Asthma And COPD Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 50.71 Billion |

| Market Size (2031) | USD 65.27 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

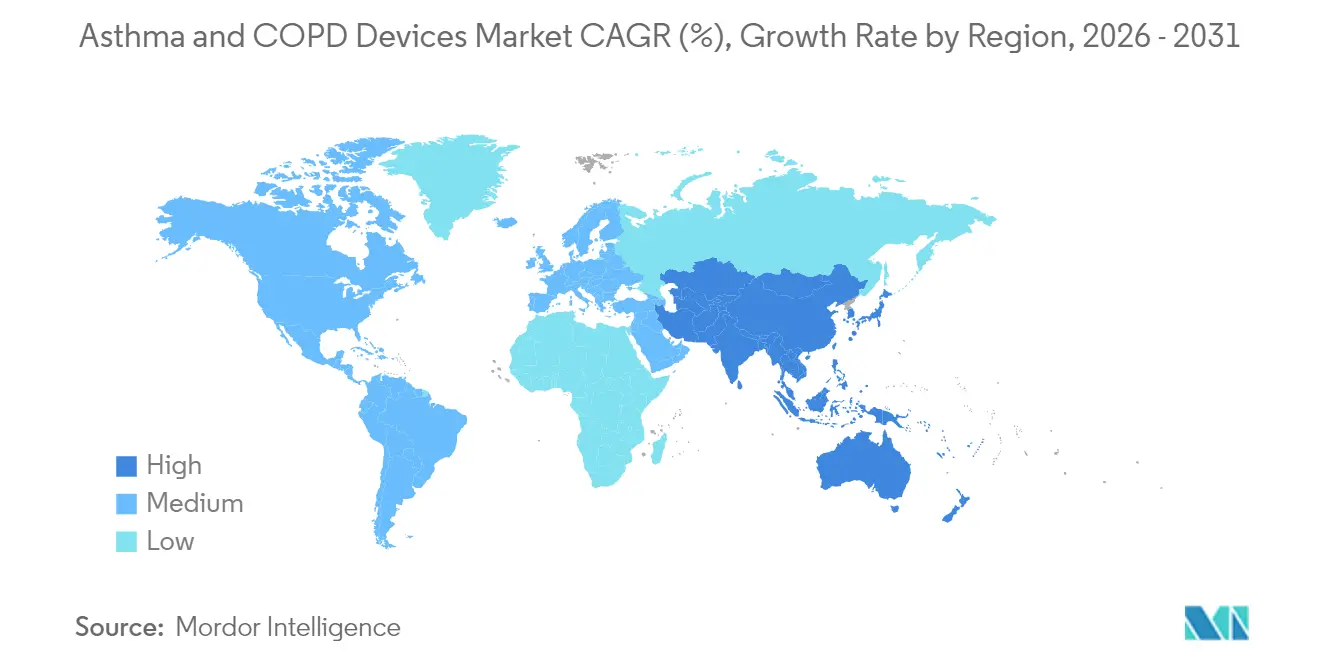

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asthma And COPD Devices Market Analysis by Mordor Intelligence

The Asthma and COPD devices market size was valued at USD 48.21 billion in 2025 and estimated to grow from USD 50.71 billion in 2026 to reach USD 65.27 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). Demographic aging, rising asthma and COPD prevalence, and tighter environmental rules around inhaler propellants are widening demand for both conventional and connected delivery systems. Vendors are weaving artificial-intelligence modules into inhalers and nebulizers, shifting respiratory care from episodic symptom relief toward data-driven, predictive interventions that fit remote-care models. Propellant reformulations with sharply lower global-warming potential are turning regulatory compliance into a source of product differentiation. Meanwhile, reimbursement caps on out-of-pocket drug spending in the United States and value-based payment frameworks in Europe are rewarding devices that tangibly improve adherence and cut exacerbations.

Key Report Takeaways

- By product category, inhalers led with 62.90% of the Asthma and COPD devices market share in 2025; mesh-platform nebulizers are on track to post the fastest 6.05% CAGR through 2031.

- By indication, asthma dominated with 65.30% revenue share in 2025, while COPD applications are projected to accelerate at a 6.18% CAGR to 2031.

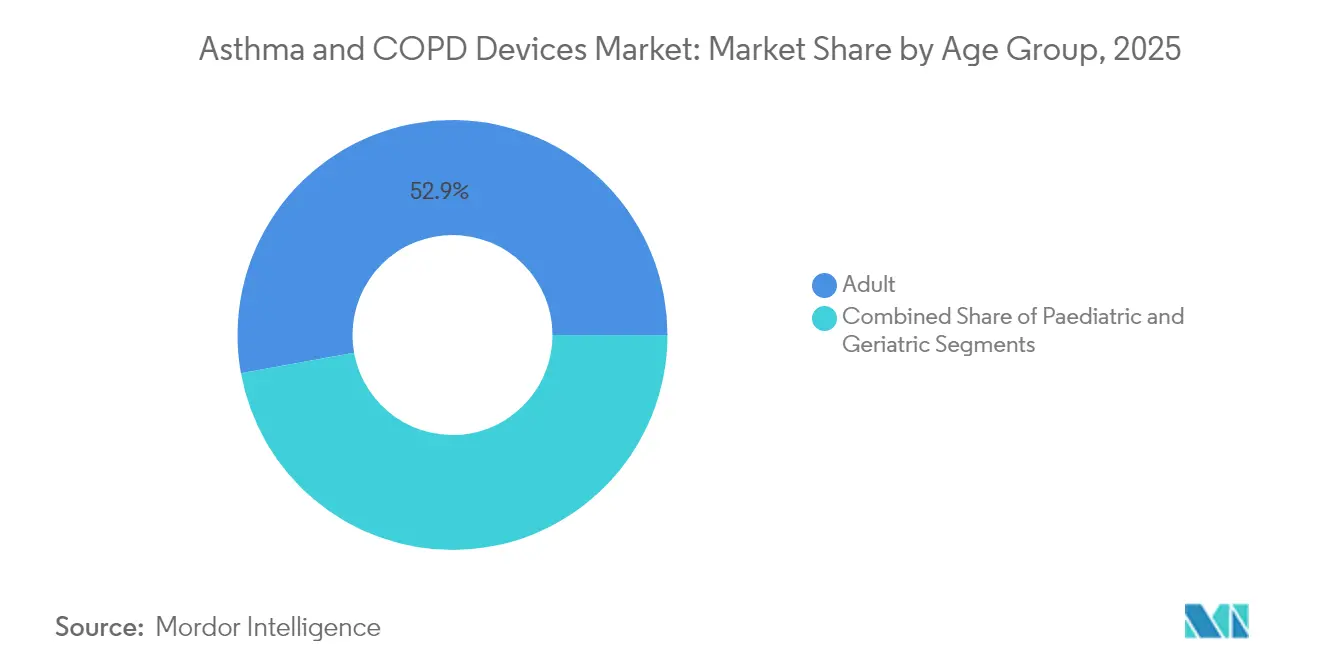

- By age group, adults accounted for 52.85% of the Asthma and COPD devices market size in 2025; pediatric applications are expanding at a 5.98% CAGR.

- By mode of operation, conventional devices held 74.60% share of the Asthma and COPD devices market size in 2025, but digital and connected systems are advancing at a 6.24% CAGR.

- By geography, North America retained a 39.10% share in 2025, whereas Asia-Pacific is forecast to expand at the fastest 6.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asthma And COPD Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of asthma & COPD | +1.2% | Global, highest in Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in inhalation & nebulization | +1.0% | North America & EU | Medium term (2-4 years) |

| Growing geriatric population base | +0.8% | Global, developed markets | Long term (≥ 4 years) |

| Increasing indoor–outdoor air-pollution levels | +0.7% | Asia-Pacific urban hubs | Medium term (2-4 years) |

| Payer-driven adherence programs in developed markets | +0.5% | North America & EU | Short term (≤ 2 years) |

| AI-enabled smart inhalers integrated into tele-pulmonology | +0.6% | North America, EU, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of asthma & COPD

More than 545 million people now live with chronic respiratory diseases that could benefit from smart-inhaler technology. Urban migration, industrial emissions, and lifestyle changes are broadening patient pools far faster than clinic capacity. Asia-Pacific health systems feel the biggest strain, yet developed economies also face aging-related prevalence spikes. As a result, demand is swelling for affordable metered-dose inhalers, premium mesh nebulizers, and data-enabled adherence platforms that can be deployed at home or in virtual-care pathways. Connected-device alerts notifying clinicians of declining peak-flow scores exemplify how epidemiological pressure is catalyzing predictive care models [1]Babajide, A, "Safeguarding Smart Inhaler Devices and Patient Privacy in Respiratory Health Monitoring," arXiv, arxiv.org.

Technological advancements in inhalation & nebulization

Mesh nebulizers achieve lung deposition rates more than triple those of jet units during non-invasive ventilation, making them the preferred platform for late-stage drug-device trials. Propellant reformulations such as HFA-152a cut carbon impact by over 90% while preserving therapeutic equivalence, allowing firms to satisfy both clinical-efficacy and sustainability mandates. Early adopters pairing environment-friendly propellants with Bluetooth-enabled dose trackers are commanding premium pricing in North America and Western Europe. The result is an innovation cycle in which device performance, eco-credentials, and digital connectivity reinforce one another.

Growing geriatric population base

Older patients frequently lack the dexterity to coordinate inhaler actuation and inhalation, so they gravitate toward nebulizers. Medicare records show that 28% of COPD beneficiaries used nebulizers in 2024, prompting suppliers to integrate voice prompts, auto-dosing, and large-display readouts. Aging accelerates comorbidity loads, making remote symptom monitoring attractive to caregivers and insurers. Device makers targeting geriatric users are embedding fall-detection sensors and real-time adherence dashboards that feed information into value-based reimbursement models.

Increasing indoor–outdoor air-pollution levels

Increasing indoor–outdoor air-pollution levelsIndustrial expansion and vehicular congestion raise particulate counts, especially across Asia-Pacific mega-cities. Governments are rolling out urban air-quality indices accessible through smartphone APIs; device makers link these feeds with inhaler-dosing algorithms that nudge patients to pre-empt exposure-triggered flare-ups. Portable PM2.5 sensors integrated into spacer chambers illustrate how pollution trends are spawning hybrid products that couple ambient monitoring with medication delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval timelines | -0.8% | North America & EU | Medium term (2-4 years) |

| Inadequate reimbursement in developing regions | -0.6% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Price sensitivity & generic competition | -0.5% | Global, price-sensitive markets | Short term (≤ 2 years) |

| Data-privacy concerns around connected devices | -0.3% | EU, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory approval timelines

The United States FDA now requires comprehensive human-factor studies and digital-component validation before clearing combination inhalers [2]FDA, "Essential Drug Delivery Outputs for Devices Intended to Deliver Drugs and Biological Products Guidance for Industry," fda.gov. Similar scrutiny from Europe’s Medical Device Regulation has elongated review cycles, lifting R&D budgets and delaying commercial launches. Large incumbents can absorb these costs, but start-ups often struggle to fund extended pivotal trials, leading to fewer novel entrants and a gradual up-tick in market concentration.

Inadequate reimbursement in developing regions

Even as prevalence rises, many lower-income countries offer minimal insurance coverage for branded inhalers and connected nebulizers. Procurement processes are fragmented, and patients frequently pay out of pocket, constraining uptake of premium technologies. Manufacturers addressing this gap are trialing pay-as-you-go models and low-cost device variants, yet commercial scale remains years away, tempering global growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Mesh technology drives nebulizer renaissance

Nebulizers generated a 6.05% CAGR outlook through 2031, the fastest within the Asthma and COPD devices market, even though inhalers retained a commanding 62.90% share in 2025. Mesh platforms improve drug delivery efficiency, trim treatment times, and run quietly enough for use during virtual consultations. Vendors pairing mesh chambers with digital-dose counters report 3-point gains in Asthma Control Test scores versus standard devices. Meanwhile, low-global-warming-potential propellants are rebooting the metered-dose inhaler line-up, and soft-mist inhalers now serve as a middle ground, offering high lung deposition without cold-gas plume discomfort .

Second-generation nebulizers capitalize on these shifts by bundling smartphone dashboards that visualize nebulization adherence trends for clinicians. The interplay of sustainability mandates, patient-experience imperatives, and biologic-drug compatibility ensures that both inhalers and nebulizers will coexist, but revenue momentum tilts toward mesh-equipped designs. Pharmaceutical partners co-developing fixed-dose triple therapies are specifying mesh units in clinical protocols, anchoring the segment’s growth runway.

By Indication: COPD emerges as growth engine

Asthma represented 65.30% of 2025 revenue, yet COPD devices are projected to grow faster at 6.18% CAGR, lifting their slice of the Asthma and COPD devices market over the next five years. COPD’s progressive pathology often necessitates dual-bronchodilator or steroid-combo inhalers, inflating per-patient spend. Late-stage trials of biologics such as IL-5 inhibitors show promise, and their delivery will require advanced inhaler platforms capable of precise microgram dosing and built-in error detection.

Asthma management is shifting toward phenotype-guided therapies and preventive monitoring, leveraging connected inhalers that record usage and transmit peak-flow trends. Both indications are converging on digitally tracked regimens, but COPD’s higher hospitalization burden aligns squarely with payers’ cost-offset goals, accelerating adoption of premium connected devices in that sub-segment.

By Age Group: Pediatric innovation accelerates

Adults held 52.85% share in 2025, but the pediatric slice is growing at a 5.98% CAGR, aided by child-friendly mouthpieces, animated inhalation coaching, and dose-dispersion tolerances calibrated for smaller lungs. Device manufacturers responded quickly after a leading inhaled-steroid brand exited the market in 2024, rolling out spacer-compatible generics and nebulizer cup adaptors that restored accessibility within months. Digital whistles that provide real-time acoustic feedback ensure correct inhalation flow, boosting adherence in children.

The geriatric cohort cements its preference for nebulizers, elevating demand for lightweight, battery-operated designs with automated cleansing cycles. Engineers are including RFID-tagged consumable filters so caregivers receive replacement alerts before performance degrades, illustrating age-related differentiation in feature road-maps.

By Mode of Operation: Digital transformation accelerates

Digital and connected devices will grow at 6.24% CAGR to 2031 while conventional platforms still supplied 74.60% of global shipments in 2025. Real-world studies show that Bluetooth-linked inhalers cut severe exacerbations by more than 20% compared with paper logbooks. Yet a 12% hardware-failure rate underscores the need for robust sensors and firmware. Vendors are standardizing over-the-air updates and secure cloud connectors to maintain reliability and comply with GDPR and HIPAA data-protection rules.

Economic considerations shape adoption curves: premium connected devices gain traction in value-based reimbursement regions, whereas cash-paying rural populations remain reliant on low-cost MDIs. Multi-tenant dashboards now integrate inhaler events, spirometry telemetry, and local air-quality feeds, supporting clinical decisions that align with pay-for-performance metrics.

Geography Analysis

North America commanded 39.10% of global revenue in 2025, aided by structured reimbursement and early uptake of connected inhalers. A USD 2,000 annual out-of-pocket drug cap effective in 2025 is expected to encourage therapy intensification and higher device-drug bundling, even as insurers press for real-world evidence of outcome gains. Leading manufacturers have introduced monthly price ceilings of USD 35 for core inhaler lines, illustrating competitive responses to affordability mandates.

Asia-Pacific is the growth pacesetter with a 6.22% CAGR outlook to 2031. China’s medical-device expansion aligns with Made in China 2025 and Healthy China 2030 agendas that incentivize domestic production of advanced respiratory devices. India’s New Drugs, Medical Devices and Cosmetics Bill 2023 similarly targets faster approvals and quality enforcement, spurring local and multinational investments in mesh-nebulizer lines. Urban air-pollution spikes in Beijing, Delhi, Jakarta, and Bangkok amplify patient demand for portable, environment-aware inhalers.

Europe shows consistent, albeit slower, expansion as sustainability regulations accelerate turnover of legacy CFC-propellant inhalers. The bloc’s Medical Device Regulation emphasizes lifecycle carbon accounting, and connected-device rollouts must satisfy stringent GDPR data-privacy thresholds. These rules raise compliance costs but reward firms delivering verified eco-performance and secure data architectures. New reimbursement paths tied to population-health metrics reinforce demand for adherence-tracking inhalers in markets such as Germany, the Nordics, and the Netherlands.

Competitive Landscape

Global supply is fragmented. Multi-year M&A has produced vertically integrated models coupling molecule discovery, formulation, device engineering, and digital platforms. Molex’s pending acquisition of Vectura Group fortifies its in-house mesh and dry-powder inhaler pipelines, while AstraZeneca, GSK, and Boehringer Ingelheim retain strong proprietary respiratory portfolios complemented by device co-development alliances.

Competition now centers on three differentiation axes. First, sustainable propellants: AstraZeneca completed clinical programs for a 99.9% lower-GWP formulation for one of its triple therapies, aiming for rapid regulatory filings in 2025. Second, connectivity: ResMed spends 7% of revenue on integrating cloud analytics that span sleep-apnea and COPD devices, expanding cross-selling synergies. Third, indication expansion: late-phase COPD biologics portend platform extensions that could reshape device requirements toward higher drug loads and stricter dose accuracy.

Start-ups focusing solely on smart sensors struggle to clear regulatory and commercial hurdles unless they team up with incumbent manufacturers. Nevertheless, white-space remains in pediatric-specific devices and low-cost digital inhalers calibrated for emerging-market affordability thresholds. Intellectual-property clustering around mesh-generator geometries, algorithmic adherence scoring, and eco-propellants reinforces barriers for new entrants.

Asthma And COPD Devices Industry Leaders

-

AstraZeneca

-

Boehringer Ingelheim

-

GlaxoSmithKline

-

Merck & Co.

-

Philips Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Theravance Biopharma agreed to sell its remaining interest in Trelegy Ellipta to GSK for USD 225 million, with potential milestones up to USD 150 million.

- September 2024: Molex announced an agreement to acquire Vectura Group, broadening its capabilities in inhalation drug delivery.

- September 2024: AstraZeneca completed clinical programs to transition Breztri to a next-generation propellant with 99.9% lower global-warming potential.

- January 2024: AstraZeneca launched AIRSUPRA (albuterol / budesonide) in the United States for adult asthma patients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the asthma and chronic obstructive pulmonary disease (COPD) devices market as global revenue from therapeutic inhalation hardware such as metered-dose, dry-powder, and soft-mist inhalers, jet or mesh nebulizers, and companion spacer accessories supplied through hospital, pharmacy, and home-care channels.

Scope exclusion: diagnostic-only flow meters, refill canisters, and all pharmaceutical sales sit outside this boundary.

Segmentation Overview

-

By Product

-

Inhalers

- Metered-Dose Inhalers

- Dry-Powder Inhalers

- Soft-Mist Inhalers

-

Nebulizers

- Compressor Nebulizers

- Ultrasonic Nebulizers

- Mesh Nebulizers

-

Inhalers

-

By Indication

- Asthma

- Chronic Obstructive Pulmonary Disease

-

By Age Group

- Paediatric

- Adult

- Geriatric

-

By Mode of Operation

- Digital / Connected Devices

- Conventional Devices

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed respiratory physicians, biomedical engineers, hospital buyers, and home-care distributors across North America, Europe, Asia-Pacific, and the Middle East. Their insight on device life cycles, net prices, and barriers to connected-inhaler uptake helped us refine desk findings.

Desk Research

We aligned prevalence, mortality, and trade data pulled from the WHO Global Health Observatory, UN population tables, the US CDC, Eurostat, and UN Comtrade codes 9019/9020. Regulatory files at the FDA and EMA, peer-reviewed articles in Chest, and patent families mined on Questel flagged shifts toward low-GWP propellant inhalers and portable mesh engines. Paid feeds from D&B Hoovers and Dow Jones Factiva added company splits and supply-chain alerts. The sources noted are illustrative only; many other references informed cross-checks.

Market-Sizing & Forecasting

We apply one top-down and bottom-up blend. Diagnosed prevalence is stepped through treatment and device-penetration ratios to estimate active users, then multiplied by use frequency and regional average prices. Supplier roll-ups and channel checks validate totals. Key variables tracked include acute-exacerbation admissions, mesh share within nebulizers, connected-device uptake, propellant-switch deadlines, urban PM2.5 levels, and price premiums. Multivariate regression coupled with scenario analysis carries the view to 2030, while nearest-neighbor benchmarks bridge local gaps.

Data Validation & Update Cycle

Outputs face variance tests against import values, prescription audits, and insurance claims before a two-stage analyst review. We refresh each study yearly and issue interim tweaks after recalls, price shocks, or major regulatory moves.

Why Our Asthma and COPD Devices Baseline Commands Boardroom Confidence

Published estimates often diverge because publishers pick different device baskets, price ladders, and refresh cadences. By locking scope early, checking prices in the field, and updating faster, Mordor Intelligence delivers a balanced baseline executives can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 48.21 B (2025) | Mordor Intelligence | - |

| USD 32.40 B (2024) | Global Consultancy A | Omits soft-mist and connected add-ons; outdated prices |

| USD 24.50 B (2023) | Regional Consultancy B | Uses shipment weight only, no patient link |

| USD 35.24 B (2024) | Industry Association C | Blends therapeutic drug revenue with device sales |

Together, we show that clear boundaries, current prices, and primary validation keep our figure transparent, reproducible, and ready for quick decisions.

Key Questions Answered in the Report

What is the current size of the Asthma and COPD devices market?

The Asthma and COPD devices market stood at USD 50.71 billion in 2026 and is forecast to reach USD 65.27 billion by 2031.

Which product category is growing the fastest?

Mesh-platform nebulizers lead growth with a projected 6.05% CAGR, driven by superior drug deposition and rising use in combination-therapy trials.

Why is Asia-Pacific considered the key growth region?

Rapid urbanization, high pollution levels, and regulatory reforms that promote domestic manufacturing are propelling Asia-Pacific to a 6.22% CAGR.

How are environmental regulations influencing device design?

Propellant phasedowns are pushing firms toward low-GWP formulations such as HFA-152a, turning sustainability compliance into a product-differentiation lever.

What role do connected inhalers play in value-based care models?

Connected devices provide adherence and symptom data that payers use to verify outcome improvements, enabling reimbursement incentives for products that demonstrably reduce exacerbations.

Are COPD devices expected to outpace asthma devices in growth?

Yes, COPD applications are projected to expand at 6.18% CAGR through 2031, faster than asthma, due to aging demographics and therapy-intensification trends.

Page last updated on: