22% revenue share in 2025; intrauterine devices are forecast to expand at a 8.67% CAGR through 2031.

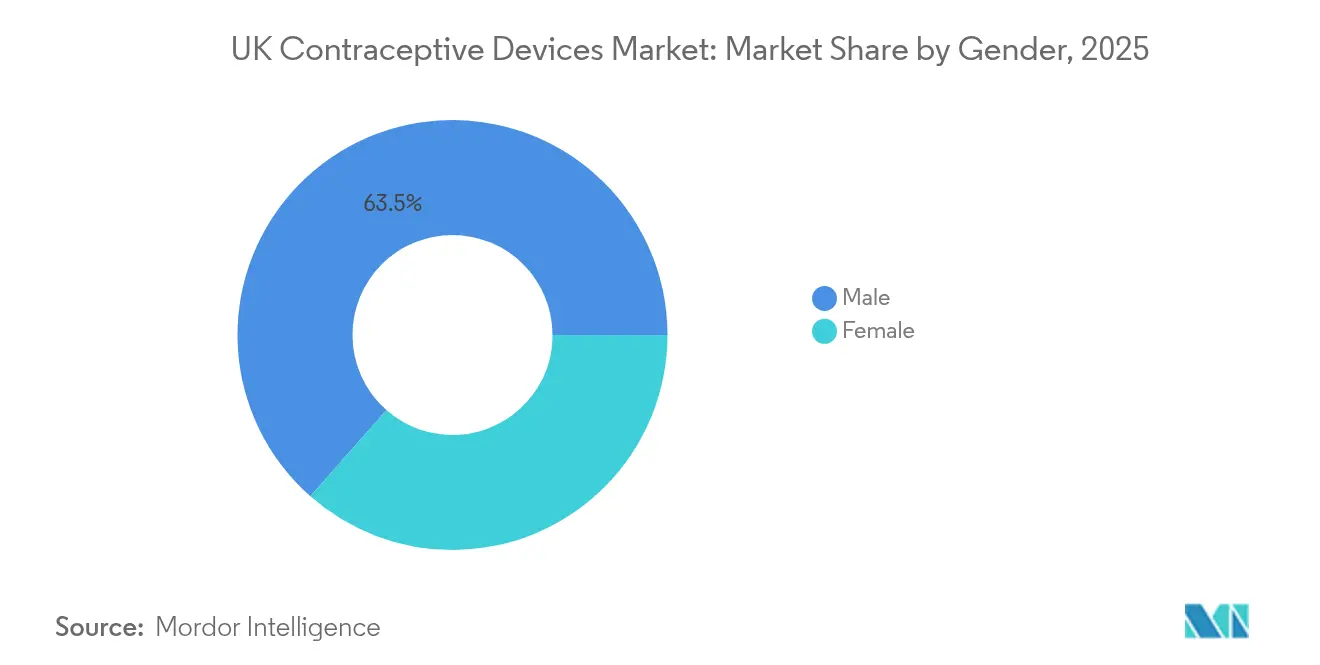

- By gender, male-targeted products held 63.51% of the UK contraceptive devices market share in 2025, while female-focused devices are set to grow at an 8.31% CAGR to 2031.

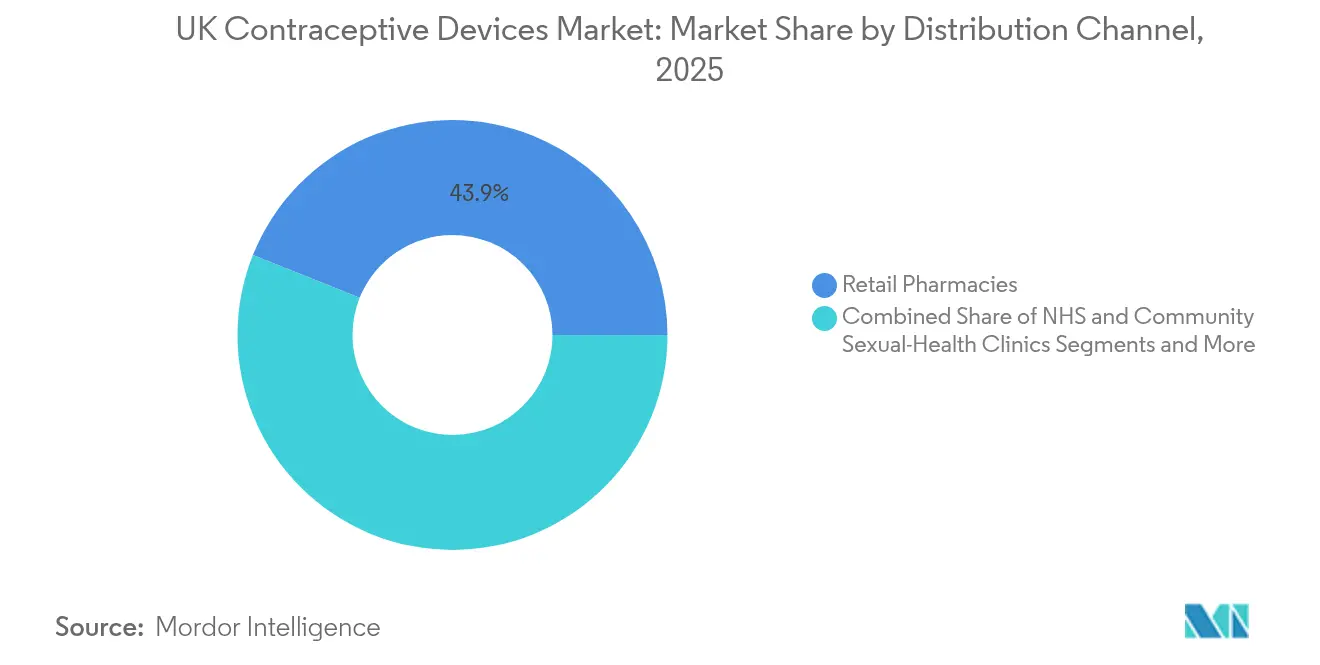

- By distribution channel, retail pharmacies captured 43.94% of the UK contraceptive devices market size in 2025 and are advancing at a 9.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of STDs & rising awareness | +1.2% | England-focused, spillover to Wales and Scotland | Medium term (2-4 years) |

| Increasing unintended pregnancies & UK-wide public-health drives | +0.9% | UK-wide with regional variations | Short term (≤ 2 years) |

| Government support for Reproductive and Family Planning services | +0.8% | England and Wales primary, Scotland secondary | Long term (≥ 4 years) |

| Consumer shift toward OTC & e-pharmacy fulfilment | +1.1% | Urban centers across UK, rural expansion | Medium term (2-4 years) |

| Growth Demand for LARCs and Innovative Devices | +0.7% | NHS-covered regions, private healthcare supplements | Long term (≥ 4 years) |

| Integration of Contraception with Digital Health Platforms | +0.6% | Tech-savvy demographics, urban concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of STIs & Rising Awareness

England alone logged 401,800 STI cases in 2023, a 4.7% year-on-year increase, keeping barrier methods at the centre of preventive policy.[2]Gareth Iacobucci, “Sexually Transmitted Infections Continued to Rise in England in 2023,” BMJ, bmj.com Gonorrhoea cases have reached their highest level since 1918, while 52 antibiotic-resistant strains had been identified by mid-2025. Public-health messaging now frames condoms as dual-function tools that curb both pregnancies and infections, boosting unit volumes in the UK contraceptive devices market. National surveillance also shows that 46% of new STI cases occur in the 15-24 age bracket, prompting age-specific outreach campaigns.[1]UK Health Security Agency, “Quarterly Report on Diagnoses of Syphilis and Gonorrhoea,” gov.ukLocal authorities, citing resource strain, increasingly promote self-care and home-delivery condom programmes, reinforcing a preventive mindset.

Increasing Unintended Pregnancies & UK-Wide Public-Health Drives

UK reproductive-health profiles show long-acting reversible contraception (LARC) uptake among women under 25 rising from 27.6% in 2019 to 36.2% in 2023, yet overall utilisation remains below pre-pandemic levels. Scotland’s bridging-contraception initiative delivers three-month supplies of progestogen-only pills through pharmacies, eliminating appointment delays and widening access. Parallel educational reforms mandate comprehensive relationships and sex education in schools, ensuring that the emerging adult cohort enters the UK contraceptive devices market with higher baseline awareness parliament.uk. Together, these programmes create latent demand for a diverse product mix that extends beyond condoms to LARCs, rings, and diaphragms.

Government Support for Reproductive and Family-Planning Services

NHS England’s 2025/26 operational guidance ranks sexual and reproductive health integration among top five priorities, reinforcing multi-year funding streams for device procurement england.nhs.uk. The Department of Health channelled more than GBP 3.5 billion (USD 4.36 billion) to local public-health budgets in 2024, underpinning subsidised access programmes that drive volume growth in the UK contraceptive devices market. From a regulatory standpoint, the MHRA now requires evidence-based post-market surveillance plans, rewarding firms that maintain robust quality systems.[3]Medicines and Healthcare Products Regulatory Agency, “Medical Devices Post-Market Surveillance Requirements,” gov.ukContraceptive caps and intra-uterine systems listed in the NHS Drug Tariff are supplied without patient co-payments, removing price barriers and guaranteeing predictable reimbursement for pharmacies.

Consumer Shift Toward OTC & E-Pharmacy Fulfilment

The January 2024 pharmacy-dispensing policy created a structural push toward walk-in and online channels, evidenced by 10% year-on-year pharmacy revenue growth at Boots in Q4 2024. SH:24, an NHS-supported telehealth portal, ships free contraceptives nationwide under clinician oversight, demonstrating the scalability of digital models. The NHS Pharmacy First service further extends pharmacist prescribing, converting community outlets into hybrid clinical hubs that lift unit throughput in the UK contraceptive devices market. Younger, tech-savvy consumers transact seamlessly on mobile interfaces, valuing discreet delivery and shorter wait times over legacy in-store consultations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device-related adverse effects & discontinuation | -0.8% | UK-wide with regional reporting variations | Short term (≤ 2 years) |

| Sociocultural resistance among specific faith & ethnic groups | -0.4% | Urban centers with diverse populations | Long term (≥ 4 years) |

| NHS funding pressure causing supply bottlenecks | -1.1% | England primary, Scotland and Wales secondary | Medium term (2-4 years) |

| Regulatory and Privacy Challenges Amid Digital Contraceptive Solutions | -0.3% | Tech-enabled services, urban concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device-Related Adverse Effects & Discontinuation

Heightened media attention on safety concerns, such as the meningioma risk linked to prolonged use of certain injectable progestogens, has raised discontinuation rates for some methods. The MHRA now obliges manufacturers to submit granular adverse-event reports within strict timelines, elevating compliance costs but also improving post-market data transparency. Professional societies such as the British Society of Urogynaecology actively encourage clinicians to report device complications, further sensitising the public to possible side effects. While long-acting progestogen therapies can reduce repeat interventions, risk-benefit calculations have become more nuanced, leading some women to revert to condoms or non-hormonal methods.

NHS Funding Pressure Causing Supply Bottlenecks

Brexit-related trade friction and global manufacturing disruptions have triggered intermittent shortages of contraceptive pills and barrier devices, forcing NHS regional procurement teams to issue guidance on therapeutic alternatives. A National Audit Office review found that central purchasing targets were missed in 2024, limiting economies of scale that might otherwise lower unit costs. While emergency sourcing frameworks exist, they can delay deliveries by weeks, creating temporary gaps in retail-pharmacy inventories and dampening short-term growth in the UK contraceptive devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Condoms Retain Scale as IUDs Accelerate Upgrade Cycles

The segment generated 55.22% of UK contraceptive devices market revenue in 2025, underscoring condoms’ strong dual-protection value proposition and extensive retail availability. The UK contraceptive devices market size for condoms amounted to USD 360.87 million in 2025, and volumes stay resilient as STI control remains a public-health priority. Intra-uterine devices (IUDs) are the fastest-growing line, advancing at a 8.67% CAGR to 2031, bolstered by extended wear times and favourable cost-utility ratios. Bayer’s Mirena and Kyleena systems now carry eight-year licences, a milestone that reduces replacement frequency and elevates lifetime adherence. Regulatory confidence also surfaced in 2024 when the Levosert hormonal IUS secured its own eight-year extension, signalling a high safety-efficacy threshold for hormonal platforms.

Innovations in non-hormonal technology add breadth to the category. The contoured Caya diaphragm, already registered in nearly 40 countries, demonstrates high acceptability in pilot studies and offers a silicone-free alternative for latex-sensitive users. Research published in Advanced Materials shows promise for stimuli-responsive hydrogels that produce reversible fallopian-tube occlusion, hinting at future patient-controlled sterilisation modalities. Vaginal rings are evolving beyond hormone-delivery systems; Bayer is co-developing a ferrous-gluconate-based ring that impedes sperm motility without altering hormonal balance. These R&D pipelines widen the technology mix, enabling manufacturers to address both safety concerns and emerging lifestyle preferences.

By Gender: Male Dominance but Strong Female Upside

Male-oriented products accounted for 63.51% of 2025 revenue, reflecting cultural acceptance of condom use and expanded free-distribution programmes such as the NHS Greater Glasgow and Clyde postal service. The UK contraceptive devices market size attached to male methods reached USD 414.43 million in 2025, but future growth moderates as female autonomy rises. Women increasingly opt for LARCs; the proportion of under-25 females selecting these devices rose to 36.2% in 2023. Digital health channels amplify this shift by supplying remote consultations and discreet deliveries that resonate with privacy-conscious users.

Academic investment is also accelerating female-controlled innovation. The University of Birmingham, backed by Gates Foundation funding, leads a multi-country study on sperm functionality aimed at developing novel, non-hormonal contraceptive frameworks. The MHRA’s guidance that women using GLP-1 weight-management drugs must adopt effective contraceptive measures opens an ancillary growth corridor among users of those therapies. Overall, female-focused devices carry an 8.31% compound pace, gradually balancing gender contributions within the UK contraceptive devices market.

By Distribution Channel: Retail Pharmacies Evolve into Omnichannel Hubs

Retail outlets controlled 43.94% revenue in 2025, equivalent to USD 286.66 million. This dominance stems from policy-enabled pharmacist prescribing, real-time inventory management, and click-and-collect services that compress delivery lead times. The UK contraceptive devices market share attributable to retail pharmacies is reinforced by NHS funding that reimburses pill supplies under the Pharmacy Contraception Service. Community sexual-health clinics retain a crucial role in complex procedures such as IUD insertion, yet their growth is capped by staffing and estate constraints.

Online pharmacies and e-commerce maintain the swiftest expansion at 9.97% CAGR through 2031. NHS-aligned telehealth portals register the sharpest relative expansion, leveraging algorithm-driven triage to channel patients toward the most suitable method while ensuring regulatory compliance. SH:24’s nationwide plain-package delivery model embodies this scalability, serving both urban and rural postcodes with equivalent efficiency. Supermarket chains lobby for over-the-counter status for emergency contraception, a move that would further democratise access but awaits regulatory clearance. Charities and youth centres cover demand peaks during festival seasons and university enrolment periods, supplying free condoms financed through local-authority grants.

Geography Analysis

England commands the largest slice of the UK contraceptive devices market, driven by population density and NHS England’s centralised purchasing frameworks that smooth procurement across 42 Integrated Care Boards. The region’s policy outreach includes the 2025 commitment to supply free morning-after pills at community pharmacies, ending postcode disparities and reinforcing condom and pill unit volumes. London and the West Midlands record the highest per-capita STI notifications, further elevating prophylactic demand.

Scotland contributes a smaller but influential share, using progressive initiatives such as bridging contraception to plug access gaps during appointment backlogs. Free-condom postal services complement the policy suite, and local Health Boards actively pilot telehealth models for LARC counselling. Wales benefits from regulatory harmonisation with England; its rural health boards rely heavily on e-pharmacy networks to ensure continuity of supply, particularly during tourist-season surges along the Pembrokeshire coast. Northern Ireland’s compliance with the European Union Medical Device Regulation adds an additional layer of certification but secures alignment with continental supply chains. The province’s younger demographic profile, coupled with targeted educational outreach, sustains condom volume growth despite a historically conservative cultural backdrop. Across all regions, digital platforms mitigate geographic inequities by centralising triage and logistics, ensuring that even remote islands receive deliveries within 48 hours.

Competitive Landscape

The UK contraceptive devices market hosts a moderately fragmented field where no single player exceeds one-third of revenue. Bayer leads the hormonal IUS category: Mirena, Kyleena, and the recently extended Levosert collectively shape clinical guidelines and influence formulary decisions. Cooper Surgical has refreshed its copper IUD offering with a single-hand inserter, a feature that trims clinic chair time and widens practitioner adoption. Reckitt-Benckiser’s Durex enjoys brand primacy in condoms, leveraging sustained investment in quality-control labs and marketing campaigns centred on STI prevention.

Digital disruptors increase competitive intensity. Community-pharmacy chains such as Boots blend e-commerce and clinical-service modules, capturing share from smaller independents and converting footfall into subscription repeats. NHS-approved portals like SH:24 position themselves as cost-avoidance tools for the public sector, compressing administrative overhead while meeting confidentiality expectations. Academic-industry collaborations, notably the University of Birmingham’s sperm-functionality study, create intellectual-property pipelines that established manufacturers may licence, accelerating product-portfolio renewal cycles.

Compliance capabilities serve as a growing differentiator under the MHRA’s strengthened surveillance regime. Firms with integrated pharmacovigilance systems respond faster to safety alerts, a feature that payers reward through preferred-supplier listings. Non-hormonal technologies represent white-space potential; early movers could insulate market positions by offering alternatives that sidestep hormone-related contraindications

UK Contraceptive Devices Industry Leaders

CooperSurgical, Inc.

Bayer AG

Gedeon Richter Plc

Organon & Co.

Reckitt Benckiser Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lovehoney partnered with Evaro to integrate an NHS-funded contraception service into its retail platform, providing online assessment and 48-hour home delivery.

- March 2025: The University of Birmingham secured Gates Foundation funding for a multi-country study on sperm functionality to advance non-hormonal female contraceptive research.

- October 2024: Boots rolled out the NHS Pharmacy Contraception Service to more than 1,250 stores across England.

- August 2024: Levosert received an eight-year UK licence extension, reinforcing long-term hormonal IUS positioning.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom contraceptive devices market as all barrier or implantable products, condoms, diaphragms, cervical caps, vaginal rings, intra-uterine devices, injectables, implants, and spermicidal aids, sold for the primary purpose of preventing pregnancy. Market values reflect factory-gate or landed prices, net of distributor margins and inclusive of NHS procurement and private sales.

Scope exclusion: Contraceptive drugs, permanent surgical sterilization, and fertility apps are outside the modeled universe.

Segmentation Overview

- By Type

- Condoms

- Diaphragms & Cervical caps

- Vaginal Rings

- Intra-Uterine Devices

- Implants & Injectables

- Spermicidal Devices

- Other Types

- By Gender

- Male

- Female

- By Distribution Channel

- NHS & Community Sexual-Health Clinics

- Retail Pharmacies

- Online Pharmacies & e-commerce

- Supermarkets & Convenience Stores

- Others (Charities, Youth Centres)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts completed expert interviews with clinicians in England and Scotland, regional NHS procurement officers, and executives from leading device distributors. These dialogues validated unit adoption curves, typical prices paid under the Pharmacy Contraception Service, and refill frequencies, giving us confidence to refine assumptions surfaced during secondary screening.

Desk Research

We initiated desk work by mapping publicly available supply and demand signals from tier-1 sources such as the Office for National Statistics, NHS Digital sexual-health dashboards, MHRA device registers, and HMRC trade codes, which outline import volumes of condoms and IUDs. Sector intelligence from associations like the Faculty of Sexual & Reproductive Healthcare, peer-reviewed journals on long-acting reversible contraception uptake, and reputable press releases rounded the foundation.

To enrich financial context, we tapped curated databases, D & B Hoovers for company revenues, Dow Jones Factiva for transactional news, and Questel for recent device patents, thereby anchoring volume, price, and innovation trends. The sources cited above are illustrative; many additional materials informed each datapoint.

Market-Sizing & Forecasting

A top-down reconstruction uses the population of women aged 15-49, contraceptive prevalence, method-mix ratios, and average selling price to estimate 2024 demand, which is then cross-checked through selective bottom-up roll-ups from key suppliers and import data. Variables such as STI incidence, e-pharmacy order share, policy shifts allowing pharmacist initiation of oral contraception, and average IUD dwell time feed a multivariate regression that projects volume and price through 2030. Where distributor or OEM splits were partial, gaps were bridged with channel checks and interpolated NHS spend shares.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, senior-analyst peer checks, and lead-author sign-off. We refresh each model annually, revisiting it sooner when material policy or supply events surface, ensuring clients always receive a current snapshot.

Why Our United Kingdom Contraceptive Devices Baseline Commands Reliability

Published market estimates often diverge because firms choose different product mixes, price points, and refresh cadences. According to Mordor Intelligence, clarity on scope and disciplined variable selection reduce these gaps for decision makers.

Key gap drivers include whether emergency contraception kits are bundled, how aggressively online sales growth is projected, and if currency is converted at transaction-date or constant rates. Our numbers reflect the device-only universe, use blended NHS plus retail prices, and update every twelve months; other publishers may fold pills into devices or freeze exchange rates for longer, skewing totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 652.38 M (2025) | Mordor Intelligence | - |

| USD 540 M (2024) | Regional Consultancy A | Combines drugs and devices share estimates, limited NHS channel validation |

| USD 395.62 M (2023) | Industry Tracker B | Historical base year, excludes e-commerce volumes and Scotland procurement data |

In summary, the modest variance across publishers stems mainly from scope and data-refresh choices. Mordor's balanced mix of real-world usage metrics, price audits, and timely updates delivers a dependable baseline that stakeholders can trace, reproduce, and stress-test with confidence.

Key Questions Answered in the Report

What is the 2026 value of the UK contraceptive devices market?

The market stands at USD 691.2 million in 2026

Which product type is growing fastest through 2031?

Intra-uterine devices are projected to expand at a 8.67% CAGR.

How have policy changes influenced pharmacy sales?

The January 2024 rule allowing pharmacist dispensing of oral contraception contributed to a 10% revenue increase at leading chains in 2024.

Why are condoms still the largest segment?

High STI prevalence makes dual-protection methods indispensable, keeping condoms at 55.22% revenue share in 2025.

Which channel shows the highest growth potential?

Online pharmacies and e-commerce, boosted by digital integration, are advancing at a 9.97% CAGR through 2031.

What regulatory trends affect market entry?

The MHRA’s 2024 post-market surveillance rules tighten safety reporting, raising compliance costs but strengthening user confidence.

Page last updated on: