Inositol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 414.98 Million |

| Market Size (2031) | USD 643.99 Million |

| Growth Rate (2026 - 2031) | 9.19% CAGR |

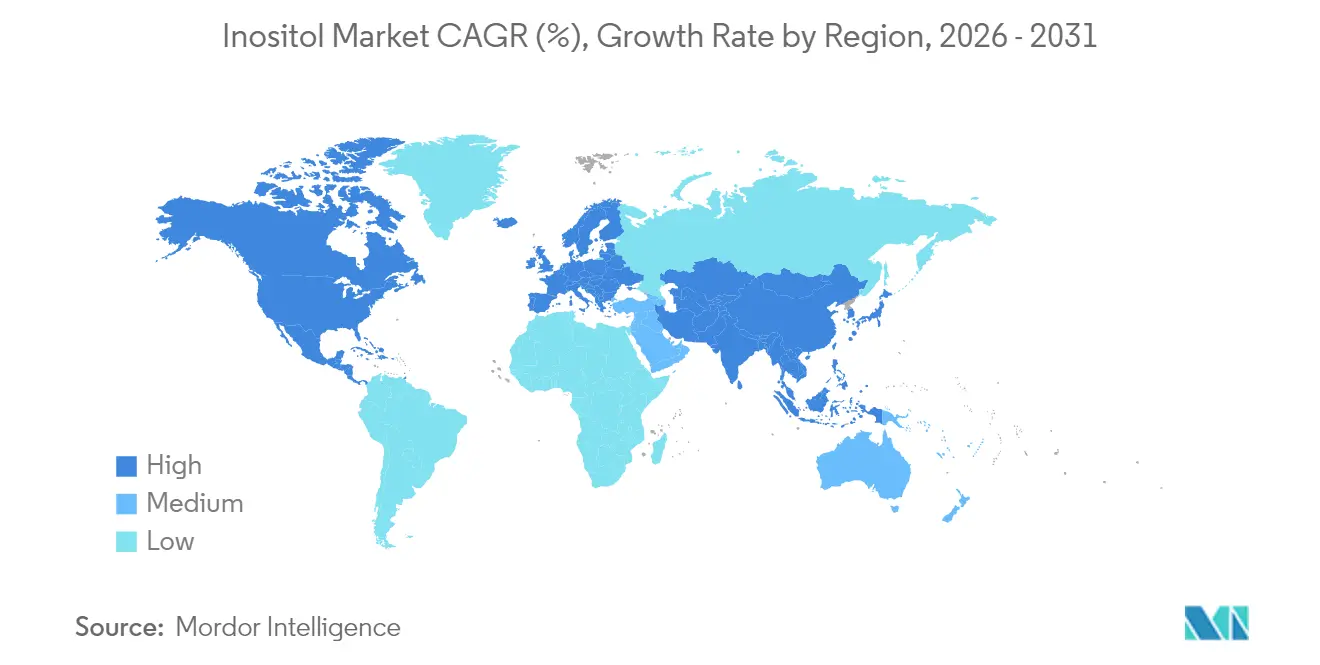

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

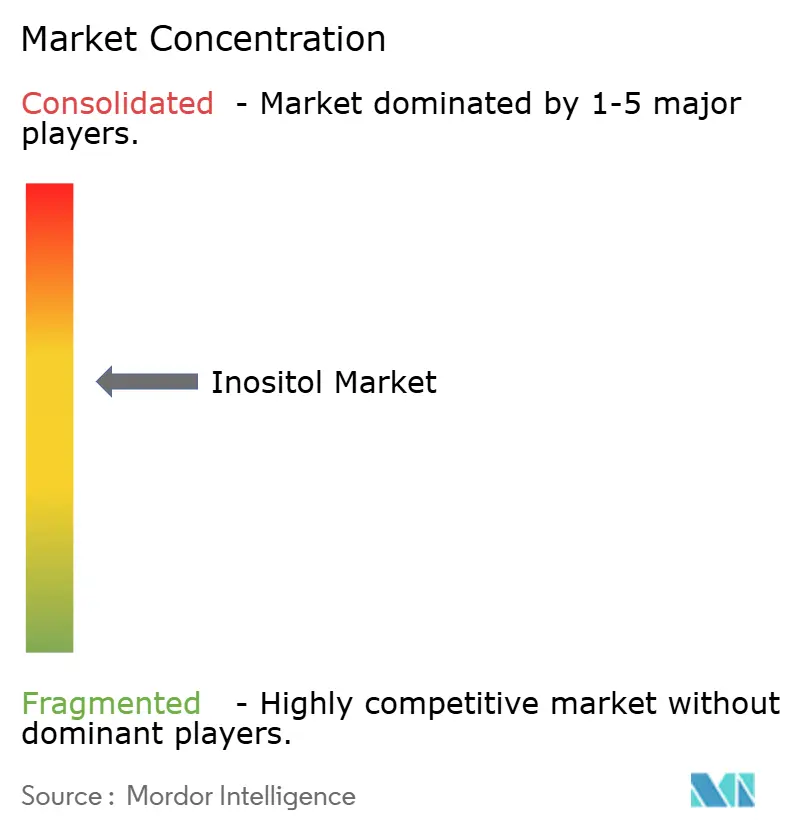

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Inositol Market Analysis by Mordor Intelligence

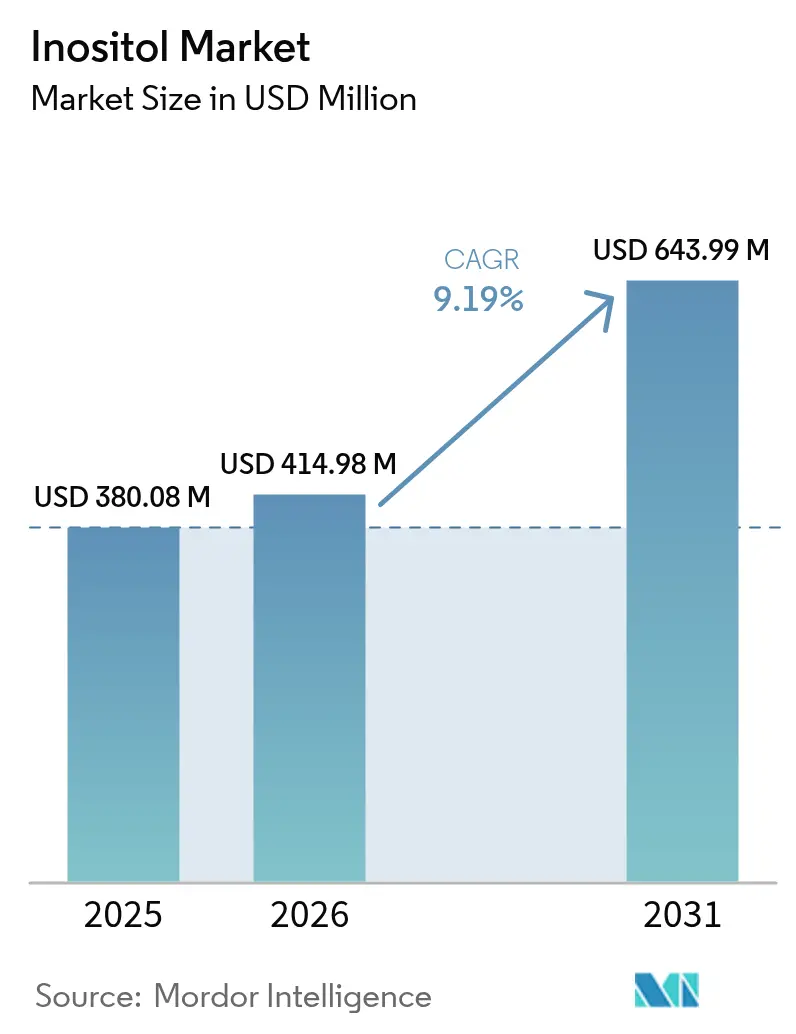

The inositol market size is expected to grow from USD 380.08 million in 2025 to USD 414.98 million in 2026 and is forecast to reach USD 643.99 million by 2031 at 9.19% CAGR over 2026-2031. The market growth is driven by increasing clinical evidence supporting its role in women's health, growing use in infant nutrition formulations, and consistent demand from the monogastric animal feed industry. These factors generate steady demand across pharmaceutical, nutraceutical, food, and feed segments. The compound's established effectiveness in treating polycystic ovary syndrome (PCOS) maintains premium pricing, while improved fermentation efficiency reduces production costs. The Asia-Pacific region, with its integrated corn, rice, and fermentation infrastructure, remains a major exporter and consumer, particularly in animal feed and dietary supplements. Regulatory approvals in the United States and the European Union expand market applications. The increase in corn prices by 2025 is prompting manufacturers to diversify their raw material sources, such as incorporating rice bran, highlighting the importance of effective supply chain management.

Key Report Takeaways

- By source, plant-based inositol captured 61.72% of the inositol market share in 2025, while synthetic variants are forecast to expand at a 9.88% CAGR through 2031.

- By type, myo-inositol dominated with an 79.56% revenue share in 2025; D-chiro-inositol is projected to grow at an 11.28% CAGR between 2026 and 2031.

- By application, dietary supplements led with 37.12% revenue share in 2025, whereas food and beverage applications are poised for an 10.95% CAGR to 2031.

- By geography, Asia-Pacific held 43.74% of the 2025 revenue base, yet South America is on track for the fastest 9.76% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inositol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing inclusion in infant formula and functional foods due to inositol's role in cognitive and metabolic support | +2.1% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of Asia-Pacific monogastric feed industry | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Rising PCOS and fertility issues boost demand for inositol for its insulin-sensitizing effects | +2.4% | Global, with concentrated demand in developed markets | Short term (≤ 2 years) |

| Expanding mental health and cognitive wellness segment | +1.3% | North America and Europe primarily, expanding to Asia-Pacific | Medium term (2-4 years) |

| Preference for plant-derived, clean-label ingredients drives demand for inositol | +1.1% | Global, led by North America and Europe consumer preferences | Medium term (2-4 years) |

| Cost-down of fermentation-based synthetic inositol | +0.9% | Global manufacturing hubs, particularly Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing inclusion in infant formula and functional foods due to inositol's role in cognitive and metabolic support

The global inositol market is growing due to its increased use in infant formula and functional foods. Inositol plays a significant role in neural development, memory formation, and metabolic programming during early life. The compound functions in phospholipids and insulin signaling pathways, supporting brain development and glucose metabolism. These findings drive inositol's expansion in food and nutrition products. The U.S. FDA's GRAS designation permits inositol use in infant formula at 4-40 mg per 100 kcal, establishing clear guidelines for manufacturers. The European Food Safety Authority (EFSA) has also confirmed inositol's safety, implementing conservative dosing guidelines. These approvals validate the compound's safety and encourage its adoption by major infant formula manufacturers. Consumer preferences indicate strong market potential for inositol products. According to Glanbia Nutritionals' 2023 data, 25% of German consumers preferred functional beverages targeting cognitive health, while 19% favored products aimed at supporting digestive wellness [1]Source: Glanbia Nutritionals, "European Functional Beverage Market Insights for 2023," glanbianutritionals.com. The DSM 2023 survey indicates parents prioritize infant formulas with immune health benefits (30%), balanced nutrition (33%), and digestive gentleness (16%) [2]Source: DSM-Firmenich, "Ask-the-Expert: What do Moms Really Want from Nutritional Products for their Children," dsm-firmenich.com. These preferences create opportunities for manufacturers to incorporate inositol into their products.

Expansion of Asia-Pacific monogastric feed industry

The Asia-Pacific monogastric feed market drives significant demand for inositol, supported by annual poultry production growth of 4-5% and increasing aquaculture intensity. The region recorded a 2.5% increase in feed production capacity in 2024 compared to 2023, with China maintaining its position as the primary producer and consumer. Inositol supplementation in monogastric nutrition improves feed conversion ratios and reduces oxidative stress in intensive production systems. The compound works synergistically with phytase enzymes to improve phosphorus utilization, addressing nutritional efficiency and environmental concerns. Feed manufacturers in the region implement phytase superdosing strategies to release inositol from phytate complexes, reducing supplementation costs while maintaining dietary benefits. This approach demonstrates the market's understanding of enzyme-substrate interactions and cost optimization, vital during periods of high corn prices and increased use of alternative feed ingredients.

Rising PCOS and fertility issues boost demand for inositol for its insulin-sensitizing effects

The increasing prevalence of polycystic ovary syndrome (PCOS) and associated fertility issues has become a significant growth driver for the global inositol market. PCOS, characterized by insulin resistance, hormonal imbalance, and anovulation, directly affects reproductive health. The two main forms of inositol, myo-inositol and D-chiro-inositol, demonstrate insulin-sensitizing properties that enhance glucose uptake, regulate ovarian function, and promote ovulation. The growing recognition of these benefits among healthcare providers and consumers has increased the adoption of inositol supplementation, stimulating growth in both nutraceutical and pharmaceutical segments. Global fertility rates continue to decline, highlighting the need for effective reproductive health solutions. According to the CIA report, Taiwan reported the world's lowest fertility rate in 2024, at 1.11 children per woman, exemplifying the demographic challenges prevalent across Asia-Pacific and other regions [3]Source: CIA, "Total fertility rate," cia.gov. This demographic shift has increased interest in fertility enhancement and adoption of inositol supplementation, particularly for PCOS, which represents a significant share of female infertility cases, thereby stimulating market growth. In this context, inositol has emerged as an evidence-based ingredient that addresses both the metabolic and reproductive aspects of infertility.

Expanding mental health and cognitive wellness segment

The mental health applications of inositol continue to expand as research demonstrates its effectiveness in treating panic disorder, depression, and obsessive-compulsive disorder. Inositol functions as a precursor to phosphatidylinositol and plays a role in serotonin receptor signaling, providing a scientific basis for its use in neuropsychiatric treatments. Clinical studies shows that psychiatric conditions require therapeutic doses of 12-18 grams daily, which is higher than standard nutritional supplement doses, creating distinct market categories with separate regulatory requirements and price points. The growing focus on cognitive wellness, especially among older populations, increases the demand for lower-dose inositol formulations that target general brain health maintenance. The supplement's strong safety record and minimal drug interactions make it an attractive alternative to synthetic cognitive enhancers. While clinical evidence strongly supports inositol's use for specific psychiatric conditions, its application for general cognitive enhancement, though growing in popularity due to consumer preference for natural alternatives, has less extensive research backing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile corn/phytic-acid raw-material prices | -1.4% | Global, with acute impact on Asian manufacturing hubs | Short term (≤ 2 years) |

| Availability of substitute ingredients | -0.8% | Global, particularly in cost-sensitive applications | Medium term (2-4 years) |

| Limited penetration in emerging markets | -0.6% | Emerging markets in Africa, Latin America, Southeast Asia | Long term (≥ 4 years) |

| Stringent purity and pharma-grade regulatory hurdles | -1.1% | Global, with varying intensity by regulatory jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile corn/phytic-acid raw-material prices

The volatility in corn starch prices in 2025 affects inositol production costs, as corn remains the primary feedstock for both extraction and fermentation-based production methods. Manufacturers face margin pressures when they cannot transfer increased costs to price-sensitive segments, particularly the animal feed sector. The market faces additional constraints from competing corn demands, including ethanol production, food applications, and export requirements. In response, manufacturers are expanding their feedstock options to include rice bran and wheat bran, though these materials require modified processing methods and generate different impurity profiles that impact purification costs. While phytic acid extraction from rice bran provides cost benefits during periods of high corn prices, its supply chain reliability remains lower compared to established corn processing systems. These market conditions influence inventory management practices and supply agreements, changing the working capital requirements and risk management strategies throughout the industry.

Availability of substitute ingredients

Compounds such as betaine, choline, and botanical extracts compete with inositol in certain applications, especially where cost is a primary consideration over therapeutic effectiveness. Betaine offers similar methyl donor properties and insulin-sensitizing benefits at reduced costs, making it suitable for feed applications that do not require precise inositol levels. Feed manufacturers use phytase enzyme supplementation to release natural inositol from phytate compounds, reducing the need for direct inositol addition while maintaining nutritional benefits. This enzyme-based approach helps manufacturers optimize costs while preserving animal performance. While alternative ingredients gain regulatory approval and quality improvements, affecting inositol's market position in cost-sensitive segments, inositol maintains its advantage in therapeutic applications due to its specific biological functions and established clinical evidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Plant-Based Dominance Meets Synthetic Innovation

In 2025, plant-based inositol commands a dominant 61.72% share of the market. This surge in popularity is largely attributed to consumers' growing preference for natural ingredients, coupled with tried-and-true extraction techniques from corn and rice. The segment's robust standing is bolstered by its clean-label designation, which appeals to health-conscious consumers, and widespread regulatory endorsements that ensure its acceptance across various regions. Additionally, plant-based inositol benefits from its versatility in applications, including dietary supplements, pharmaceuticals, and functional foods. However, it's worth noting that production costs for plant-based inositol are susceptible to the whims of agricultural commodity price fluctuations, which can impact its overall profitability.

Synthetic inositol is projected to grow at a CAGR of 9.88% through 2031. This growth is attributed to advancements in fermentation-based production methods that lower manufacturing costs while maintaining consistent purity levels. Recent manufacturing innovations have reduced the traditional distinctions between plant-based and synthetic categories, as new biotechnology processes combine plant substrates with engineered microorganisms for inositol production. This integrated approach offers both the marketing benefits of plant-based origins and the production advantages of controlled fermentation. Both production methods comply with USP and EP monograph specifications, meeting established purity and safety standards.

By Type: Myo-Inositol Leadership with D-Chiro-Inositol Acceleration

Myo-inositol dominates the type segmentation with 79.56% market share in 2025, supported by extensive clinical evidence, regulatory acceptance, and established manufacturing infrastructure across multiple production routes. The compound's versatility spans therapeutic applications in PCOS treatment, infant formula fortification, and feed supplementation, creating diverse revenue streams that support market stability. D-chiro-inositol emerges as the fastest-growing segment at 11.28% CAGR through 2031, driven by specialized therapeutic protocols and combination therapy approaches that leverage its unique metabolic properties. Clinical research increasingly demonstrates that D-chiro-inositol addresses specific aspects of insulin resistance that myo-inositol cannot fully correct, creating complementary rather than competitive market dynamics.

The optimal therapeutic ratio of 40:1 myo-inositol to D-chiro-inositol drives demand for both compounds, though D-chiro-inositol's higher production complexity and limited manufacturing capacity create supply constraints that support premium pricing. Fermentation-based production of D-chiro-inositol requires specialized enzyme systems and longer cultivation periods compared to myo-inositol, resulting in higher manufacturing costs that pharmaceutical applications can absorb but feed applications cannot. This cost differential creates natural market segmentation where myo-inositol serves broader applications while D-chiro-inositol focuses on high-value therapeutic uses. Regulatory considerations favor myo-inositol due to its longer safety history and more extensive toxicological database, though D-chiro-inositol benefits from growing clinical evidence that supports its therapeutic positioning.

By Application: Dietary Supplements Lead While Food Applications Surge

The dietary supplement segment holds 37.12% market share in 2025, as inositol maintains a strong presence in the nutraceutical industry due to increased consumer awareness of its health benefits. This segment operates under less complex regulatory requirements compared to pharmaceutical applications while generating higher margins than food and feed uses. The food and beverage segment exhibits the strongest growth trajectory at 10.95% CAGR through 2031, primarily due to infant formula enrichment and functional food development. The FDA's GRAS status for inositol in infant formula expands market opportunities, particularly in developed nations where demand for premium infant nutrition products remains robust.

The pharmaceutical segment shows consistent growth despite regulatory complexities, supported by inositol's proven effectiveness in PCOS treatment and mental health applications. This segment maintains high pricing due to strict pharmaceutical-grade purity standards and documentation requirements, though regulatory approval processes limit volume expansion. Animal feed and personal care applications provide market stability through diversification, albeit at lower price points. The animal feed segment expands with Asia-Pacific's growing monogastric production, where inositol improves feed efficiency and reduces oxidative stress in intensive farming. Personal care remains a small but expanding segment, with inositol's moisturizing and skin barrier enhancement properties supporting its use in premium skincare products.

Geography Analysis

In 2025, Asia-Pacific commands a dominant 43.74% share of the inositol market, solidifying its role as both a leading consumer and the foremost manufacturing hub. While China's robust feed production and corn processing have traditionally bolstered its inositol manufacturing, recent fluctuations in corn prices have prompted a shift towards alternative feedstocks, such as rice bran and wheat. The region's burgeoning middle class, coupled with heightened health consciousness, fuels a rising demand for dietary supplements, particularly those targeting metabolic health and cognitive function. Simultaneously, initiatives aimed at regulatory alignment, such as harmonization of standards under ASEAN, are smoothing the path for international suppliers to access the market, further enhancing the region's global competitiveness.

Japan's pharmaceutical industry consistently seeks high-purity inositol, fostering premium market segments. This demand not only propels advancements in manufacturing processes but also elevates quality control standards to meet stringent pharmaceutical-grade requirements. The focus on therapeutic applications, including mental health and liver health, continues to drive innovation in the sector. South America, led by Brazil, is on a rapid ascent, boasting the highest growth rate at 9.76% CAGR through 2031. Brazil's dietary supplement market surged by 43% in Q1 2024, spurred by evolving regulations under ANVISA and a heightened awareness of PCOS treatments, bolstered by better healthcare access. Additionally, the region's growing fitness culture and demand for functional foods are contributing to the expansion of the inositol market.

While Argentina's agricultural sector presents opportunities for plant-based inositol production, its manufacturing infrastructure lags behind its Asian counterparts, limiting its ability to scale production efficiently. However, the country's abundant raw material availability, such as corn and soy, positions it as a potential future player in the market. North America and Europe, while holding steady market positions, are channeling their focus towards high-value applications. In these regions, the emphasis on pharmaceuticals and premium dietary supplements is underscored by stringent regulatory compliance and elevated quality standards, allowing them to command higher prices that offset increased manufacturing costs. Furthermore, the growing trend of personalized nutrition and the rising prevalence of chronic diseases are driving demand for specialized inositol-based products in these markets.

Competitive Landscape

The inositol market shows moderate consolidation, characterized by a balance between established multinational suppliers and regional manufacturers who benefit from cost advantages and local market expertise. Market leaders such as DSM-Firmenich focus on high-value applications and vertical integration across the supply chain, from raw material sourcing to end-product manufacturing. The major players in the market include Koninklijke DSM N.V., Merck KGaA (Sigma-Aldrich), Zhucheng Haotian Pharm Co. Ltd (HOWTIAN), Shandong Runde Biotechnology Co., and Charles Bowman & Company.

Smaller manufacturers struggle to match the competitive edge gained through advanced fermentation techniques, automated process controls, and optimization methods, primarily due to their limited technical resources. These advanced methods enable manufacturers to achieve higher efficiency, better scalability, and improved product consistency, which are critical in maintaining a competitive position. There's been a notable uptick in patent activity, focusing on new production methods and therapeutic applications, especially in innovative microbial strategies and specialized formulations for treating PCOS. This surge in patent filings highlights the industry's focus on innovation and the growing demand for effective and targeted therapeutic solutions.

Precision fermentation methods present emerging opportunities, promising reduced production costs and enhanced purity profiles. These methods leverage advanced biotechnological processes to produce high-quality outputs with minimal impurities, making them highly attractive for pharmaceutical applications. However, high capital demands and the need for technical expertise pose challenges for market entry. Regulatory standards, particularly USP and EP monograph requirements for pharmaceutical-grade products, act as formidable entry barriers, benefiting established manufacturers equipped with advanced quality management and compliance systems. These manufacturers are better positioned to navigate complex regulatory landscapes and meet stringent quality requirements, further solidifying their dominance in the market.

Inositol Industry Leaders

-

Shandong Runde Biotechnology Co

-

Charles Bowman & Company

-

Zhucheng Haotian Pharm Co. Ltd (HOWTIAN)

-

Merck KGaA (Sigma-Aldrich)

-

DSM Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: DMC Biotechnologies launched fermented D-chiro-inositol through a proprietary solvent-free process. The process provides higher purity, traceability, and sustainability compared to traditional chemical synthesis methods. The product is designed for nutraceutical applications, focusing on women's health and metabolic formulations. D-chiro-inositol supports hormonal balance, insulin sensitivity, and men's health, with a clinical study demonstrating a 23% increase in testosterone levels.

- May 2025: DMC Biotechnologies introduced fermented myo-inositol using a proprietary solvent-free precision fermentation process. The product features high purity, traceability, and reduced environmental impact compared to traditional synthetic methods. The ingredient targets food, beverage, supplement, and infant nutrition manufacturers, supporting glucose metabolism, reproductive health (including PCOS and fertility), and infant brain development.

- April 2024: Merck KGaA announced a EUR 300 million investment to build an Advanced Research Center at its global headquarters in Darmstadt, Germany. The facility, scheduled for completion by early 2027, will concentrate on biotechnological production and pharmaceutical development.

Global Inositol Market Report Scope

Inositol is a substance that is found in plants and animals. It is also known as vitamin B8. Grains, beans, nuts, fresh fruits, and vegetables are rich sources of inositol. The human body can also produce inositol. It acts as a type of sugar that controls blood sugar and affects the function of a chemical messenger in the brain.

The inositol market is segmented by source, application, and geography. Based on the source, the market is segmented into plant-based and synthetic inositol. Based on the application, the market is segmented into dietary supplement, beverage, feed industry, pharmaceutical industry, and other applications. By geography, the study analyzes the inositol market in emerging and established markets, including North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Plant-based Inositol |

| Synthetic Inositol |

| Myo-inositol (MI) |

| D-chiro-inositol (DCI) |

| Dietary Supplement | |

| Food and Beverage | Beverages |

| Infant Formula | |

| Others | |

| Pharmaceutical Industry | |

| Other Applications (animal feed, personal care and cometics) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Australia | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| Source | Plant-based Inositol | |

| Synthetic Inositol | ||

| Type | Myo-inositol (MI) | |

| D-chiro-inositol (DCI) | ||

| Application | Dietary Supplement | |

| Food and Beverage | Beverages | |

| Infant Formula | ||

| Others | ||

| Pharmaceutical Industry | ||

| Other Applications (animal feed, personal care and cometics) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Australia | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the inositol market by 2031?

Global revenue is expected to reach USD 643.99 million by 2031, rising at a 9.19% CAGR from 2026 levels.

Which region will grow the fastest through 2031?

South America is forecast to expand at a 9.76% CAGR, led by Brazil’s booming dietary supplement sector.

Why are synthetic inositol grades gaining traction?

Advances in precision-fermentation have reduced unit costs and improved purity consistency, making synthetic grades attractive for pharmaceutical use.

How does inositol support PCOS management?

Clinical evidence confirms that combined myo-inositol and D-chiro-inositol therapy restores insulin sensitivity and ovarian function with favorable tolerability.

Page last updated on: