Insight Engine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 8.93 Billion |

| Growth Rate (2026 - 2031) | 25.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insight Engine Market Analysis by Mordor Intelligence

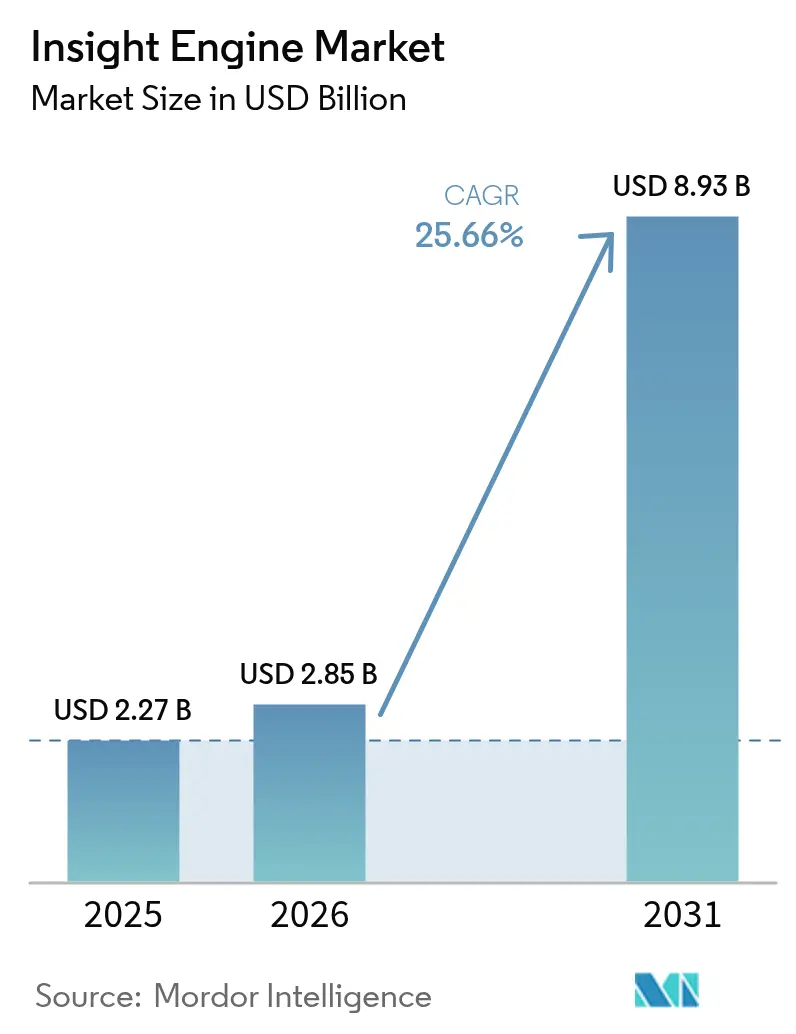

The Insight Engine Market size is expected to grow from USD 2.27 billion in 2025 to USD 2.85 billion in 2026 and is forecast to reach USD 8.93 billion by 2031 at 25.66% CAGR over 2026-2031.

Accelerated adoption of large language models, rising cloud-native deployments, and mounting regulatory scrutiny in data-intensive sectors are reshaping demand patterns. Enterprises are migrating from keyword search toward semantic, multimodal retrieval that unifies text, image, and structured content, cutting information-seeking time for knowledge workers from minutes to seconds. Vector database implementations that support retrieval-augmented generation strengthen user confidence by grounding generative answers in verifiable corporate sources. At the same time, falling infrastructure barriers enable mid-size firms to access capabilities once restricted to global conglomerates, broadening the insight engines market addressable base. Competitive activity revolves around embedding contextual search in security, DevOps, and customer service workflows, creating sticky, outcome-oriented use cases that sustain multi-year contracts.

Key Report Takeaways

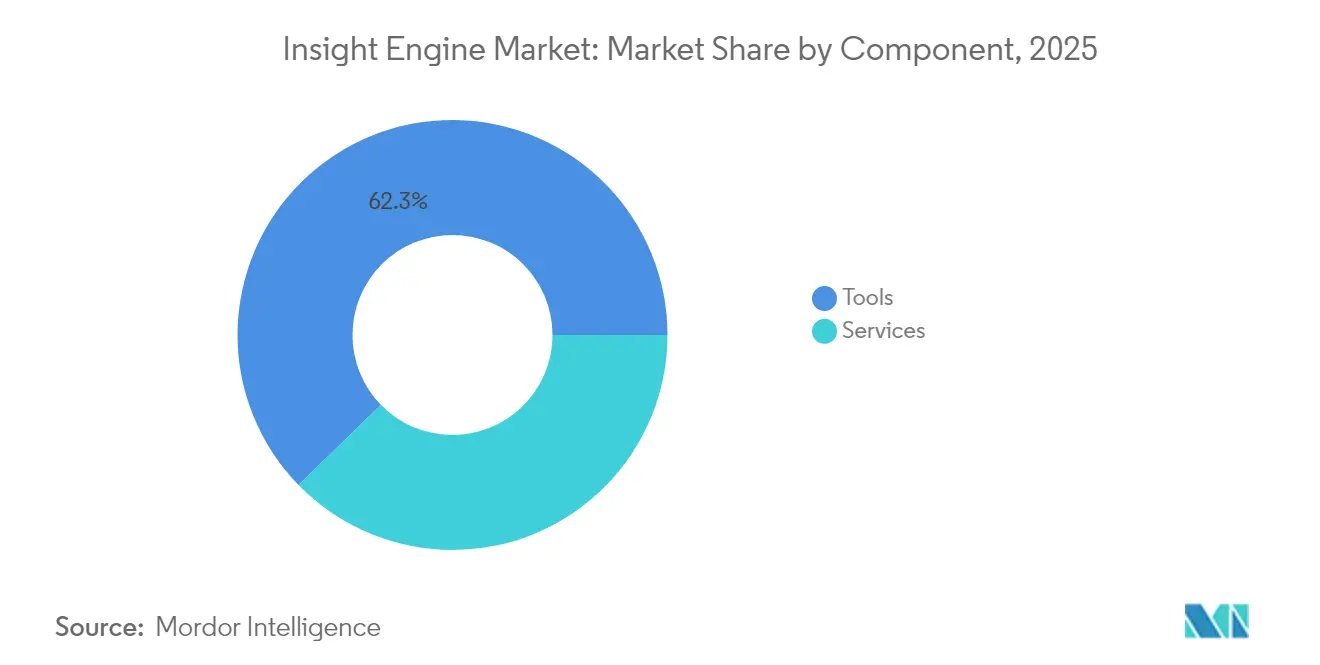

- By component, Tools led with 62.30% revenue share in 2025; Services are projected to expand at a 27.24% CAGR through 2031.

- By deployment mode, Public Cloud held 57.40% of the insight engines market share in 2025 and is advancing at a 31.15% CAGR to 2031.

- By insight type, Contextual Search commanded a 34.60% share of the insight engines market size in 2025, while Conversational Search is set to grow at a 29.05% CAGR through 2031.

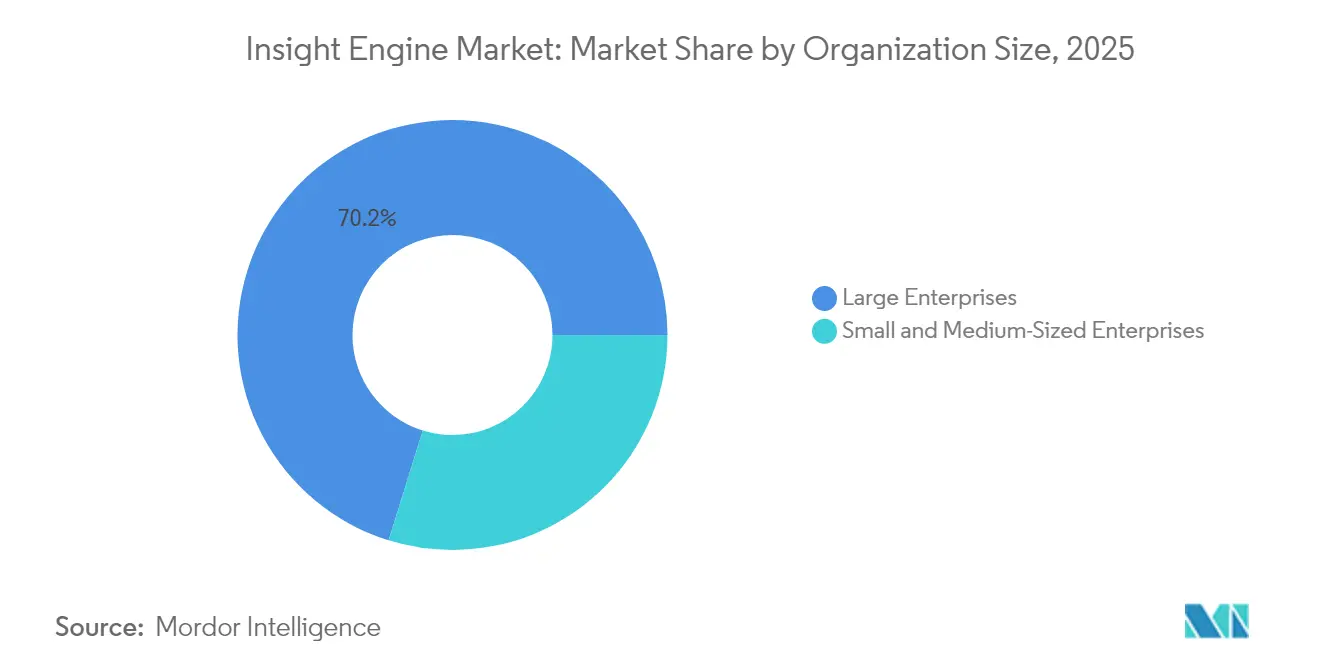

- By organization size, Large Enterprises controlled 70.20% share in 2025; Small and Medium Enterprises recorded the fastest growth at 33.00% CAGR.

- By end-user industry, BFSI captured a 26.70% share in 2025, whereas Healthcare and Life Sciences is forecast to post a 28.55% CAGR to 2031.

- By geography, North America retained a 45.60% share in 2025, while Asia Pacific displays the quickest trajectory at 25.80% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insight Engine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of unstructured enterprise data volumes | +4.2% | Global, highest in North America and Asia Pacific | Medium term (2-4 years) |

| Mainstream adoption of GenAI-augmented enterprise search | +5.8% | Global, led by North America, expanding to Europe and APAC | Short term (≤ 2 years) |

| Shift toward cloud-native SaaS insight platforms | +3.9% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rise of search-based GenAI copilots in SecOps and DevOps | +2.7% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Regulatory-driven surge in e-discovery and ESG investigations | +2.1% | North America and Europe, with spillover to APAC | Long term (≥ 4 years) |

| Embedding of vector DB-RAG architectures enabling multimodal search | +4.5% | Global, with early adoption in North America and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosion of Unstructured Enterprise Data Volumes

Unstructured content constituted 90% of new corporate data in 2024, and global volumes are on track to exceed 73,000 exabytes within two years. Organizations analyze barely half of this information, leaving sizeable value locked in emails, technical manuals, and multimedia assets. Georgia-Pacific’s collaboration with Amazon Web Services illustrates the monetary upside: digitizing decades of plant knowledge through AI chat interfaces is projected to save millions in annual production downtime.[1]Georgia-Pacific and AWS, “Transforming Mill Knowledge With Generative AI,” Amazon Web Services, aws.amazonFinancial institutions replicate the model to surface contextual insights that curb fraud and raise conversion rates. As data footprints balloon, the insight engines market grows because firms require architectures that index billions of vectors while enforcing semantic coherence across evolving knowledge graphs.

Mainstream Adoption of GenAI-Augmented Enterprise Search

Large language models are entering daily workflows as internal copilots. A 2025 cross-industry survey found 63% of firms piloting GenAI first on employee-facing use cases to safeguard brand and privacy.[2]David Carmona, “Granite 3.0: Advancing Enterprise-Grade Language Models,” IBM, ibm.com Cisco’s implementation reduced average query latency by 73% and enabled support teams to resolve 90% of tickets on first contact, saving 5,000 staff hours monthly.[3]Pierre Chao, “Cisco Uses AI to Improve Support Search,” Cisco, cisco.com Natural-language interfaces empower users to ask “why did revenue dip in Q2?” instead of stringing Boolean clauses, trimming decision cycles across banking, healthcare, and manufacturing. The productivity proof points are catalyzing board-level commitments that propel the insight engines market.

Shift toward Cloud-Native SaaS Insight Platforms

Public-cloud deployments capture the largest slice of the insight engines market because scalability and managed security outweigh on-premise control concerns. Mining conglomerates moving to Amazon OpenSearch cut query runtimes from hours to seconds while avoiding capital-intensive refresh cycles. Google Cloud’s native integration of Elasticsearch lets developers ground Gemini responses in enterprise data without custom plumbing. Subscription pricing appeals to finance chiefs seeking predictable OPEX, further accelerating penetration among mid-size firms and emerging markets.

Rise of Search-Based GenAI Copilots in SecOps and DevOps Workflows

Security teams lose time swiveling between SIEM dashboards, ticketing systems, and threat feeds. AI-native platforms that blend high-fidelity threat intel with semantic retrieval cut investigation effort by up to 50%, letting analysts neutralize incidents before lateral movement occurs. DevOps groups mirror the approach, querying large language models for code snippets and automated tests; early adopters report productivity lifts of 20–55% once repetitive scripting work is abstracted away. These tangible benefits spur budget reallocations that enlarge the insight engines market footprint inside cyber-resilience and software delivery toolchains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and governance compliance complexity | –2.8% | Global, highest in Europe and North America | Short term (≤ 2 years) |

| Integration hurdles with legacy knowledge repositories | –3.1% | Global, impacting large enterprises | Medium term (2-4 years) |

| High GPU compute costs for on-prem embeddings | -1.9% | Global, with higher impact in cost-sensitive SME segment | Short term (≤ 2 years) |

| Open-source LLM commoditization of search features | -1.4% | Global, affecting proprietary solution providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Governance Compliance Complexity

The EU’s GDPR and incoming Digital Operational Resilience Act raise the bar for evidence logging, consent management, and model explainability. Financial institutions regard high-quality data lineage as a prerequisite for GenAI rollouts, with 77% citing it as a gating factor. Multinationals therefore funnel resources into encryption, anonymization, and audit trails, elongating project timelines and trimming near-term insight engines market uptake among compliance-heavy sectors.

Integration Hurdles with Legacy Knowledge Repositories

Enterprises hold petabytes of contracts, CAD drawings, and incident tickets inside aging on-premise systems. Two-thirds of IT leaders are migrating users off legacy platforms, yet inconsistent metadata schemes and brittle APIs add 12–18 months to full deployment schedules.[4]Ed McQuiston, “Overcoming Legacy ECM Migration Challenges,” Hyland, hyland.com Manufacturers face extra work extracting tacit know-how from PDF manuals and call-center logs before it can be embedded. These frictions delay ROI and can redirect budgets toward incremental upgrades rather than net-new insight engines market rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Tools Dominance

Tools captured 62.30% of 2025 revenue, reflecting buyer preference for configurable software that dovetails with existing IT stacks. Vendors bundle advanced vector search, ranking algorithms, and relevancy tuning dashboards that out-of-the-box lift retrieval precision beyond keyword baselines. Yet the services segment is projected to grow 27.24% annually as organizations seek advisory partners to integrate domain ontologies, migrate content, and calibrate governance. Services already underpin 55% of total cost of ownership for highly regulated deployments, anchoring sticky multi-year engagements. ServiceNow’s recent Raytion buyout underscores the strategic weight placed on implementation expertise. The dual-track dynamic keeps the insight engines market balanced between product innovation and consultative value capture.

Enterprises adopting industry-specific models demand blueprints for compliance mapping, embedding redaction, and performance monitoring. Specialist integrators differentiate on accelerators that shrink time-to-insight for healthcare, BFSI, or public-sector use cases. Managed services models, delivered via subscription, shift upkeep to vendors and unlock capacity for in-house teams. This transition aligns with CFO goals to turn capex into opex, reinforcing growth momentum in the services slice of the insight engines market.

By Deployment Mode: Public Cloud Dominates Growth

Public cloud accounted for 57.40% of the insight engines market share in 2025 and is set to expand 31.15% per year as customers trade data-center lock-in for elastic compute. Cloud providers integrate GPU instances, vector databases, and policy-driven access controls, letting clients deploy pilots in days rather than quarters. On-premise installations persist in defense, government, and highly regulated finance where data sovereignty or air-gap mandates override convenience. Hybrid models bridge regulated datasets with global SaaS apps, yet operational complexity limits their appeal to organizations with mature DevOps cultures.

The cost economics of storing billions of embeddings favour object storage tiers coupled with serverless query front-ends. Consumption-based billing resonates with SMEs, widening the funnel for the insight engines market size among companies previously priced out of enterprise-grade search. As model weights shrink through quantization and distillation, compute overheads fall, further tilting economics toward cloud-delivered platforms.

By Insight Type: Conversational Search Transforms User Experience

Contextual search maintained 34.60% revenue in 2025, excelling at facet-aware ranking that aligns results with user intent. Conversational interfaces, however, are climbing at a 29.05% CAGR as natural-language questions replace Boolean syntax. The fusion of retrieval-augmented generation with chat UIs produces synthesized answers that cite corporate sources, raising trust and accelerating decision cycles. Predictive and prescriptive analytics modules add scenario modeling, helping planners evaluate “what-if” outcomes inside a single workspace.

Healthcare shows real-world gains: pharmaceutical teams query trial data across siloed registries and condense literature reviews from months to hours. Manufacturing maintenance crews ask handheld copilots for step-by-step repair actions, drawing on historical sensor logs and manuals. Retailers use conversational search to coach customer-service agents on product features in real time. These tangible efficiencies reinforce buyer confidence and fortify the insight engines market trajectory.

By Organization Size: SMEs Drive Adoption Acceleration

Large enterprises commanded 70.20% of spending in 2025, leveraging scale to build cross-functional knowledge layers that support thousands of employees. Yet SMEs post the quickest climb, clocking 33.00% CAGR as cloud SaaS slashes infrastructure prerequisites. Turnkey packages with pre-built connectors, enterprise-grade security, and pay-as-you-grow licensing answer the budget constraints typical of firms with under 500 employees. Survey data shows 91% of AI-adopting small businesses reporting revenue bumps within a year.

SMEs gravitate toward use-case templates such as AI help desks, sales-intelligence digests, and policy search bots. Limited IT headcount magnifies the appeal of managed platforms that abstract patching, scaling, and model upgrades. As open-source language models shrink inference costs, smaller firms access capabilities comparable to Fortune 500 peers, deepening the insight engines market penetration within the mid-market tier.

By End-User Industry: Healthcare Accelerates Beyond BFSI Leadership

BFSI retained the top spot with 26.70% share in 2025 due to stringent e-discovery, anti-money-laundering, and customer-service mandates. Audit trails and explainability features native to enterprise search align with risk-averse banking cultures. Healthcare and Life Sciences, however, is set to outrun BFSI with a 28.55% CAGR through 2031. Drug-discovery teams use semantic search to correlate gene targets with literature citations, expediting candidate identification. Hospitals deploy chat-based interfaces that aggregate patient histories, lab results, and imaging notes into coherent snapshots, trimming diagnosis cycles.

Manufacturing continues digitizing tribal knowledge as baby-boomer experts retire, embedding repair manuals and incident logs into searchable knowledge graphs. Government bodies experiment with multilingual policy bots that speed constituent responses while respecting archival mandates. These sector-specific pain points drive the insight engines industry toward configurable frameworks that overlay domain ontologies and compliance guardrails, sustaining multi-vertical growth.

Geography Analysis

North America generated 45.60% of 2025 revenue, reflecting deep cloud adoption, high digital-talent density, and early-stage GenAI pilots funded by abundant venture capital. Cisco’s documented 73% latency reduction exemplifies how firms convert semantic search into service-cost savings, reinforcing board-level support. Federal agencies also bankroll AI-first knowledge-management programs, cementing a robust reference base that fuels regional network effects within the insight engines market.

Europe trails in topline share but pushes vendors to elevate governance tooling. German developer IntraFind embeds GDPR-compliant anonymization and consent tracking, enabling manufacturers and insurers to scale search while satisfying strict privacy statutes. Funding programmes under Horizon Europe spur public–private consortia that pilot multilingual retrieval across cross-border datasets. These dynamics position Europe as a test bed for explainable AI features likely to propagate globally.

Asia Pacific records the fastest climb at 25.80% CAGR as governments roll out strategic blueprints and allocate research grants. Singapore’s AI Verify initiative certifies model robustness, lending credibility to local deployments. Japanese and South Korean conglomerates layer conversational search on decades of PDF manuals to preserve institutional know-how. Cloud connectivity expansions in India, Indonesia, and the Philippines widen access for SMEs, inflating the insight engines market size across emerging economies. Yet skills shortages and bandwidth constraints still hamper rural adoption, suggesting a staggered maturation curve.

Competitive Landscape

Top Companies in Insight Engines Market

Competitive intensity is moderate. IBM, Microsoft, and Google leverage integrated stacks that bundle vector databases, model hubs, and governance consoles. IBM’s Granite 3.0 foundation models augment watsonx search with transparency scores that flag low-confidence passages. Microsoft embeds enterprise search across Teams, Outlook, and Azure OpenAI Service, creating switching costs through workflow ubiquity. Google federates Gemini with cloud-native ground-truth connectors, simplifying rollouts for multilingual corporations.

Specialist vendors carve niches via focused innovation. Elastic fuses log analytics with generative answers, courting DevSecOps buyers. Coveo pairs relevance engines with e-commerce merchandising to lift conversion rates. Sinequa’s neural ranking excels at multi-lingual industrial documentation, now reinforced by ChapsVision’s post-acquisition resources. Open-source ecosystems erode entry barriers: Weaviate, Milvus, and LlamaIndex let startups craft bespoke retrieval pipelines at lower cost, intensifying mid-market competition inside the insight engines market.

Merger and funding activity underlines strategic urgency. ServiceNow bought Raytion and, more recently, data.world to enrich its Workflow Data Fabric. OpenAI’s purchase of Rockset signals ambition to blend real-time analytics with chat interfaces. Perplexity AI leveraged a USD 500 million raise to buy Carbon, sharpening retrieval-augmented generation accuracy for consumer and enterprise users. Vendors unable to couple strong data-ingest pipelines with transparent governance risk marginalization as buyers prioritize end-to-end compliance.

Insight Engine Industry Leaders

IBM Corporation

Mindbreeze GmbH

Sinequa SAS

LucidWorks, Inc.

Coveo Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IBM and Tavily released an open-source connector that injects real-time web data into Granite models, adding citation-rich answers for market-research teams.

- May 2025: ServiceNow closed its acquisition of data.world to fortify metadata governance capabilities within the Now Platform.

- March 2025: Allen Institute for AI partnered with Google Cloud to list OLMo-series models in Vertex AI Model Garden, targeting highly regulated sectors.

- January 2025: Databricks Ventures invested in LlamaIndex to streamline knowledge-agent pipelines across enterprise data.

Global Insight Engine Market Report Scope

Insight engines are a significant improvement over search technologies that provide proactive and on-demand knowledge discovery and exploration augmented by semantic and machine learning technologies. Typical use cases of insight engines are intranet search, public search, and data extraction for analytics.

The insight engines market is segmented by component (software and services), deployment type (on-premises and cloud), size of the enterprise (small and medium-sized enterprises and large enterprises), end-user industry (BFSI, retail, and IT and telecom), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Tools / Software |

| Services |

| On-premise |

| Public Cloud |

| Private and Hybrid Cloud |

| Contextual Search |

| Conversational / NLP Search |

| Recommendation and Personalization |

| Predictive and Prescriptive Analytics |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| BFSI |

| Retail and eCommerce |

| IT and Telecom |

| Healthcare and Life Sciences |

| Manufacturing |

| Government and Public Sector |

| Media and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Tools / Software | ||

| Services | |||

| By Deployment Mode | On-premise | ||

| Public Cloud | |||

| Private and Hybrid Cloud | |||

| By Insight Type | Contextual Search | ||

| Conversational / NLP Search | |||

| Recommendation and Personalization | |||

| Predictive and Prescriptive Analytics | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By End-user Industry | BFSI | ||

| Retail and eCommerce | |||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Media and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the insight engines market?

The insight engines market is worth USD 2.85 billion in 2026 and is projected to grow to USD 8.93 billion by 2031 at a 25.66% CAGR.

Which component segment is growing the fastest?

Services are expanding at a 27.24% CAGR as enterprises seek integration, data-migration, and managed-services expertise to maximize ROI.

Why is public-cloud deployment gaining popularity?

Public-cloud options offer elastic GPU capacity, integrated security, and consumption-based pricing, helping the segment capture 57.40% share and achieve a 31.15% CAGR.

Which region is projected to grow the quickest?

Asia Pacific is forecast to post a 25.80% CAGR through 2031 as government AI strategies and expanding cloud connectivity spur adoption.

How are SMEs benefiting from insight engines?

Cloud-native, turnkey packages let SMEs deploy semantic and conversational search without heavy infrastructure, leading to the segment’s 33.00% CAGR.

What is restraining faster market expansion?

Tough privacy regulations and the complexity of integrating legacy knowledge repositories create compliance costs and lengthen deployment timelines, reducing overall CAGR by an estimated 5.9%.

Page last updated on: