Annatto Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

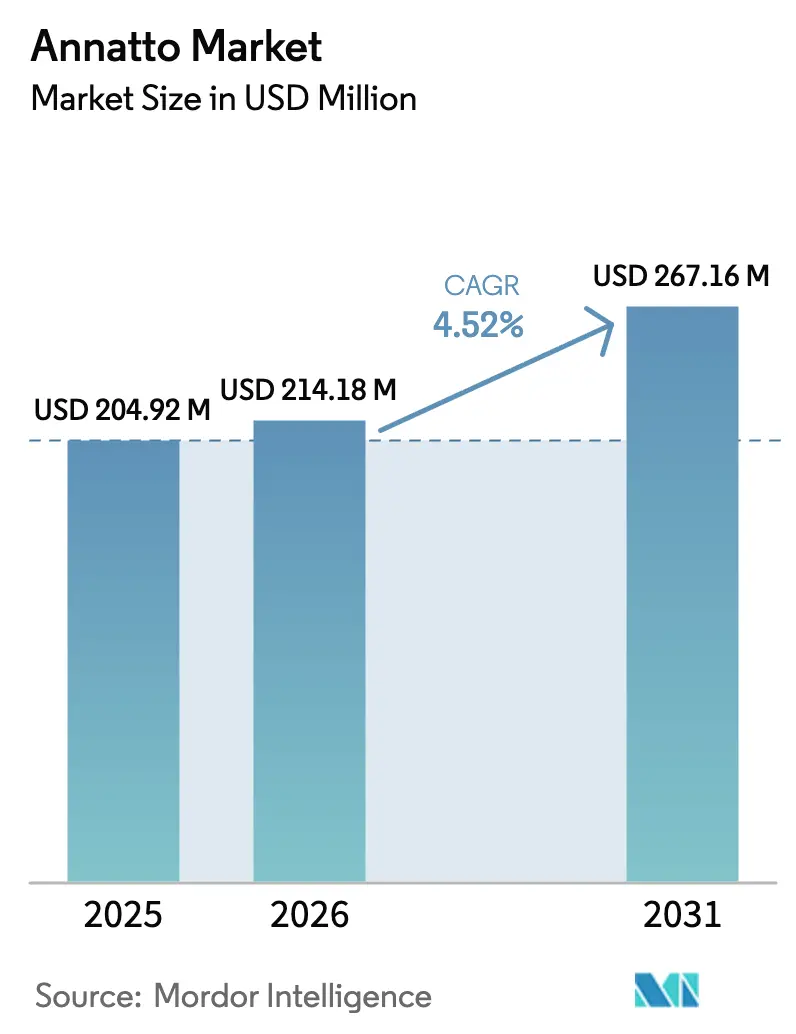

| Market Size (2026) | USD 214.18 Million |

| Market Size (2031) | USD 267.16 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

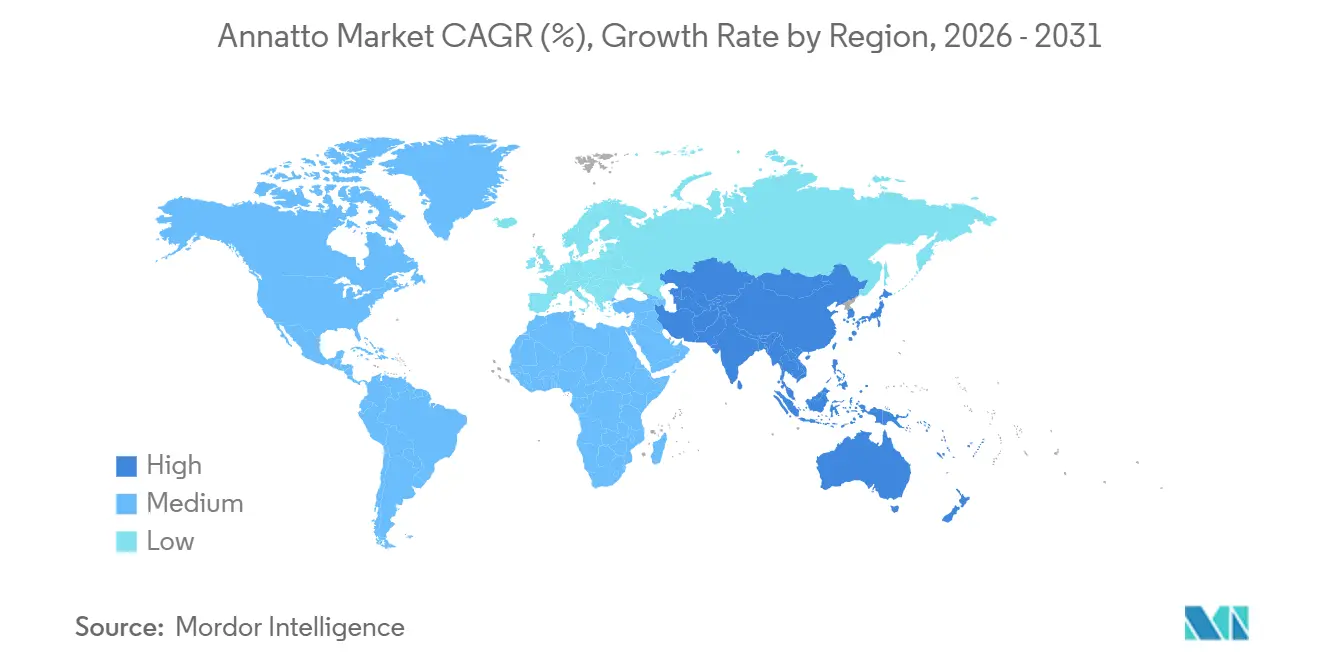

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Annatto Market Analysis by Mordor Intelligence

The Annatto Market size is expected to grow from USD 204.92 million in 2025 to USD 214.18 million in 2026 and is forecast to reach USD 267.16 million by 2031 at 4.52% CAGR over 2026-2031. Demand pivots on tighter rules against artificial dyes and rising consumer preference for familiar botanical ingredients that simplify label reading. Bixin and norbixin pigments extracted from Bixa orellana seeds now color cheese, margarine, baked snacks, plant-based meat, and dairy alternatives with minimal reformulation effort. Oil-soluble formats dominate fat-rich foods while emulsified dispersions unlock hybrid and low-fat systems that once relied on azo dyes. Technology advances in supercritical CO₂ extraction, micronization, and encapsulation improve color strength, shelf life, and heat tolerance, allowing the Annatto Market to defend its share against turmeric, beta-carotene, and paprika. Producers that secure certified-organic seed supply and demonstrate solvent-free processing win contracts from global consumer packaged-goods companies seeking robust ESG narratives.

Key Report Takeaways

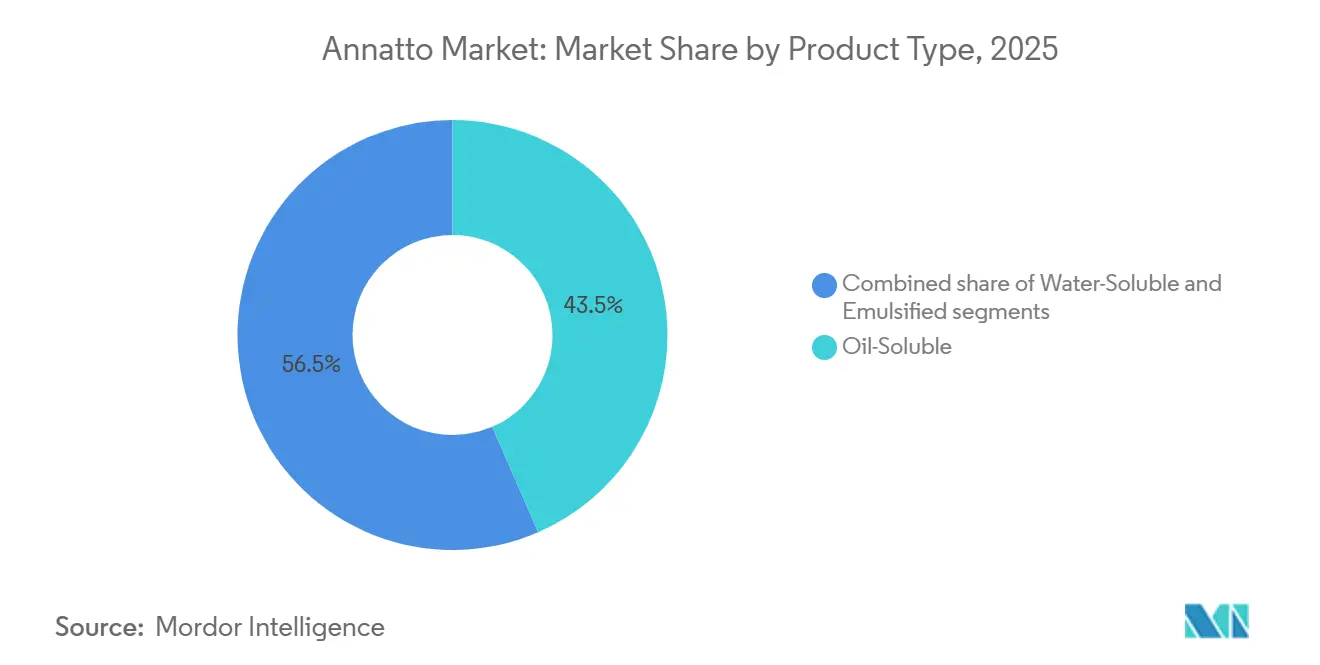

- By product type, oil-soluble grades commanded 43.48% of the Annatto market share in 2025; emulsified formats are forecast to post the fastest 7.41% CAGR through 2031.

- By nature, conventional variants captured 60.33% of the Annatto market share in 2025; organic-certified extracts are projected to advance at an 8.42% CAGR between 2026-2031.

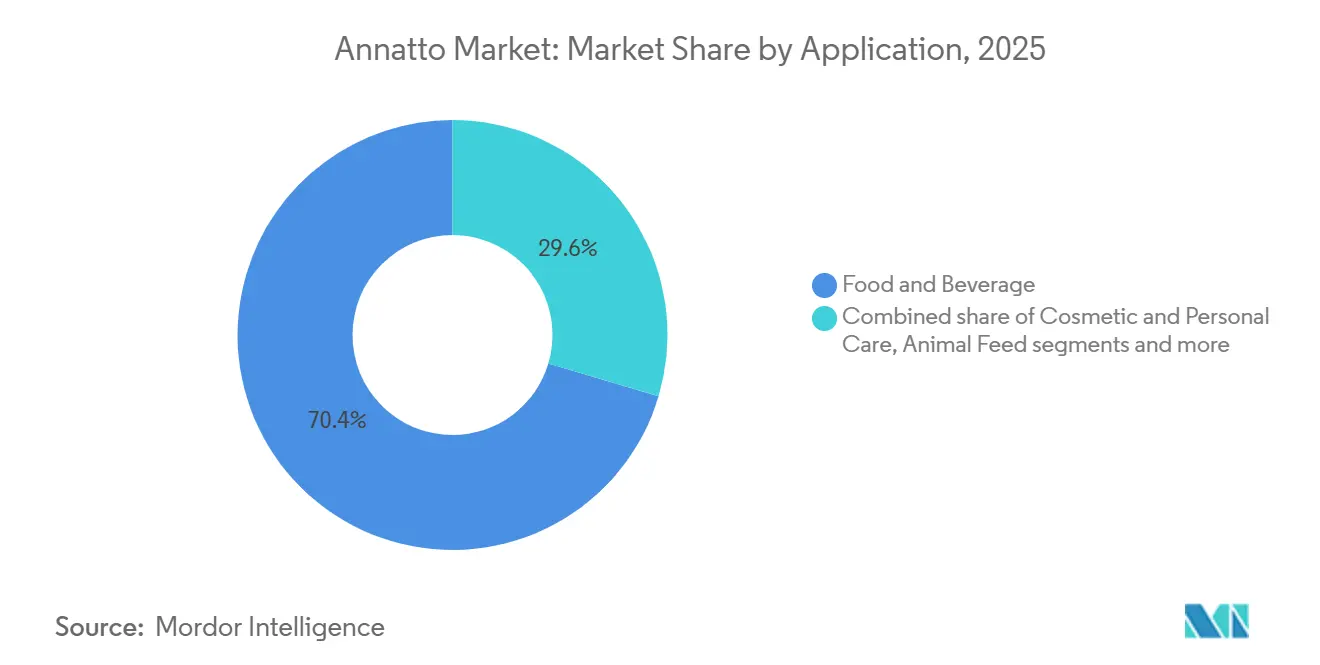

- By application, food and beverage accounted for 70.41% of the Annatto market size in 2025; cosmetics and personal care are expected to grow at a 7.70% CAGR through 2031.

- By geography, North America held 31.44% of the Annatto market share in 2025, and Asia-Pacific is poised to record the quickest 7.47% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Annatto Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong shift toward clean-label and naturally sourced food additives | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising demand for certified organic and non-GMO ingredient solutions | +0.9% | North America, Europe, and emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Growing adoption of plant-forward and vegan dietary lifestyles | +0.8% | Global, led by North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Expansion of the global processed and packaged food industry | +0.7% | Asia-Pacific core, with spillover to Middle East and Africa | Short term (≤ 2 years) |

| Broader utilization across cosmetics and pharmaceutical formulations | +0.5% | Global, with early gains in Europe and North America | Long term (≥ 4 years) |

| Ongoing innovation in extraction and formulation technology | +0.4% | Global, driven by North America and Europe Research and Development hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong shift toward clean-label and naturally sourced food additives

Consumer demand for clean-label and naturally sourced food additives is driving significant changes in the annatto market. Food manufacturers are increasingly replacing artificial colors with natural pigments like annatto extract to align with evolving consumer preferences. In the United Kingdom, over 76% of adults read food labels before purchasing, with 82% of individuals aged 18-34 doing so. Additionally, nearly 45% of consumers report paying more attention to label information compared to five years ago, and 70% focus on processing and ingredient details, as per the National Science Foundation [1]Source: National Science Foundation (NSF), "NSF Research Reveals Brits Demand Greater Clarity, Transparency and Standardisation in Food Labelling", nsf.org. This shift has prompted food brands to prioritize ingredient transparency and secure clean-label certifications to maintain consumer trust and strengthen their market positioning. Annatto ingredient manufacturers, such as DDW The Color House, are responding to these trends by investing in sustainable extraction technologies and expanding their clean-label product portfolios. As a globally recognized supplier of high-purity natural annatto extracts, DDW supports multinational food and beverage producers across applications like cheese, snacks, beverages, and other processed foods. These developments highlight how consumer preferences for natural and transparent ingredients are shaping innovation and competitive strategies within the annatto market.

Growing adoption of plant-forward and vegan dietary lifestyles

The increasing adoption of plant-forward and vegan dietary lifestyles is driven by consumer preferences for sustainable, ethical, and health-focused alternatives to animal-based products. This shift has created a growing demand for clean, recognizable ingredients, with annatto emerging as a key natural colorant in plant-based formulations. According to data from The Good Food Institute and the Plant Based Food Association, 6 in 10 or 59% of United States households purchased plant-based foods in 2024, reflecting mainstream acceptance and the need for natural additives to enhance the visual appeal of vegan dairy alternatives and meat substitutes [2]Source: The Good Food Institute, "U.S. Retail Market Insights for the Plant-Based Industry," gfi.org. This trend has intensified reformulation efforts, as brands prioritize transparency and clean-label solutions to meet consumer expectations. Annatto ingredient manufacturers, such as Kalsec, are addressing these demands by offering verified vegan-compliant oleoresins, supporting scalability in beverages, snacks, and other applications. Additionally, regulatory initiatives promoting sustainability have further positioned annatto as a critical component in aligning plant-based products with wellness and ethical sourcing goals. The minimal processing of annatto aligns with consumer scrutiny of product labels, reinforcing its role in delivering authenticity without compromising vibrancy or stability. As plant-based portfolios diversify, annatto manufacturers are leveraging these dynamics to expand their applications, solidifying naturally sourced additives as essential to the evolving vegan market.

Expansion of the global processed and packaged food industry

The expansion of the global processed and packaged food industry is a key factor driving the demand for annatto. Rising consumer preferences for convenience foods, ready-to-eat meals, and pre-packaged products are pushing manufacturers to increase production volumes and diversify their portfolios with visually appealing, shelf-stable offerings. This shift is fostering greater reliance on natural colorants like annatto as alternatives to synthetic options. The global packaged food market, now valued at a multi-trillion-dollar scale and projected to grow steadily throughout the decade, reflects evolving urban lifestyles that prioritize convenience while maintaining quality and label transparency. These trends are compelling food producers to incorporate plant-based ingredients to enhance product appeal and meet regulatory and consumer expectations regarding additives. For instance, Imbarex S.A., a verified natural colorant manufacturer specializing in annatto extracts for processed food applications, is expanding its production capacity and supply networks to cater to this growing demand. The structural growth in packaged food production and consumption is directly contributing to the increased adoption of annatto solutions across various categories, including dairy, snacks, sauces, and other products where natural coloring and clean-label positioning are critical to commercial success.

Broader utilization across cosmetics and pharmaceutical formulations

The increasing utilization of annatto in cosmetics and pharmaceutical formulations is driving market growth, supported by rising consumer demand for personal care and health products. Ingredient suppliers are diversifying beyond food applications to address the need for naturally derived colorants and bioactive compounds. In 2024, UK households spent an estimated GBP 37.9 billion on personal care products and services, as reported by the Office for National Statistics, reflecting strong consumer spending and market potential in cosmetics and related goods [3]Source: Office for National Statistics (UK), "Consumer Trends: Q4 2024," ons.gov.uk. This aligns with the growing preference for plant-based, multifunctional ingredients that provide both coloring and functional benefits, such as antioxidant properties, while meeting clean-label standards and regulatory requirements. Annatto’s versatility is demonstrated by its use in cosmetics, including lipsticks, shampoos, soaps, and skincare products, as well as in pharmaceutical applications like pill coatings. These applications highlight their cross-sector relevance and appeal to formulators prioritizing natural and compliant raw materials. Verified annatto portfolios from manufacturers such as Sensient Technologies enable brands to incorporate this plant-derived pigment into diverse products, leveraging consumer preferences for sustainable, natural ingredients. The expanding personal care and health markets present significant opportunities for annatto-based solutions, driven by the demand for innovative, natural formulations that align with evolving consumer and regulatory expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating prices of annatto seeds due to supply-side uncertainties | -0.6% | Global, with acute exposure in Latin America and Asia-Pacific | Short term (≤ 2 years) |

| Stability limitations in aqueous and light-sensitive formulations | -0.4% | Global, particularly in beverage and refrigerated dairy applications | Medium term (2-4 years) |

| Restricted cultivation zones and dependence on specific sourcing regions | -0.3% | Global supply chain, concentrated risk in Latin America | Long term (≥ 4 years) |

| Intensifying competition from other natural coloring agents | -0.2% | Global, with regional variations in substitute availability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating prices of annatto seeds due to supply-side uncertainties

Fluctuating prices of annatto seeds, driven by supply-side uncertainties, present a significant challenge for the market. Annatto seeds, primarily sourced from tropical regions like Latin America, are subject to unpredictable weather conditions, seasonal harvest cycles, and agricultural volatility, leading to inconsistent yields and supply. This dependency results in frequent price fluctuations, with agricultural data showing substantial year-to-year variations in seed availability and market prices. These fluctuations directly impact extract producers' raw material costs and profit margins, complicating planning and pricing for food, cosmetic, and pharmaceutical formulators relying on annatto-derived colorants and ingredients. Furthermore, limited mechanization and smallholder farming practices in key producing countries exacerbate issues of inconsistent quality and availability, increasing lead times and procurement costs. Manufacturers are often forced to absorb higher input expenses or seek alternative colorants, which dampens market growth. Companies like Novonesis, a global supplier of natural annatto extracts for food and beverage applications, have implemented diversified sourcing strategies and optimized supply chains to address price instability and ensure supply continuity. However, these measures underscore the broader challenges posed by raw material price volatility, which continues to affect the market's stability and competitive dynamics.

Stability limitations in aqueous and light-sensitive formulations

Stability limitations in aqueous and light-sensitive formulations present a significant challenge for the adoption of annatto-based pigments. The primary carotenoid pigments in annatto, such as norbixin and bixin, are highly sensitive to environmental factors like light exposure, water activity, and processing conditions, leading to accelerated degradation and color loss compared to synthetic alternatives. For example, norbixin’s color intensity diminishes significantly under light and in aqueous systems without protective measures, making it difficult for manufacturers to maintain consistent hues in clear beverages, sauces, or other water-based products. Additionally, photodegradation, along with susceptibility to pH and oxidation, complicates formulation design and shelf-life stability. These challenges are further intensified as consumer and regulatory demands for clean labels and transparency discourage the use of synthetic stabilizers, leaving manufacturers to address the inherent limitations of natural pigments. While advanced techniques such as microencapsulation can enhance stability, they also increase processing complexity and costs. In applications requiring aqueous clarity or prolonged light exposure, the instability of annatto may deter its use. Ingredient producers like GNT Group, through their Exberry® range, provide natural color solutions and invest in stabilization technologies to mitigate these challenges. However, stability constraints can limit annatto’s adoption in certain segments or necessitate additional formulation optimization, tempering its growth potential despite rising demand for natural colorants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Emulsified Formats Gain Traction

Oil-soluble annatto held the largest market share of 43.48% in 2025, primarily driven by its use in fat-based applications such as cheese and margarine. However, the growing demand for emulsified annatto is reshaping the market landscape. Emulsified formats are projected to expand at a CAGR of 7.41% from 2026 to 2031, surpassing oil-soluble and water-soluble formats. These formats address the need for versatile dispersions that perform effectively in both aqueous and lipid phases without phase separation or color migration. By combining bixin or norbixin with emulsifiers like lecithin, polysorbates, or modified starches, emulsified annatto creates stable systems that withstand pH changes, ionic variations, and thermal processing. Regulatory approvals under FDA 21 CFR 73.30, 73.1030, and EU E160b(i)/(ii) further support its adoption by enabling flexible "annatto color" labeling, which aligns with consumer scrutiny of ingredient lists.

The processed food industry's focus on simplified formulations and clean-label trends is a key driver of emulsified annatto's growth. These formats reduce inventory complexity and accelerate product launches, particularly as vegan food adoption rises, with 59% of United States households purchasing plant-based foods in 2024. Additionally, encapsulation techniques such as spray-drying with maltodextrin or gum arabic enhance shelf life for dry mixes, consolidating the position of established suppliers. Emulsified annatto's technical advantages, including phase stability and compatibility across diverse applications, position it as a critical solution for evolving market demands.

By Nature: Organic Certification Drives Premium Growth

Conventional annatto is expected to maintain the largest market share, accounting for 60.33% in 2025. Its dominance is attributed to its suitability for price-sensitive applications such as animal feed, industrial bakery, and private-label dairy, where cost efficiency outweighs certification requirements. In contrast, organic-certified annatto, projected to grow at a CAGR of 8.42% from 2026 to 2031, is gaining traction due to compliance with USDA National Organic Program and EU organic regulations. These certifications enable premium shelf placement in natural and specialty retail markets, driven by increasing consumer demand for clean-label and plant-based products. Organic annatto's 20-30% price premium stems from higher cultivation costs of Bixa orellana without synthetic inputs, resulting in 10-15% lower yields and reliance on manual labor. Regulatory frameworks, such as the USDA's National List and EU Regulation (EC) No 2018/848, further support organic growth by permitting compliant solvents and banning synthetic inputs, respectively.

Organic annatto's adoption is also bolstered by the FDA's planned phase-out of synthetic dyes by 2026, accelerating its use in processed foods and pharmaceuticals. While conventional annatto dominates fat-based applications with a 43.48% share in oil-soluble formats, organic annatto is rapidly expanding in aqueous norbixin applications for low-fat brines, catering to plant-based demands. Non-GMO certification and encapsulation with organic maltodextrin enhance its appeal, extending shelf life for dry mixes and supporting multinational companies in a consolidated market landscape. These factors position organic-certified annatto as a premium option in health-driven markets.

By Application: Cosmetics Accelerate Beyond Food

Food and beverage applications accounted for the largest share of annatto demand, representing 70.41% in 2025. The dairy industry leads this segment, utilizing annatto to provide consistent golden hues in cheese, butter, yogurt, and ice cream, compensating for milk fat beta-carotene variability. In the bakery sector, encapsulated annatto is replacing synthetic colorants like tartrazine, despite challenges posed by high temperatures of up to 180°C. Emulsified annatto formats, offering enhanced stability, are projected to grow at a CAGR of 7.41%. Beverages also utilize water-soluble norbixin in juices, though pH instability below 4.5 has led to the development of emulsified dispersions for plant-based analogues, enhancing the richness of meat substitutes. Encapsulation with maltodextrin further improves photo-stability, favoring multinational companies with consolidated supply chains.

Cosmetics and personal care applications are expected to grow at a CAGR of 7.70% through 2031, driven by the increasing demand for clean beauty products and regulatory compliance. Fat-soluble bixin is used in lipsticks, foundations, and blushes to create coral shades without iron oxides, supported by FDA and EU approvals. Tocotrienols derived from annatto seeds add antioxidant and anti-aging benefits, appealing to the 59% of US plant-based households favoring vegan-friendly cosmetics. Clean-label and organic products command a 20-30% price premium, positioning high-purity annatto extracts as key ingredients in premium personal care products, reflecting a shift from food dominance to cosmetics growth in health-conscious markets.

Geography Analysis

North America held the largest share of the annatto market in 2025, accounting for 31.44%. The region reflects a mature market where annatto usage in dairy, bakery, and processed food applications is well established. With clean-label reformulation cycles largely completed, growth is primarily driven by population expansion and per-capita consumption rather than new substitution opportunities. In contrast, Europe’s demand is shaped by stringent regulatory oversight and high consumer preference for natural ingredients. EU Regulation 2020/771, which divides E160b into E160b(i) for bixin and E160b(ii) for norbixin, enhances technical transparency but increases compliance complexity for suppliers. While regulatory clarity supports stable demand, Europe’s mature food sector and slower population growth limit volume expansion compared to other regions.

The Asia-Pacific region is projected to grow at the fastest CAGR of 7.47% through 2031, driven by rising processed food consumption in China, India, and Southeast Asia. Strengthened regulatory enforcement and alignment with Codex Alimentarius standards create a harmonized operating environment for multinational food producers. For example, China’s National Health Commission includes annatto under GB 2760 standards, and India’s Food Safety and Standards Authority permits its use under INS 160b. These developments enable standardized formulations across markets, reducing reformulation costs and accelerating adoption in dairy, confectionery, and snack categories. South America, meanwhile, plays a dual role as a major production hub and an emerging consumption market. Brazil, Peru, and Colombia account for over 85% of global annatto seed production, while rising middle-class incomes drive domestic demand for processed foods and cosmetics, strengthening vertical integration opportunities.

The Middle East and Africa represent developing markets where expanding modern retail formats and growing awareness of natural ingredients support early-stage demand. However, infrastructure gaps, import tariffs, and evolving regulatory frameworks constrain faster adoption compared to more established regions. Suppliers focusing on Asia-Pacific distribution networks, regulatory compliance, and local partnerships are well-positioned for growth, while incumbents in North America and Europe must prioritize formulation innovation and premium organic offerings to maintain competitiveness. Companies like Oterra A/S exemplify this approach by aligning geographic strategies with evolving consumption and regulatory trends.

Competitive Landscape

The global annatto market exhibits moderate consolidation, with multinational ingredient companies such as Cargill, ADM, Sensient Technologies, and Oterra holding significant market share. These companies operate through vertically integrated supply chains, managing processes from raw material sourcing to advanced extraction and application support. This structure enables them to maintain strict control over quality, traceability, and cost efficiencies. By utilizing proprietary extraction technologies and leveraging global regulatory expertise, they secure long-term contracts with multinational dairy, snack, and processed food manufacturers. These partnerships allow them to deliver standardized natural color solutions across regions, reinforcing their competitive advantage in a market increasingly shaped by clean-label reformulation, regulatory compliance, and supply chain security.

Regional processors and specialty extractors continue to play a significant role, particularly in niche segments such as organic, high-purity, and application-specific annatto products. These smaller suppliers differentiate themselves through customization, flexible batch sizes, and close collaboration with customers. By fostering direct relationships with seed growers and niche food or cosmetic brands, they address the growing demand for certified organic, sustainably sourced, or minimally processed extracts. This approach enables them to maintain pricing power in premium subsegments of the annatto value chain, where larger players often focus on standardized production at scale.

Market conditions, including increased scrutiny of ingredient sourcing, stability performance in diverse formulations, and substitution pressures from alternatives like turmeric, paprika, and beta-carotene, have intensified competition. Large multinational companies are responding by investing in innovation, enhancing stability, and diversifying their portfolios to protect their market positions. Meanwhile, regional companies compete by emphasizing purity claims and offering targeted technical support. This competitive environment reflects a balance between global incumbents defending their core processed food contracts and agile niche manufacturers capturing margins in differentiated, high-specification applications. The annatto market remains structurally consolidated yet strategically dynamic, driven by evolving consumer preferences and regulatory demands.

Annatto Industry Leaders

-

Cargill, Incorporated

-

Kalsec Inc.

-

Sensient Technologies Corporation

-

Oterra A/S

-

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ROHA Group acquired Tebracc, a Brazilian natural color manufacturer specializing in annatto extraction and processing. The acquisition strengthened ROHA's position in the natural colors market, expanded production capabilities in Brazil, ensured raw material security, and diversified its natural color offerings for global food, beverage, nutraceutical, and pet food brands.

- May 2025: Everwell Health, the parent company of ingredient supplier Nutrition21, announced its acquisition of American River Nutrition (ARN) from Designs for Health. ARN had specialized in annatto extracts. The acquisition included ARN’s patented and branded ingredients, DeltaGold and GG-Gold, as well as other functional ingredients and intellectual property.

- April 2025: Sensient has introduced Natpure® Col Orange LC215L, a 100% natural orange dye made by combining Bixin powder derived from annatto seeds with annatto oil repurposed from the food industry. This ingredient is fully traceable and provides a vibrant orange color to cosmetic products, along with skin benefits such as antioxidant properties.

- February 2025: Oterra, a natural colors specialist, inaugurated a color blending and application center in Kerala, India, to serve the Indian, Asia-Pacific, and Middle East markets. Previously, it exported raw materials to Europe for processing and imported finished blends to India. The new facility enabled direct supply of commonly used food and beverage color shades, including yellow, orange, red, and pink, derived from plant-based materials like turmeric, paprika, annatto, and red beet.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the annatto market as the value generated from purified achiote-seed extracts that are standardized into oil-soluble bixin, water-soluble norbixin, or emulsified forms and then sold to food, beverage, cosmetics, and feed processors worldwide.

Scope exclusion: Raw seed trade, pharmaceutical isolates of tocotrienols, and synthetic norbixin preparations remain outside this assessment.

Segmentation Overview

-

By Product Type

- Oil-Soluble

- Water-Soluble

- Emulsified

-

By Nature

- Organic

- Conventional

-

By Application

-

Food and Beverage

- Dairy Products

- Bakery and Confectionery

- Beverages

- Meat and Plant-based Analogues

- Other Food and Beverages

- Cosmetic and Personal Care

- Animal Feed

- Other Applications

-

Food and Beverage

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed output processors in Peru and Brazil, dairy formulators in the United States and the EU, and natural-ingredient distributors across South-East Asia. These dialogs validated extraction yields, average selling prices, regulatory transition timelines, and substitution rates away from synthetic dyes.

Desk Research

We compiled baseline data from tier-one public sources such as FAOSTAT crop output tables, UN Comtrade shipment codes, USDA Foreign Agricultural Service import alerts, the European Food Safety Authority additive register, and FDA Color Additive Status lists. Annual reports of leading color-ingredient formulators, patent filings tracked through Questel, and news flows in Dow Jones Factiva fortified the evidence trail. D&B Hoovers supplied screened revenue splits that helped us benchmark supplier size. The sources named here illustrate rather than exhaust the reference pool tapped throughout the study.

Market-Sizing & Forecasting

A top-down construct converts annatto-seed harvest volumes and extraction yields into pigment output, which is then valued with region-specific average selling prices. Supplier roll-ups and channel checks supply selective bottom-up cross-checks that correct for captive consumption and re-exports. Key variables like seed acreage expansion, extraction yield drift, dairy colorant usage shares, cosmetic reformulation counts, and import tariff moves anchor the model. Multivariate regression, with seed price, per-capita cheese consumption, and regulatory milestone dummies, projects demand through 2030. Data gaps in smaller geographies are bridged with proxy indicators such as natural colorant penetration in adjacent carotenoid segments.

Data Validation & Update Cycle

Outputs pass variance scans against historical trade, analyst peer review, and a secondary sanitation run before sign-off. We refresh every twelve months; interim rechecks trigger when policy bans, price shocks, or plant closures shift fundamentals.

Why Mordor's Annatto Baseline Guides Reliable Plans

Published estimates often diverge because firms pick differing functional scopes, price bands, and refresh cadences.

Key gap drivers include whether seed sales are counted as market value, if non-color antioxidant derivatives are folded in, how quickly post-2024 FDA synthetic dye restrictions are priced, and the frequency of exchange-rate resets that Mordor updates quarterly while others revise less often.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 204.9 million (2025) | Mordor Intelligence | - |

| USD 275.9 million (2025) | Global Consultancy A | counts raw seed exports and applies global average price without regional mix correction |

| USD 198.5 million (2023) | Trade Journal B | excludes cosmetics and feed uses, leaving a narrower functional scope |

| USD 60.6 million (2024) | Industry Report C | values only oil-soluble grades sold into dairy, omitting other forms and channels |

The comparison shows that once scope and price filters are aligned, Mordor's disciplined bottom-up checks atop a transparent top-down scaffold deliver a balanced, reproducible starting point that executives can trust for budget planning and opportunity screening.

Key Questions Answered in the Report

What is the projected value of the Annatto Market by 2031?

The Annatto Market is forecast to reach USD 267.16 million by 2031.

Which region will grow the fastest through 2031?

Asia-Pacific is expected to record the quickest 7.47% CAGR, driven by expanding processed-food demand and supportive regulations.

Which product format shows the strongest growth outlook?

Emulsified annatto dispersions are set to rise at a 7.41% CAGR owing to their versatility across aqueous and fat-rich foods.

Why is organic-certified annatto gaining share?

Retailers require organic logos for premium ranges, and certified extracts will expand 8.42% annually due to higher consumer willingness to pay.

Page last updated on: