Italy Contraceptive Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

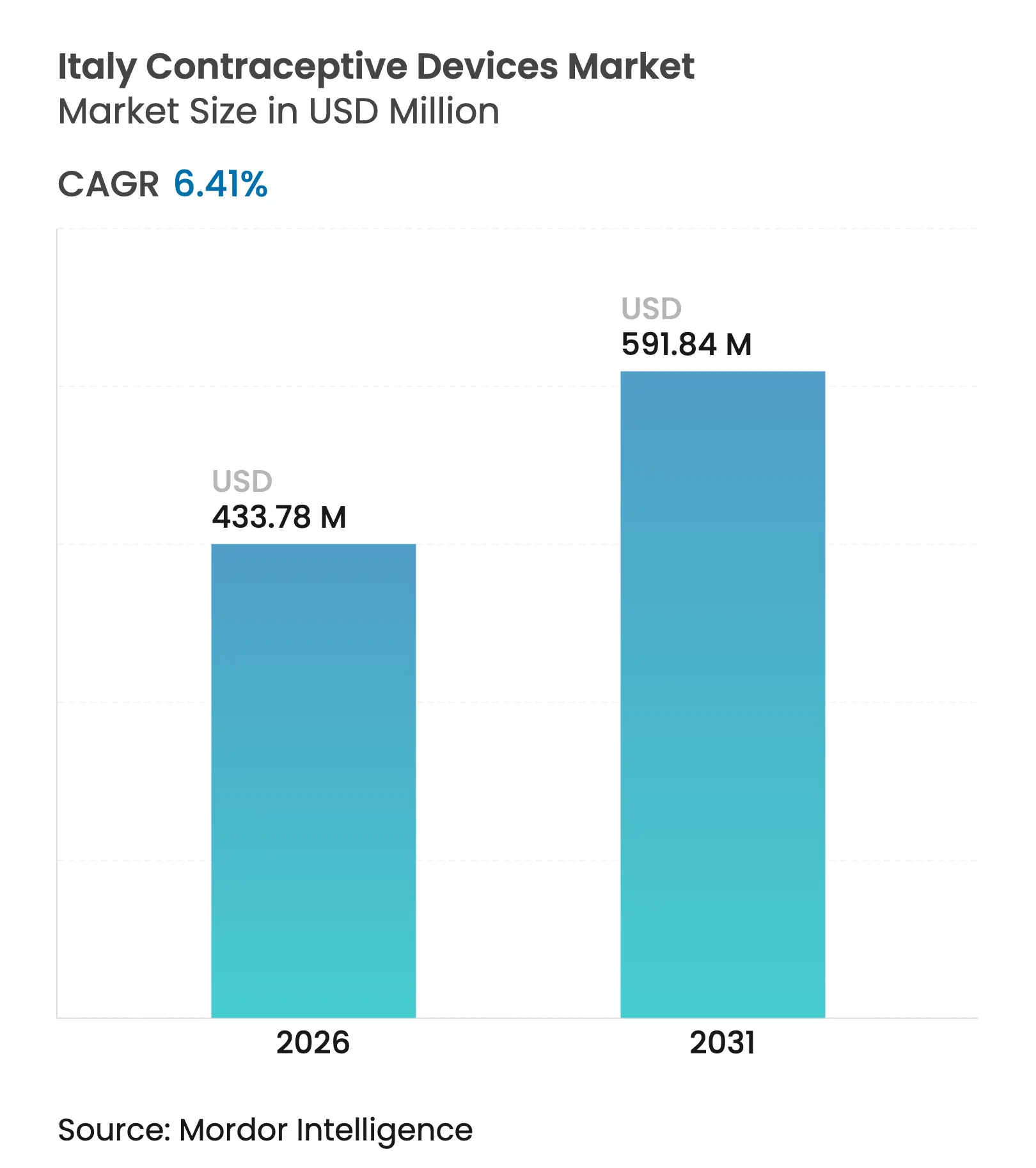

| Market Size (2026) | USD 433.78 Million |

| Market Size (2031) | USD 591.84 Million |

| Growth Rate (2026 - 2031) | 6.41 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Italy Contraceptive Devices Market Analysis by Mordor Intelligence

The Italy contraceptive devices market size was valued at USD 407.66 million in 2025 and estimated to grow from USD 433.78 million in 2026 to reach USD 591.84 million by 2031, at a CAGR of 6.41% during the forecast period (2026-2031). Solid public-sector investment, rising sexually transmitted infection (STI) alerts, and rapid digital-health adoption are driving uptake, even as regional conscience-based objections create pockets of unmet need. The Italian Medicines Agency’s June 2024 decision to offer free contraceptives to women under 26 increases baseline demand, while growing e-commerce penetration removes traditional access barriers in underserved areas. Manufacturers that balance cost-effective public-tender offerings with premium eco-friendly lines are best positioned to capture the Italy contraceptive devices market’s widening opportunity set. Regulatory timelines under the EU Medical Device Regulation remain a headwind but also raise the bar for product quality, favoring well-capitalized players.

Key Report Takeaways

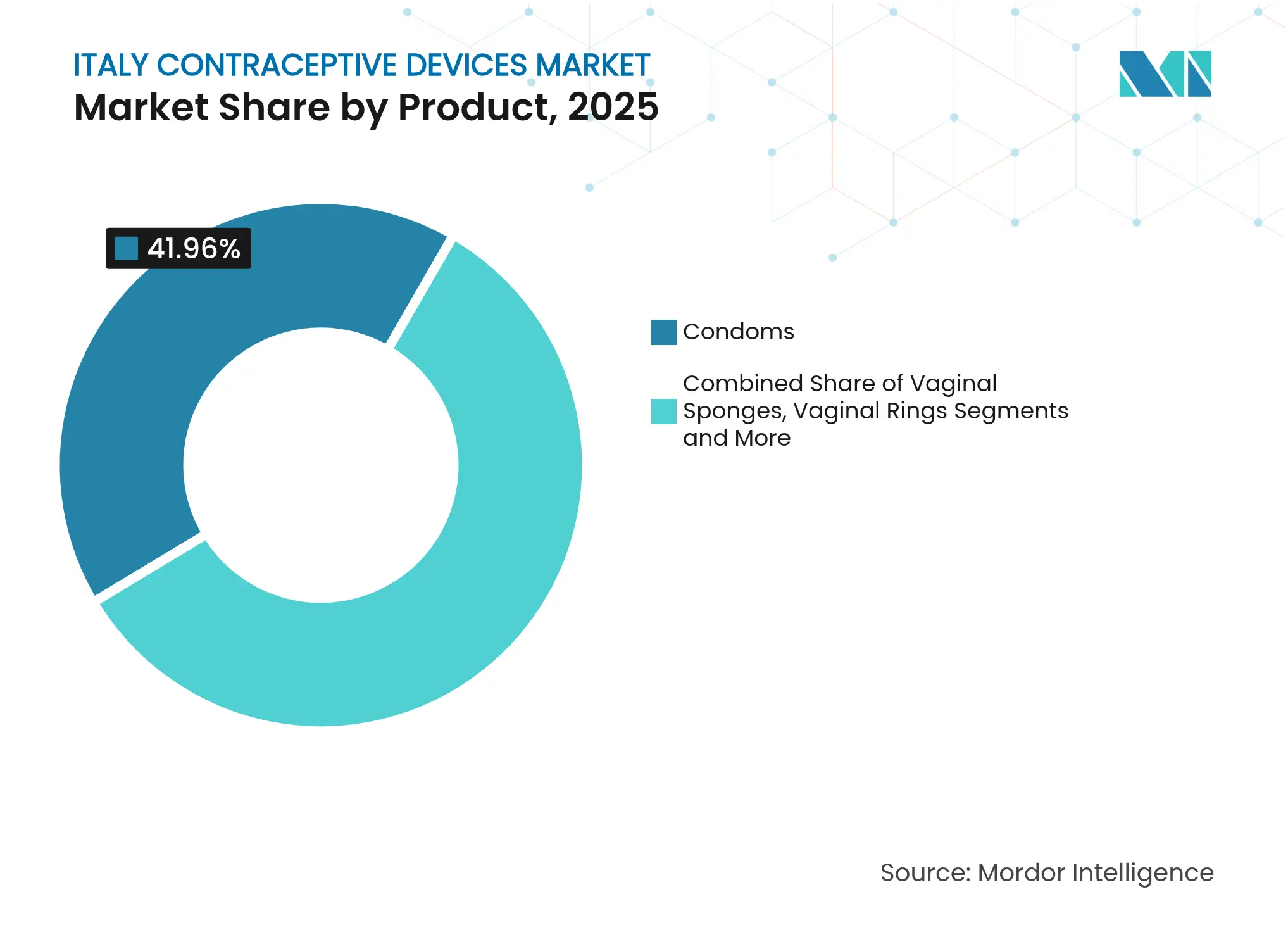

- By product type, condoms held the leading 41.96% Italy contraceptive devices market share in 2025, whereas intrauterine devices are forecast to post the fastest 8.05% CAGR through 2031.

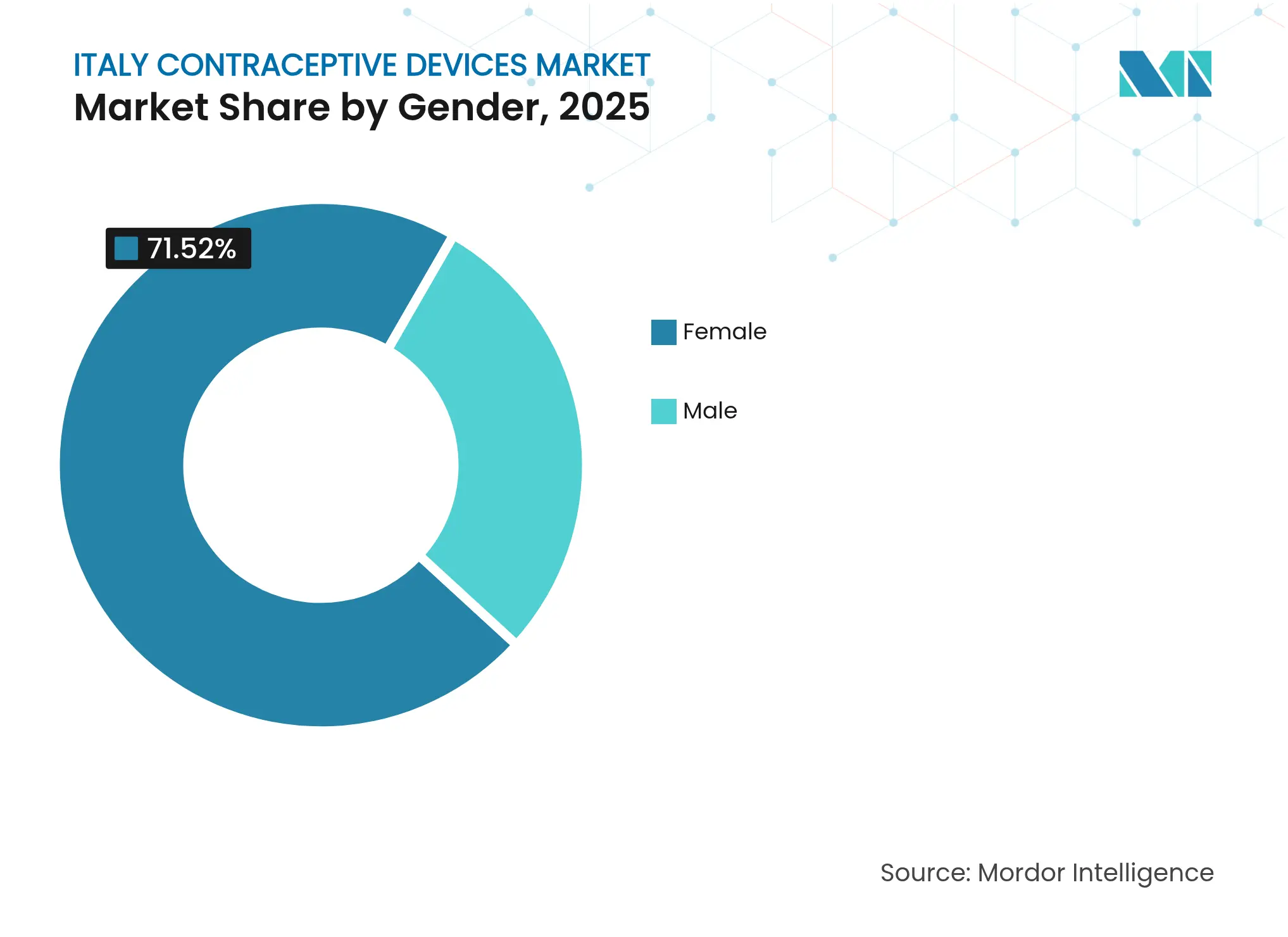

- By gender, female-oriented devices commanded 71.52% of 2025 revenue; the male segment records the highest 7.12% CAGR to 2031.

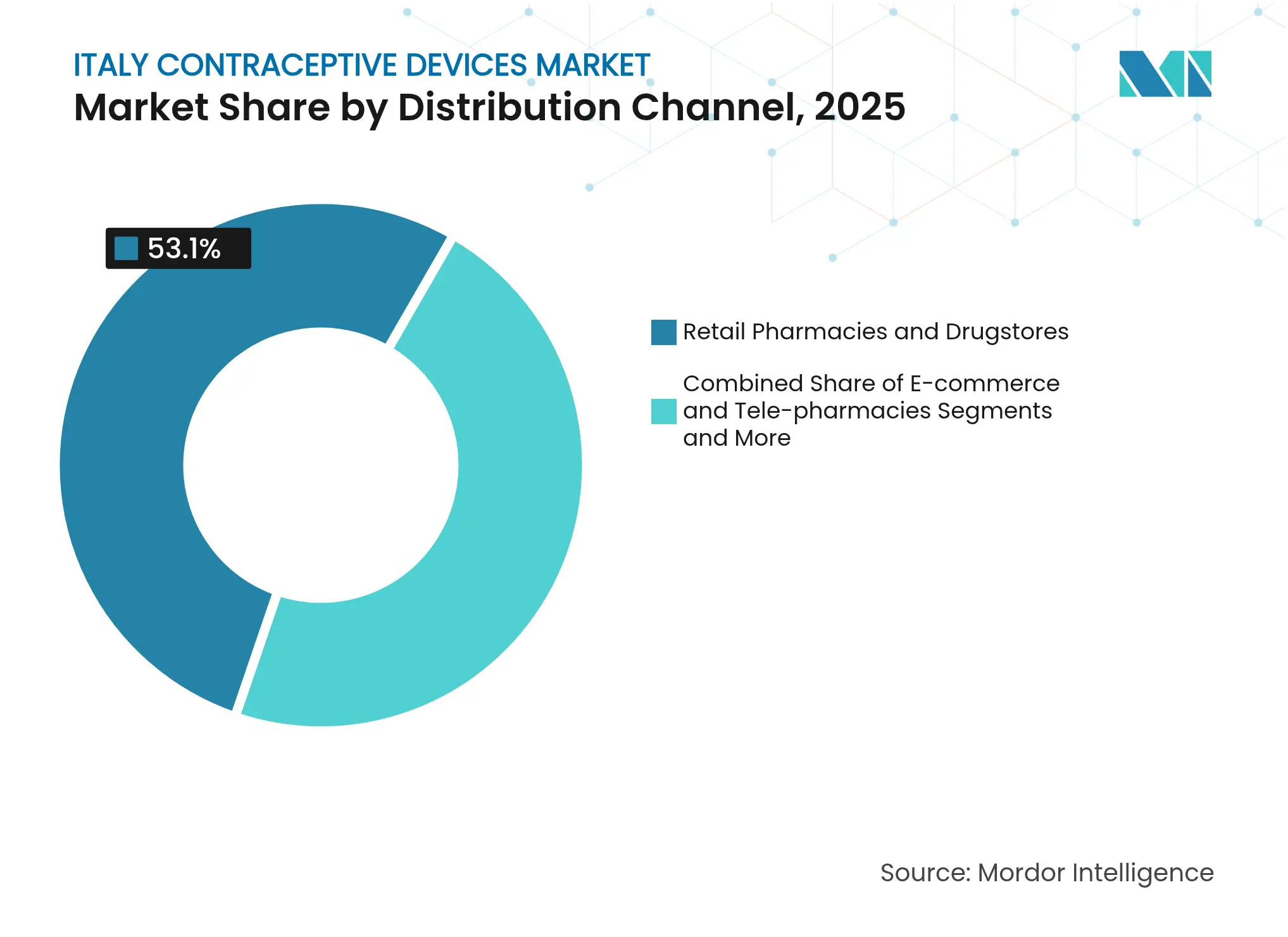

- By distribution channel, retail pharmacies accounted for 53.10% of the Italy contraceptive devices market size in 2025, while e-commerce and tele-pharmacy platforms are expanding at a 10.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High burden of STIs and growing STD

awareness

High burden of STIs and growing STD

awareness

| +1.2% | National, higher in urban centers | Medium term (2-4 years) | ( ~ ) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

National, higher in urban centers

|

Impact Timeline

:

Medium term (2-4 years)

|

High rate of unintended pregnancies

High rate of unintended pregnancies

| +1.5% | National, greatest where access is limited | Short term (≤ 2 years) | |||

Government and non-profit

initiatives to reduce early pregnancy

Government and non-profit

initiatives to reduce early pregnancy

| +0.8% | National, with targeted programs | Long term (≥ 4 years) | |||

Expansion of tele-pharmacy and

e-prescription platforms

Expansion of tele-pharmacy and

e-prescription platforms

| +1.8% | National, strongest in Northern Italy | Short term (≤ 2 years) | |||

Rising demand for non-hormonal,

latex-free products

Rising demand for non-hormonal,

latex-free products

| +0.7% | National, premium urban segments | Medium term (2-4 years) | |||

Delayed family-planning trend and demographic

shift

Delayed family-planning trend and demographic

shift

| +1.0% | National, chiefly metropolitan areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High burden of STIs and growing STD awareness

Italy recorded an rise in STI alerts, prompting a prevention-focused National Plan that prioritizes free condom distribution and broader PrEP access. School-based programs such as EduforIST reinforce dual-protection messaging and have already reached more than 1,200 students across four regions. Together these initiatives are lifting demand for barrier devices, particularly among adolescents and young adults who respond quickly to health-risk education.

High rate of unintended pregnancies

Class C pharmaceutical outlays rose to EUR 7.1 billion in 2023, up 9.8%, underscoring the cost of suboptimal family-planning coverage.[1]Agenzia Italiana del Farmaco, “The Use of Medicines in Italy 2023,” AIFA, aifa.gov.it AIFA. AIFA’s EUR 140 million annual subsidy for women under 26 now removes the price hurdle for long-acting reversible contraceptive (LARC) devices. Early uptake data suggest a shift toward intrauterine devices that offer superior efficacy over user-dependent methods.[2]Redazione, “AIFA Approva la Contraccezione Gratuita per Tutte,” Quotidiano Sanità, quotidianosanita.it

Government and non-profit initiatives to reduce early pregnancy

National Law 194 permits minors to access contraception without age limits, and AIFA has lifted prescription requirements for emergency methods. Non-profit organizations extend outreach through culturally attuned counseling, anchoring long-run growth by establishing early engagement with reliable contraceptive solutions.

Expansion of tele-pharmacy and e-prescription platforms

Research on Italy’s drug distribution network identifies community pharmacies as critical access points that lighten hospital workloads during crises. Online ordering and home delivery compensate for conscious-objection shortages in parts of the country, pushing the Italy contraceptive devices market into double-digit e-commerce growth.

Restraints Impact Analysis

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Side effects linked to intrauterine

and hormonal devices

Side effects linked to intrauterine

and hormonal devices

| -0.9% | National, higher where care access is low | Medium term (2-4 years) | ( ~) % Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

National, higher where care access

is low

|

Impact Timeline

:

Medium term (2-4 years)

|

Religious-cultural resistance in

Southern regions

Religious-cultural resistance in

Southern regions

| -1.3% | Southern Italy | Long term (≥ 4 years) | |||

EU-MDR compliance raises cost and

slows launches

EU-MDR compliance raises cost and

slows launches

| -0.8% | Nationwide | Short term (≤ 2 years) | |||

Shortage of trained medical

professionals

Shortage of trained medical

professionals

| -1.1% | Nationwide, acute in rural South | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Religious-cultural resistance in Southern regions

Conscientious objection reaches 91% of physicians in Molise and exceeds 79% in Sicily and Basilicata, shrinking service access points below mandated thresholds. Community stigma further dampens adoption by discouraging open discussion and purchase of modern contraceptives.

Shortage of trained medical professionals

Family-planning clinics fell from 1,871 in 2021 to 1,819 in 2022, mirroring broader staff gaps. Provider scarcity directly limits uptake of long-acting products that need specialist insertion, prompting consumers to favor self-administered options where available.

Segment Analysis

By Product Type: Condoms hold lead while IUDs accelerate

Condoms represented 41.96% Italy contraceptive devices market share in 2025, benefiting from immediate availability and zero clinician involvement. Their grip remains strong where provider refusal is common. In contrast, intrauterine devices post the fastest 8.05% CAGR through 2031 on the back of AIFA’s under-26 subsidy and evidence of superior pregnancy avoidance. The Italy contraceptive devices market size for IUDs is on track to rise sharply as insertion training expands within public clinics. Niche products such as diaphragms serve users seeking hormone-free alternatives, while subdermal implants advance steadily despite limited specialist capacity in the South. Vaginal rings add upside potential through combined health-benefit formulations. Female sterilization, including laparoscopic tubal ligation, is chosen by women concluding family building; legal and clinical guidance point to the lowest 10-year pregnancy risk among permanent options.

Advances in smart materials and eco-friendly coatings enlarge the condom subsegment’s premium tier. Meanwhile, European real-world data show 96.3% of Italian LARC users opt for IUDs chiefly for contraception. Over the forecast horizon, manufacturers that offer both cost-efficient barrier methods and higher-margin LARCs can mitigate price compression from public tenders.

Note: Segment shares of all individual segments available upon report purchase

By Gender: Female devices dominate yet male solutions grow

Female products controlled 71.52% of revenue in 2025, mirroring long-standing care pathways through gynecological clinics. The Italy contraceptive devices market size allocated to female methods is expected to grow steadily but share will narrow as male offerings gain traction. Male devices record a 7.12% CAGR because younger couples seek shared responsibility and dual-protection against infections. Traditional condoms already make up 35% of national contraceptive use. Pipeline developments in reversible hormonal gels and heat-based devices attract rising media coverage and could open new revenue lanes late in the forecast window.

Cultural evolution complements technology. Surveys show higher male participation in reproductive-health decisions in metropolitan areas where STI messaging is pervasive. Marketing narratives that highlight partnership and health co-ownership resonate with this audience and underpin the male segment’s fast clip despite its smaller baseline.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Retail strength meets digital disruption

Retail pharmacies captured 53.10% of 2025 turnover, and remain the first stop for counseling on side effects and product choice. Pharmacists’ established rapport with customers sustains loyalty even as online services grow. The e-commerce-plus-tele-pharmacy route produces a 10.56% CAGR to 2031, the quickest across channels, by matching privacy preferences and reducing travel requirements in regions with scarce providers. The Italy contraceptive devices market share for online channels will surpass hospital pharmacies before 2027. Community-pharmacy click-and-collect models blend digital convenience with human advice, giving omnichannel firms an edge. Family-planning clinics, although fewer in number, still serve as insertion hubs for LARCs and hold strategic value for companies targeting long-acting portfolio growth.

COVID-19 normalized telemedicine for contraception refills, and insurers now reimburse remote consults at parity with in-person visits, spurring permanent behavior change. Firms integrating prescription fulfillment into tele-consult platforms secure recurring revenue while creating data loops that sharpen demand forecasting.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Northern regions such as Lombardia, Veneto, and Emilia-Romagna exhibit the highest per-capita spending on contraceptive devices, aided by robust provider availability and lower conscientious-objection rates. Urban centers Milan, Turin, and Bologna favor premium innovations including latex-free condoms and smart rings that sync with mobile reminders. Regional school programs embed sexuality education early, cementing contraceptive literacy and brand familiarity.

Central areas, notably Lazio and Toscana, present blended characteristics. Rome’s cosmopolitan population mirrors Northern adoption patterns, yet pockets of cultural conservatism linger in rural provinces. Targeted outreach via tele-pharmacy mitigates these micro-barriers, bolstering the Italy contraceptive devices market presence across Central Italy.

Southern Italy, led by Molise, Sicily, and Basilicata, trails owing to 79%–91% physician objection rates and scarce family-planning clinics. Consumers often rely on retail stores for condoms or purchase online to avoid stigma. E-commerce growth here outpaces the national average as digital platforms circumvent local resistance. Government efforts to expand free-contraceptive distribution are expected to soften disparities, yet near-term growth continues to hinge on remote access tools and grassroots education.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The market remains moderately fragmented. No single company exceeds a one-quarter share, and the top five players together hold about 40%. Multinationals leverage scale to navigate EU-MDR paperwork, while local firms exploit cultural insight and agile digital marketing. Following the under-26 reimbursement policy, competition intensifies around public tenders, pressing prices yet enlarging volumes. Successful suppliers pair economy lines for the subsidized cohort with premium SKUs aimed at self-pay urban users.

Strategic activity centers on omnichannel engagement. Leading brands integrate telemedicine scripts, same-day pharmacy pickup, and loyalty apps to retain customers. Sustainability claims, such as biodegradable condoms or reduced-plastic packaging, differentiate offerings among environmentally focused millennials. Male-method innovation remains a white space, with early-stage research in reversible vas-occlusive devices attracting venture funding.

Italian firms like S&R Farmaceutici scale up women’s-health portfolios and sponsor continuing-education events to shore up clinician advocacy. International entrants partner with regional distributors to navigate linguistic nuances and variable provider attitudes, ensuring consistent in-store merchandising and compliance training across the country.

Italy Contraceptive Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Italian Ministry of Health finalized the National Plan for HIV, hepatitis, and STI prevention 2024-2028, including free condom distribution and expanded PrEP access programs.

- December 2024: Altroconsumo launched a national campaign seeking redress for harm linked to Essure contraceptive devices.

- October 2024: S&R Farmaceutici expanded its women’s-health line and supported the 8th Interactive Obstetrics and Gynecology Course in Capri to deepen physician ties.

Table of Contents for Italy Contraceptive Devices Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1High Burden of STIs and Increasing awareness of STDs

- 4.2.2High rate of unintended Pregnancies

- 4.2.3Government and Non Profit Organziation Initiatives for Reducing Pregancy at Early Age

- 4.2.4Expansion of Tele-pharmacy & e-prescription Platforms

- 4.2.5Rising Demand for Non-Hormonal, Eco-friendly/Latex-free Products

- 4.2.6Delayed Family Planning Trend and Demographic Shift

- 4.3Market Restraints

- 4.3.1Side-effects Linked to Intra-uterine & Hormonal Devices

- 4.3.2Religious-cultural Resistance in Southern Regions

- 4.3.3EU-MDR Compliance Raises Device Cost & Time-to-market

- 4.3.4Shortage of Trained Medical Professionals

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Product Type

- 5.1.1Condoms

- 5.1.2Diaphragms and Cervical Caps

- 5.1.3Vaginal Sponges

- 5.1.4Vaginal Rings

- 5.1.5Intra-Uterine Devices (IUD)

- 5.1.6Subdermal Implants

- 5.1.7Spermicidal Devices

- 5.1.8Tubal Sterilization Clips

- 5.2By Gender

- 5.2.1Male

- 5.2.2Female

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Retail Pharmacies & Drugstores

- 5.3.3E-commerce & Tele-pharmacies

- 5.3.4Family-planning Clinics

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Reckitt Benckiser Group plc

- 6.3.2Bayer AG

- 6.3.3CooperSurgical Inc.

- 6.3.4Organon & Co.

- 6.3.5Church & Dwight Co. Inc.

- 6.3.6DKT International

- 6.3.7Okamoto Industries Inc.

- 6.3.8Pregna International Ltd.

- 6.3.9Veru Inc.

- 6.3.10Linepharma International

- 6.3.11LifeStyles Healthcare Pty Ltd.

- 6.3.12Control

- 6.3.13Mithra Pharmacueticals

- 6.3.14Exeltis Healthcare

- 6.3.15Gedeon Richter

- 6.3.16MKT PHARMA SAS DI RITA

- 6.3.17OCON Medical Ltd.

7. Market Opportunities and Future Outlook

- 7.1White-Space and Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian contraceptive devices market as all non-pharmacological products that create a physical or hormonal barrier to prevent pregnancy (condoms, diaphragms, cervical caps, vaginal rings, intra-uterine devices, subdermal implants, spermicidal carriers, and tubal clips included).

Scope exclusion: emergency contraceptive pills and injectables fall outside this remit.

Segmentation Overview

- By Product Type

- Condoms

- Diaphragms and Cervical Caps

- Vaginal Sponges

- Vaginal Rings

- Intra-Uterine Devices (IUD)

- Subdermal Implants

- Spermicidal Devices

- Tubal Sterilization Clips

- Condoms

- By Gender

- Male

- Female

- Male

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drugstores

- E-commerce & Tele-pharmacies

- Family-planning Clinics

- Hospital Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with gynecologists in Lombardy, pharmacy chains in Lazio, and distributors active in Sicily; then validated pricing, conscientious-objection service gaps, and hormonal-IUD adoption trends.

Web surveys of women aged 18-45 quantified brand switching triggers and willingness to pay, giving us confidence to close residual information gaps.

Desk Research

We sifted health-ministry procurement bulletins, Eurostat birth-rate tables, customs import codes 392690 and 9021, and position papers from the Italian Gynecology & Obstetrics Society, alongside peer-reviewed journals that chart device uptake.

Company 10-Ks, AIFA price lists, and open tender portals added recent volume and average-selling-price clues. Paid databases such as D&B Hoovers for local revenue splits and Dow Jones Factiva for recall notices rounded out baseline inputs.

We also cross-walked retail scanner data from Nielsen IQ extracts with shipment-level volumes pulled from Volza to gauge the rapid migration toward e-commerce. The sources named illustrate the mix, while many other references supported data checks and context building.

Market-Sizing & Forecasting

The core model begins with a top-down reconstruction of national demand using live-birth counts, sexually active female population, and contraceptive prevalence ratios, which are filtered through method-specific penetration and replacement factors.

Supplier roll-ups and sampled ASP × unit checks provide a bottom-up lens that adjusts outliers before totals lock. Key variables include public reimbursement for women under 26, condom import growth, physician conscientious-objection rates, digital prescription uptake, and EU-MDR compliance costs.

A multivariate regression, supported by expert consensus, drives the 2025-2030 forecast, and scenario analysis handles policy shocks.

Data Validation & Update Cycle

Outputs pass variance thresholds versus Eurostat fertility shifts and AIFA sales audits; then a senior analyst reviews anomalies.

Reports refresh each year, with interim updates when material events (for instance, reimbursement rule changes) occur. A final pass just before delivery ensures clients receive the latest view.

Why Our Italy Contraceptive Devices Baseline Commands Reliability

Benchmark comparison

Published estimates often differ because firms pick different scopes, refresh cadences, and channel assumptions.

We flag three usual gap drivers: mixing drugs with devices, omitting internet-only sales, and freezing exchange rates at data collection rather than analysis.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 407.66 million (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 463.8 million (2025) | Regional Consultancy A | Bundles hormonal implants with pill kits and keeps a fixed euro-dollar rate | ||

USD 424.44 million (2023) | Trade Journal B | Uses urban pharmacy panel only and omits direct-to-consumer online volumes |