Integrated Microwave Assembly Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

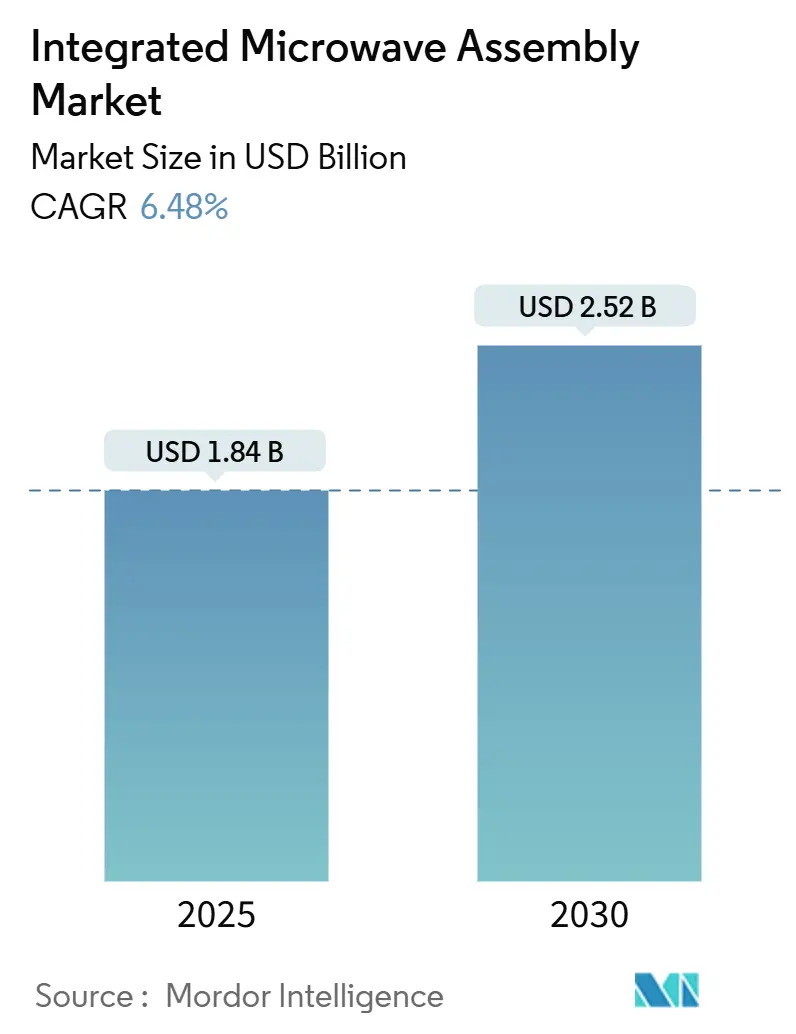

| Market Size (2025) | USD 1.84 Billion |

| Market Size (2030) | USD 2.52 Billion |

| Growth Rate (2025 - 2030) | 6.48% CAGR |

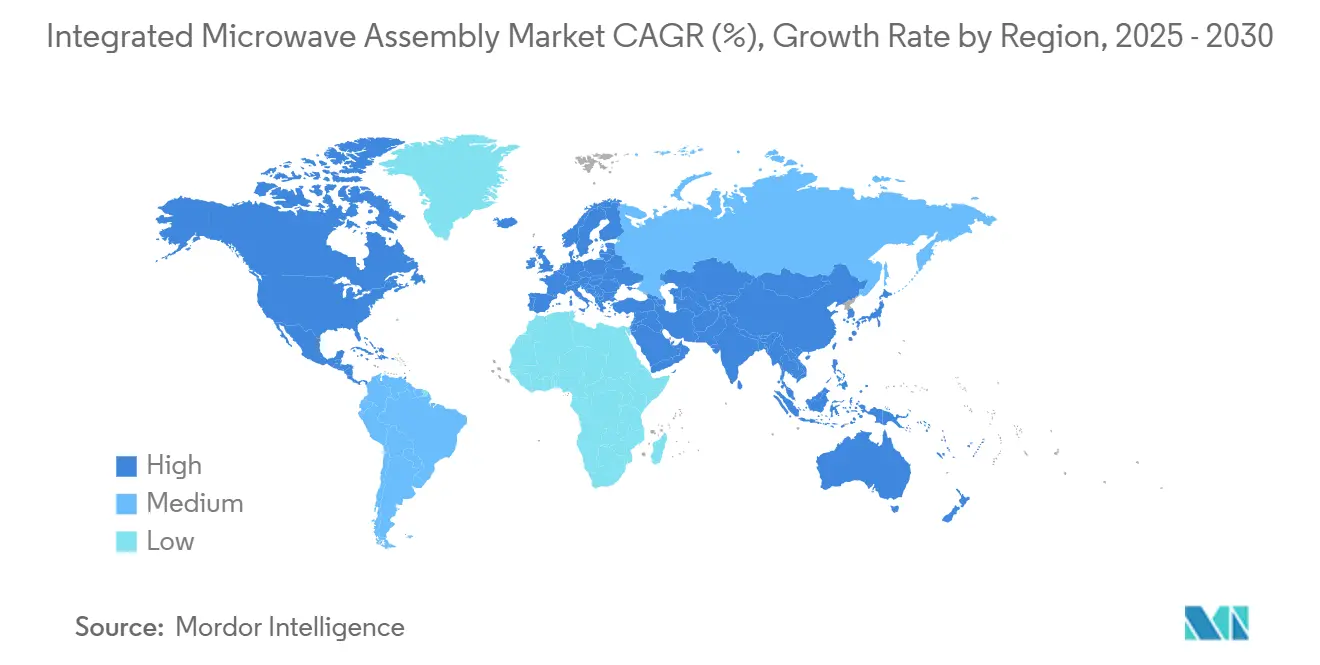

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Integrated Microwave Assembly Market Analysis by Mordor Intelligence

The Integrated Microwave Assembly market size reached USD 1.84 billion in 2025 and is projected to climb to USD 2.52 billion by 2030, registering a 6.48% CAGR over the forecast period. Robust 5G backhaul roll-outs, accelerating low-Earth-orbit (LEO) satellite launches, and active electronically scanned array (AESA) radar modernization programs are converging to lift demand for miniaturized, high-frequency modules. Gallium nitride (GaN) power density breakthroughs are letting integrators shrink size, weight, and power (SWaP) metrics while pushing into W-Band frequencies that enable wider bandwidth and tighter beam steering. At the same time, edge-AI sensing applications require microwave front-ends that combine ultra-low latency with reconfigurable architectures, creating new opportunities for system-on-chip (SoC) designs. Geopolitical efforts to secure domestic gallium supply chains and the CHIPS and Science Act’s incentives for on-shore wafer processing further bolster capital investment in advanced packaging lines. Competition now centers on vertical integration, workforce scale-up, and differentiated IP that shortens design-win cycles.

Key Report Takeaways

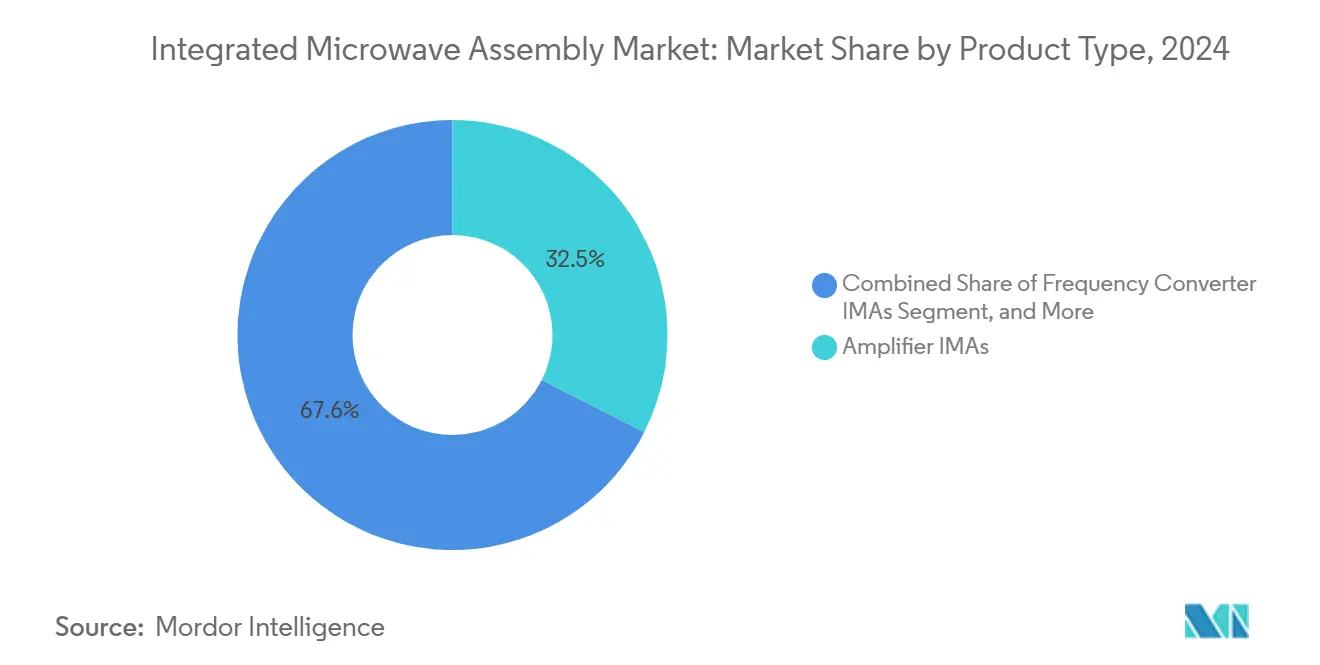

- By product type, amplifier IMAs held 32.45% of the Integrated Microwave Assembly market share in 2024 while synthesizer/LO IMAs are advancing at a 6.94% CAGR through 2030.

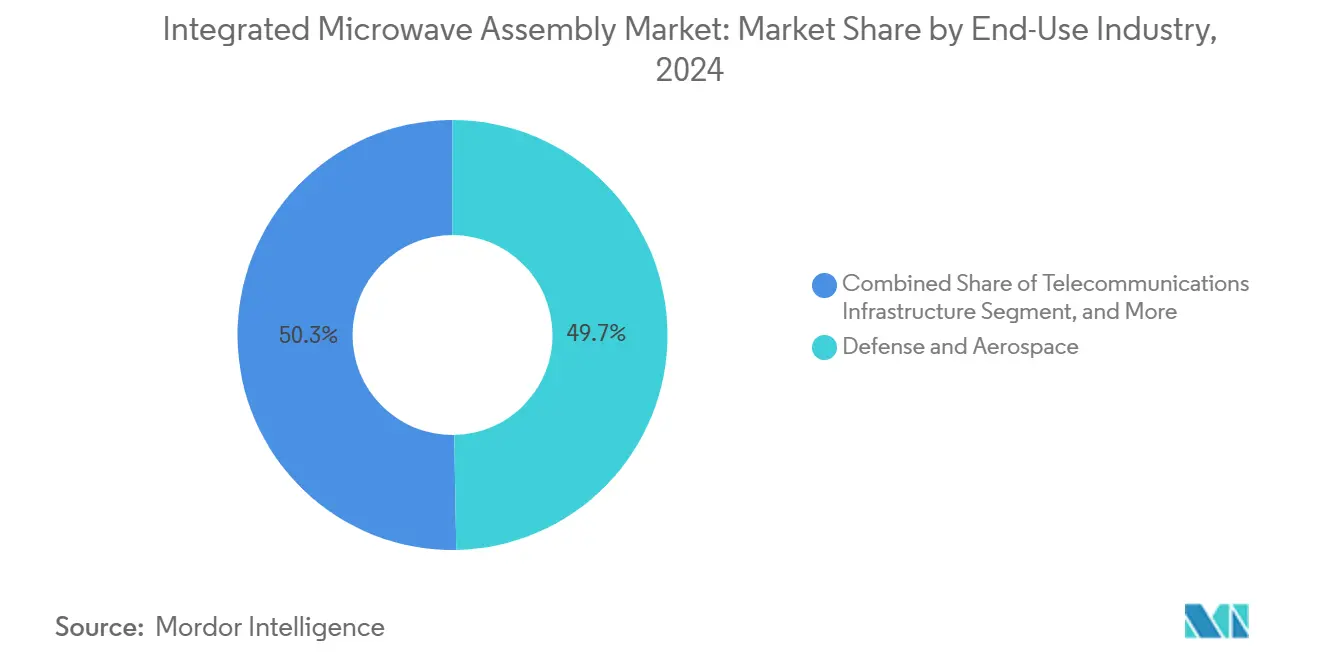

- By end-use industry, defense and aerospace led with 49.73% revenue share in 2024; space and satellite end-uses are forecast to expand at a 6.88% CAGR to 2030.

- By frequency range, X-Band systems accounted for 28.49% of the Integrated Microwave Assembly market size in 2024 and Ka-Band applications are accelerating at a 7.11% CAGR to 2030.

- By integration level, multi-function modules captured 35.12% share of the Integrated Microwave Assembly market size in 2024 while SoC IMAs post the highest projected CAGR at 7.23% between 2025 and 2030.

- By geography, North America commanded 37.87% of the Integrated Microwave Assembly market in 2024 and Asia-Pacific is set to rise at a 6.71% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Integrated Microwave Assembly Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G and SATCOM roll-outs | +1.2% | North America, Asia-Pacific | Medium term (2-4 years) |

| Modernization of AESA radar platforms | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Rising CubeSat launch cadence | +1.1% | Global | Medium term (2-4 years) |

| Edge-AI sensing demand for ultra-low SWaP | +0.9% | North America, Asia-Pacific | Short term (≤ 2 years) |

| GaN-on-Si power density breakthroughs | +1.0% | Global | Medium term (2-4 years) |

| Offset programs nurturing local production | +0.4% | Middle East, ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G and SATCOM roll-outs lift demand for miniaturized high-frequency modules

The Seamless Air Alliance’s push to certify 5G non-terrestrial networks for in-flight connectivity illustrates how terrestrial and satellite architectures are merging, forcing operators to source broadband IMAs that tolerate both millimeter-wave attenuation and stringent linearity requirements. [1]Seamless Air Alliance. "Seamless Air Alliance works to integrate 3GPP 5G satellite networks into aviation sector." militaryaerospace.com Dual-carrier microwave backhaul links already support 60% of macro cell sites, and traffic growth tied to 4.1 billion projected 5G subscriptions by 2029 will intensify the pull for software-defined, frequency-agile front-ends. Equipment makers therefore prioritize broadband power amplifiers with GaN transistors that dissipate heat efficiently while meeting E-band spectral masks.

Modernization of AESA radar and electronic-warfare platforms

Northrop Grumman’s USD 1.7 billion APG-83 upgrade for legacy F-16 fleets shows how multi-function AESA apertures are redefining radar architecture. Next-generation arrays must switch between surveillance, electronic attack, and communication duties in real time, prompting designers to specify wideband IMAs that maintain phase coherency across multiple octaves. The United Kingdom’s GBP 870 million commitment to ECRS Mk 2 further signals sustained European funding for high-power X- and Ku-Band transmit-receive modules. [2]Jennings, Gareth. "UK awards E-Scan radar contract for Typhoon." janes.com

Rising CubeSat and small-sat launch cadence seeking radiation-hardened IMAs

NASA and NOAA’s USD 54 million QuickSounder contract embodies the pivot toward constellations that rely on lightweight, rad-hard microwave radiometers capable of operating up to 325 GHz. The global rad-hard electronics segment exceeded USD 1.5 billion in 2024, reflecting commercial operators’ need for parts that survive trapped-particle flux in Van Allen belts. [3]Stewart, Duncan, David Jarvis, Christie Simons, and Gillian Crossan. "That's just rad! Radiation-hardened chips take space tech and nuclear energy to new heights." www2.deloitte.com Small-sat integrators thus favor SiGe and GaN processes qualified to 100 krad total-ionizing-dose while preserving low noise figures and DC power budgets.

Edge-AI sensing needs ultra-low-SWaP microwave front-ends

Researchers at City University of Hong Kong fabricated a microwave photonics chip delivering 67 GHz analog bandwidth with 1,000 × lower energy per operation than CMOS digital logic, making it suitable for AI inference at the tactical edge. Combining optical modulators, bandpass filters, and photodetectors on one die eliminates bulky coax cables and helps meet weight constraints on unmanned aerial vehicles. Similar single-chip microwave-photonics demonstrators from IMEC show that programmable optical filters can adapt beam shapes to dynamic interference, a key capability for contested RF environments.

Restraints Impact Analysis of Integrated Microwave Assembly Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High NRE and qualification costs | -1.4% | Global | Medium term (2-4 years) |

| Supply-chain volatility of GaAs/GaN substrates | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Talent shortage in advanced packaging | -0.9% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Export-control compliance burdens | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High NRE and qualification costs for custom IMAs

Full military qualification can stretch 18 months and cost several million USD, a hurdle that deters emerging suppliers and slows design refreshing cycles. The Defense Logistics Agency’s mentor-protégé incentives ease test-equipment access, yet custom IMAs still demand specialized CAD tools, temperature-cycling ovens, and radiation chambers, elevating break-even volumes. Radiation-tolerant designs face even steeper economics because long-duration high-energy-particle testing often repeats after each mask spin, doubling non-recurring spend.

Supply-chain volatility of advanced substrates (GaAs/GaN)

China controls 98% of primary gallium output, and a 30% export disruption could erase up to USD 602 billion in downstream U.S. economic activity, according to the Center for Strategic and International Studies. The U.S. Geological Survey estimates that a blanket gallium ban would lift spot prices by over 150%. Domestic recovery projects like Montana’s Sheep Creek deposit are promising but years away from commercial scale, leaving defense primes dependent on strategic stockpiles and second-source epitaxy vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Integrated Microwave Assembly Market Segment Analysis

By Product Type:

Amplifiers Underpin Volume, Synthesizers Accelerate InnovationAmplifier IMAs accounted for 32.45% of the Integrated Microwave Assembly market share in 2024, underscoring their ubiquity from S-Band telemetry links to Ka-Band satcom gateways. Adoption of GaN Doherty topologies improved back-off efficiency by 7 percentage points, letting operators boost link margins without enlarging heat sinks. Synthesizer/LO IMAs register a 6.94% CAGR as system architects tighten phase-noise budgets for E-Band radios that carry fiber-equivalent throughput. Frequency-converter modules remain critical for heterodyne architectures, while switch-matrix IMAs gain traction in electronic-warfare suites that hop among threat bands in microseconds.

The shift toward multi-function transceiver IMAs is trimming bill-of-materials lines by 18% on average, improving mean-time-between-failures in airborne pods. Meanwhile, digital control IMAs embed SPI-controlled attenuators and phase shifters that simplify calibration at the box level. Independent design houses are offering open-VPX cards populated with drop-in IMAs, bridging legacy RF backplanes with modern software-defined radios.

By Frequency Range:

X-Band Retains Scale, Ka-Band Sets the PaceX-Band captured 28.49% of the Integrated Microwave Assembly market size in 2024, benefiting from entrenched maritime and surface-to-air radar fleets. Its moderate rain attenuation, ample 1 GHz allocations, and mature test infrastructure anchor ongoing retrofit programs. Ka-Band units grow fastest at 7.11% CAGR as LEO operators demand higher spectral efficiency and smaller antennas. The U.S. Army’s requirement for Ka-Band multi-beam terminals with 40 dB/K G/T ratios validates this migration.

Ku-Band maintains relevance in broadcast and inflight-entertainment uplinks, though C-Band faces headwinds from 5G reallocation pressures. V-/W-Band applications are emerging for automotive radar, where 140 GHz prototypes deliver centimeter-level resolution at lower cost than lidar. Multi-band IMAs that cover multiple octaves in a single package are gaining favor with electronic-warfare operators who must counter frequency-agile threats. Hughes Network Systems' exploration of E-Band for very-high-throughput satellites demonstrates how operators are pushing toward higher frequencies despite the rain-fade challenges.

By End-Use Industry:

Defense Dominates, Space AcceleratesDefense and aerospace applications commanded 49.73% of the Integrated Microwave Assembly market in 2024, anchored by multi-billion-dollar radar modernization programs. The F-16 APG-83 AESA upgrade alone represents USD 1.7 billion in addressable content, with similar initiatives underway across NATO fleets. Space and satellite end-uses post the highest growth at 6.88% CAGR, fueled by proliferated LEO constellations and next-generation weather satellites. NASA and NOAA's USD 54 million QuickSounder contract exemplifies how microwave radiometers are becoming central to climate monitoring.

Telecommunications infrastructure represents a substantial segment as carriers densify 5G networks with millimeter-wave small cells and microwave backhaul links. Industrial and test equipment makers specify IMAs for process-control radar and vector network analyzers. Automotive radar adoption accelerates as 140 GHz systems from IMEC and others deliver high-resolution object detection at lower cost than lidar. Medical applications represent a niche but growing segment, with microwave imaging systems offering portable alternatives to MRI for stroke detection and breast cancer screening.

By Integration Level:

Multi-Function Modules Lead, SoC Integration SurgesMulti-function modules (MFMs) held 35.12% of the Integrated Microwave Assembly market share in 2024, striking a balance between integration density and design flexibility. MFMs combine multiple RF functions in a single package while preserving the ability to optimize individual blocks for specific applications. System-on-chip (SoC) IMAs register the highest growth at 7.23% CAGR, enabled by advances in SiGe BiCMOS and GaN-on-Si processes. City University of Hong Kong's 67 GHz microwave photonic chip demonstrates how monolithic integration can slash power consumption by three orders of magnitude.

Connectorized IMAs retain market share in applications requiring field replacement and maximum configuration flexibility. System-in-package (SiP) approaches occupy the middle ground, enabling heterogeneous integration of different semiconductor technologies while maintaining reasonable manufacturing costs. The evolution toward SoC architectures is most pronounced in high-volume applications like automotive radar and 5G handsets, where the economics of custom silicon development become compelling at scale.

Geography Analysis

North America Integrated Microwave Assembly Market

North America captured 37.87% of the Integrated Microwave Assembly market in 2024, supported by robust defense modernization programs and the CHIPS Act's USD 52 billion commitment to domestic semiconductor manufacturing. MACOM Technology Solutions' USD 345 million expansion plan, backed by preliminary CHIPS Program Office agreements for up to USD 70 million in federal funding, exemplifies how policy incentives are catalyzing private investment in advanced manufacturing. The region benefits from a mature ecosystem spanning research universities, defense primes, and specialized foundries that accelerate technology transfer. U.S. dominance in GaN MMIC design and radiation-hardened electronics further cements its leadership position, though supply chain dependencies on imported gallium and germanium represent strategic vulnerabilities.

APAC Integrated Microwave Assembly Market

Asia-Pacific registers the fastest growth at 6.71% CAGR, propelled by China's electronics production surge of 11.3% in 2024 and Taiwan's leadership in advanced semiconductor manufacturing. Taiwan's semiconductor industry faces a 34,000-worker shortage amid rapid capacity expansion, highlighting both the opportunities and constraints shaping regional growth. Japan maintains strength in high-frequency components and test equipment, while South Korea leverages its memory and logic manufacturing expertise to enter adjacent RF markets. India's emerging role in semiconductor design and manufacturing adds another growth vector, though the region's development remains uneven and subject to geopolitical tensions that impact technology transfer.

Europe Integrated Microwave Assembly Market

Europe represents a significant but mature market, with growth driven by defense modernization programs and the European Union's Chips Act aimed at reducing dependence on Asian suppliers. The UK's GBP 870 million investment in ECRS Mk 2 radar systems for Typhoon aircraft demonstrates the region's commitment to maintaining technological sovereignty in critical defense systems. France's semiconductor sector strengthens through the Chips Joint Undertaking and companies like STMicroelectronics expanding GaN-on-Si capabilities. Germany's industrial automation leadership and the Nordic countries' telecommunications infrastructure contribute to steady demand growth, though the region faces challenges from energy costs and regulatory complexity.

Competitive Landscape

The Integrated Microwave Assembly market exhibits moderate fragmentation with established players pursuing vertical integration and technology diversification. MACOM Technology Solutions exemplifies this approach, reporting USD 725.8 million in 2023 revenue with a 49.7% gross margin while simultaneously acquiring ENGIN-IC for GaN MMIC expertise and OMMIC for European semiconductor capabilities. The company's USD 345 million investment to expand 100mm GaN and GaAs production while introducing 150mm GaN capabilities demonstrates its commitment to manufacturing scale.

Strategic positioning increasingly centers on technology portfolio breadth, as evidenced by onsemi's USD 115 million acquisition of Qorvo's Silicon Carbide JFET business and Qorvo's purchase of Anokiwave for beamforming technologies. These transactions reflect how RF semiconductor companies are expanding into adjacent power and antenna markets to capture more system-level value. The semiconductor industry's M&A activity surged to 44 transactions valued at USD 45.4 billion in 2024, up from 33 transactions worth USD 2.7 billion in 2023, indicating accelerating consolidation.

Talent acquisition represents a critical competitive dimension, with semiconductor companies facing a projected shortage of over 67,000 technical roles by 2030. This scarcity creates both recruitment challenges and opportunities for differentiation through workforce development initiatives. Companies with established university partnerships and internship pipelines gain advantage in securing specialized RF design and packaging engineers. The competitive landscape is further complicated by geopolitical factors, with China's control over 98% of gallium production creating supply chain dependencies that favor companies with diversified sourcing strategies and domestic manufacturing capabilities.

Integrated Microwave Assembly Industry Leaders

-

Analog Devices, Inc.

-

Teledyne Microwave Solutions (Teledyne Technologies Incorporated)

-

Mercury Systems, Inc.

-

Qorvo, Inc.

-

MACOM Technology Solutions Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Integrated Microwave Assembly Market Companies Covered in this Report

- Analog Devices, Inc.

- Teledyne Microwave Solutions (Teledyne Technologies Incorporated)

- Mercury Systems, Inc.

- Qorvo, Inc.

- MACOM Technology Solutions Holdings, Inc.

- Cobham Limited

- L3Harris Technologies, Inc.

- Keysight Technologies, Inc.

- Narda-MITEQ (L3 Narda MITEQ Corp.)

- Aethercomm, Inc.

- Anaren, Inc. (TT Electronics plc)

- NuWaves Engineering (NuWaves Ltd.)

- Aviat Networks, Inc.

- K&L Microwave, Inc. (Smiths Interconnect Inc.)

- Nisshinbo Micro Devices Inc.

- API Technologies Corp. (Carlisle Interconnect Technologies LLC)

- Planar Monolithics Industries, Inc.

- Akon, Inc.

- Giga-tronics Incorporated

- Microwave Engineering Corporation

Recent Industry Developments in Integrated Microwave Assembly Market

- June 2025: The U.S. Army issued requirements for Ka-band multi-beam lens array antenna terminals under its Next Generation Tactical Terminal project, seeking production-ready systems capable of supporting LEO, MEO, and GEO satellite constellations.

- April 2025: Honeywell International received a USD 1.5 million DARPA contract to develop atomic vapor sensors for millimeter-wave communications, imaging, and RF electrometry applications under the EQSTRA program.

- February 2025: RTX's Raytheon division completed flight testing of the first AI/ML-powered Radar Warning Receiver for fourth-generation aircraft, known as the Cognitive Algorithm Deployment System.

- January 2025: MACOM Technology Solutions unveiled a five-year, USD 345 million investment plan to expand 100mm GaN and GaAs production while introducing 150mm GaN capabilities, supported by preliminary agreements with the CHIPS Program Office for up to USD 70 million in federal funding.

Global Integrated Microwave Assembly Market Report Scope

Segmentation Overview

| Amplifier IMAs |

| Frequency Converter IMAs |

| Synthesizer / LO IMAs |

| Transceiver IMAs |

| Switch-Matrix IMAs |

| Digital Control and Mixed-Signal IMAs |

| C-Band (4–8 GHz) |

| X-Band (8–12 GHz) |

| Ku-Band (12–18 GHz) |

| Ka-Band (26.5–40 GHz) |

| V-/W-Band (40–110 GHz) |

| Multi-band / Broadband |

| Defense and Aerospace |

| Telecommunications Infrastructure |

| Industrial and Test Instrumentation |

| Space and Satellite |

| Automotive and Transportation |

| Medical and Life-Sciences |

| Connectorized IMA |

| Multi-Function Module (MFM) |

| System-in-Package (SiP) IMA |

| System-on-Chip (SoC) IMA |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Amplifier IMAs | ||

| Frequency Converter IMAs | |||

| Synthesizer / LO IMAs | |||

| Transceiver IMAs | |||

| Switch-Matrix IMAs | |||

| Digital Control and Mixed-Signal IMAs | |||

| By Frequency Range | C-Band (4–8 GHz) | ||

| X-Band (8–12 GHz) | |||

| Ku-Band (12–18 GHz) | |||

| Ka-Band (26.5–40 GHz) | |||

| V-/W-Band (40–110 GHz) | |||

| Multi-band / Broadband | |||

| By End-Use Industry | Defense and Aerospace | ||

| Telecommunications Infrastructure | |||

| Industrial and Test Instrumentation | |||

| Space and Satellite | |||

| Automotive and Transportation | |||

| Medical and Life-Sciences | |||

| By Integration Level / Technology | Connectorized IMA | ||

| Multi-Function Module (MFM) | |||

| System-in-Package (SiP) IMA | |||

| System-on-Chip (SoC) IMA | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving growth in the Integrated Microwave Assembly market?

The market is primarily driven by 5G infrastructure deployment, defense radar modernization programs, and proliferating small satellite constellations. GaN power density breakthroughs and edge-AI sensing requirements are creating demand for ultra-low SWaP microwave front-ends, with the market projected to reach USD 2.52 billion by 2030 at a 6.48% CAGR.

How is the defense sector impacting the Integrated Microwave Assembly market?

Defense applications command nearly 50% of the Integrated Microwave Assembly market, with multi-billion dollar AESA radar upgrades like the F-16's APG-83 program (USD 1.7 billion) and the UK's ECRS Mk 2 (GBP 870 million) creating sustained demand for high-performance X-band and Ku-band modules.

What frequency bands are seeing the most growth in Integrated Microwave Assembly applications?

Ka-band applications are growing fastest at 7.11% CAGR through 2030, driven by next-generation satellite communications and the U.S. Army's requirements for multi-beam terminals supporting LEO, MEO, and GEO constellations simultaneously. X-band maintains the largest share at 28.49% due to established radar and defense applications.

How are supply chain vulnerabilities affecting the Integrated Microwave Assembly industry?

China's 98% control of global gallium production creates significant vulnerability, with the USGS estimating a potential USD 3.4 billion impact on U.S. GDP from export disruptions. This has prompted strategic stockpiling and investments in domestic gallium recovery projects, though these remain years from commercial scale.

What integration trends are shaping the future of microwave assemblies?

System-on-Chip (SoC) IMAs are growing fastest at 7.23% CAGR as advances in SiGe BiCMOS and GaN-on-Si processes enable monolithic integration of RF, analog, and digital functions. Multi-Function Modules currently lead with 35.12% market share, offering a balance between integration density and design flexibility.

Which companies are leading the Integrated Microwave Assembly market?

MACOM Technology Solutions, Qorvo, and Analog Devices lead with approximately 27% combined market share. MACOM reported USD 725.8 million in 2023 revenue with 49.7% gross margin and is investing USD 345 million to expand GaN and GaAs production capabilities, while strategic acquisitions like Qorvo's purchase of Anokiwave reflect industry consolidation trends.

Page last updated on: