Text Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.81 Billion |

| Market Size (2031) | USD 51.17 Billion |

| Growth Rate (2026 - 2031) | 22.16% CAGR |

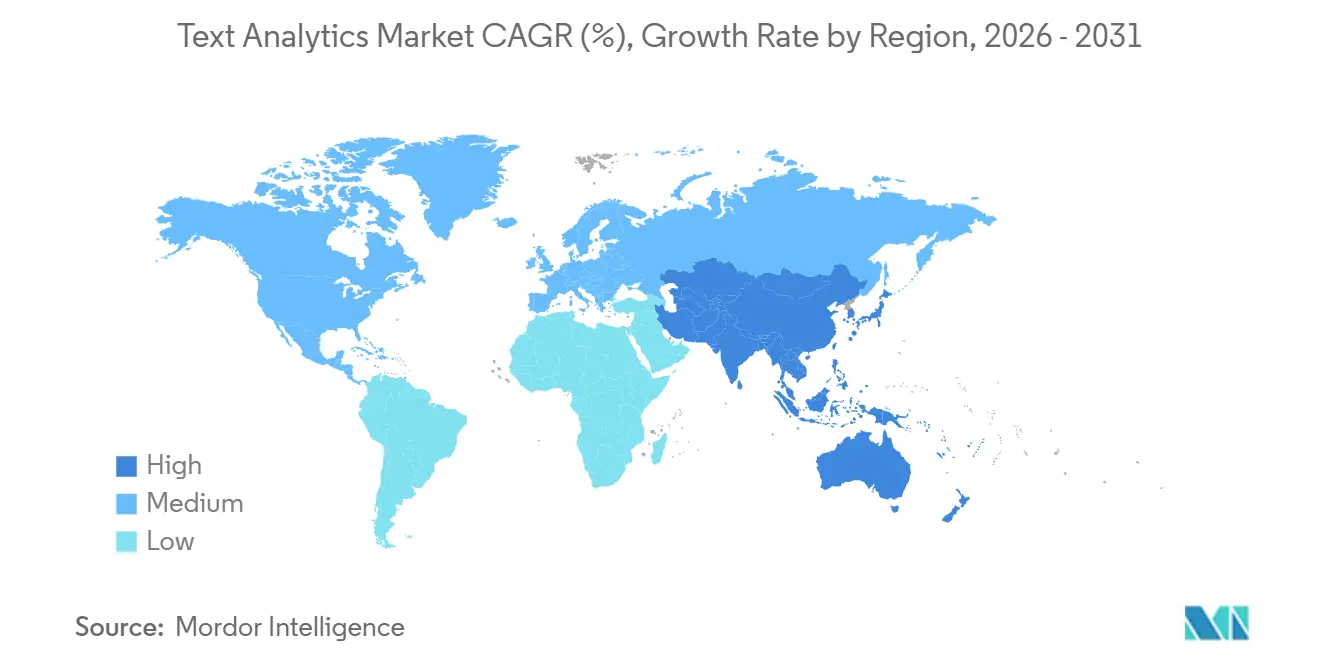

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

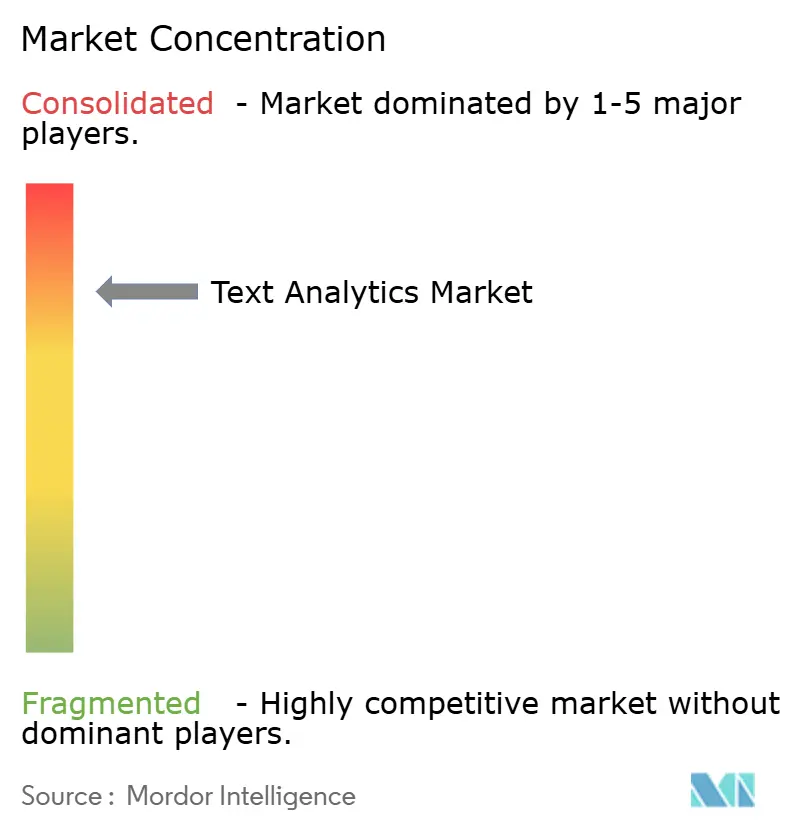

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Text Analytics Market Analysis by Mordor Intelligence

The text analytics market reached USD 18.81 billion in 2026 and is forecast to climb to USD 51.17 billion by 2031, advancing at a 22.16% CAGR during 2026-2031. This rapid expansion reflects enterprises’ growing determination to unlock insight from unstructured text that traditional business-intelligence tools cannot parse. Real-time sentiment engines now adjust prices mid-transaction, route support tickets, and flag compliance risks in milliseconds, slashing time-to-action for customer and risk teams. Regulatory mandates for environmental, social, and governance (ESG) disclosures compel firms to extract emissions, labor, and diversity metrics from thousands of pages of filings, driving broad adoption of natural-language pipelines. Cloud vendors have bundled text analytics into AI platforms, pushing down per-document costs even as model sophistication rises. At the same time, enterprises face sharper scrutiny of energy use; training a single 175-billion-parameter language model consumes the annual electricity of 120 U.S. homes, sparking demand for distilled, energy-efficient architectures.

Key Report Takeaways

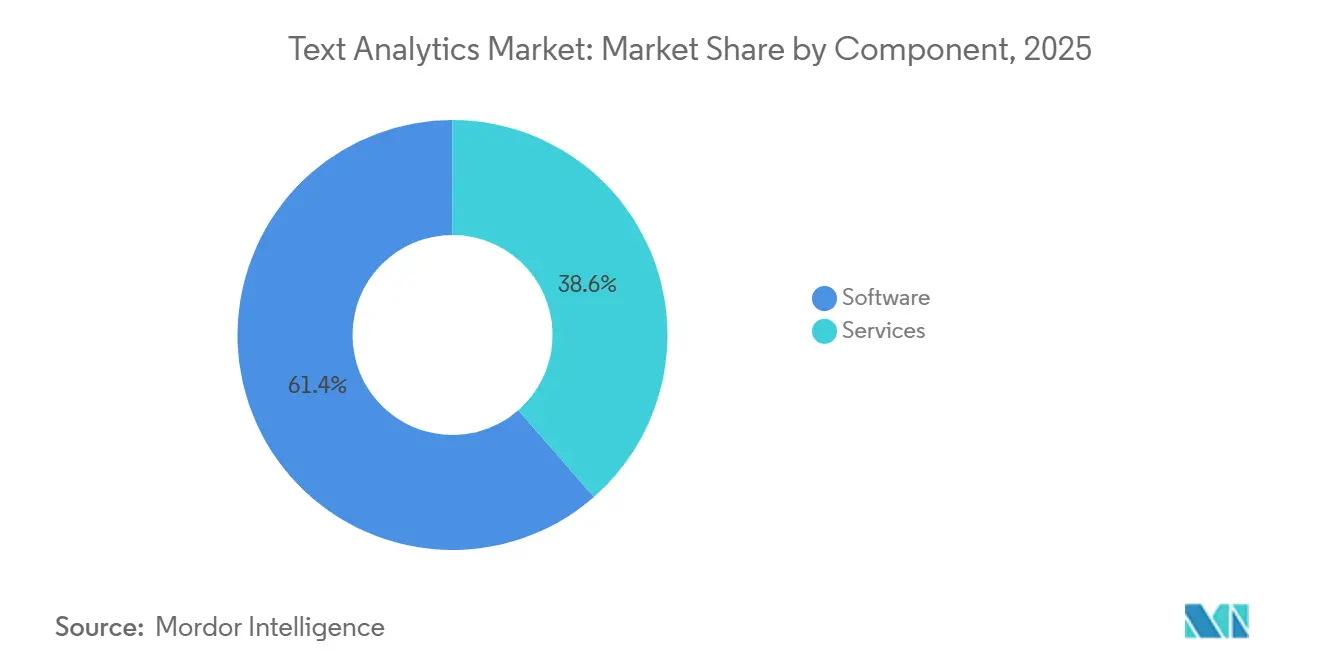

- By component, software held 61.43% of the text analytics market share in 2025; services are projected to grow at a 23.06% CAGR through 2031.

- By deployment model, on-premises installations commanded 59.89% share of the text analytics market size in 2025, while cloud is advancing at a 22.99% CAGR to 2031.

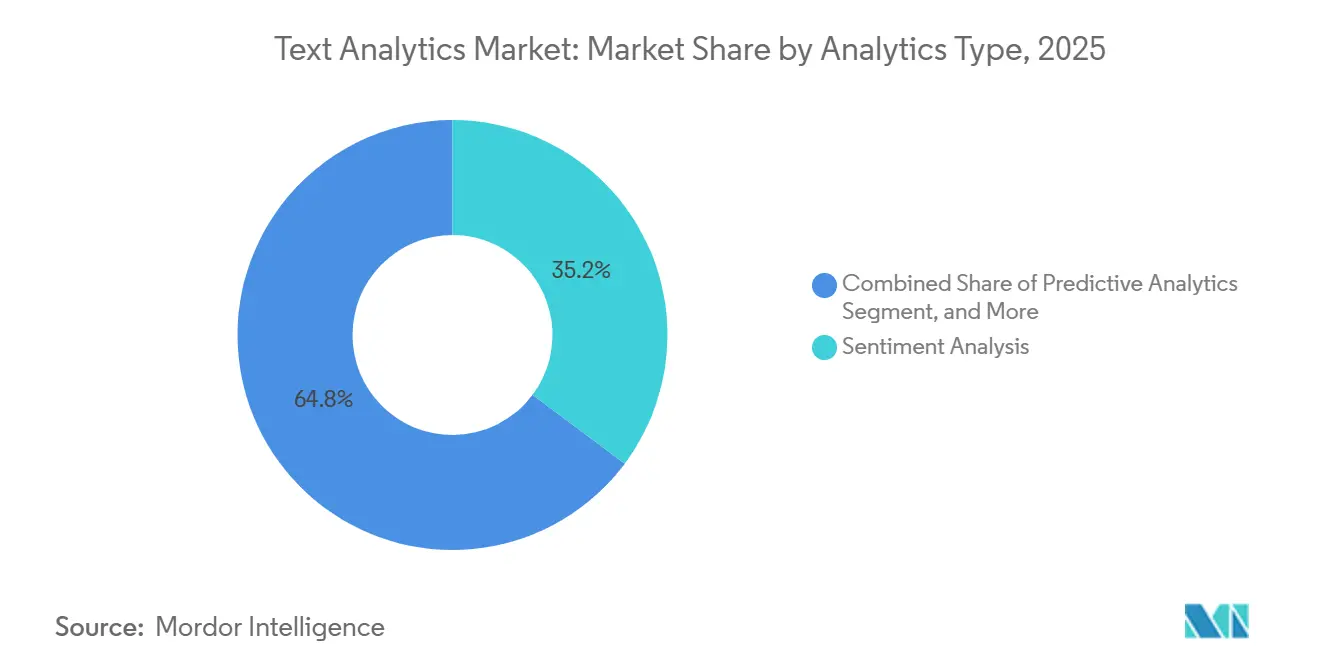

- By analytics type, sentiment analysis led with 35.21% revenue share in 2025; generative-AI-enhanced text analytics are forecast to post a 24.23% CAGR through 2031.

- By application, customer experience management captured 29.72% of 2025 revenue, whereas social media analysis is set to expand at a 24.76% CAGR during 2026-2031.

- By end-user industry, retail generated 27.88% of revenue in 2025, while healthcare adoption is projected to rise at a 22.16% CAGR to 2031.

- By enterprise size, large companies accounted for 66.54% share in 2025, yet small and medium enterprises (SMEs) are expected to grow at a 22.86% CAGR through 2031.

- By geography, North America held 42.33% share in 2025, although Asia-Pacific is forecast to surge at a 23.57% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Text Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Social Media Analytics | +3.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Predictive Analytics for Customer Insights | +3.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Proliferation of Unstructured Text Data Across Enterprises | +4.2% | Global | Long term (≥ 4 years) |

| Integration of Large Language Models into Enterprise Text Analytics | +5.1% | North America, Europe, and Asia-Pacific core markets | Short term (≤ 2 years) |

| Expansion of Real-Time Text Analytics in Edge IoT Devices | +2.9% | Asia-Pacific and North America, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Regulatory Mandates for ESG Disclosure Requiring Textual Data Parsing | +2.7% | Europe and North America, with emerging adoption in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration of Large Language Models into Enterprise Text Analytics

Enterprises plugged large language models (LLMs) into production workflows to automate clause extraction, nuance detection, and conversational summarization. Microsoft’s 2025 release of GPT-4 inside Azure AI Language cut labeled-data requirements by 40% compared with prior transformers, trimming annotation budgets for procurement and legal teams.[1]Microsoft Corporation, “Azure AI Language Services Updates,” microsoft.com Oracle added generative document understanding to its cloud stack, letting customers surface payment terms and liability caps across thousands of contracts in minutes.[2]Oracle Corporation, “Oracle Cloud Infrastructure AI Services,” oracle.com These gains arrive with bias and hallucination risks, so organizations increasingly deploy human-in-the-loop validation layers. Despite mitigation costs, the economic upside is significant; McKinsey estimates generative AI could unlock USD 2.6-4.4 trillion in annual value across functions.

Proliferation of Unstructured Text Data Across Enterprises

Customer reviews, help-desk notes, safety logs, and regulatory filings pour into corporate repositories faster than manual teams can read them. A mid-2025 LinkedIn survey found that enterprises stored 55% more unstructured text than in 2024, exceeding structured-data growth by a factor of four. This flood makes automated parsing a necessity rather than an optimization. Vendors now bundle pre-trained entity catalogs for domains such as life sciences and oil and gas, accelerating time-to-benefit for specialized users. However, as vocabularies evolve, models face drift, reinforcing demand for continuous retraining services.

Growing Demand for Social Media Analytics

Brand-reputation teams moved from weekly sentiment snapshots to minute-by-minute monitoring. Sixty-three percent of consumers expect a social-media response within one hour, a benchmark impossible without automated classification. Retailers track TikTok trends during product drops, while banks use natural-language filters to spot insider-trading hints on Reddit, complying with FINRA retention rules. Dialect shifts, sarcasm, and emoji semantics once confounded rule-based approaches, but fine-tuned transformers now achieve 85% detection accuracy in controlled tests, narrowing the gap to human moderators.

Rising Adoption of Predictive Analytics for Customer Insights

Firms extend text analytics from retrospective sentiment scoring toward forward-looking churn and cross-sell models. By fusing email threads, chat logs, and purchase histories, telecom operators raised churn-prediction recall by 12 points in 2025 pilots, improving retention campaign ROI. Insurance carriers extract intent signals from claim narratives to pre-empt fraudulent submissions. Wider use hinges on explainability; regulators increasingly demand rationales for automated denials, steering vendors to embed attention-highlight visualizations and model scorecards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Skilled Personnel and Awareness | -2.1% | Global, with acute shortages in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Data Privacy and Compliance Concerns | -3.2% | Europe and North America, with emerging scrutiny in Asia-Pacific | Short term (≤ 2 years) |

| High Carbon Footprint of Deep-Learning Text Analytics Workloads | -1.8% | Global, with regulatory pressure in Europe | Medium term (2-4 years) |

| Increasing Cost of High-Quality Multilingual Training Data | -1.6% | Global, with acute impact in low-resource language markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Compliance Concerns

Fragmented data-protection regimes create compliance silos. The EU GDPR authorizes fines up to 4% of global revenue; Meta paid EUR 1.2 billion (USD 1.3 billion) in 2023 for unlawful transfers, while TikTok incurred EUR 345 million (USD 378 million) for child-data lapses, raising executive sensitivity to textual-data flows. California’s 2023 Consumer Privacy amendments grant residents the right to opt out of automated decision-making, forcing dual pipelines for opted-in and opted-out records.[3]State of California Department of Justice, “California Consumer Privacy Act,” oag.ca.gov The EU AI Act classifies sentiment and emotion recognition as high risk, layering conformity assessments onto deployment timelines. Compliance costs land heaviest on SMEs that lack in-house counsel, motivating uptake of audit-ready SaaS platforms.

High Carbon Footprint of Deep-Learning Text Analytics Workloads

Training a 175-billion-parameter LLM emits about 552 t of CO₂e, comparable to five gasoline cars over their life cycle. Data centers already consume 1-1.5% of global electricity, with AI training the fastest-growing slice. Enterprises respond by shifting compute to renewable grids in Iceland and Quebec and by adopting distillation techniques that shrink parameters 90% while retaining 95% accuracy. The EU Energy Efficiency Directive now obliges data centers to disclose energy use, pushing CIOs to weigh carbon budgets alongside compute budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Model Complexity Rises

Services claimed 23.06% CAGR potential, outstripping software growth as organizations grapple with model drift and domain fine-tuning. In 2025, software still held 61.43% of text analytics market share, spanning NLP engines, sentiment scorers, and pretrained transformers. Yet rising linguistic variation and regulatory audits make continuous retraining a must, steering budgets toward managed services and annotation outsourcing.

Vendors respond with outcome-based contracts, cost per extracted entity, or per summarized page, that cap risk for buyers. However, proprietary schemas can lock enterprises into a single provider, prompting calls for open-source formats. For software vendors, bundling low-cost APIs with premium consulting offers a hedge against margin squeeze.

By Deployment Model: Cloud Adoption Accelerates Despite Sovereignty Concerns

On-premises installations controlled 59.89% of 2025 spend, yet the cloud slice is growing at a 22.99% CAGR as hybrid patterns mature. A 2025 preliminary study calculated that shifting to the cloud cut the total cost of ownership 40-50% by eliminating hardware refresh and granting instant access to updated models. Cloud deployments are projected to overtake on-premises deployments by 2029 if current momentum holds.

Hybrid designs anonymize text in public clouds while retaining personally identifiable information on-premises, appeasing bankers and hospitals that fear data-residency breaches. The EU Data Act bolsters portability rights, forcing providers to support open export formats and sparking a race for interoperability. Edge deployments, though niche, enable factory gateways and autonomous vehicles to parse logs offline, cutting latency. The primary hurdle is model sync; rural facilities may update only monthly, letting drift accumulate.

By Analytics Type: Generative AI Disrupts Traditional Sentiment Scoring

Sentiment analysis delivered 35.21% revenue share in 2025, yet generative AI segments are forecast for 24.23% CAGR, the fastest in the landscape. Platforms now bundle summarization, synthetic-data creation, and response drafting in a single pipeline, giving users cross-functional insight with minimal integration overhead. The text analytics market size for generative workflows is expected to double by 2028, fueled by retrieval-augmented generation that grounds outputs in proprietary data.

Predictive analytics keeps traction in fraud and churn, while speech analytics expands as businesses mine contact-center calls. Vendors face a balancing act—larger models boost accuracy but swell compute bills and carbon footprints. Explainability remains a gating factor; black-box decisions risk non-compliance under emergent AI transparency laws, spurring adoption of saliency-map visualizers.

By Application: Social Media Analysis Outpaces Traditional Use Cases

Customer experience management dominated 29.72% of 2025 revenue, but social media analysis is set to accelerate at 24.76% CAGR, moving the text analytics market toward real-time, event-driven workflows. Brands rely on TikTok and WeChat monitors during product launches to pre-empt sentiment dips. Risk-management use cases broaden as banks parse filings and news to quantify geopolitical shocks. Fraud teams integrate narrative anomaly detection to flag synthetic identities earlier than rules can.

Business-intelligence dashboards increasingly embed natural-language queries, letting executives interrogate earnings-call transcripts without SQL. Governance and compliance modules auto-track regulatory changes, pulling citations into audit trails overnight. The hurdle is context preservation; hallucinated summaries can mislead boards, underscoring the need for human review checkpoints.

By End-User Industry: Healthcare Adoption Accelerates Under Value-Based Care

Retail generated 27.88% of 2025 revenue through review mining and dynamic pricing. Healthcare’s 22.16% CAGR arises from clinical-documentation improvement and patient-sentiment tracking, now tied to reimbursement under value-based contracts. Hospitals deploy NLP to surface adverse drug events from physician notes, cutting manual chart review time. Financial services lean on contract analytics for credit and compliance, while energy operators parse maintenance logs to predict failures.

Government and defense agencies apply text analytics to intelligence fusion and citizen-query bots, though data-classification rules slow cloud migration. IT and telecom providers embed NLP in network operations for outage diagnostics. Manufacturers employ document clustering for quality audits. Each sector inherits its own regulatory overlay from HIPAA to anti-money-laundering shaping deployment choices.

By Enterprise Size: SMEs Embrace SaaS to Bypass Infrastructure Costs

Large enterprises retained 66.54% share in 2025, leveraging bespoke model training on private clusters. Yet SMEs are growing at 22.86% CAGR as pay-as-you-go SaaS slashes upfront spend. A small retailer can launch sentiment analysis for USD 500 per month rather than USD 50,000 for on-premises hardware. However, generic models often falter on niche jargon, pushing SMEs toward managed services that bundle fine-tuning.

Hyperscalers court SMEs with low-cost APIs, while specialist vendors focus on vertical depth. Talent scarcity weighs heavier on smaller firms; 72% cite recruiting data scientists as a barrier, versus 48% of large enterprises. Outcome-based managed services bridge the gap but raise lock-in risk.

Geography Analysis

North America accounted for 42.33% of global revenue in 2025, anchored by early adoption across tech, finance, and retail. Vendors in the region bundle text analytics into wider AI portfolios, driving down per-document pricing. Regulatory headwinds, notably the California privacy amendments, spark investment in explainability toolkits.

Asia-Pacific is projected to post a 23.57% CAGR, the fastest worldwide. China’s 2025 guidelines promoted sovereign LLMs for industry and government, mandating domestic hosting and splintering the global model ecosystem. Japan’s Digital Agency digitizes municipal services, spawning demand for Japanese-language chatbots, while India’s IT services giants export multilingual analytics covering Hindi, Tamil, and Bengali. The text analytics market size in Asia-Pacific is poised to exceed USD 15 billion by 2031 if growth holds.

Europe shows steady uptake, driven by ESG-reporting mandates that require textual data parsing. The EU AI Act introduces conformity assessments, raising entry barriers but fueling demand for compliant, explainable platforms. South America’s market remains nascent, hampered by cloud-infrastructure gaps and currency volatility. In the Middle East and Africa, sovereign wealth funds in the United Arab Emirates and Saudi Arabia bankroll smart-city projects that embed NLP into citizen-service portals.

Regulatory Landscape

Text analytics deployments are increasingly managed within AI governance regimes focused on transparency, documentation, and data controls. In the European Union, Regulation (EU) 2024/1689 (AI Act) defines harmonized AI rules, with full application beginning August 2, 2026. Its technical documentation and transparency obligations (including Annex IV and Annex XI) heighten expectations for data provenance, methodology description, performance evaluation, and human oversight, particularly for in-scope systems such as sentiment and emotion recognition classified as high risk.

In the United States, the 2026 policy direction emphasized risk management and benchmarking without creating blanket preclearance for model releases. A June 5, 2026 Executive Order directed the Secretary of Commerce, via NIST and partner agencies, to develop a classified benchmarking process for frontier AI models within 60 days, while explicitly rejecting mandatory licensing or preclearance for developing, publishing, or releasing new AI models. Many enterprises reference NISTs AI Risk Management Framework (AI RMF) and its Govern, Map, Measure, and Manage functions as a practical control set for text analytics in regulated environments.

Value Chain Analysis

The text analytics value chain covers (1) data sourcing and rights management (enterprise documents, contact center transcripts, social and web content, regulatory filings), (2) data engineering and governance (collection, labeling, de-identification, retention, lineage), (3) model and pipeline development (embeddings, classifiers, retrieval-augmented generation, evaluation and red-teaming), (4) deployment and operations (cloud, on-premises, and edge runtime, monitoring for drift and hallucinations), and (5) application-layer integration into business workflows (customer experience management, fraud and risk management, governance and compliance, and sector-specific use cases). Hyperscalers and major software vendors increasingly bundle capabilities across multiple layers, including storage, vector search, model hosting, and APIs, while specialist firms differentiate through domain corpora, multilingual coverage, and explainability toolkits that reduce validation effort in audits.

Compute availability and data sovereignty have become more visible upstream constraints, with infrastructure choices shaping downstream product design. In Europe, sovereign infrastructure initiatives such as T-Systems Industrial AI Cloud (operating since February 2026 in Munich) show how large-scale GPU capacity is being positioned to keep sensitive text and model operations within regional control boundaries. On the services side, systems integrators and managed-service providers bridge platforms and end users by handling continuous retraining, human-in-the-loop review, and compliance documentation, which become more central as organizations expand from pilot sentiment scoring to regulated, production workflows.

Competitive Landscape

The top 10 vendors captured roughly 55% of 2025 revenue, indicating moderate concentration. Hyperscalers Microsoft, Amazon Web Services, Google, and Oracle bundle NLP APIs into broader AI clouds, leveraging scale to cut unit costs, but compressing margins for pure-play vendors. Specialists differentiate with vertical-specific models: legal discovery engines trained on millions of contracts, clinical NLP attuned to ICD-10 codes, and finance models that tag earnings-call sentiment. Open-source challengers such as LLaMA and Mistral offer lower cost and data sovereignty, though they demand fine-tuning expertise beyond many SMEs.

White-space opportunities surface in low-resource languages, edge deployment, and explainability tooling. Providers building Swahili or Vietnamese corpora can unlock underserved regions. Edge-optimized models running in industrial gateways satisfy latency constraints in manufacturing and autonomous fleets. Explainability layers that highlight word-level contributions meet EU transparency rules and reassure auditors. Patent activity underscores competitive tempo; the United States Patent and Trademark Office issued 1,847 NLP patents in 2025, up 23% year on year, with claims spanning multilingual embeddings and federated learning. Standards bodies, including IEEE and ISO, launched working groups on evaluation metrics, but consensus remains years away.

Text Analytics Industry Leaders

SAP SE

IBM Corporation

SAS Institute Inc.

Microsoft Corporation

Clarabridge Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operational, in-workflow text analytics is moving beyond dashboards into embedded decision loops, creating room for vendors focused on low-latency and governed deployments. Deutsche Telekoms July 2026 deployment of the Magenta AI Call Assistant is a concrete example, as it parses calls in real time, translates languages, and generates summaries within the network. This in-line capability supports opportunities for vendors delivering edge or in-network text processing with privacy controls, measurable latency, and audit-ready oversight, particularly for telecom, customer care, and regulated contact-center environments.

Agentic and retrieval-centric architectures also widen the addressable use case set by reducing the integration burden for multi-step tasks such as content review, contract analysis, and investigative workflows. In 2026, Teradata launched agentic and multi-modal capabilities for its Enterprise Vector Store, MongoDB announced generally available hybrid search and native reranking for enterprise retrieval, and Veeva acquired Copli while launching Veeva Falcon MLR for medical, legal, and regulatory content review, all indicating stronger enterprise packaging around governed retrieval and task automation. At the analytics consumption layer, Google Cloud made Conversational Analytics in BigQuery generally available in July 2026, reinforcing demand for natural-language querying and multi-step analysis experiences that can be audited and controlled. Together, these shifts sharpen opportunities for providers that combine retrieval accuracy, explainability layers, and deployment flexibility (hybrid and sovereign options) aligned to evolving EU AI Act documentation expectations and broader AI risk management practices.

Recent Industry Developments

- March 2026: IBM announced IBM SQL Data Insights Pro for Db2 for z/OS, enabling analysis of structured data alongside unstructured text without moving data off the platform, with general availability set for March 20, 2026. The release supports in-place text analytics for industries that keep data on mainframes for security and residency reasons, reducing integration friction for governed NLP use cases.

- December 2025: SAP published SAP HANA Cloud 2025 Q4 updates that included text embedding model enhancements aimed at reducing vector dimensionality and added automated log text analysis capabilities. These updates reinforce the database-layer foundation for enterprise search and observability use cases that depend on embeddings and scalable text processing close to governed data.

- October 2024: SAP delivered SAP SuccessFactors 2H 2024 updates that introduced a text analyzer feature for AI-assisted writing, bias detection, and content translation. Embedding text analytics features into a core HCM suite increases day-to-day enterprise exposure to NLP capabilities and raises demand for compliant language processing across HR content workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the text analytics market is defined as revenue earned from software and related services that convert unstructured text (documents, emails, chats, social posts, and notes) into searchable insights using techniques such as NLP, classification, and sentiment analysis.

The scope excludes general-purpose translation, basic keyword search tools that do not run analytics, and custom in-house analytics work that is not sold as a product or service.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Model

- On-premise

- Cloud

- By Analytics Type

- Sentiment Analysis

- Predictive Analytics

- Speech Analytics

- Other Analytics Types

- By Application

- Risk Management

- Fraud Management

- Business Intelligence

- Social Media Analysis

- Customer Care Services

- Governance, Risk and Compliance Management

- Other Applications

- By End-User Industry

- BFSI

- Healthcare

- Energy and Utilities

- Retail and E-commerce

- Government and Defense

- IT and Telecom

- Other End-User Industries

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Oceania

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, map the value chain, and build the first pass of demand signals by region and industry. We relied on non-paywalled sources such as the US Census Bureau, the US Bureau of Labor Statistics, Eurostat, the OECD, and World Bank digital economy indicators to anchor macro assumptions that shape software and services spend.

To keep the model grounded in how spend is actually positioned, we also reviewed public company filings, earnings transcripts, product documentation, security and privacy guidance published by regulators, association websites, and reputable press coverage of analytics and AI adoption. In a few places, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to cross-check revenue exposure, product positioning, and innovation intensity. These examples are illustrative only, and many other sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being purchased and deployed, and on testing pricing and adoption assumptions that are hard to see in public sources. We spoke with a mix of solution providers, implementation partners, and enterprise users across APAC, EMEA, and the Americas, so differences in cloud maturity, regulation, and language coverage could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 16% | Managers: 54% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing was built using a top-down approach where enterprise software and analytics spend pools were reconstructed by region, then filtered through text analytics penetration, typical deployment mix, and industry adoption intensity. To keep the totals realistic, we also corroborated the outcome with selective bottom-up approximations, such as sampling vendor-reported revenue exposure, partner channel checks, and an ASP x user or document-volume logic for common use cases.

Key inputs included cloud versus on-prem deployment share, average contract values by enterprise size, the share of customer experience and risk workflows that embed text analytics, and the pace of AI feature bundling that changes how much is paid for a standalone tool. Language coverage requirements and regulated-industry adoption patterns were treated as practical market fingerprints, because they influence implementation effort and service attachment.

For forecasting, scenario analysis was used with a base case shaped by primary feedback on budget cycles and renewal behavior, then followed by sensitivity checks on cloud migration speed and service intensity. Where bottom-up inputs were missing for smaller geographies, gaps were handled by applying region-specific adoption ratios, and then re-checking against observed IT spending direction and interview feedback before finalizing.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as enterprise software spending direction, cloud adoption indicators, and the observed mix of software versus services implied by implementation complexity. Large variances by region or vertical were flagged, reviewed by another analyst, and then traced back to specific drivers, such as penetration rates, pricing bands, or deployment mix assumptions.

If a major change is spotted, such as a pricing shift due to bundling, a regulatory move affecting data handling, or a step-change in adoption, we re-contact relevant participants and adjust the assumptions in the model. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery review pass is done so clients receive the latest updated view.

Mordor Intelligence's Text Analytics Market Size Versus Other Published Estimates

Published market values for text analytics can look far apart because teams do not always count the same revenue lines, and they often anchor on different base years and adoption speeds. The table helps show the spread clearly before reviewing what drives it.

The table shows a higher 2026 value on our side versus the other two figures, and in Mordor Intelligence's model the market includes both software and associated implementation and support services tied to text analytics deployments, rather than limiting the count to software-only revenue or narrower use cases.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.81 B (2026) | |

| Regional Consultancy A | USD 9.22 B (2024) | Uses an earlier base year, and its disclosed scope leans toward technology and application views that can undercount service-heavy deployments and multi-year implementation revenue recognized outside software subscriptions. |

| Industry Publisher B | USD 12.10 B (2026) | Reports a lower 2026 estimate that can come from tighter inclusion of what qualifies as text analytics revenue, plus more conservative assumptions on cloud migration speed and how quickly advanced features translate into paid contracts. |

Looking across the three numbers, most of the difference is explained by year alignment and what is counted as part of a text analytics purchase, especially services and bundled functionality. By tying the estimate to clear spend pools, practical adoption ratios, and interview-checked pricing and deployment mix, the resulting value is easier to follow and to recreate when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the text analytics market?

The text analytics market was valued at USD 18.81 billion in 2026.

How fast is global demand for text analytics growing?

The market is projected to register a 22.16% CAGR between 2026 and 2031.

Which analytics type is expanding most quickly?

Generative-AI-enhanced text analytics are forecast to grow at a 24.23% CAGR through 2031.

Why is Asia Pacific attracting investment in text analytics?

Government AI initiatives in China, Japan’s municipal digitization, and India’s IT-services exports are driving a 23.57% regional CAGR.

What are the main barriers to adoption?

Data-privacy compliance, carbon footprint concerns, talent shortages, and high multilingual training costs constrain uptake.

Which vendors dominate the competitive landscape?

Microsoft, Amazon Web Services, Google, Oracle, and IBM lead, but specialized providers hold niches in healthcare, legal, and finance.

Page last updated on: