Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

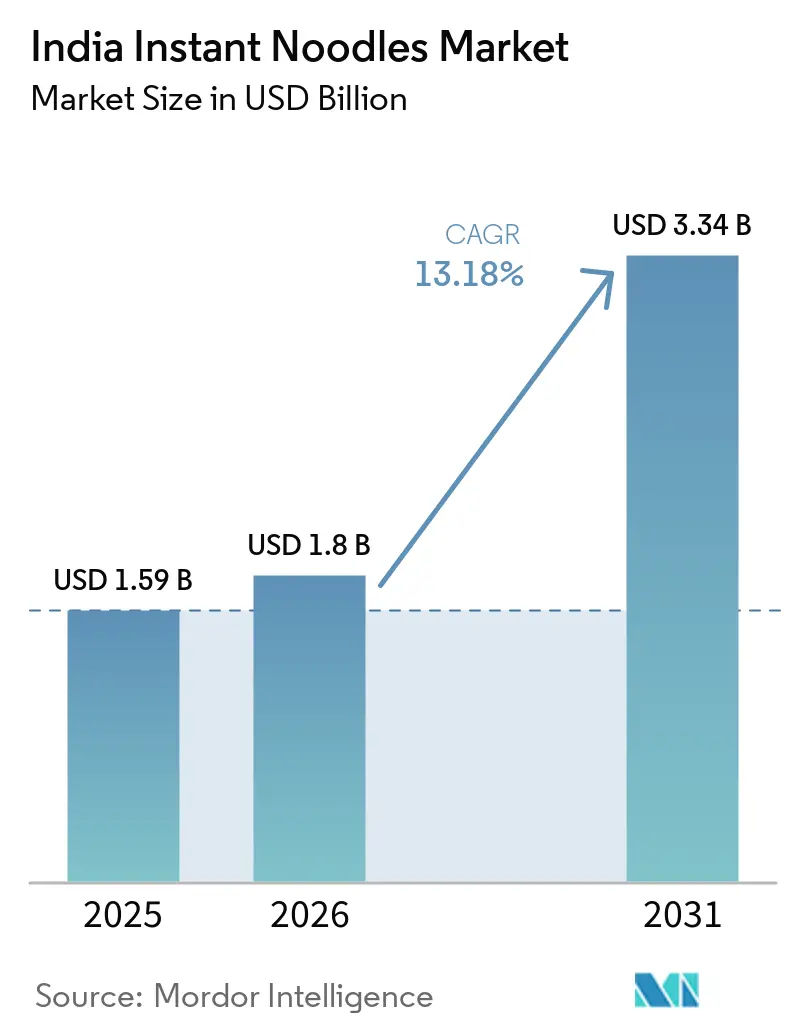

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 13.18% CAGR |

| Market Concentration | High |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Instant Noodles Market Analysis by Mordor Intelligence

The Indian instant noodles market size was valued at USD 1.59 billion in 2025 and estimated to grow from USD 1.8 billion in 2026 to reach USD 3.34 billion by 2031, at a CAGR of 13.18% during the forecast period (2026-2031). Rapid urban migration, quick-commerce penetration, and a growing appetite for global flavors are broadening both the buyer base and the usage occasions for the Indian instant noodles market. Urban households now combine traditional masala preferences with adventurous Korean variants, creating parallel value and volume growth streams. Retail digitalization, led by 10-minute delivery apps, is reshaping route-to-market economics, while packaging innovation in cup formats adds premium price ceilings without material demand erosion. Simultaneously, programs focusing on fortification, millet incorporation, and sodium reduction highlight the Indian instant noodles market's blend of nutrition and convenience in its offerings.

Key Report Takeaways

- By product type, vegetarian noodles led with 67.62% revenue share in 2025; vegetarian options are expanding at a 13.42% CAGR through 2031.

- By serving size, single-serve packs captured 62.05% of the Indian instant noodles market share in 2025, while multi-serve volumes are projected to climb at 13.36% CAGR through 2031.

- By packaging, packets retained 74.61% share of the Indian instant noodles market size in 2025, and cup/bowl formats are advancing at a 14.31% CAGR to 2031.

- By flavor, traditional masala held 79.88% share in 2025; Korean spicy variants post the highest 13.27% CAGR outlook to 2031.

- By distribution channel, supermarkets and hypermarkets controlled 41.05% revenue in 2025, yet online retail is tracking a 14.56% CAGR through the forecast period

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Instant Noodles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and changing lifestyles | +3.2% | National, concentrated in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Premiumization via Korean/K-flavour wave | +2.1% | Urban metros, North India early adoption | Short term (≤ 2 years) |

| Product innovation and packaging | +1.8% | National, with manufacturing hubs in Gujarat, Maharashtra | Medium term (2-4 years) |

| Rising demand for convenient, ready-to-eat food | +2.9% | Urban centers, expanding to semi-urban markets | Long term (≥ 4 years) |

| Flavor experimentation and trend adoption | +1.4% | Metro cities, youth demographics | Short term (≤ 2 years) |

| Growth of e-commerce and quick-commerce platforms | +2.5% | Urban markets, rapid expansion in Tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid urbanization and changing lifestyles

India's urban transformation is driving shifts in demand patterns, extending beyond basic convenience. This change highlights that urbanization is not only increasing consumption volumes but also redirecting spending towards premium segments. The Ministry of Statistics and Programme Implementation reported that the average monthly per capita consumption expenditure (MPCE) in urban India for 2023-24 was INR 6,996, excluding the value of items provided free through various social welfare programs[1]Source: Ministry of Statistics and Programme Implementation, "Household Consumption Expenditure Survey", pib.gov.in. As more of India's working-age population moves to cities, this trend is accelerating, particularly in areas where traditional cooking facilities are less accessible. Urban residents, often pressed for time, are increasingly opting for quick meal solutions like instant noodles. Urbanization is not restricted to large metropolitan areas; smaller cities are also expanding, widening the customer base for instant noodles beyond conventional urban markets. According to the World Bank, India's urbanization rate reached 36.36% in 2023[2]Source: World Bank, "Development Data", worldbank.org. This urban expansion is driving the growth of supermarkets, hypermarkets, and modern retail outlets, where instant noodles are widely available, boosting their market penetration. These urban and lifestyle changes are creating a favorable environment for instant noodles to emerge as a preferred, convenient meal option in India, driving substantial market growth.

Premiumization via Korean/K-flavour wave

The influence of Korean culture, initially rooted in entertainment, is now reshaping Indian culinary preferences, a shift often underestimated by traditional market analyses. Driven by the popularity of K-pop, K-dramas, and Korean cuisine, Indian consumers, especially millennials and Gen Z, are increasingly drawn to authentic Korean flavors, with spicy ramen varieties gaining significant traction. This rising demand has created a premium segment within the instant noodle market, where Korean-style noodles are sold at higher price points. Indo Nissin's Geki brand exemplifies this trend, appealing to consumers willing to pay more for authentic Korean spice profiles. This cultural shift not only challenges conventional perceptions of Indian taste preferences but also highlights a key insight: cultural affinity can outweigh price sensitivity in specific demographic groups. Recognizing this opportunity, major FMCG companies are capitalizing on the demand for Korean flavors. Nestle and Hindustan Unilever have introduced Korean variants to capture this growing market. In November 2023, Nestle Maggi launched barbecue-flavored Korean noodles in two variants, BBQ Chicken and BBQ Veg. Priced at INR 60 and INR 55, respectively, each 90g pack reflects the premium positioning of these products.

Product innovation and packaging

Innovation now goes beyond flavor development, encompassing advancements in packaging technology and nutritional enhancements to meet changing consumer expectations. By offering a variety of flavors, such as PAN Asian, Korean, fusion, and regional Indian, brands address evolving consumer preferences while generating excitement. This approach appeals to trend-sensitive youth and drives repeat purchases. To cater to increasing health awareness, companies have introduced millet-based, whole-grain, low-sodium, and organic noodle options, broadening their consumer base beyond traditional instant noodle consumers. ITC's launch of millet-based YiPPee noodles highlights this health-focused trend. Simultaneously, companies are adopting sustainable packaging solutions, utilizing materials like sugarcane bagasse and other biodegradable alternatives. Cup and bowl formats are experiencing significant growth, with a 14.82% CAGR, driven by demand for portion control and premium positioning. The packaging innovation cycle is accelerating as companies strive to balance convenience, sustainability, and cost, while adhering to FSSAI labeling requirements that mandate clear nutritional and allergen information.

Rising demand for convenient, ready-to-eat food

Structural changes in Indian household dynamics are driving the demand for convenience, extending beyond urban areas into semi-urban and rural regions. Urban consumers, particularly working professionals and students, often face time constraints, leaving little opportunity for cooking. Instant noodles, which require minimal time and effort to prepare, perfectly address this need for convenience. Busy families, single-person households, hostellers, and young adults increasingly rely on instant noodles as a quick meal or snack option. This widespread adoption reinforces instant noodles' position as a staple convenience food. The growing popularity of multi-serve packs, with a 13.51% CAGR, highlights a shift in perception, as instant noodles are now viewed as complete meal solutions rather than just snacks. This trend is further fueled by the rise of nuclear families, which reduces the transfer of traditional cooking knowledge and increases dependence on packaged solutions. Regional players like Wai Wai are leveraging this trend by introducing location-specific flavors, such as Akabare noodles in North Bengal and Sikkim, effectively combining convenience with regional taste preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns about high sodium, MSG, and preservatives | -2.3% | National, particularly urban educated consumers | Long term (≥ 4 years) |

| Regulatory and food safety scrutiny | -1.1% | National, with stricter enforcement in metros | Medium term (2-4 years) |

| Intense competition and price wars | -1.8% | National, most intense in North and West India | Short term (≤ 2 years) |

| Anti-HFSS advertising rules restricting kid-focused promos | -0.9% | National, immediate impact on marketing strategies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns about high sodium, MSG, and preservatives

With rising health consciousness, companies are focusing on balancing convenience with wellness. Regular consumption of instant noodles, especially among women, has been associated with cardiometabolic syndrome. Seasoning packets typically contain most of the sodium and additives, which can worsen health issues. The combination of high sodium and capsaicin in spicy instant noodles can further aggravate these problems. The increased risks of heart disease and diabetes linked to frequent instant noodle consumption have driven calls for reformulation. In response, companies are enhancing noodles with iron, launching reduced-sodium options, and using organic ingredients. However, these adjustments often lead to higher costs and potential changes in taste profiles, posing challenges to retaining consumer loyalty. The situation is further complicated as health-conscious consumers prioritize both convenience and transparency in ingredient lists.

Anti-HFSS advertising rules restricting kid-focused promos

FSSAI's stringent restrictions on marketing high-fat, sugar, and salt foods near schools are transforming promotional strategies for instant noodles. The regulations ban advertising within 50 meters of school premises and limit marketing efforts aimed at children under 16. This change significantly affects brands that have traditionally relied on youth-focused campaigns to build loyalty. Hindustan Unilever's decision to cease marketing food products to children under 16 highlights an industry-wide adjustment to these rules. As a result, companies are shifting their focus to adult-oriented messaging and health-centric strategies, which may weaken the emotional connections that drive long-term brand loyalty. Compliance costs are rising as businesses must redesign marketing campaigns and distribution strategies to adhere to school proximity restrictions while maintaining market reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetarian Staples Sustain Growth Headroom

Vegetarian SKUs held 67.62% share of the India instant noodles market in 2025 and are on track for 13.42% CAGR through 2031. Familial dietary norms and price competitiveness underpin this dominance. In 2023, about 30% of India's population adhered to a vegetarian diet, as per the India Brand Equity Foundation (IBEF). This reflects increasing awareness among Indians regarding the health and environmental benefits of plant-based diets. Producers exploit whole-grain flours and Ayurvedic herbs to extend the vegetarian palette, thereby shielding margins from commodity-meat volatility and halal certification overheads. Non-vegetarian SKUs appeal to protein seekers in metro cities yet face episodic supply disruptions.

Regional consumption patterns heighten segmentation complexity. North Indian buyers prefer paneer-flavored variants, while southern states gravitate toward curry-leaf and tomato notes. Patanjali positions its INR 15 wheat-based noodle as a “satvik” snack, reinforcing trust among cost-conscious buyers. This granular tailoring tightens shelf rotation, indicating that cultural alignment is critical for maintaining leadership in the Indian instant noodles market.

By Serving: Single-Serve Dominance Gives Way to Multi-Serve Momentum

In 2025, single-serve units led the category, contributing 62.05% of its value. These packets, designed for single meals or snacks, minimize food wastage compared to multi-packs and appeal to small families, bachelors, and students. At the same time, multi-serve packs are experiencing growth, with a 13.36% CAGR, surpassing the category average. This growth is fueled by nuclear families increasingly choosing noodles as a quick dinner option. On e-commerce platforms, 4-pack and 6-pack bundles are popular due to improved shipping economics, which see an 8-10% cost reduction. This allows platforms to set free delivery thresholds, encouraging larger purchases.

From a production perspective, multi-serve packs offer significant cost advantages, with per-unit film costs decreasing by 12% compared to single-serve packs. Brands are using these savings to enhance the quality of spice mixes. For example, Tata Consumer repackaged its Schezwan range into family packs to target weekday dinner occasions. These innovations are shifting noodles from being just snacks to quasi-meals, broadening their consumption throughout the day.

By Packaging: Cup Formats Carve Premium Islands Amid Packet Strongholds

In 2025, packets held a dominant 74.61% share of the revenue. Packet noodles are more affordable than their cup and bowl counterparts, making them popular across both urban and rural areas in India. This cost advantage drives high sales volumes, reinforcing their market leadership. However, cup formats are growing faster, with a notable CAGR of 14.31%. Office canteens, hostels, and transit lounges favor the convenience of boil-in-cup noodles. To meet this demand, manufacturers are implementing dual-line facilities that can switch between pillow packs and thermoformed cups within 30 minutes, reducing downtime and enhancing asset efficiency.

As sustainability pressures increase, the industry is responding. Sugarcane-bagasse sleeves reduce virgin plastic usage by 60% and comply with proposed EPR targets, though they add 3-5 cents per unit to costs. Early adopters of these eco-friendly solutions are gaining favor with environmentally conscious consumers, leading to measurable shelf visibility improvements in modern trade outlets. This shift indicates that packaging could soon become a critical factor in shaping price and value dynamics in India's instant noodles market.

By Flavor Variant: Masala Heritage Persists as Korean Heat Accelerates

In 2025, masala flavors captured a substantial 79.88% of the revenue, emphasizing the strong preference for local spices. Meanwhile, Korean flavors, such as hot chicken, kimchi, and buldak recipes, are gaining traction with an impressive 13.27% CAGR. Indo Nissin's Geki line, inspired by aspirational pop culture, is distributed through its premium outlets. The resilience of masala is showcased through regional variations like Biryani Masala in Hyderabad and Sambhar Masala in Chennai, which help established players fend off niche competitors.

Flavor diversification plays a crucial role as a risk mitigation strategy. In the event of stricter regulatory limits on sodium content, Korean offerings could adapt by shifting toward gochujang-based heat profiles, which maintain their bold and spicy appeal. Similarly, masala products could evolve into reduced-salt variants while retaining their aromatic intensity through garam spice blends. These adaptive strategies ensure that sensory satisfaction remains intact, enabling manufacturers to safeguard market volumes in India's instant noodle sector, even under stringent health and regulatory mandates. By proactively addressing potential challenges, the industry can continue to meet consumer demands while adhering to evolving health standards.

By Distribution Channel: Supermarkets Anchor Volume as Online Outpaces All

In 2025, supermarkets and hypermarkets contributed 41.05% of retail receipts, serving as key locations for discovering new flavors through dedicated noodle bays. Offering a wide range of instant noodle brands and variants, these outlets have become the preferred choice for consumers seeking variety. In 2024, DMart operates 424 locations, maintaining its position as India's leading supermarket chain. On the other hand, online stores achieved a notable 14.56% CAGR, driven by the convenience of rapid doorstep delivery. Brands now consider quick-commerce shelves as high-velocity end-caps and are willing to pay slotting fees comparable to eye-level placements in physical stores.

Traditional kiranas continue to provide last-mile services in semi-urban areas, but their market share is gradually shrinking due to increasing smartphone penetration. To avoid channel conflicts and ensure shelf presence, forward-thinking manufacturers are introducing exclusive bundle SKUs for kiranas while capitalizing on digital volume growth. This dual-track strategy expands their market reach while maintaining pricing discipline.

Geography Analysis

India's instant noodles market showcases distinct regional variations, shaped by cultural preferences, economic development, and distribution capabilities. Northern states lead in per-capita consumption, influenced by wheat-centric diets and urban hubs like Delhi NCR, Punjab, and Uttar Pradesh. Recognizing the region's growth potential, ITC is intensifying its YiPPee market share efforts in Northern India, despite facing stiff competition from established brands.

Gujarat and Maharashtra have emerged as significant manufacturing hubs in the western region of India. These states benefit from strategic advantages such as access to ports and a well-established industrial infrastructure, which have attracted companies like Balaji Wafers and Ayoni Foods to set up their production facilities. Additionally, the region's thriving entrepreneurial ecosystem plays a crucial role in fostering private label manufacturing and contract production. This environment enables smaller brands to scale their operations effectively, leveraging the support and opportunities provided by the robust industrial framework.

The southern states, with their advanced food processing infrastructure and export focus, present unique opportunities. Tamil Nadu stands out as a leader in processed food exports, while Karnataka is carving a niche as a tech-driven manufacturing hub. In the east, there's a marked preference for spicier variants. Companies like Wai Wai are responding by launching products like Akabare noodles in North Bengal and Sikkim, tailored to local heat-intensive flavor preferences. This regional analysis underscores that successful market entry hinges on grasping local tastes, distribution nuances, and the competitive landscape, all of which vary widely across India's vast geography. While FSSAI regulations are uniform nationwide, the intensity of enforcement and consumer awareness fluctuates by region, posing challenges for companies with pan-India strategies.

Competitive Landscape

The Indian instant noodles market is consolidated, with Nestle's Maggi holding a significant market share. However, it faces ongoing competition from regional players and emerging Korean-influenced brands that capitalize on cultural trends and localized distribution strategies. The competitive landscape highlights a market where established players must defend their position against premium Korean entrants and value-driven regional brands that address distribution gaps and cater to price-sensitive segments. The major players operating in the market are Nestle SA, Unilever Plc, ITC Limited, Nissin Foods Holdings Co., Ltd, and Patanjali Ayurved, among others.

Established brands prioritize regional adaptation and rural market penetration, while D2C and imported brands focus on niche urban consumers. Strategic consolidation is gaining momentum, for instance, in January 2024, Tata Consumer's acquisition of a 75% stake in Capital Foods, aimed at challenging Maggi's dominance and strengthening its foothold in the instant noodles segment.

Opportunities are emerging in health-focused variants, premium Korean flavors, and sustainable packaging solutions. However, incumbents face innovation challenges due to scale economics and legacy brand positioning. Private label manufacturing, offered by companies like Ayoni Foods, enables smaller brands to scale production while concentrating on marketing and distribution. This dynamic increases competitive pressure on established players, who must balance premium positioning with cost competitiveness across diverse market segments.

India Instant Noodles Industry Leaders

-

Nestle SA

-

ITC Limited

-

Unilever Plc

-

Nissin Foods Holdings Co., Ltd

-

Patanjali Ayurved Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nestlé India has launched a new Maggi noodles production line at its Sanand facility in Gujarat. This expansion, achieved with an investment of INR 105 crores, enhances the facility's capacity by approximately 20,300 tonnes per year.

- December 2024: Wai Wai Noodles has introduced three bold new flavors: Dynamite Range Super Spicy Korean Noodles, Xpress Cheese Range, and Seasoned Masala Noodles (SMN). These offerings are designed to meet evolving consumer preferences, blending authentic ingredients with creative recipes to deliver exceptional flavor.

- November 2023: Nestle Maggi launched barbeque-flavored Korean noodles in two variants—BBQ Chicken and BBQ Veg. Priced at INR 60 and INR 55, respectively, each 90g pack reflects the premium positioning of these products.

- January 2023: WickedGud, a direct-to-consumer (D2C) health food brand, introduced a new line of instant noodles crafted from a blend of oats, lentils, whole wheat, millets, and brown rice. These noodles are 100% free from refined flour, devoid of any added oils, and entirely free from harmful chemicals. They offer a wholesome and nutritious alternative compared to traditional instant noodles.

India Instant Noodles Market Report Scope

Instant noodles are sold in a precooked and dried block with flavoring powder and seasoning oil.

India's instant noodles market is segmented by product type and distribution channel. The market is segmented by product type into cup/bowl and packet. The market is segmented by distribution channel into supermarkets/hypermarkets, convenience/ grocery stores, online retail stores, and other distribution channels.

The market sizing and forecasts have been done for each segment based on value (in USD).

By Product Type

| Vegetarian |

| Non-Vegetarian |

By Serving

| Single Serve Packs |

| Multi Serve Packs |

By Packaging

| Cup/Bowl |

| Packet |

By Flavor Variant

| Masala |

| Spicy (Korean) |

| Chinese |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Vegetarian |

| Non-Vegetarian | |

| By Serving | Single Serve Packs |

| Multi Serve Packs | |

| By Packaging | Cup/Bowl |

| Packet | |

| By Flavor Variant | Masala |

| Spicy (Korean) | |

| Chinese | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How big is the India instant noodles market in 2026?

The India instant noodles market size is valued at USD 1.8 billion in 2026.

What is the projected growth rate for instant noodles in India through 2031?

Category revenue is forecast to rise at a 13.18% CAGR, reaching USD 3.34 billion by 2031.

Which flavor segment is growing fastest?

Korean spicy variants exhibit the quickest expansion with a 13.27% CAGR outlook.

Why are cup noodles gaining share in India?

Cup formats offer utensil-free preparation, portion control, and premium positioning, driving 14.31% CAGR growth.

Page last updated on: