Intracranial Stents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

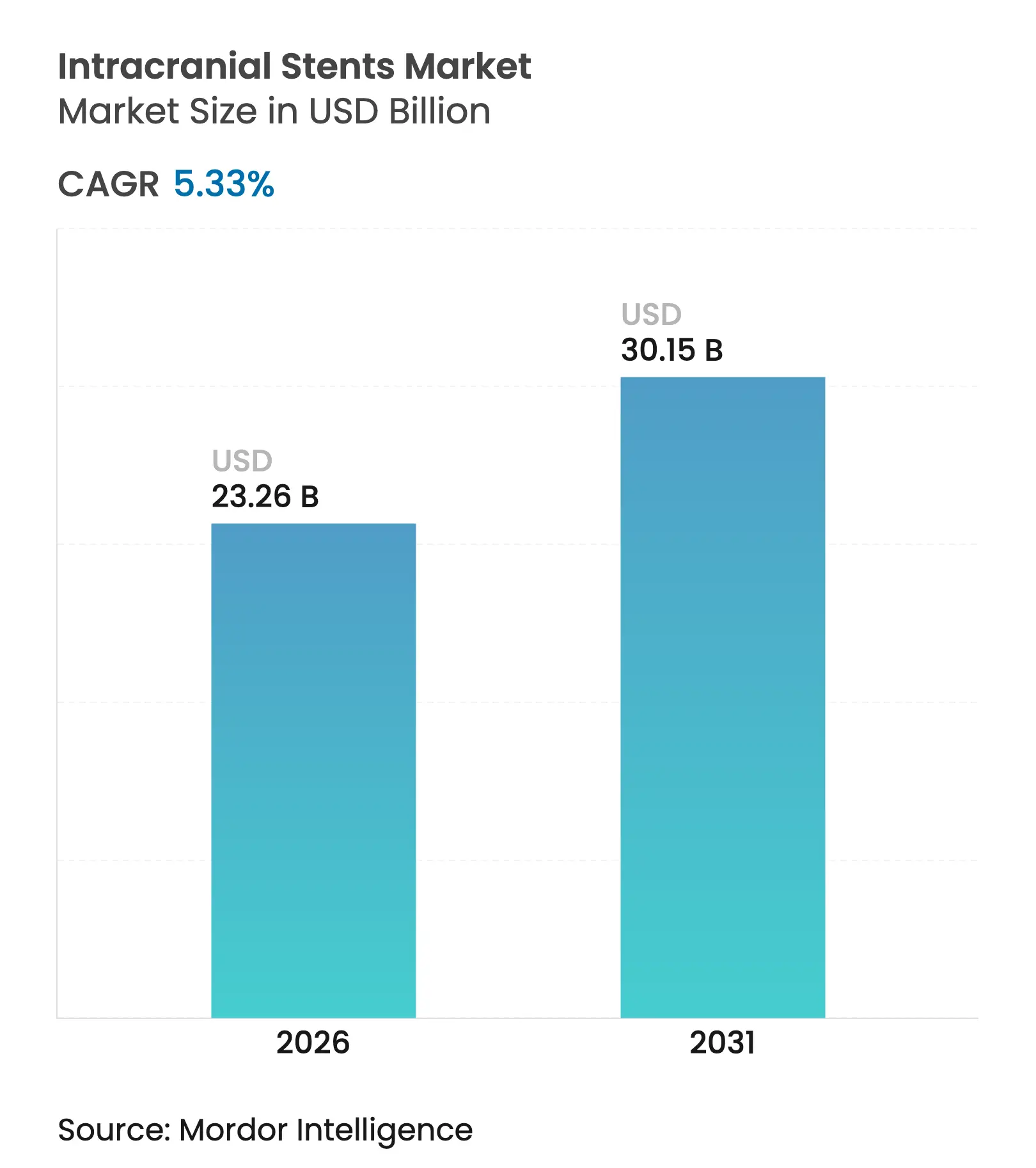

| Market Size (2026) | USD 23.26 Billion |

| Market Size (2031) | USD 30.15 Billion |

| Growth Rate (2026 - 2031) | 5.33 % CAGR |

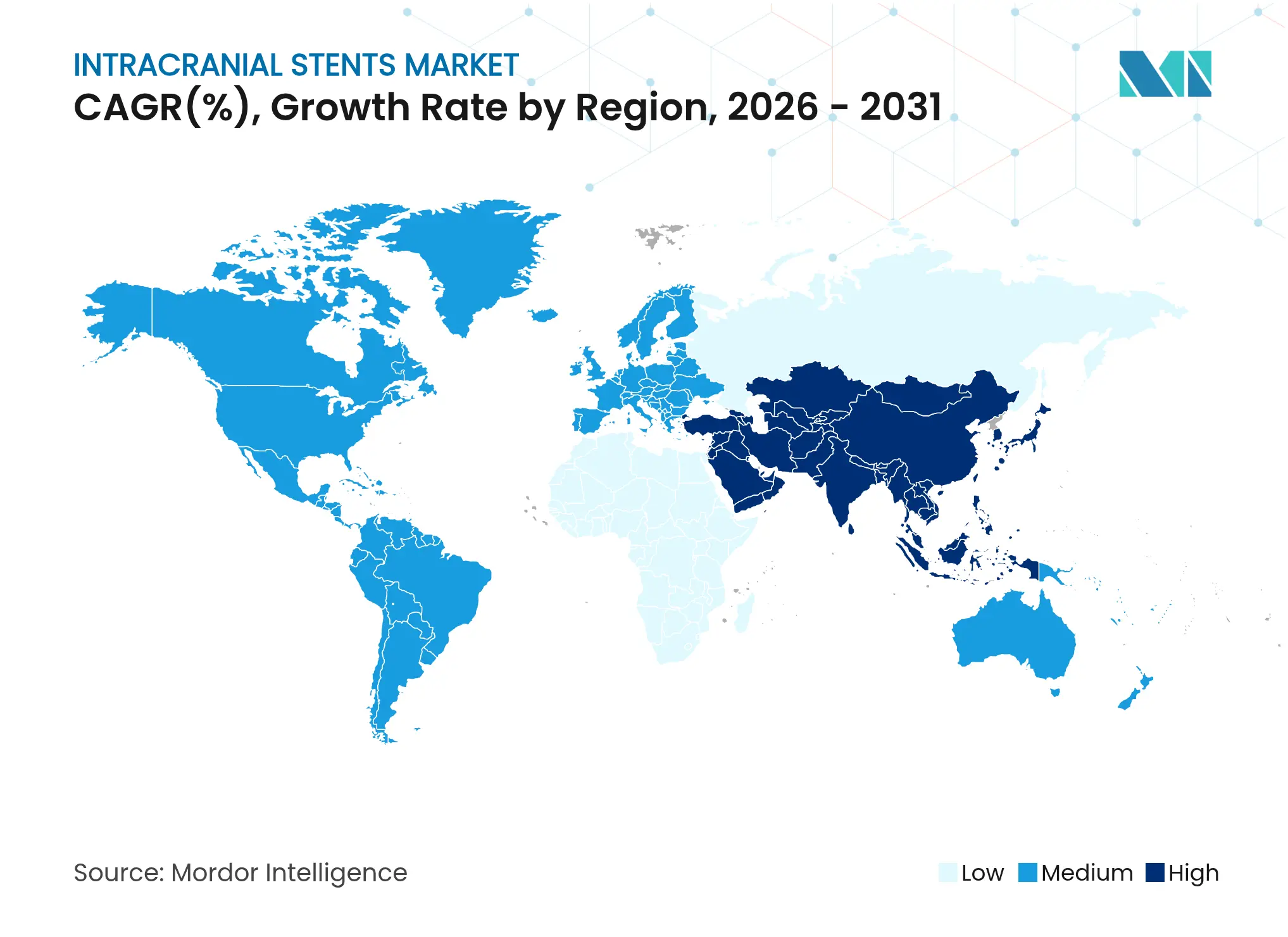

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Intracranial Stents Market Analysis by Mordor Intelligence

The intracranial stents market size is expected to grow from USD 22.08 billion in 2025 to USD 23.26 billion in 2026 and is forecast to reach USD 30.15 billion by 2031 at 5.33% CAGR over 2026-2031. Uptake is propelled by an aging population, steady gains in flow-diversion technology, and wider reimbursement that collectively expand candidacy for minimally invasive neurovascular care.[1]Melika Amoukhteh, “Flow Diverters in the Treatment of Intracranial Dissecting Aneurysms,” Journal of NeuroInterventional Surgery, jnis.bmj.comFlow-diverter breakthroughs now let physicians treat aneurysms once deemed inoperable while shortening procedural steps, a change that is reshaping everyday practice. Artificial-intelligence guidance, growing self-expanding stent familiarity, and coating innovations further raise success rates and lower complication profiles. At the same time, stroke-center accreditations and outpatient migration are leaning the market toward capacity-optimized, technology-enabled growth, especially in Asia-Pacific where infrastructure projects are accelerating.

Key Report Takeaways

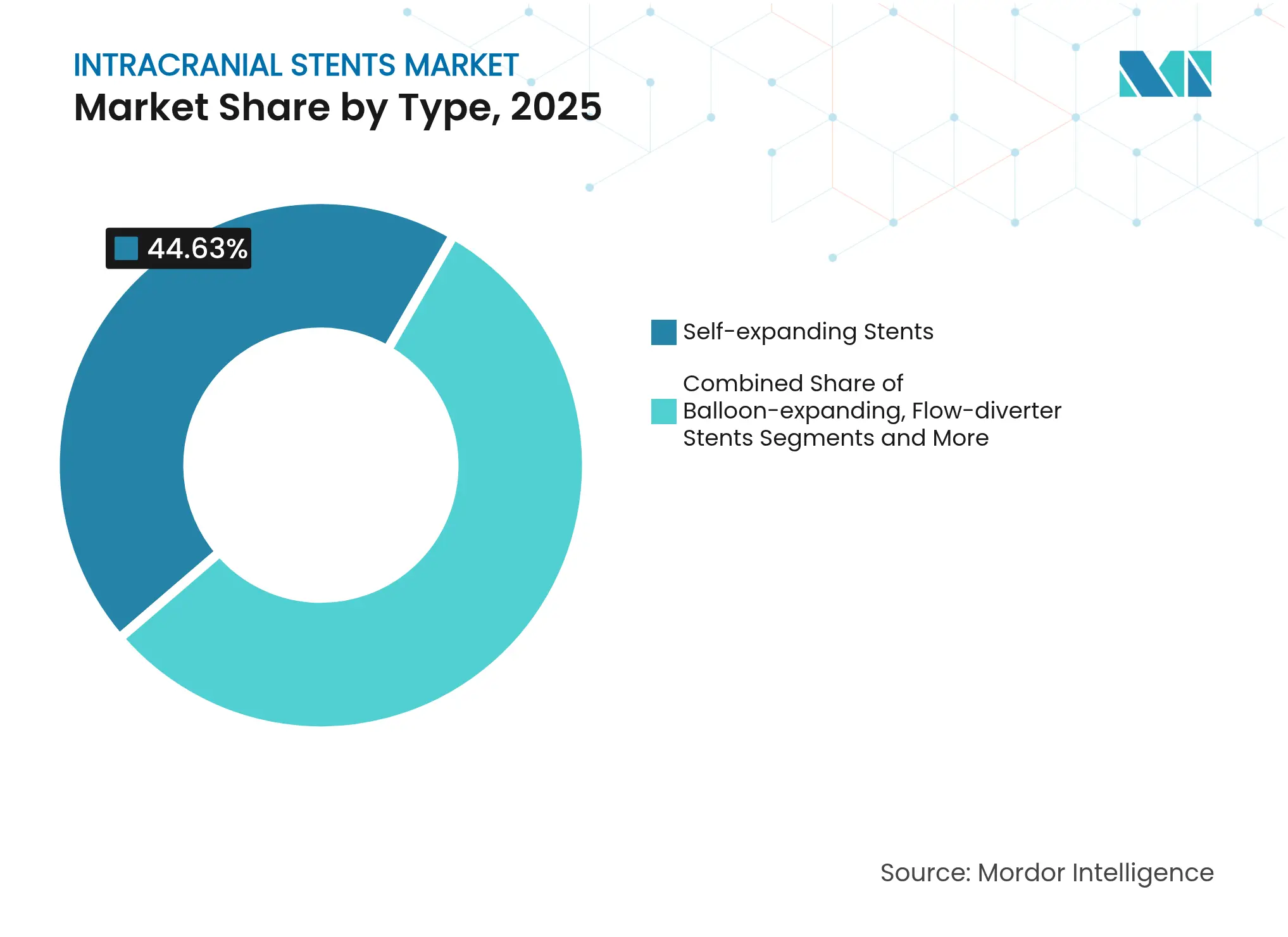

- By product type, self-expanding devices led with 44.63% of the intracranial stents market share in 2025, while flow-diverter systems are projected to climb at 8.85% CAGR to 2031.

- By material, nitinol commanded 58.64% share of the intracranial stents market size in 2025; bioresorbable and advanced polymers are pacing at 8.21% CAGR through 2031.

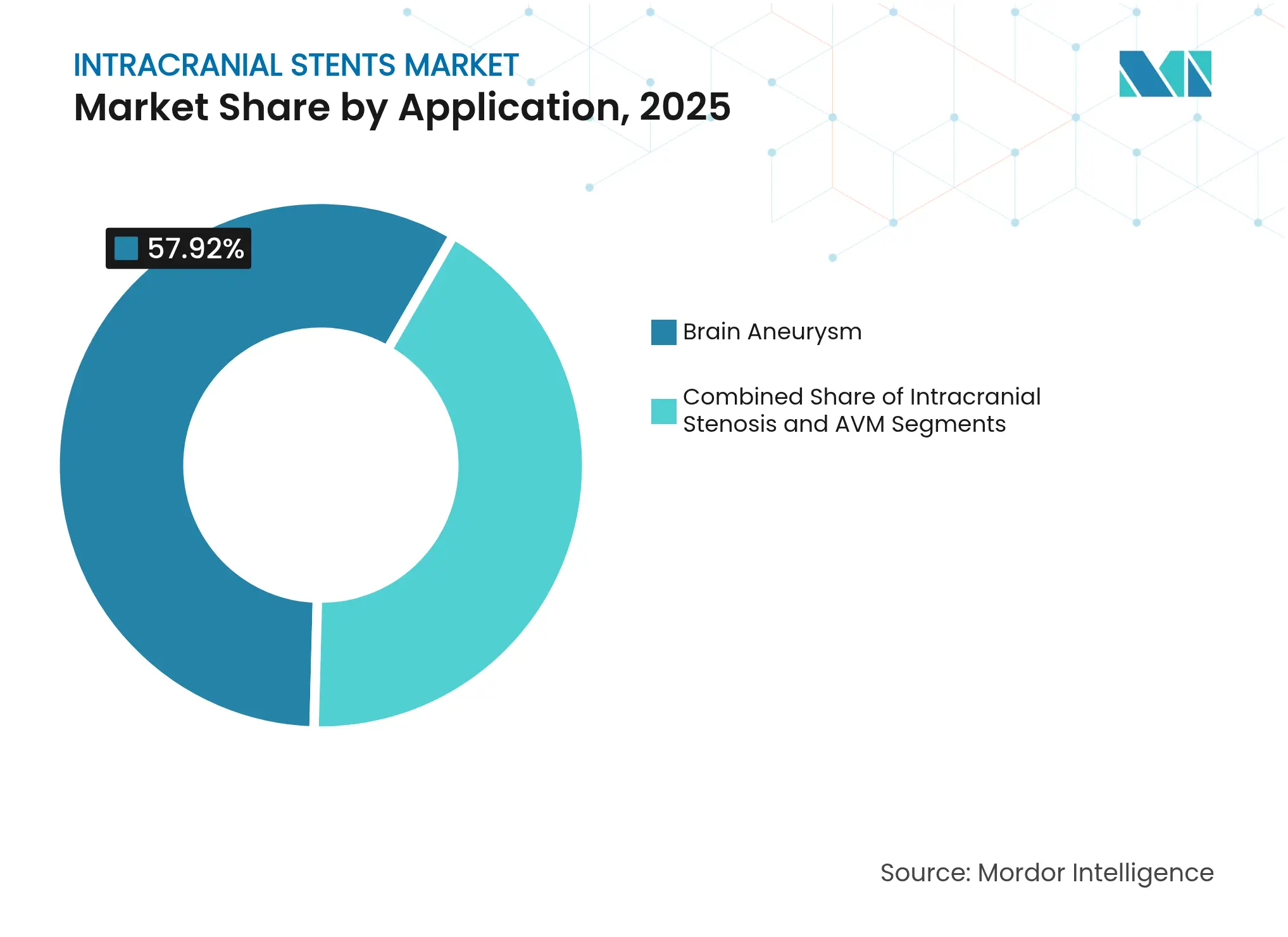

- By application, brain aneurysm treatment accounted for 57.92% of the intracranial stents market size in 2025 and is progressing at a 6.62% CAGR. Arterio-venous malformations are the fastest-growing application at 7.44% CAGR.

- By end-user, hospitals held 64.12% revenue share in 2025, while ambulatory surgery centers exhibit the highest projected CAGR at 7.1% through 2031.

- By geography, North America controlled 35.88% revenue in 2025, yet Asia-Pacific is the fastest-growing region at 7.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intracranial Stents Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing demand for minimally

invasive intracranial procedures

Increasing demand for minimally

invasive intracranial procedures

| +1.2% | Global; early uptake in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

Global; early uptake in North

America and Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing prevalence of

cerebrovascular disorder and aging demographics

Growing prevalence of

cerebrovascular disorder and aging demographics

| +0.9% | Global; pronounced in Asia-Pacific and North America | Long term (≥ 4 years) | |||

Improving healthcare infrastructure

and expanding reimbursement coverage

Improving healthcare infrastructure

and expanding reimbursement coverage

| +0.8% | Asia-Pacific core; spill-over to MEA and Latin America | Medium term (2-4 years) | |||

Technological advancement and

product innovation

Technological advancement and

product innovation

| +1.1% | Global; R&D focus in North America and Europe | Short term (≤ 2 years) | |||

Growing awareness and early

diagnosis of neurovascular disorders

Growing awareness and early

diagnosis of neurovascular disorders

| +0.6% | Global; faster in emerging markets | Long term (≥ 4 years) | |||

AI-guided neuro-interventional

planning improving treatment candidacy

AI-guided neuro-interventional

planning improving treatment candidacy

| +0.7% | North America and EU; expanding to Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Demand for Minimally Invasive Intracranial Procedures

Radial-access approaches now dominate current training modules because they lower vascular complication rates and trim recovery times without undermining procedural safety. Flow-diverting stents exemplify this change by replacing multi-stage coil embolization with single-device deployment, reducing catheter time and radiation exposure. Certification of thrombectomy-capable stroke centers in the United States is cementing standardized use, and the same-day-discharge model inside ambulatory surgery centers aligns perfectly with value-based payment initiatives.

Growing Prevalence of Cerebrovascular Disorder & Aging Demographics

Population aging raises the baseline incidence of aneurysms and intracranial stenosis, expanding the global candidate pool for stenting frontiersin.org. AI-imaging tools now detect silent aneurysms earlier, while five-year occlusion rates of 96% for flow-diverters confirm durable performance and reinforce broader guidelines jnis.bmj.com. In China, 25,438 patients were enrolled for unruptured aneurysm care, with 73.6% managed endovascularly, illustrating huge latent demand.[2]Kaige Zheng, “China Treatment Trial for Unruptured Intracranial Aneurysm,” Chinese Neurosurgical Journal, springeropen.com

Improving Healthcare Infrastructure and Expanding Reimbursement Coverage

Stroke-center build-outs in India, China, and Indonesia add cath-lab capacity, while fellowship programs in the United States and Europe continue to graduate specialists, narrowing historical gaps vumc.org. Payors in Japan and South Korea have broadened reimbursement for carotid and intracranial stenting, directly lowering out-of-pocket costs and encouraging earlier intervention. AI-assisted case-planning platforms shorten learning curves, letting mid-volume centers deliver outcomes comparable to flagship institutions.

Technological Advancement and Product Innovation

Hydrophilic polymer coatings cut thromboembolic event rates to 4.7%, boosting physician confidence in flow-diverter safety jnis.bmj.com. Bioresorbable designs aim to deliver acute scaffolding but disappear once healing is complete, which could eliminate chronic inflammatory risks tied to permanent metal. Fourth-generation devices such as Pipeline Vantage hit 100% deployment success and 81.7% occlusion at six months, underscoring iterative gains in deliverability and wall apposition.[3]Hal Rice, “Vanguard Study: Pipeline Vantage Flow Diverter 6-Month Results,” Journal of NeuroInterventional Surgery, jnis.bmj.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Scarcity of highly-skilled

neuro-interventionalists

Scarcity of highly-skilled

neuro-interventionalists

| -0.8% | Global; most acute in emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-0.8%

|

Geographic Relevance

:

Global; most acute in emerging

markets

|

Impact Timeline

:

Long term (≥ 4 years)

|

Post-procedural in-stent restenosis

& thrombosis risk

Post-procedural in-stent restenosis

& thrombosis risk

| -0.5% | Global; higher in complex cases | Medium term (2-4 years) | |||

Cost-containment pressures in

emerging public health systems

Cost-containment pressures in

emerging public health systems

| -0.6% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) | |||

Limited long-term clinical evidence

for next-gen bio-resorbable designs

Limited long-term clinical evidence

for next-gen bio-resorbable designs

| -0.4% | Global; premium segment | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Scarcity of Highly-Skilled Neuro-Interventionalists

Training demands of 250 cumulative cases, including 25 stent placements, slow workforce expansion and leave many secondary hospitals understaffed. High-volume hubs such as Penn Medicine handle over 2,000 interventions annually, but talent remains clustered in urban centers, leading to access disparities for rural or frontier markets. AI guidance may ease skill gaps, yet large randomized trials and regulatory review are still pending.

Post-Procedural In-Stent Restenosis & Thrombosis Risk

In-stent stenosis appears in 53.6% of pipeline cases, especially among younger patients and longer procedures. Drug-eluting platforms and cutting-balloon angioplasty reduce restenosis rates, but add device cost and procedural time that may strain reimbursements. Consistent dual-antiplatelet therapy adherence is also a challenge in resource-constrained settings, raising readmission risks.

Segment Analysis

By Type: Flow-Diverters Drive Innovation Leadership

The intracranial stents market size for flow-diverters is projected to expand at 8.85% CAGR between 2026-2031, reflecting strong physician preference for single-device aneurysm occlusion and reduced retreatment burden. Self-expanding devices nevertheless control 44.63% 2025 volume thanks to their broad indication list and operator familiarity.

Fourth-generation flow-diverters such as Pipeline Vantage now achieve 81.7% six-month occlusion, while hydrophilic coatings have lowered thromboembolic complications to 4.7%, narrowing the safety gap with coils. Balloon-expandable models retain niche roles in tortuous pediatric cases where exact placement is critical, and stent-assisted coils continue to bridge practice for operators transitioning toward full flow diversion.

Note: Segment shares of all individual segments available upon report purchase

By Material: Bioresorbable Polymers Challenge Permanent Implants

Nitinol-based devices accounted for 58.64% of the intracranial stents market share in 2025, benefiting from shape-memory reliability and long clinical track records. Yet polymer and bioresorbable alternatives are growing at 8.21% CAGR as surgeons aim to avoid lifelong metal in young or low-risk patients.

Iron-based resorbables are undergoing corrosion-rate optimization, while polydioxanone scaffolds from cardiovascular trials provide proof of two-month support before safe dissolution. Cobalt-chromium remains favored for visualization in complex reconstructions. This material shift adds new procurement questions for providers weighing up-front cost versus lifetime risk mitigation.

By Application: Arterio-Venous Malformations Emerge as Growth Frontier

Brain-aneurysm cases represent the bulk of current revenue at 57.92% in 2025, supported by 96% five-year occlusion with modern flow-diverters. However, arteriovenous-malformation therapy is advancing at 7.44% CAGR, fueled by liquid embolic agents that fully lose radiopacity within 12 months, improving follow-up imaging.

Intracranial stenosis procedures now leverage drug-eluting stents, cutting one-year restenosis by 23% versus bare-metal, a gain that boosts payer acceptance for early intervention. Expansion of indications into dissecting aneurysms where functional success exceeds 89% underscores ongoing diversification.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Ambulatory Centers Capitalize on Procedural Efficiency

Hospitals still dominate revenue due to high-acuity stroke programs, yet ambulatory centers are growing at 7.1% CAGR as radial access enables same-day discharge that aligns with payer bundling . The intracranial stents market size for outpatient sites is projected to roughly double by 2031, supported by AI overlays that give less experienced interventionists immediate feedback.

Neurology clinics act as referral nodes, triaging cases through tele-consult to optimize cath-lab scheduling and follow-up imaging, thereby maintaining continuum-of-care quality with lower capital requirements than tertiary hospitals.

Geography Analysis

North America led the intracranial stents market in 2025 with 35.88% revenue, anchored by comprehensive stroke-center networks, favorable reimbursement, and a robust fellowship pipeline that supplies skilled operators. Device manufacturers often pilot next-generation coatings and AI software in United States or Canadian centers before global roll-out, accelerating domestic adoption cycles.

Europe maintains steady growth through regulatory harmonization and cross-border clinical trials such as the COATING study, which evaluates polymer-coated flow-diverters across multiple countries. National health systems in Germany, France, and the Nordic region have also upgraded stroke guidelines to include flow-diversion for complex aneurysms, securing reimbursement faster than past device classes.

Asia-Pacific is the fastest-growing region at 7.72% CAGR, propelled by public investment in stroke centers and a large untreated aneurysm population. The China Treatment Trial for Unruptured Intracranial Aneurysm highlights demand scale, enrolling over 25,000 patients with an endovascular treatment rate above 70%. India and Indonesia follow with capacity pledges for new neuro-cath labs, while Japan and South Korea serve as early adopters of polymer-coated stents due to national reimbursement clarity.

The Middle East and Africa are at an earlier adoption curve but benefit from medical-city initiatives in Saudi Arabia and United Arab Emirates that import high-end imaging suites and training partnerships. South America shows dual-speed dynamics: Brazil and Colombia grow quickly under private-payer segments, while smaller economies lag amid budget constraints.

Competitive Landscape

Market Concentration

The intracranial stents market remains moderately consolidated, with a handful of global med-tech firms leveraging acquisitions and distribution alliances to widen portfolios. Medtronic’s exclusive deal with Contego Medical for the 3-in-1 Neuroguard IEP platform integrates stent, balloon, and embolic protection, illustrating a trend toward multi-function devices. Boston Scientific’s USD 1.16 billion purchase of Silk Road Medical strengthened its stroke-prevention line with a focus on minimally invasive trans-carotid access.

Teleflex’s EUR 760 million acquisition of BIOTRONIK’s vascular division adds drug-eluting capabilities and bioresorbable scaffold IP, reinforcing the shift toward coated and dissolving implants. Meanwhile, MicroVention’s rebrand to Terumo Neuro signals deeper neuro-vascular commitment, including FDA clearance of an all-visible coil-assist stent that enhances procedural visualization.

Differentiation now centers on coating science, AI-enabled workflow, and material innovation. Early-access programs for hydrophilic polymer-coated flow-diverters show marked declines in platelet activation, while real-time catheter-tracking software is being bundled with hardware to create ecosystem lock-in. White-space opportunities linger in emerging regions where simplified deployment kits and remote proctoring tools can offset limited specialist density.

Intracranial Stents Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex acquires BIOTRONIK’s vascular intervention business for EUR 760 million (USD 820 million), adding drug-eluting stents and scaffold technologies.

- June 2024: MicroVention (Terumo Neuro) launches LVIS EVO intraluminal support device in the United States, the first fully visible coil-assist intracranial stent approved domestically.

- June 2024: Boston Scientific finalizes USD 1.16 billion purchase of Silk Road Medical, broadening trans-carotid stroke-prevention offerings

Table of Contents for Intracranial Stents Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Demand For Minimally-Invasive Intracranial Procedures

- 4.2.2Growing Prevalence of Cerebrovascular Disorder & Ageing Demographics

- 4.2.3Improving Healthcare Infrastructure and Expanding Reimbursement Coverage

- 4.2.4Technological Advancement and Product Innovation

- 4.2.5Growing Awareness and Early Diagnosis of Neurovascular Disorders

- 4.2.6AI-Guided Neuro-Interventional Planning Improving Treatment Candidacy

- 4.3Market Restraints

- 4.3.1Scarcity Of Highly-Skilled Neuro-Interventionalists

- 4.3.2Post-Procedural In-Stent Restenosis & Thrombosis Risk

- 4.3.3Cost-Containment Pressures In Emerging Public Health Systems

- 4.3.4Limited Long-Term Clinical Evidence For Next-Gen Bio-Resorbable Designs

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Type

- 5.1.1Self-expanding Stents

- 5.1.2Balloon-expanding Stents

- 5.1.3Stent-assisted Coil Embolization Systems

- 5.1.4Flow-diverter Stents

- 5.2By Material

- 5.2.1Nitinol

- 5.2.2Cobalt-Chromium

- 5.2.3Polymer / Bioresorbable

- 5.3By Application

- 5.3.1Intracranial Stenosis

- 5.3.2Brain Aneurysm

- 5.3.3Arterio-Venous Malformation (AVM)

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Ambulatory Surgery Centers

- 5.4.3Specialty Neurology Clinics

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Wallaby Medical

- 6.3.2Stryker Corp.

- 6.3.3Terumo Corp.

- 6.3.4MicroPort Scientific

- 6.3.5Acandis GmbH

- 6.3.6Balt Group

- 6.3.7phenox GmbH

- 6.3.8Medtronic plc

- 6.3.9Rapid Medical

- 6.3.10InspireMD

- 6.3.11Boston Scientific Corporation

- 6.3.12TonBridge Medical

- 6.3.13Lepu Medical Technology(Beijing)Co.,Ltd

- 6.3.14Sino Medical Sciences Technology Inc.

- 6.3.15Contego Medical, Inc

7. Market Opportunities and Future Outlook

- 7.1White-Space and Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Type

- Self-expanding Stents

- Balloon-expanding Stents

- Stent-assisted Coil Embolization Systems

- Flow-diverter Stents

- Self-expanding Stents

- By Material

- Nitinol

- Cobalt-Chromium

- Polymer / Bioresorbable

- Nitinol

- By Application

- Intracranial Stenosis

- Brain Aneurysm

- Arterio-Venous Malformation (AVM)

- Intracranial Stenosis

- By End-User

- Hospitals

- Ambulatory Surgery Centers

- Specialty Neurology Clinics

- Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Intracranial Stents Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 22.08 bn (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 2.90 bn (2023) | Global Consultancy A | Narrower device list; excludes flow-diverter hybrids; static ASPs | ||

USD 0.44 bn (2024) | Trade Journal B | High-income sample only; relies on historical sales extrapolation | ||

USD 3.22 bn (2025) | Industry Association C | Focus on hospital invoices; omits ambulatory centers and emerging regions |