Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

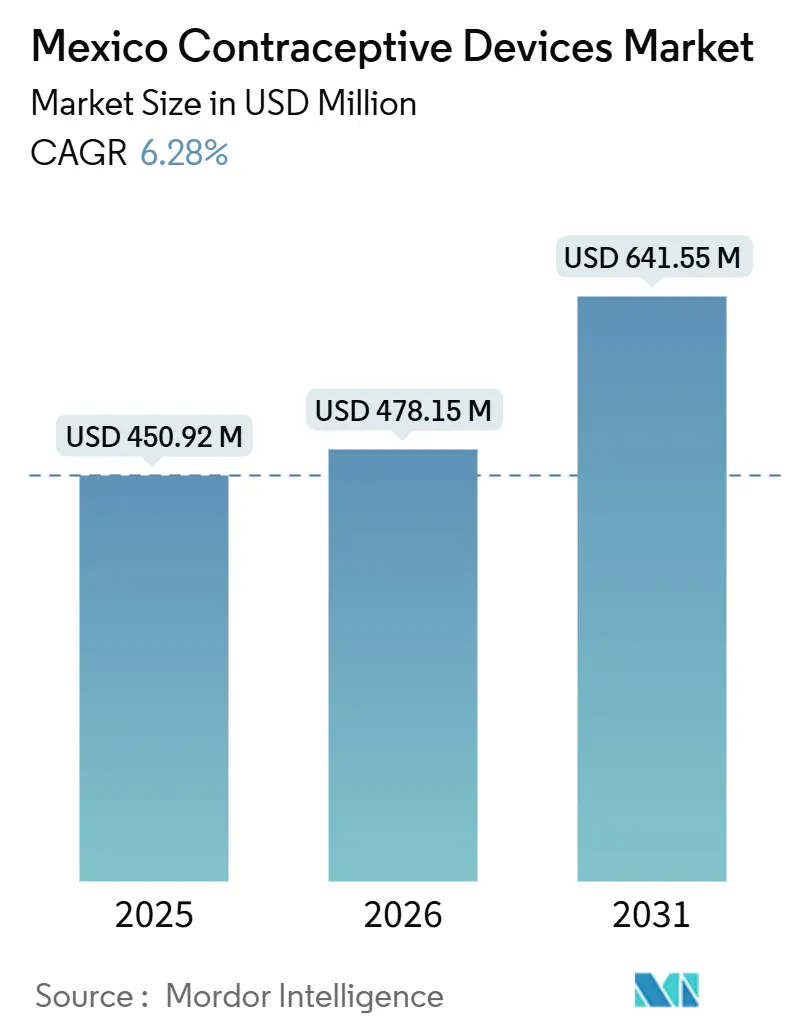

| Base Year Market Size (2025) | USD 450.92 Million |

| Market Size (2026) | USD 478.15 Million |

| Market Size (2031) | USD 641.55 Million |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

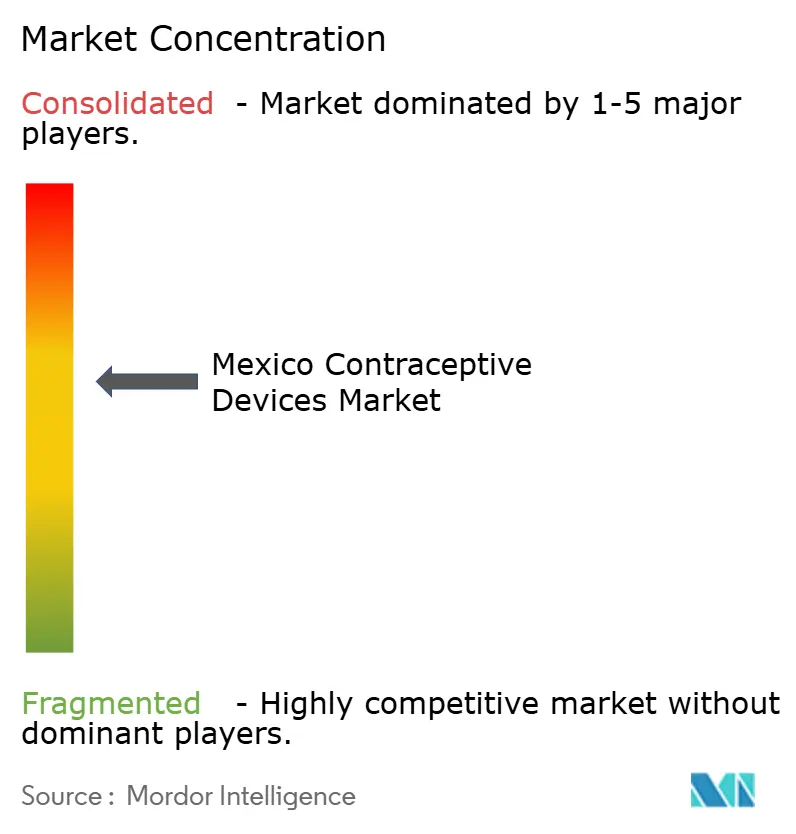

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Contraceptive Devices Market Analysis by Mordor Intelligence

The Mexico Contraceptive Devices Market size is expected to increase from USD 450.92 million in 2025 to USD 478.15 million in 2026 and reach USD 641.55 million by 2031, growing at a CAGR of 6.28% over 2026-2031.

Mexico’s persistently high adolescent fertility rate, rising sexually transmitted infection (STI) incidence, and an ambitious government procurement agenda continue to shape demand fundamentals. Public health authorities are scaling long-acting reversible contraceptive (LARC) programs in post-obstetric and adolescent-friendly services, while private buyers gravitate toward discreet online channels that bypass social stigma. Regulatory shifts now let BIRMEX import devices approved by reference regulators, which widens supplier pools but tightens price ceilings. Parallel nearshoring investments in Xochimilco, Querétaro, and the CaliBaja cluster promise lower unit costs and shorter lead times. Together, these forces position the Mexican contraceptive devices market for steady volume growth and deeper competitive rivalry through 2031.

Key Report Takeaways

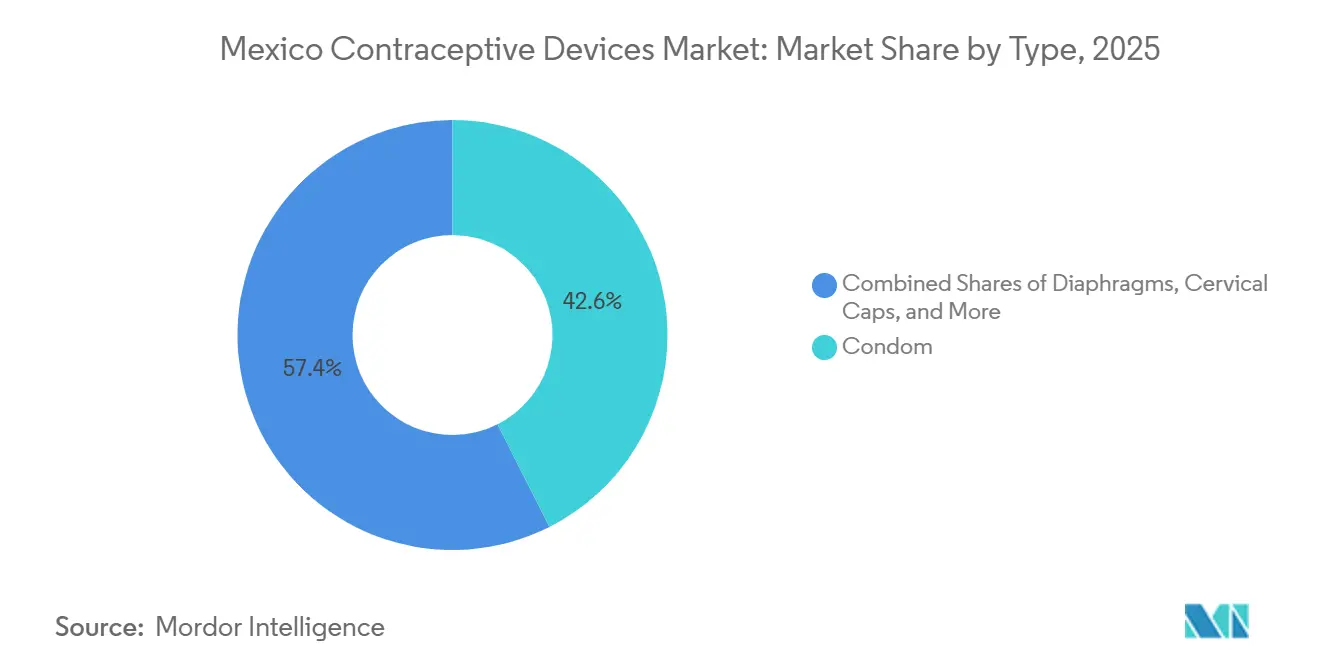

- By type, condoms led with 42.56% of the Mexico contraceptive devices market share in 2025, while intrauterine devices are forecast to grow at a 9.40% CAGR to 2031.

- By gender, female users accounted for 67.60% of 2025 revenue and are projected to grow at a 7.20% CAGR through 2031.

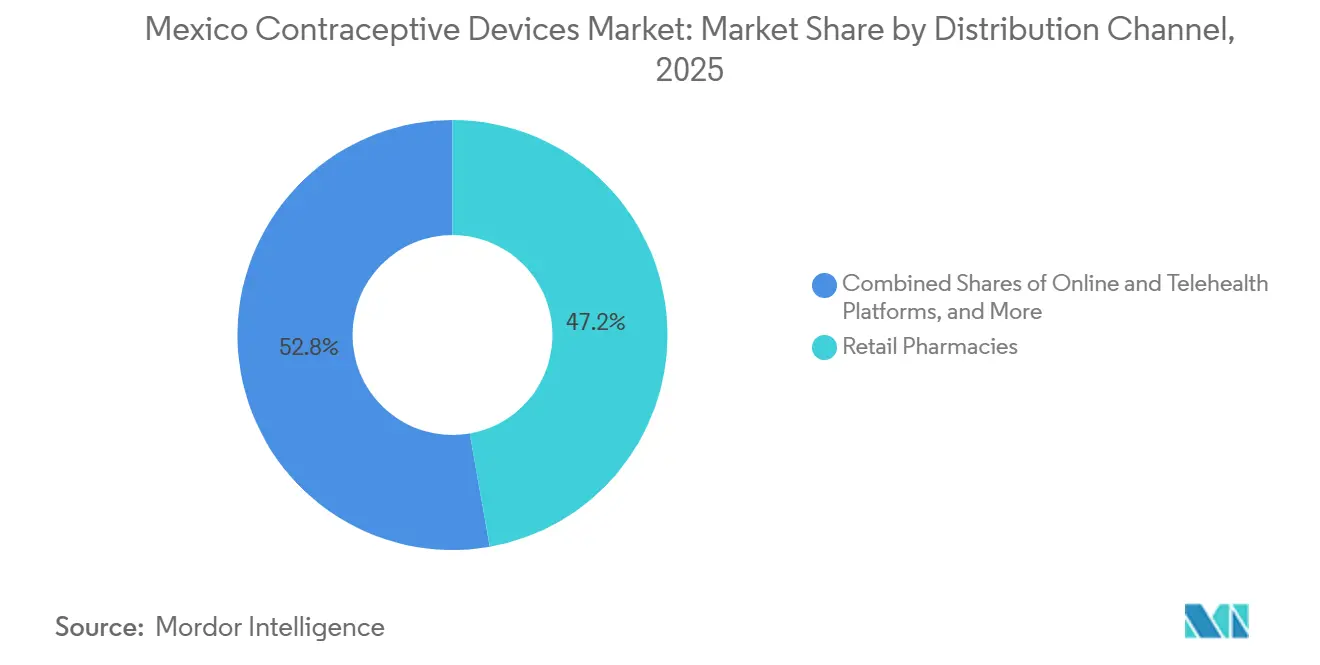

- By distribution channel, retail pharmacy platforms captured 47.23% of the Mexico contraceptive devices market in 2025, and online & telehealth Platforms are expanding at a 11.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent high adolescent fertility rate fueling contraceptive demand | 1.5% | National, with concentration in Estado de México, Chiapas, Guerrero, Puebla, Veracruz | Long term (≥ 4 years) |

| Escalating STI incidence prompting condom uptake | 0.8% | National, urban centers and border states with higher mobility | Medium term (2-4 years) |

| Expansion of government-funded distribution via BIRMEX consolidated tenders | 1.0% | National, 22 states served by BIRMEX Last-Kilometer infrastructure | Medium term (2-4 years) |

| Digital-first telehealth and e-pharmacy channels improving discreet access | 1.2% | National, accelerated adoption in Mexico City, Guadalajara, and Monterrey metropolitan areas | Short term (≤ 2 years) |

| Nearshored local device manufacturing reducing cost and import reliance | 0.7% | National, manufacturing hubs in Xochimilco (Mexico City), Querétaro, CaliBaja region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent High Adolescent Fertility Rate Fueling Contraceptive Demand

Teenage pregnancy stands at 77 births per 1,000 females aged 15-19, the highest figure in the OECD, and accounted for 16% of all births in Mexico in 2024.[1]Presidencia de la República, “Decreto Nearshoring,” presidencia.gob.mx Health authorities, therefore, prioritize provider-dependent implants and intrauterine devices over oral pills that require daily adherence. Walk-in LARC campaigns in Colima, Tabasco, and Mexico City remove documentation hurdles and keep demand resilient even when budgets contract. Continuous emphasis on post-obstetric contraception embeds LARC counseling into prenatal and delivery visits. As a result, structural demand for implants and copper IUDs is expected to outlast cyclical funding swings. Suppliers who can bundle device supply with clinical training support will capture disproportionate volume as adolescent-friendly services scale nationwide.

Escalating STI Incidence Prompting Condom Uptake

Mexico logged 16,323 new HIV infections in 2025, with the highest rates in Quintana Roo, Baja California Sur, Yucatán, Colima, and Tabasco.[2]Institute for Health Metrics and Evaluation, “CENSIDA,” ihmeuw.edu Dual-method counseling now appears in the January 2025 PROY-NOM-005-SSA-2025 draft, requiring providers to address STI protection along with pregnancy prevention. Condom awareness exceeds 89%, and both public tenders and private e-commerce outlets stock international brands such as Durex, LifeStyles, and Trojan. Growing surveillance by CENSIDA and heightened risk messaging among youth keep condom volumes resilient, even as LARC adoption rises. Manufacturers that pair branded education with online subscription models can widen margins in a category often treated as a commodity.

Expansion of Government-Funded Distribution via BIRMEX Consolidated Tenders

Mexico plans to centralize public health procurement under Birmex by 2030, aiming to improve supply reliability, pricing, and logistics.[3]BIRMEX, “Infraestructura Logística,” birmex.gob.mx Although its 2025-2026 megatender was annulled for overpricing, a December 2024 rule now allows imports cleared by trusted foreign regulators, accelerating competition but shaving prices. A June 2025 decree also links procurement preference to local production. Suppliers that establish Mexican assembly lines will gain tender priority under the new framework. Nevertheless, procurement resets inject timing uncertainty that can hamper stock continuity for state clinics. Consistent quality documentation and flexible pricing will become critical to maintain share in the Mexico contraceptive devices market.

Digital-First Telehealth & E-Pharmacy Channels Improving Discreet Access

Farmacias del Ahorro and Walmart Mexico have since expanded e-pharmacy footprints, while Doctoralia and on-demand couriers such as Rappi facilitate remote counseling and doorstep delivery. Barrier methods can be bought without a prescription, and oral pills require only a brief online questionnaire, removing the need for in-person visits. Digital health funding surpassed USD 50 million during 2021-2023, reflecting investor confidence in scalable e-pharmacy models. Smartphone penetration and m-payment adoption make online platforms the fastest-growing route to consumers, particularly younger cohorts seeking privacy. Device makers that integrate with telehealth ecosystems will secure early-mover advantages in the Mexico contraceptive devices market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Side-effect apprehension with hormonal and invasive devices | -0.9% | National, more pronounced in rural and indigenous communities | Medium term (2-4 years) |

| Cultural resistance in rural and indigenous communities | -0.6% | Rural areas, indigenous-majority states (Chiapas, Oaxaca, Guerrero, Yucatán) | Long term (≥ 4 years) |

| COFEPRIS post-market surveillance tightening raises compliance costs | -0.5% | National, affecting all manufacturers and importers | Short term (≤ 2 years) |

| Centralized procurement price ceilings squeeze innovator margins | -0.7% | National, impacting BIRMEX tender participants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Side-Effect Apprehension with Hormonal & Invasive Devices

First-year discontinuation for hormonal LARCs ranges from 30% to 40% owing to bleeding changes, weight gain, mood shifts, and IUD-related discomfort. Myths about infertility intensify reluctance, especially where counseling resources are scarce. Public clinics often provide reactive rather than proactive guidance, so negative anecdotes circulate quickly. Evidence-based side-effect management protocols are included in U.S. CDC guidance, yet their adoption in Mexico is uneven. Device makers that fund provider training and multilingual digital helplines can improve continuation rates and blunt this drag on the Mexico contraceptive devices market.

Cultural Resistance in Rural & Indigenous Communities

Modern contraceptive prevalence stands at 62% in rural zones versus 72% in cities, and indigenous women are twice as likely to forgo modern methods. Language gaps across 68 indigenous tongues and traditional male decision-making norms hinder uptake. The draft PROY-NOM-005-SSA-2025 now obliges culturally pertinent service delivery, yet progress will be incremental. Partnerships with NGOs such as MSI México, which deliver free implants via mobile clinics, illustrate viable outreach models. Brands willing to co-create content in native languages and engage community leaders can erode cultural obstacles over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: IUDs Propel LARC Shift

In 2025, condoms accounted for 42.56% of revenue, while intrauterine devices are forecast to grow at a 9.40% CAGR, the fastest among all categories. New offerings such as DKT’s SilverCare Mini address comfort and sizing issues for nulliparous women. The April 2025 FEUM draft set strict copper-purity and biocompatibility standards, solidifying quality expectations. Condoms will maintain their lead through reliable government tenders and the expanding e-commerce shelf, while implants and IUDs will capture incremental share as walk-in campaigns normalize LARC use. Niche devices like diaphragms and sponges remain constrained by low public-sector availability and user-dependent efficacy. Sustained education on dual protection will maintain condom relevance, but the long-term trend favors LARC penetration in the Mexico contraceptive devices market size for this segment.

Condom brands compete on price, latex quality, and eco credentials. Ansell advances natural rubber sourcing, while Reckitt leverages Durex brand equity for premium positioning. Implants enjoy tailwinds from PROY-NOM-005-SSA-2025, which mandates contraceptive offers during prenatal visits. As continuation rates improve, implants and IUDs will displace short-acting pills and injectables, reshaping the Mexican contraceptive devices market share across the method mix by 2031.

By Gender: Female Segment Dominance

Female users delivered 67.60% of 2025 revenue and are growing at a 7.20% CAGR. A January 2025 policy lets adolescents seek contraception without parental consent, widening the female addressable base. The segment covers oral pills, IUDs, implants, patches, injectables, vaginal rings, and female condoms, giving women multiple avenues to align contraception with life stage and health profile. Male options remain limited to condoms and vasectomy; reversible male hormonal products are not yet available in Mexico. Dual-method campaigns that pair female LARCs with male condoms for STI protection will sustain male participation but female methods will continue to dominate the Mexico contraceptive devices market.

By Distribution Channel: Digital Disruption

Retail pharmacies held a 47.23% share in 2025, driven by nationwide store density, yet online and telehealth platforms recorded an 11.50% CAGR and are on pace to outgrow every other channel. Amazon Pharmacy’s fast shipping, Farmacias del Ahorro’s omnichannel strategy, and Walmart’s online pharmacy have reshaped consumer expectations. Teleconsultations through Doctoralia satisfy prescription requirements for oral pills, and Rappi and Uber Eats deliver same-day. Hospital and clinic pharmacies remain central for insured populations because PROY-NOM-005-SSA-2025 mandates free contraceptive dispensing in public facilities. Yet urban millennials and Gen Z favor the convenience, anonymity, and subscription discounts offered by e-pharmacies. This dynamic will continue to shift shares toward digital formats in the Mexico contraceptive devices market.

Geography Analysis

Mexico City, Guadalajara, and Monterrey dominate private retail and e-pharmacy spend, benefiting from higher incomes, dense pharmacy networks, and robust last-mile logistics. The State of Mexico leads in implant placements due to its large population and proximity to federal hospitals. Rural states such as Chiapas, Oaxaca, Guerrero, and Yucatán rely heavily on public distribution, where unmet need can be 10 percentage points above urban averages. Indigenous populations face language barriers that undercut educational outreach, which contributes to lower modern contraceptive use. Border states like Baja California use cross-border purchasing to access United States brands, reflecting arbitrage on prices and availability. The CaliBaja manufacturing corridor strengthens export capacity, but domestic market uptake remains clustered in urban retail. Colima and Tabasco illustrate policy innovation by institutionalizing walk-in LARC clinics, a model now under review for nationwide replication. Geographic disparities will persist, yet digital channels mitigate some access gaps, particularly in areas with high smartphone uptake, thereby supporting a broad-based expansion of the Mexico contraceptive devices market.

Competitive Landscape

The market is moderately competitive. Bayer AG, Merck, Co., Inc., Pfizer Inc., Johnson & Johnson Services, Inc., and Reckitt Benckiser Group PLC share the stage with Ansell, Karex Berhad, and HLL Lifecare. DKT’s 2025 SilverCare Mini launch targets adolescents and nulliparous women, a niche underserved by standard copper devices. Condom competition hinges on brand equity and e-commerce logistics; Durex, LifeStyles, and Trojan dominate shelf space. Karex supplies private-label SKUs for cost-sensitive buyers and places aggressive bids in BIRMEX tenders. Nearshoring gives Organon and Abbott a cost edge for public procurement. NGOs such as MSI México disrupt rural markets by distributing free implants funded by philanthropy. Telemedicine firms like Doctoralia and pharmacy apps integrate prescription, payment, and delivery into one workflow, shifting power toward digital gatekeepers. As COFEPRIS compliance demands scale resources and BIRMEX margins tighten, players with local plants, diversified channels, and strong cash flow will consolidate share in the Mexico contraceptive devices market.

Mexico Contraceptive Devices Industry Leaders

Bayer AG

Cooper Surgical Inc.

Pregna International Limited

Reckitt Benckiser Group PLC

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DKT Mexico extended its support to migrant women in Mexico by facilitating access to contraceptive devices, addressing their reproductive health needs.

- October 2025: DKT introduced the hormone-free SilverCare Mini IUD aimed at adolescents and nulliparous women, reducing insertion discomfort and targeting public-sector LARC programs.

- June 2025: A presidential decree linked public procurement preference to domestic manufacturing, signaling future BIRMEX tenders will favor suppliers with Mexican production footprints.

Mexico Contraceptive Devices Market Report Scope

As per the scope of the report, contraceptive devices are barriers that attempt to prevent pregnancy by physically preventing sperm from entering the uterus. Contraception is more commonly known as fertility and birth control and is described as the method used to avoid pregnancy. They include male condoms, female condoms, cervical caps, diaphragms, and contraceptive sponges with spermicide.

The Mexico contraceptive devices market is segmented by type, gender, and distribution channel. By type, the market is segmented into condoms, diaphragms, cervical caps, sponges, vaginal rings, intra-uterine devices, and implants. By gender, the market is segmented into male and female. By distribution channel, the market is segmented into hospital & clinic pharmacies, retail pharmacies, and online & telehealth platforms. The market forecasts are provided in terms of value (USD).

By Type

| Condoms |

| Diaphragms |

| Cervical Caps |

| Sponges |

| Vaginal Rings |

| Intra-Uterine Devices (IUD) |

| Implants |

By Gender

| Male |

| Female |

By Distribution Channel

| Hospital & Clinic Pharmacies |

| Retail Pharmacies |

| Online & Telehealth Platforms |

| By Type | Condoms |

| Diaphragms | |

| Cervical Caps | |

| Sponges | |

| Vaginal Rings | |

| Intra-Uterine Devices (IUD) | |

| Implants | |

| By Gender | Male |

| Female | |

| By Distribution Channel | Hospital & Clinic Pharmacies |

| Retail Pharmacies | |

| Online & Telehealth Platforms |

Key Questions Answered in the Report

How large is the Mexico contraceptive devices market in 2026?

It reached USD 450.92 million in 2026 and is on track for USD 641.55 million by 2031 at a 6.28% CAGR.

Which contraceptive type is growing fastest in Mexico through 2031?

Intrauterine devices lead with a projected 9.40% CAGR, driven by government LARC campaigns and improved adolescent access.

Why are online and telehealth channels important for contraception sales in Mexico?

They remove purchase stigma, offer 24/7 access, and are expanding at an 11.50% CAGRoutpacing retail pharmacies.

How does government procurement influence device pricing?

BIRMEXs consolidated tenders impose aggressive price ceilings, compressing innovator margins while guaranteeing large volumes.

What regulatory changes affect contraceptive suppliers in Mexico?

COFEPRISs 2025 framework requires stricter reporting and in-country testing, raising compliance costs but aligning with global standards.

Which regions show the highest unmet contraceptive need?

Rural and indigenous-majority states such as Chiapas, Oaxaca, Guerrero, and Yucatán lag urban centers by about 10 percentage points in modern method use.

Page last updated on: