Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

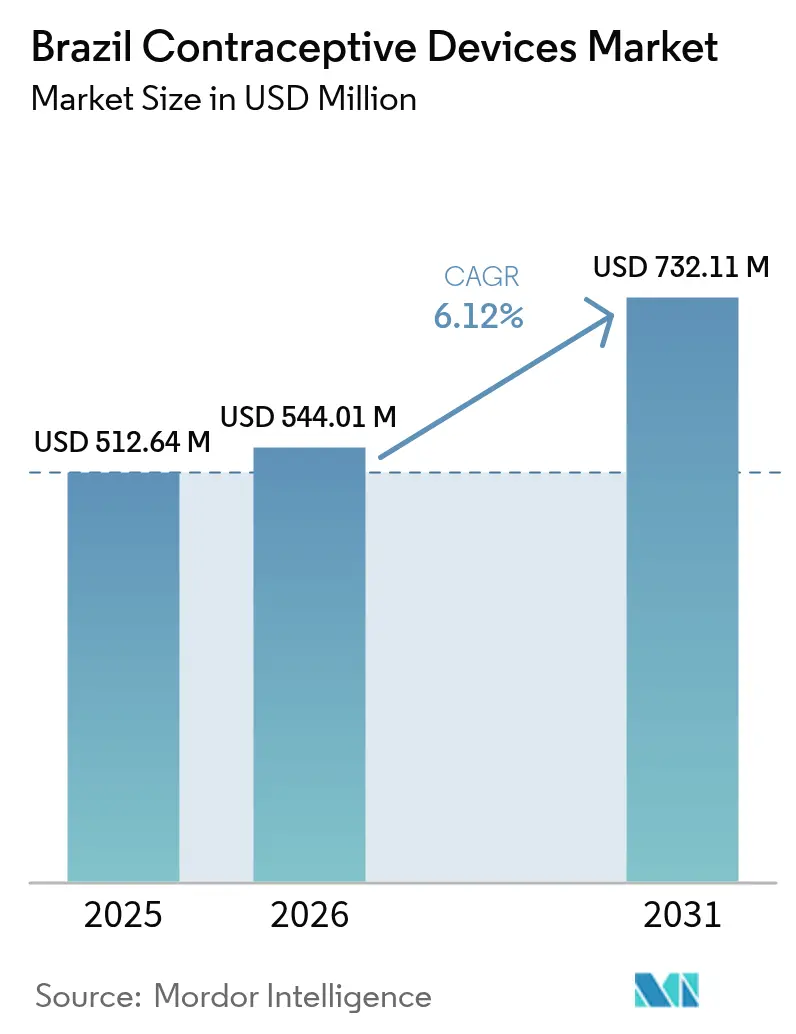

| Base Year Market Size (2025) | USD 512.64 Million |

| Market Size (2026) | USD 544.01 Million |

| Market Size (2031) | USD 732.11 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Contraceptive Devices Market Analysis by Mordor Intelligence

Brazil contraceptive devices market size in 2026 is estimated at USD 544.01 million, growing from 2025 value of USD 512.64 million with 2031 projections showing USD 732.11 million, growing at 6.12% CAGR over 2026-2031. This trajectory reflects a policy environment that prioritizes domestic manufacturing, streamlined regulation, and primary-care expansion, all of which collectively widen method availability and spur technological upgrades. Rapid growth in e-commerce and direct-to-consumer channels strengthens privacy and price transparency, encouraging uptake among digitally active users. Heightened concern around sexually transmitted infections (STIs) sustains barrier-method demand, while government promotion of long-acting reversible contraceptives (LARCs) stimulates implant and IUD adoption. Material innovation focused on hypoallergenic and biodegradable options differentiates brands and aligns with Brazil’s rising environmental consciousness. Competitive positioning hinges on local production capacity, regulatory know-how, and the ability to pair digital engagement with clinician outreach.

Key Report Takeaways

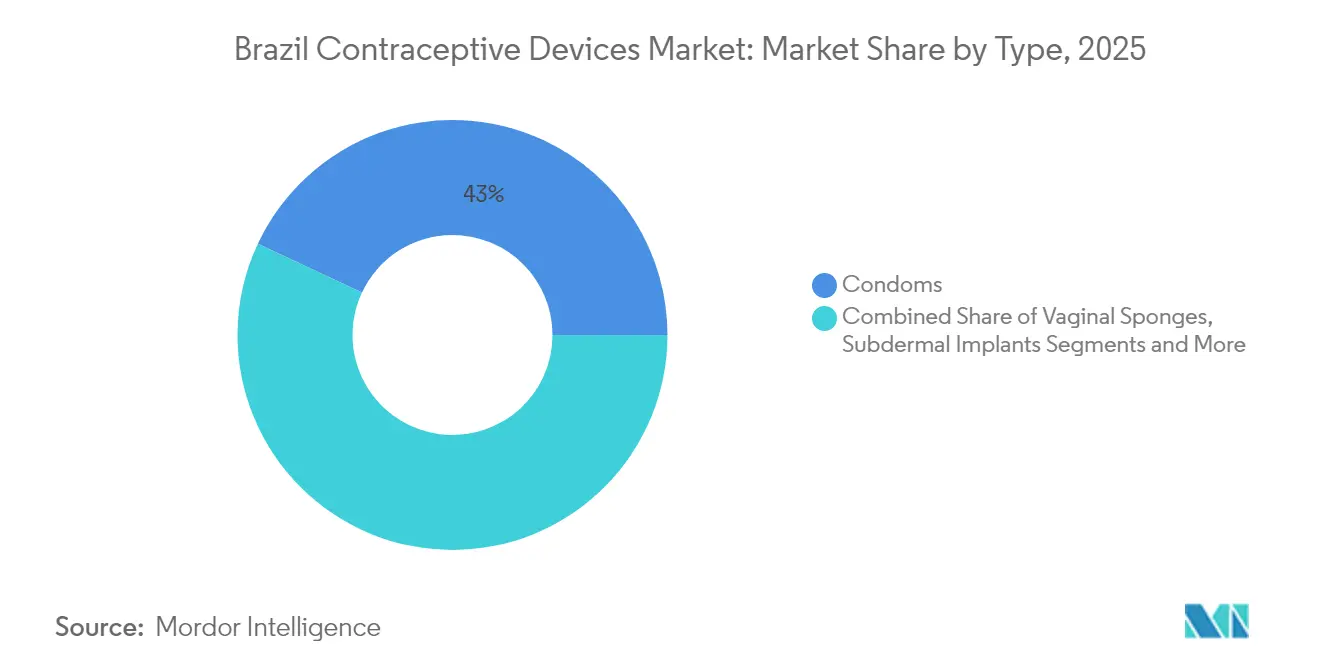

- By type, condoms led with 43.02% of Brazil contraceptive devices market share in 2025, whereas subdermal implants are set to expand at a 7.12% CAGR to 2031.

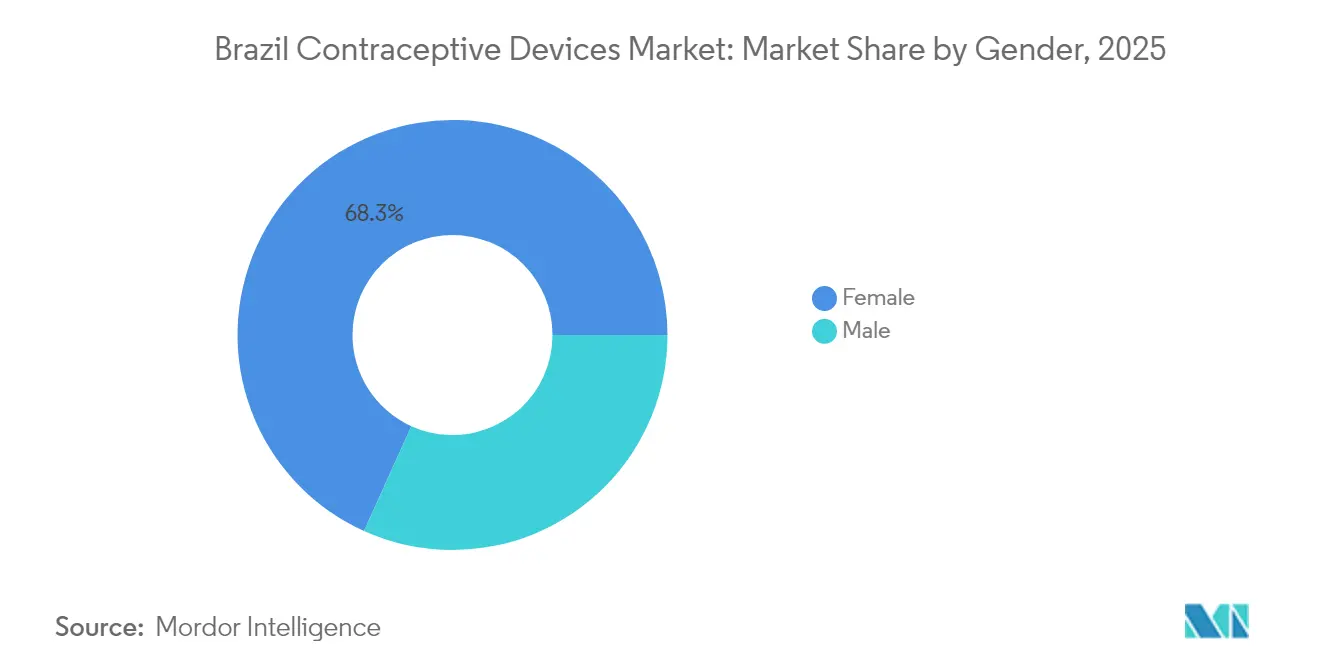

- By gender, female-oriented devices commanded 68.25% share of the Brazil contraceptive devices market size in 2025; male devices exhibit the highest projected CAGR at 7.89% through 2031.

- By material, latex held 78.62% share of the Brazil contraceptive devices market in 2025, and non-latex alternatives are growing at 8.05% CAGR.

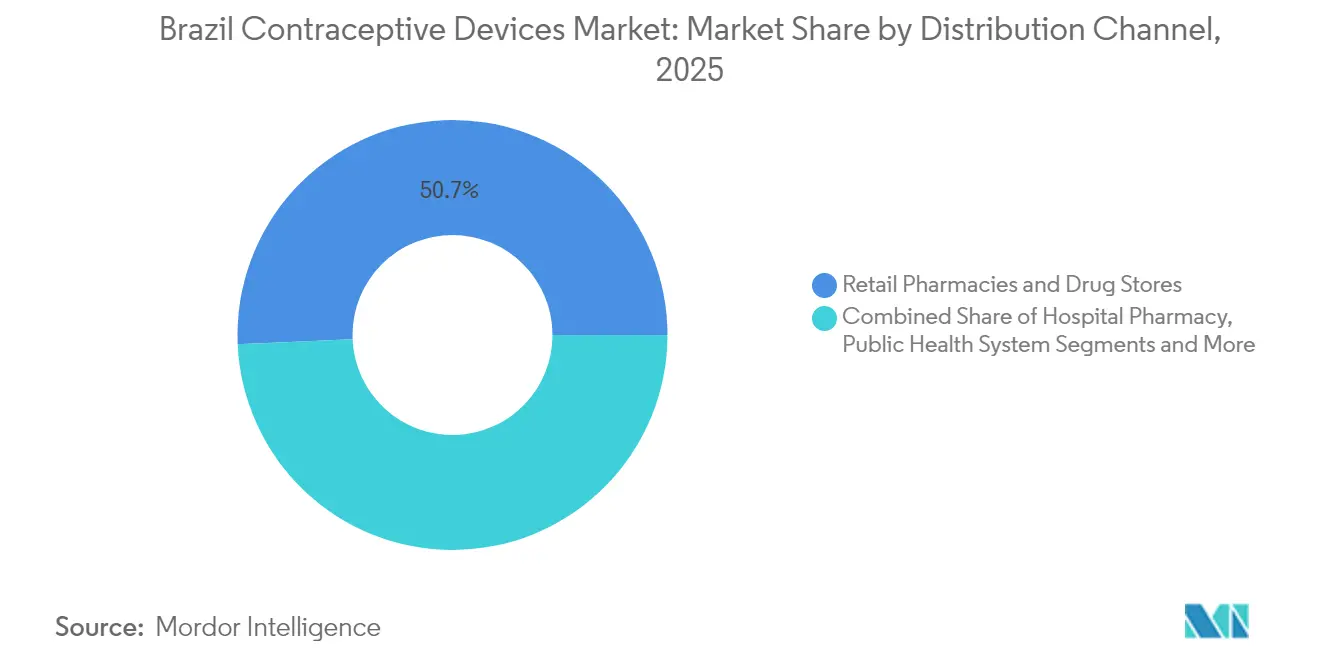

- By distribution channel, retail pharmacies accounted for 50.68% of the Brazil contraceptive devices market size in 2025, whereas e-commerce and direct sales record a 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Initiatives and Rising Awareness for Contraceptive Devices | +1.2% | National, with stronger impact in urban centers | Medium term (2-4 years) |

| Rising Burden of Sexually Transmitted Infections (STIs) | +0.8% | National, concentrated in high-risk demographics | Short term (≤ 2 years) |

| Growing Rate of Unplanned Adolescent Pregnancies | +0.9% | National, with emphasis on Northeast and North regions | Medium term (2-4 years) |

| ANVISA 2024-25 e-labelling & reprocessing rules easing market entry | +0.7% | National regulatory framework | Short term (≤ 2 years) |

| Rising Initiatives for Long-Acting Reversible Contraceptives (LARCs) | +1.1% | Urban centers with advanced healthcare infrastructure | Long term (≥ 4 years) |

| Technological Advancements and Emerging demand for eco-friendly/biodegradable barrier materials | +0.6% | Urban, environmentally conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government initiatives and rising awareness for contraceptive devices

Brazil’s Family Health Strategy now funds 2,360 new teams per year, creating routine touchpoints where nurses and physicians counsel users on a broader mix of methods. The Nova Indústria Brasil policy channels BRL 300 billion into domestic device production, lowering import reliance and shortening lead times.[1]Brazilian Government, “Brazil Launches New Industrial Policy with Development Goals and Measures up to 2033,” gov.br Community-health workers integrate contraception messaging into home visits, enhancing method literacy in underserved districts. A unified procurement model for primary-care units strengthens supply continuity, helping clinics maintain stock of implants, IUDs, and condoms simultaneously. As awareness improves, method switching rises, pushing demand for both short-acting and long-acting products.

Rising burden of sexually transmitted infections (STIs)

A recent multicenter study recorded 24% STI prevalence among pregnant women in major urban hospitals, intensifying public-health campaigns that spotlight condoms for dual protection[2]Angelica Espinosa Miranda et al., “Prevalence and Risk Behaviors for Chlamydial Infection in Female Adolescents in Brazil,” journals.lww.com. Youth-oriented initiatives such as UNFPA’s “Mais Direitos, Menos Zika” reinforce consistent barrier use, driving steady condom replenishment cycles. Clinicians increasingly recommend dual-method strategies, pairing hormonal devices with barrier products, which boosts cross-category sales. Online ordering enables discreet access for high-risk groups, and digital pharmacies bundle condoms with STI self-test kits, raising average transaction value. Manufacturers highlight antiviral lubricant coatings and thinner non-latex options to differentiate premium lines.

Growing rate of unplanned adolescent pregnancies

Although Brazil’s adolescent fertility rate continues to fall, unplanned pregnancy remains a concern in the North and Northeast. Health-post data show implants gaining traction where teenagers seek low-maintenance options after counseling sessions.[3]Ana Luiza Vilela Borges et al., “Individual and Context Correlates of Oral Pill and Condom Use among Brazilian Female Adolescents,” scielo.br Public campaigns emphasize educational attainment links to contraception, nudging municipalities to stock LARCs in school-linked clinics. Retail chains tailor promotions around graduation seasons, bundling pregnancy tests and emergency contraception. Social-media influencers partner with NGOs to normalize conversations about method choice, helping brands engage digitally native consumers. These aligned efforts lift implant and hormonal ring volumes while sustaining condom sales for dual protection.

ANVISA 2024-25 e-labelling and streamlined import rules

ANVISA now permits electronic instructions and extended import windows for devices manufactured up to five years prior to registration, slashing administrative delays. Foreign companies enter with niche products such as biodegradable diaphragms, enriching assortment diversity. Domestic players re-label existing SKUs faster, targeting e-commerce first because digital listings update instantly. Simplified reprocessing guidelines clarify sterilization for single-use items like cervical caps, encouraging broader catalogues. Together, these reforms underpin the 9.34% CAGR forecast for online and direct-to-consumer channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Side-effects & discomfort concerns with device/hormonal methods | -0.9% | National, particularly affecting LARC adoption | Medium term (2-4 years) |

| Cultural resistance & misinformation around LARCs | -1.1% | Rural and conservative regions, religious communities | Long term (≥ 4 years) |

| Copper price volatility disrupting IUD supply chain | -0.6% | Global supply chain affecting domestic availability | Short term (≤ 2 years) |

| Low reimbursement incentives for private OB-GYN counselling | -0.8% | Private healthcare sector, urban middle-class | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Side-effects and discomfort concerns with device/hormonal methods

Surveys in primary-care settings reveal that many women feel constrained by side-effect anxiety, citing cramps, bleeding changes, or weight gain as key discouragers. Insertion of copper IUDs remains uneven because some clinics still impose unnecessary eligibility criteria. Device withdrawal rates highlight counseling gaps, where expectations for initial adjustment go unaddressed. Pharmaceutical firms respond with patient-friendly leaflets and 24-hour chatbots that clarify typical adaptation timelines. Training initiatives for nurses now incorporate updated pain-management protocols and shared decision-making techniques to rebuild confidence in LARC safety.

Cultural resistance and misinformation around LARCs

Deep-rooted religious beliefs in parts of the Northeast and rural interior frame long-acting contraception as incompatible with family norms. Community leaders sometimes propagate misconceptions about fertility loss or invasive removal. Such narratives circulate quickly on social media, overshadowing clinical evidence. NGOs collaborate with local faith-based groups to create culturally aligned education modules that explain reversibility. Male partner engagement sessions aim to shift decision-making from unilateral to shared, reducing covert discontinuation. Despite gradual progress, entrenched attitudes continue to temper uptake, especially among low-literacy households

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Condoms Sustain Scale While Implants Accelerate

Condoms contributed 43.02% to the Brazil contraceptive devices market in 2025, supported by broad retail coverage and dual-protection messaging. Subdermal implants, while accounting for a smaller base, are on track for a 7.12% CAGR through 2031 as public clinics scale LARC programs. The Brazil contraceptive devices market size for implants is projected to grow steadily as domestic factories, financed under Nova Indústria Brasil, ramp up output. Condom vendors emphasize non-latex SKUs and antiviral lubricants to command premium shelf placement, whereas implant producers invest in provider training to boost insertion competencies across family-health teams.

Supply-chain volatility for copper complicates IUD production, yet localized assembly mitigates part of the pricing pressure. Vaginal rings gain niche appeal among health-conscious urban women seeking routine-free hormonal delivery. Diaphragms, cervical caps, and sponges remain niche because they require fitting or carry lower efficacy perceptions. Emerging “other devices,” including stimuli-responsive hydrogels, signal future avenues for reversible male and female contraception, though commercial impact lies beyond the current forecast horizon.

By Gender: Female Dominance Meets Rising Male Engagement

Female-focused products held 68.25% share in 2025, but male devices are positioned for an 7.89% CAGR as societal attitudes evolve toward shared responsibility. A push for dual-method use means condom demand coexists with hormonal and LARC adoption, rather than replacing it. Promotional campaigns now feature couple-based narratives, encouraging joint decision-making at clinic visits. Retailers report that multipacks sized for month-long use appeal to budget-sensitive male buyers; meanwhile, telehealth platforms experiment with mail-order vasectomy consultations, expanding the Brazil contraceptive devices industry reach.

Female device growth stems from expanding implant and IUD programs financed by state and municipal authorities. Manufacturers embed QR codes on packaging that link users to removal service locators, reducing anxiety around reversibility. As more men participate in contraceptive conversations, brands offering discreet male options, such as soon-to-launch reversible gels, stand to diversify revenue streams in the Brazil contraceptive devices market.

By Material: Latex Dominates but Non-Latex Options Grow

Latex still delivers 78.62% of unit sales in 2025 because of favorable cost and manufacturing scale. Nonetheless non-latex alternatives advance at 8.05% CAGR, responding to allergy concerns and eco-impact scrutiny. The Brazil contraceptive devices market share for non-latex condoms remains low in unit terms, yet revenue contribution rises because of premium pricing. Polyurethane and polyisoprene brands highlight enhanced heat transfer and oil-based lubricant compatibility, positioning them for consumers valuing comfort and environmental claims.

Domestic producers invest in biodegradable wrappers and plant-based rubber sourcing to align with corporate ESG goals. Research into zinc-based IUDs seeks to offset copper price shocks while maintaining efficacy. Start-ups explore natural fiber diaphragms treated with antimicrobial coatings, aiming for environmental differentiation. As hospital procurement criteria evolve to include sustainability metrics, suppliers offering green credentials may secure priority in public tenders, reinforcing the shift within the Brazil contraceptive devices market size dynamics.

By Distribution Channel: Digital Platforms Disrupt Traditional Models

Retail pharmacies maintained 50.68% share in 2025 through professional guidance and widespread presence. Yet e-commerce and direct sales are accelerating at 8.92% CAGR, fueled by privacy, price comparison, and ANVISA’s e-labelling reforms. The Brazil contraceptive devices market size for online channels is projected to climb steadily as consumers increasingly opt for home delivery subscriptions timed with menstrual cycles or prescription refills. Influencer-curated bundles and same-day logistics enhance convenience, edging share away from brick-and-mortar formats.

Public health facilities concentrate on implants and IUDs that rely on clinician insertion, while retail chains dominate short-acting methods. Hospital pharmacies manage higher-cost hormonal rings and emergency contraception. NGOs distribute condoms and fertility awareness tools in remote communities, often using mobile clinics. Cross-channel strategies emerge: pharmacy chains launch online storefronts and integrate electronic prescriptions, and digital-first brands open pop-up kiosks during festivals to boost visibility and trust. This omnichannel interplay underpins consumer choice diversity within the Brazil contraceptive devices market.

Geography Analysis

Brazil’s contraceptive landscape displays marked regional contrasts. The Southeast, led by São Paulo, benefits from mature healthcare infrastructure, capturing a sizable portion of implant and IUD demand. Public hospitals there report stock-out rates below 5%, supporting uninterrupted LARC programs. Higher household incomes translate into above-average uptake of non-latex condoms and hormonal rings, reinforcing premium market tiers within the Brazil contraceptive devices market.

In the North and Northeast, primary-care units record lower IUD availability and elevated adolescent pregnancy indicators. The Ministry of Health channels Family Health Strategy funding toward these zones, prioritizing provider training and device supply. NGO partnerships deploy mobile health units that leverage QR-based ordering to bypass logistical hurdles, fostering incremental increases in implant use. E-commerce adoption lags urban centers yet gains traction via smartphone penetration and cashless payment expansion.

The South registers the highest STI screening coverage, propelling consistent condom distribution. Local authorities integrate digital awareness campaigns during regional festivals, pairing QR codes with free condom samples. The Central-West combines agricultural prosperity with patchy clinic density, prompting a hybrid model where private telemedicine platforms coordinate prescription delivery. Across all regions, inflationary pressures influence brand choice, with consumers shifting between premium and value segments depending on real wage dynamics. Regional tailoring of product mix, pricing, and promotional channels is therefore essential to capture the full potential of the Brazil contraceptive devices market.

Regulatory Landscape

Brazil regulates contraceptive devices as medical devices under ANVISA, with risk-based classification anchored in RDC No. 751/2022. Many contraceptive products fall into higher-risk categories, commonly Class III, and Class IV for long-term implantable or invasive devices. This typically translates into more extensive technical dossier expectations, GMP evidence, and formal marketing authorization before commercialization.

Recent policy signals also feed into landed cost and portfolio strategy. In November 2025, GECEX Resolution No. 818 reduced the import tariff for female condoms made of nitrile rubber and natural materials, while December 2025 GECEX Resolution No. 821 raised the import tariff for a set of medical devices under NCM 9018.90.99. Together, these measures reinforce that access and pricing can shift in parallel with ANVISA compliance requirements.

Value Chain Analysis

Brazil’s contraceptive devices value chain begins with global and domestic sourcing of key inputs, including latex and non-latex polymers for condoms, and metals and polymers for IUDs and implant systems. Products are then manufactured locally or imported through an in-country legal representative, with ANVISA-compliant quality systems. For higher-risk devices aligned with RDC 751/2022 classifications, quality and documentation steps, including GMP certification or protocol and technical dossier maintenance, act as central gating items that affect time-to-market and batch availability.

Commercialization and access are shaped by two main routes, public-sector procurement and private retail. The Ministry of Health and the Unified Health System (SUS) anchor volume via centralized inclusion and distribution programs, while retail pharmacies and e-commerce drive consumer-paid demand and brand competition. A concrete public-channel inflection is the Ministry of Health pathway for etonogestrel implants, where Portaria SECTICS/MS No. 47 (July 2025) expanded inclusion within SUS for women aged 18 to 49. A February 2026 technical note further operationalized distribution at scale with 1.3 million etonogestrel 68 mg implants sent to state and municipal health secretariats, highlighting how government purchasing, logistics, and provider capability influence downstream uptake.

Competitive Landscape

Competition remains moderate, with a cluster of multinationals and agile domestic firms shaping the Brazil contraceptive devices market. Bayer leads the implant category through its Mirena franchise and leverages in-country manufacturing upgrades to comply with Nova Indústria Brasil localization targets. Q2 2024 results note implant revenue gains attributed to higher unit volumes and selective pricing. Ansell and LifeStyles Healthcare dominate condoms, pushing thin non-latex variants and antiviral coatings that cater to STI concerns.

Local specialist Hypera Pharma scales production of latex condoms and injectables, benefitting from BRL-denominated cost bases that hedge currency volatility. DKT International collaborates with community health programs to expand social-marketing reach, offering subsidized pricing in low-income municipalities. Start-ups experiment with biodegradable materials and male contraceptive prototypes, banking on ANVISA’s streamlined pathways to accelerate approval. Intellectual-property barriers remain modest, so differentiation hinges on brand equity, clinician trust, and omnichannel distribution strength.

Strategic moves in 2024-2025 emphasize vertical integration and digital engagement. Multinationals forge supply agreements with leading e-commerce marketplaces to guarantee next-day delivery, while domestic firms pilot WhatsApp-based refill reminders. Several providers invest in carbon-neutral packaging plants, aligning with procurement criteria that now weigh ESG metrics. Joint ventures between material-science companies and contraceptive brands explore plant-based rubber sources, signaling future competitive levers within the Brazil contraceptive devices industry.

Brazil Contraceptive Devices Industry Leaders

Bayer AG

Reckitt Benckiser Group plc

Ansell Ltd

Hypera Pharma S.A.

CooperSurgical Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is the expansion of long-acting reversible contraception inside primary care, where device availability is linked to training and centralized distribution rather than specialist-only pathways. SUS actions on subdermal implants show this dynamic in practice. After Portaria SECTICS/MS No. 47 (July 2025) formalized expanded access for women aged 18 to 49, the Ministry of Health moved to larger-scale distribution, including 1.3 million etonogestrel 68 mg implants referenced in a February 2026 technical note, alongside provider qualification programs. Suppliers can target this channel by supporting insertion training, post-insertion follow-up tools, and dependable supply to state and municipal health secretariats.

A second opportunity comes from a mix shift supported by regulatory and channel modernization. ANVISA’s framework under RDC 751/2022, combined with more digital-ready labeling and documentation practices referenced in the report context, supports faster portfolio refresh and online channel execution for barrier methods and select devices. At the same time, tariff adjustments in late 2025, GECEX Resolutions No. 818 and No. 821, underline the commercial value of local sourcing, localization, and resilient import planning. Brands that pair compliant labeling with privacy-forward e-commerce distribution can meet demand for non-latex and differentiated condom offerings, while clinic-driven growth in implants and IUDs continues to anchor higher-need segments.

Recent Industry Developments

- July 2026: Apollo Global acquired a minority stake in Bayer’s long-acting reversible contraceptive business for EUR 3 billion. The transaction reshaped ownership and capital allocation around a major LARC portfolio, with implications for investment pace and partnering strategy in core markets such as Brazil.

- March 2025: Bayer signed a partnership agreement with Megalabs for the commercialization and distribution of its contraceptive and cardiology product lines in Brazil. The agreement expanded local go-to-market reach through an established regional partner, supporting broader access and continuity of supply for branded contraceptive offerings.

- June 2024: Brazil’s Ministry of Health initiated a national Carnival campaign promoting condom use under the slogan “Carnival, respect and protection #MustHave”. The campaign reinforced barrier-method demand through high-visibility public health messaging tied to STI prevention and seasonal consumption peaks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Brazil contraceptive devices market is defined as the value of devices used to prevent pregnancy that are sold through public and private channels in Brazil, including retail, hospital supply, and approved online sales.

Scope exclusions: We exclude contraceptive drugs, emergency contraception pills, and fertility-tracking apps because they follow different prescribing, pricing, and usage patterns.

Segmentation Overview

- By Type

- Condoms

- Diaphragms and Cervical Caps

- Vaginal Sponges

- Vaginal Rings

- Intra-Uterine Devices (IUD)

- Subdermal Implants

- Spermicidal Devices

- Other Devices

- By Gender

- Male

- Female

- By Material

- Latex

- Non-latex

- By Distribution Channel

- Public Health System

- Hospital Pharmacies

- Retail Pharmacies & Drugstores

- E-commerce & Direct Sales

- Family-planning Clinics & NGO Programs

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public health and regulatory signals that describe what products are allowed and how they move in the system. Sources such as ANVISA product and registration information, Brazil Ministry of Health publications, and DATASUS indicators were used to frame access, care settings, and how contraception programs are structured.

To anchor demand-side context, we also referred to sources such as IBGE population and women of reproductive age statistics, UNFPA and WHO contraceptive prevalence references, and selected peer-reviewed articles on method mix and continuation. These were then complemented with company filings, investor presentations, association websites, and reputed press, plus limited use of paid subscriptions for company financials and intelligence, news and financials, and patent databases when clarifying product pipelines. The sources listed here are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what actually sells in Brazil, how pricing behaves across channels, and where adoption is shifting between short-acting and longer-acting methods. We spoke with a mix of manufacturers, distributors, pharmacy and hospital procurement stakeholders, clinicians, and public health-focused experts across Brazil to close gaps from desk findings and then confirm the final assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 32% | |

| Smaller Players: 14% | Managers: 55% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where contraceptive demand was reconstructed from population and women-of-reproductive-age counts, method mix, and estimated device replacement or usage cycles, and then converted into value using channel-aware pricing. Once the demand pool was shaped, we ran selective bottom-up checks using supplier and importer revenue cues, distributor channel checks, and sampled average selling price times volume for high-usage device groups. When those checks did not align with the top-down view, totals were adjusted accordingly.

Key model inputs included ANVISA product availability and registration timing, contraceptive prevalence and method mix signals, public versus private channel split, typical device replacement frequency (for example, for condoms versus longer-duration devices), and observed pricing bands by channel and brand tier. Where direct volume indicators were thin for a device category, we used a conservative penetration proxy informed by clinician feedback and kept price assumptions within observed pharmacy and tender ranges.

For forecasting, scenario analysis was used and guided by expert views on access expansion, channel shifts toward e-commerce, and expected pricing progression under inflation and currency movement. The final forecast stayed consistent with how quickly new products can be adopted in practice, based on what providers and distributors described as feasible over the next few years.

Data Validation & Update Cycle

Each major assumption was checked using more than one angle before it was accepted, including cross-checking against independent health indicators, pricing references, and channel feedback. Variance checks were run at device group level and at the total market level, and any outliers were reviewed again by an analyst who was not the original model builder, before sign-off.

The report is refreshed annually, and interim reviews are triggered when material events occur, such as major policy shifts, meaningful pricing changes, or new device approvals that can move volumes. Before delivery, a final pass is completed so the client receives the most current view based on the latest accessible data and any newly completed expert reconfirmations.

Mordor Intelligence's Brazil Contraceptive Devices Market Sizing Compared With Other Published Estimates

Published market sizes for contraceptive devices in Brazil can look far apart because each publisher draws the line in a different place and does not always use the same pricing, channel, or base year logic. Differences also show up when one estimate leans heavily on high-growth assumptions without matching them to real-world access constraints.

ANVISA-cleared device lists, contraceptive prevalence signals, and channel-level price checks are the evidence points that keep Mordor Intelligence's estimate tied to devices that are actually sold and replenished in Brazil, rather than being blended with drugs or adjacent wellness categories. The main gap drivers we saw across other numbers were scope mixing (devices plus drugs), aggressive price progression that is not aligned to observed pharmacy and tender bands, and base year differences that are later inflated forward without enough validation steps.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 512.64 M (2025) | |

| Industry Publisher A | USD 352.89 M (2025) | This estimate appears to apply a narrower realized revenue capture for devices, with a simpler treatment of channel coverage and price bands, which can undercount private-channel volumes for higher-value long-acting devices. |

| Research Publisher B | USD 1.30 B (2024) | This figure is likely influenced by a broader definition and faster growth assumptions, and it may also be sensitive to base-year selection and price escalation steps that are not clearly tied back to observable channel pricing and product scope boundaries. |

The spread in the table is mainly explained by what gets counted as a device sale in Brazil and how pricing and channels are converted into a single USD value for the year. By keeping the scope limited to contraceptive devices, using channel-aware prices, and validating key assumptions with real-world supply and care-setting feedback, the resulting number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Brazil contraceptive devices market?

The market stands at USD 544.01 million in 2026 and is projected to hit USD 732.11 million by 2031.

Which type holds the largest Brazil contraceptive devices market share?

Condoms lead with 43.02% share in 2025, driven by dual-protection messaging.

What segment is growing fastest within the market?

Subdermal implants post the highest CAGR at 7.12% through 2031, reflecting government support for LARCs.

How are digital channels influencing sales?

E-commerce and direct sales grow at 8.92% CAGR, supported by ANVISA e-labelling rules that simplify online dispensing.

Which material segment is gaining momentum?

Non-latex options register an 8.05% CAGR as consumers seek hypoallergenic and eco-friendly alternatives.

What is the main regulatory development shaping market entry?

ANVISA’s 2024-25 reforms permit electronic labelling and extended import timelines, cutting approval delays for new devices.

Page last updated on: