Digital Dose Inhaler Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

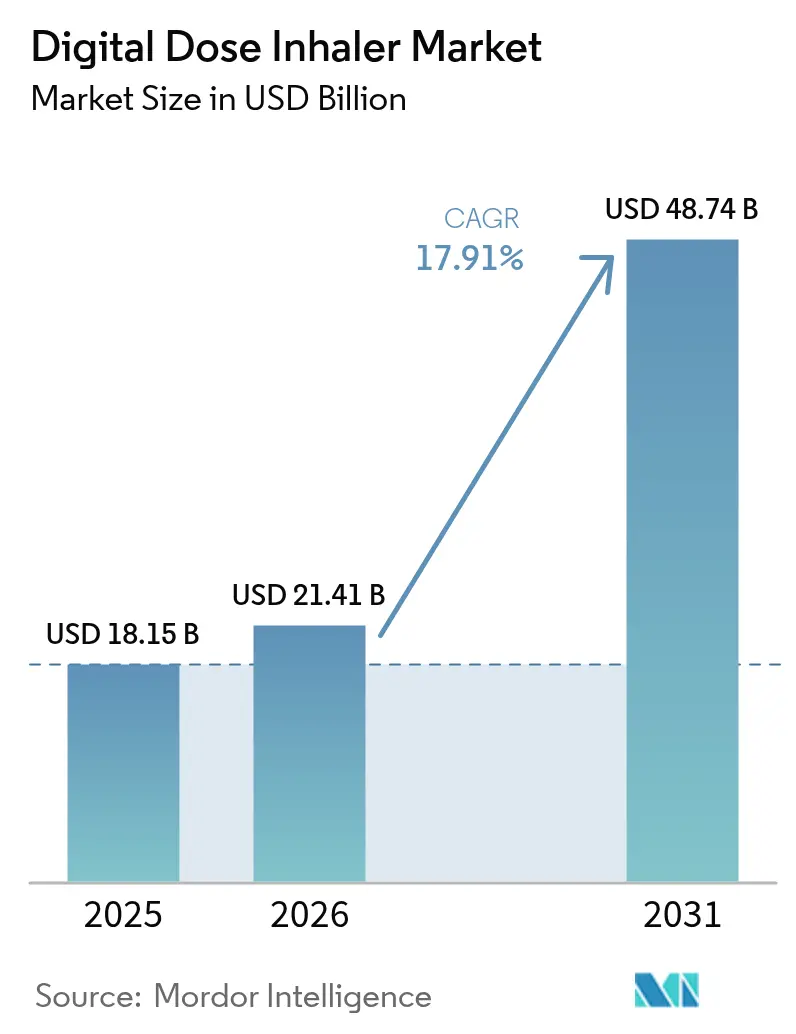

| Market Size (2026) | USD 21.41 Billion |

| Market Size (2031) | USD 48.74 Billion |

| Growth Rate (2026 - 2031) | 17.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Dose Inhaler Market Analysis by Mordor Intelligence

The digital dose inhaler market size is expected to grow from USD 18.15 billion in 2025 to USD 21.41 billion in 2026 and is forecast to reach USD 48.74 billion by 2031 at 17.91% CAGR over 2026-2031. Robust growth is linked to rising respiratory disease prevalence, rapid uptake of connected therapeutics, and stringent environmental regulations that are forcing propellant innovation. Real-time data capture from Internet of Things–enabled inhalers is giving physicians objective adherence evidence, while artificial intelligence is beginning to predict exacerbations before they occur. Capital inflows into digital respiratory care start-ups continue to climb, strengthening the competitive landscape and expanding patient access to sensor-equipped devices. Environmental legislation in Europe is accelerating the switch to low-GWP propellants, prompting major suppliers to overhaul meter-dose inhaler portfolios well ahead of 2030 compliance deadlines.

Key Report Takeaways

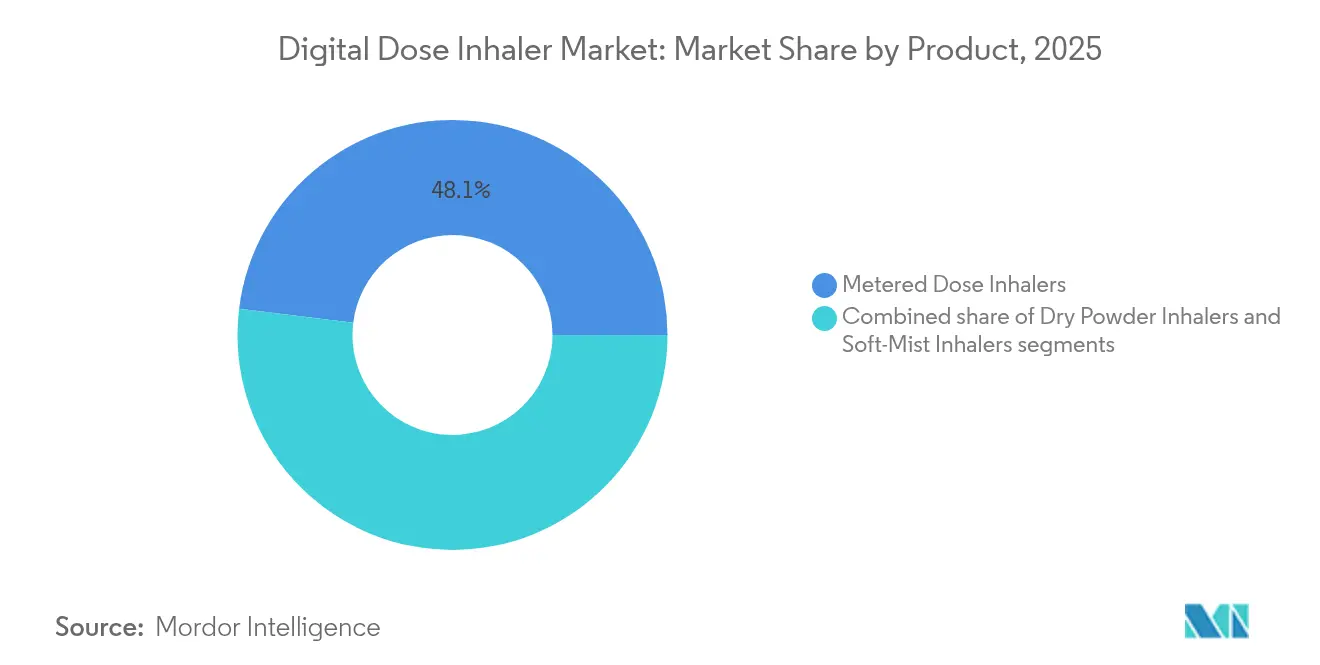

- By product, metered dose inhalers led with 48.05% of digital dose inhaler market share in 2025, while soft-mist inhalers are advancing at a 19.62% CAGR to 2031.

- By indication, asthma accounted for 41.02% share of the digital dose inhaler market size in 2025; cystic fibrosis is projected to expand at a 19.18% CAGR through 2031.

- By type, branded products captured 59.72% revenue share in 2025, whereas generics exhibit the highest projected CAGR at 19.62% to 2031.

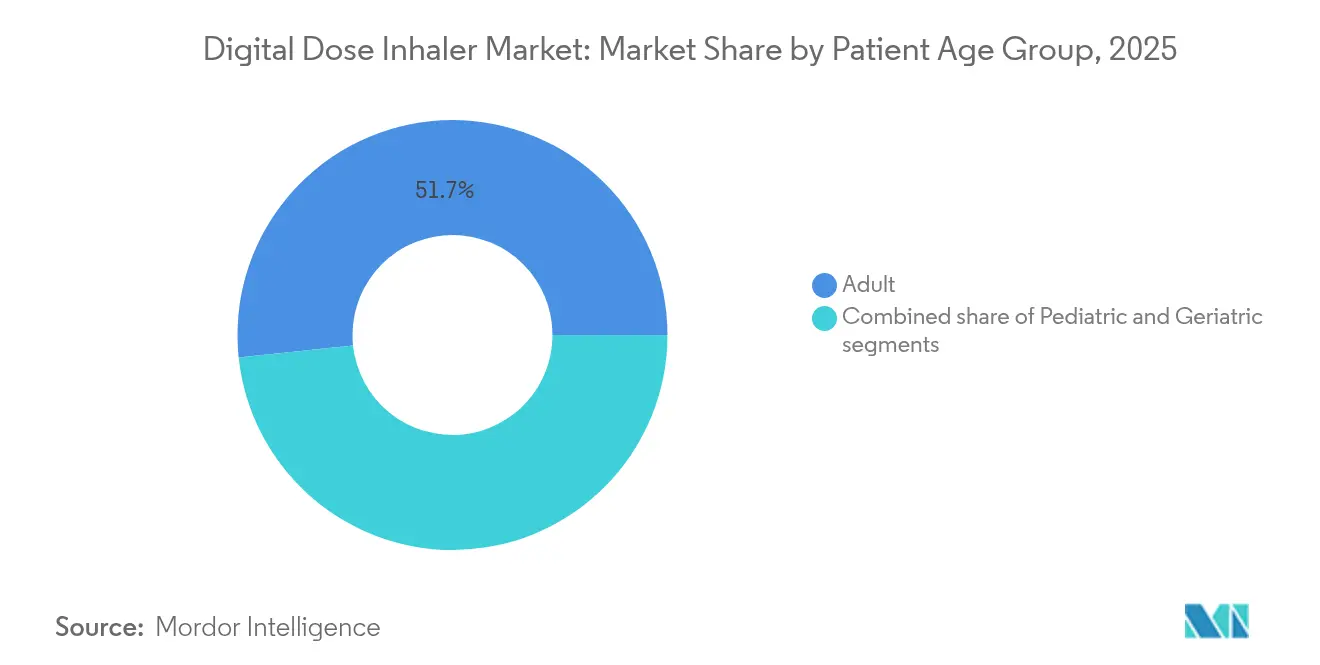

- By patient age, adults held 51.66% share of the digital dose inhaler market size in 2025, and pediatrics is growing at 18.41% CAGR to 2031.

- By distribution channel, retail pharmacies dominated with 46.10% of digital dose inhaler market share in 2025, while online pharmacies are forecast to post a 20.12% CAGR through 2031.

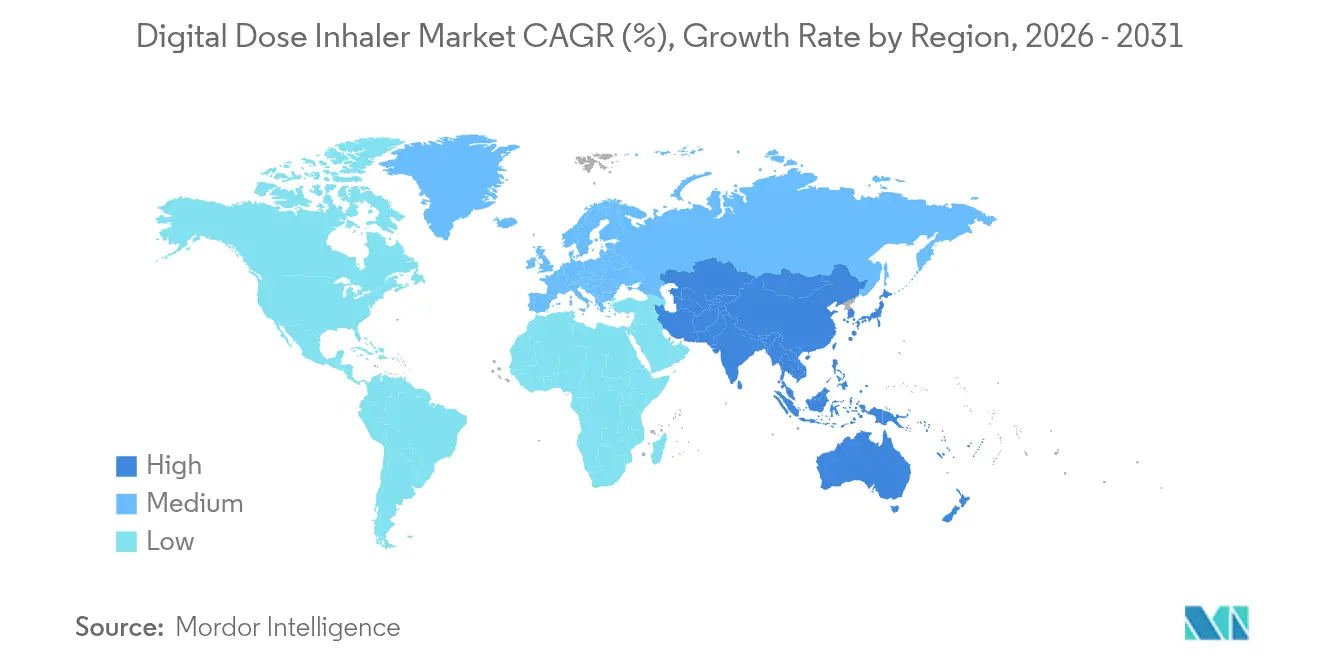

- By geography, North America controlled 42.85% revenue in 2025; Asia-Pacific is the fastest-growing region at a 19.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Dose Inhaler Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Respiratory Disease Burden | +4.2% | Highest in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Expanding Geriatric Patient Pool | +3.1% | North America & Europe; rising in Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements In Smart Inhaler Platforms | +5.8% | North America & Europe lead; Asia-Pacific catching up | Medium term (2-4 years) |

| Transition Toward Digital Therapeutics And Remote Monitoring | +3.7% | Global, with regulatory variations | Medium term (2-4 years) |

| Integration Of Data Analytics And Value-Based Care Models | +2.9% | Primarily North America & Europe | Medium term (2-4 years) |

| Environmental Compliance And Low-Gwp Propellant Adoption | +2.1% | European Union now; global roll-out expected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Respiratory Disease Burden

Chronic respiratory diseases affected 213.39 million people in 2021, sustaining demand for connected inhalers that objectively record adherence. Studies show 44% adherence improvement among COPD patients using behavior-change programs linked to smart devices[1]Ravi Patel, “Behavior-Change Programs Boost COPD Adherence,” Expert Review of Pharmacoeconomics & Outcomes Research, tandfonline.com. Integration of artificial intelligence is enabling early exacerbation alerts, moving digital devices from passive trackers to proactive disease-management tools.

Expanding Geriatric Patient Pool

The geriatric cohort is the fastest-growing user group at an 18.67% CAGR through 2030 as age-related dexterity limitations make intuitive breath-activated devices attractive. Simplified interfaces and larger displays improve usability, while Medicare payment pilots are experimenting with sensor reimbursement, although national coverage remains uneven.

Technological Advancements in Smart Inhaler Platforms

The ProAir Digihaler became the first FDA-cleared inhaler with embedded monitoring, and real-world data from 360 patients captured 53,083 inhalations over 12 weeks, demonstrating granular insight into technique and frequency. Emerging wearables like AI Asthma Guard extend analytics beyond the device to ambient environment and physiology, creating closed-loop management frameworks.

Transition Toward Digital Therapeutics and Remote Monitoring

The FDA Digital Health Center of Excellence is shortening review cycles for combination products, and telemedicine infrastructure built during the COVID-19 pandemic remains in place, allowing inhaler data to flow directly into virtual visits. Real-time dashboards alert clinicians to non-adherence, reducing emergency visits and inpatient days, though high device costs and patient-education needs temper universal deployment[2]Anna Smith, “Artificial Intelligence Enhances Digital Inhaler Adherence,” Frontiers in Digital Health, frontiersin.org.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing Of Connected Inhaler Devices | -2.8% | Greatest in price-sensitive markets worldwide | Short term (≤ 2 years) |

| Complex Regulatory And Reimbursement Pathways | -1.9% | Most challenging in EU and emerging economies | Medium term (2-4 years) |

| Stringent Data Privacy And Cybersecurity Requirements | N/A | Global; strongest where data laws are strict | Medium term (2-4 years) |

| Semiconductor Supply Chain Constraints | N/A | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing of Connected Inhaler Devices

Smart inhalers cost substantially more than conventional units, and total ownership expenses include data plans and software subscriptions. Economic evaluations find clinical benefits but question cost-effectiveness when pharmacy margins are narrow. Tiered pricing and payer partnerships are evolving, yet the lack of consistent reimbursement, especially in public systems, limits penetration in developing regions.

Complex Regulatory and Reimbursement Pathways

Digital inhalers are regulated as drug-device combinations, requiring simultaneous conformity with pharmaceutical and medical-device standards. Manufacturers navigate 510(k) clearances for sensors while maintaining NDA or ANDA status for formulations, prolonging timelines and inflating costs[3]FDA, “Digital Health Center of Excellence Guidance,” U.S. Food and Drug Administration, fda.gov. Data-protection statutes such as GDPR add cybersecurity obligations, and value-based payment models demand extensive real-world evidence before premium price approval.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Metered Dose Inhalers Lead Despite Environmental Pressures

Metered dose inhalers retained 48.05% of digital dose inhaler market share in 2025, underscoring user familiarity and mature manufacturing economics. The digital dose inhaler market size for this segment is projected to rise at a 13.97% CAGR as companies transition to ultra-low-GWP propellants. Environmental mandates are accelerating formulation re-engineering, with AstraZeneca’s HFO-1234ze(E) rollout reducing broad environmental impact by 99.9%.

Soft-mist inhalers provide higher lung deposition and need no propellant, fueling a 19.62% CAGR that outpaces the broader digital dose inhaler market. Device miniaturization and embedded sensors allow real-time flow measurement, appealing to providers seeking precise dose verification. Dry-powder inhalers remain relevant in regions with cooler climates and robust inspiratory flow among adult users, yet high humidity limits uptake in tropical geographies.

By Indication: Asthma Dominance Faces COPD Growth Acceleration

Asthma accounted for 41.02% of revenue in 2025, buoyed by large pediatric and young-adult cohorts and plentiful clinical evidence supporting connected adherence solutions. The digital dose inhaler market size for COPD is expanding faster at 18.56% CAGR as aging populations lengthen disease duration and payers seek cost offsets through fewer hospitalizations. HealthPrize RespiPoints documented a 44% adherence increase among tiotropium users, translating to material cost savings.

Cystic fibrosis growth at 19.18% CAGR demonstrates willingness of caregivers to invest in premium monitoring to optimize high-value medication regimens. AI algorithms now differentiate disease-specific inhalation patterns, personalizing coaching for each indication and raising the clinical relevance of connected platforms.

By Type: Branded Segment Maintains Premium Position

Branded products commanded 59.72% revenue in 2025 as physicians place a premium on consistent aerosol performance and integrated apps. One example is Novartis’ Enerzair Breezhaler, which received European Commission clearance bundled with a sensor and reminder app. Generic entrants are gaining momentum, though duplicating sophisticated digital ecosystems strains development budgets. As exclusivity cliffs appear, partnerships between generic manufacturers and software specialists may narrow the feature gap.

Regulators demand bioequivalence for both medicine and device, further complicating generic smart inhaler launches. Nevertheless, price pressure in public systems is likely to produce hybrid models whereby low-cost device shells pair with subscription-based digital overlays.

By Patient Age Group: Adult Segment Leadership with Pediatric Growth

Adults held 51.66% share in 2025 thanks to expansive insurance coverage and established clinic pathways. Seniors face dexterity challenges, driving refresh cycles toward breath-triggered units with wider mouthpieces and visual dose counters. Pediatric adoption is accelerating at 18.41% CAGR, propelled by child-specific trials such as INHALE-1 evaluating inhaled insulin delivery for young diabetes patients.

User-interface gamification boosts engagement among children, while parental dashboards enable dose confirmation. Withdrawal of certain age-specific corticosteroids in early 2024 illuminated supply vulnerabilities, supporting policy arguments for diversified pediatric portfolios.

By Distribution Channel: Retail Pharmacy Dominance Faces Online Disruption

Retail pharmacies sold 46.10% of units in 2025 because inhaler technique training often happens in person. Chain-pharmacy pilots now incorporate Bluetooth-enabled teaching stations that sync with patient smartphones for later self-assessment. Online pharmacies are set to post a 20.12% CAGR as telehealth legitimacy grows, particularly for chronic-disease refills.

Regulatory reform permitting e-prescriptions for controller inhalers underpins channel migration. Direct-to-consumer storefronts for attachable sensors reinforce cross-sell opportunities, though regulators still require pharmacy fulfilment for medicated canisters.

Geography Analysis

North America generated 42.85% of revenue in 2025 on the back of sophisticated payer systems, high COPD prevalence, and early FDA approvals of digital therapeutics. GSK and Propeller Health broadened their collaboration to ship sensor-enabled Ellipta inhalers nationwide, demonstrating the commercial viability of integrated prescription-tech bundles. Canada benefits from single-payer purchasing leverage, while Provincial formularies are piloting outcome-based procurement tied to adherence reports. Mexico’s growing middle class and digital-health incentives open gateways for mid-priced devices.

Asia-Pacific is the fastest-growing region at 19.12% CAGR through 2031 as urban air pollution and smoking contribute to rising COPD cases. China’s population-level burden pressures policymakers to adopt preventive tools; public hospitals are trialling cloud dashboards that integrate inhaler data with electronic medical records. India’s expanding 4G coverage and revised telemedicine guidelines underpin online pharmacy distribution of sensor kits, yet affordability gaps persist. Japan couples rapidly aging demographics with a mature technology culture, making it a fertile market for premium soft-mist inhalers bundled with AI coaching. Europe remains a mature but innovative market where environmental regulation sets global precedents. The F-Gas Regulation 2024/573 bans new HFC-filled inhalers outside of quota allocations from 2025, accelerating low-GWP adoption schedules. Germany’s DiGA framework reimburses certified digital health apps, positioning inhaler companion software for rapid uptake. The United Kingdom maintains a pragmatic stance, reimbursing devices that demonstrate hospital-admission avoidance. Middle East & Africa and South America are nascent yet promising, limited by infrastructure, clinician training, and consumer purchasing power. Donation programs and tiered pricing models aim to bridge these gaps.

Regulatory Landscape

Digital dose inhalers typically fall under drug-device combination product oversight in major markets, which pushes compliance beyond aerosol performance to software-as-a-medical-device controls, cybersecurity, and interoperability. In the United States, FDA oversight commonly pairs drug pathways (NDA/ANDA) with device review for embedded sensing and related software functions, supported by FDA digital health guidance activity, including a January 2026 final guidance on clinical decision support software that clarifies when software falls under full device requirements.

In Europe, manufacturers manage EU MDR conformity assessment alongside medicines regulation. The EU AI Act (Regulation (EU) 2024/1689), in force since August 1, 2024, raises compliance obligations for AI-enabled medical-device software that can be classified as high-risk. Environmental rules also shape pMDI portfolios: the EU F-Gas Regulation 2024/573 became effective in January 2025, tightening conditions for HFC propellants and accelerating low-GWP transitions that affect both formulation change control and device recertification strategies.

Value Chain Analysis

The value chain separates into (1) pharmaceutical development and manufacturing (API, formulation, canister filling, and inhaler assembly) and (2) electronics and software (sensors, connectivity modules, firmware, mobile apps, cloud analytics, and cybersecurity maintenance). Integration often happens through specialized inhalation CDMOs and device engineering partners that can combine dose-delivery hardware validation with software lifecycle management, then support post-market surveillance and real-world evidence generation for payers and regulators.

Upstream constraints concentrate around precision components and qualified electronics, where sourcing, validation, and traceability requirements are stricter than for conventional inhalers, and semiconductor availability can create lead-time volatility. Midstream, quality and regulatory documentation expands due to change-management needs when propellants or digital modules are updated, reinforced by EMA implementation of an updated scientific guideline on the pharmaceutical quality of inhalation and nasal medicinal products (Revision 1), effective January 2, 2026. Downstream, distribution remains anchored in retail and hospital pharmacies for training and refill continuity, while online pharmacy fulfillment grows where e-prescribing and telehealth workflows support app-linked adherence monitoring.

Competitive Landscape

The digital dose inhaler market shows moderate consolidation, with incumbents acquiring specialized design firms to lock in end-to-end capabilities. Molex finalized its purchase of Vectura Group through Phillips Medisize, combining component miniaturization expertise with large-scale manufacturing. Altaris merged Kindeva Drug Delivery with Meridian Medical Technologies to create a hybrid CDMO spanning inhalers, autoinjectors, and transdermal patches, signaling a trend toward platform-agnostic drug-delivery contractors.

Technology alliances are equally influential. Teva collaborated with Amazon Web Services to analyze inhalation flow data, improving predictive algorithms for asthma attack risk. Start-ups offer disruptive innovation: Aevice Health raised USD 7 million to commercialize a wearable stethoscope that pairs with inhaler data streams to validate symptom-dose relationships. Intellectual-property filings in closed-loop vapor delivery and acoustic technique analysis are proliferating, indicating competitive differentiation is shifting from formulation to data science.

Regulatory expertise has emerged as a competitive asset. Firms with established quality-management systems and cybersecurity certifications secure faster approvals, shortening time-to-market. Market entry for new players is possible but resource-intensive, encouraging collaboration over direct confrontation.

Digital Dose Inhaler Industry Leaders

Teva Pharmaceutical Industries

GlaxoSmithKline plc

AstraZeneca plc

Boehringer Ingelheim

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity is scaling embedded connectivity from pilot programs into routine care pathways that reimburse clinician review of patient-generated adherence and technique data. Remote therapeutic monitoring reimbursement in the United States (using CPT coding structures for reviewing transmitted data) supports commercial models that bundle inhalers, apps, and dashboards, and collaborations such as GSK and Propeller Health to ship sensor-enabled Ellipta inhalers show how prescription therapeutics and digital platforms are being commercialized together.

Environmental compliance is also creating a second opportunity track: re-engineering high-volume pMDIs around lower-GWP propellants while preserving (or adding) digital features to maintain differentiation. Company actions underline the direction, including AstraZeneca filings in March 2025 for HFO-1234ze(E) pMDIs and GSKs October 2025 pivotal Phase III data for a next-generation low-carbon Ventolin (HFA-152a) version. These moves drive device, manufacturing, and quality-system changes that can be paired with digital dose tracking and connected-care services. Expansion of complex inhalation programs and new entrants into respiratory MDIs, such as Amneals April 2026 US launches in metered-dose inhalation products, also increases the addressable base for integrated digital platforms, where manufacturers can embed electronics at the device-design stage rather than relying on detachable add-ons.

Recent Industry Developments

- May 2026: Chance Pharma reported that Chinas NMPA accepted its NDA for the CXG87 budesonide/formoterol dry powder inhaler after positive Phase 3 results. The filing expands late-stage inhalation pipelines in a market where cloud-connected care is being trialed in public hospitals, increasing the value of pairing new inhalers with integrated monitoring and data workflows.

- March 2025: AstraZeneca filed in the EU, UK, and China for HFO-1234ze(E) pressurized metered-dose inhalers as part of its low-GWP transition program. The filings increase formulation and device change-control activity across multiple regulators, tightening development timelines for companies that also need to maintain software, connectivity, and cybersecurity compliance in connected inhaler portfolios.

- August 2024: Aevice Health secured USD 7 million seed-plus funding to scale its wearable respiratory monitoring platform in the United States, Japan, and Singapore. The financing supports broader data-stream integration around respiratory management, strengthening the set of data sources that digital dose inhalers rely on for validation of symptoms, adherence, and outcomes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers inhaler devices with built in electronics that capture dose events, time stamp usage, and share data to a paired app or system to support respiratory disease management and adherence tracking.

Scope exclusions: Excludes nebulizers, add on sensor sleeves that clip onto a standard inhaler, and purely mechanical inhalers without onboard dose logging.

Segmentation Overview

- By Product

- Dry Powder Inhalers

- Metered Dose Inhalers

- Soft-Mist Inhalers

- By Indication

- COPD

- Asthma

- Cystic Fibrosis

- Other Respiratory Disorders

- By Type

- Branded

- Generic

- By Patient Age Group

- Pediatric

- Adult

- Geriatric

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the demand pool for asthma and COPD, then linking that to device adoption and replacement cycles.

We mainly used public health and epidemiology series such as the US CDC and WHO, alongside regulator and guidance sources such as FDA and the European Medicines Agency, to determine which digital functions are typically counted as part of the device. To keep the model grounded in real shipments and pricing direction, we reviewed customs and trade signals where available, such as UN Comtrade, plus policy and reimbursement context such as CMS and OECD health statistics. We also checked company filings, earnings decks, and clinical publications on adherence outcomes to confirm launch timing and usage patterns, and we used credible press as a cross-check.

Paid subscriptions were used only for company financials and patent landscapes, so device pipelines and revenue mixes could be sanity checked. These sources are illustrative, and we used other public references as well to support data capture, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to test what buyers actually pay for, device only versus device plus software enablement, and how adoption differs by care setting. We spoke with a mix of device stakeholders, care providers, and distribution side experts across major regions so assumptions on attach rates, connectivity usage, and replacement timing could be adjusted before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 42% | EMEA: 37% |

| Smaller Players: 17% | Managers: 45% | Americas: 21% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where treated asthma and COPD populations are converted into an addressable inhaler demand pool using therapy mix and device utilization patterns, then filtered through the share that is digitally enabled.

Results are cross checked with selective bottom-up approximations. For example, we reviewed typical device ASP ranges and applied them to implied unit volumes by region, then used distributor and channel feedback to adjust outliers. Key inputs in the model include asthma and COPD prevalence and treatment rates, annual inhaler usage per patient, digital adoption or penetration by care setting, average selling price progression for connected devices, replacement cycle and durability assumptions, and the pace of regulatory clearances and launches that affect availability. For forecasting, scenario analysis was used so conservative and aggressive adoption paths could be tested, and then the scenarios were aligned to what primary respondents viewed as practical for reimbursement and provider workflow.

Where bottom-up signals were incomplete in smaller countries, we applied regional ratios and then validated against healthcare spend and diagnosis volume so the totals remained realistic.

Data Validation & Update Cycle

Outputs are validated in multiple passes by comparing the model against independent signals, including regional respiratory diagnosis volumes, connected device uptake indicators, and visible shipment or import trends.

When a large variance shows up by region or year, we revisit the underlying assumption and, if needed, re contact experts to confirm whether the change reflects a real shift or data noise. Before sign off, the sizing logic and calculations are reviewed by another analyst to catch inconsistencies in units, currency timing, and adoption steps.

The report is refreshed annually, and interim updates are made when material events occur, such as major approvals, pricing shifts, or reimbursement moves. Right before delivery, a final pass is done so clients receive the most current view available at that time.

Mordor Intelligence's Digital Dose Inhaler Market Size Compared Against Other Published Estimates

Published numbers for this market can look far apart because the device definition is not consistent across sources, and the year used as the starting point also varies.

Differences also come from how quickly adoption is assumed to move from pilot programs into routine prescribing, and from whether pricing is treated as stable or rising with added software features. Add on sensor sleeves that attach to a standard inhaler sit outside Mordor Intelligence's scope, which keeps the totals closer to digitally integrated inhalers rather than broader connected respiratory add ons. Other estimates may use earlier base years, assume penetration jumps without checking treated patient pools, or blend device revenues with wider digital therapeutics value, which can inflate the stated market size.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.15 B (2025) | |

| Trade Journal A | USD 3.20 B (2023) | Uses an earlier base year and a narrower definition that can undercount digitally integrated inhalers in later years, and it is not always clear how regional roll ups and pricing escalation are handled. |

| Global Consultancy B | USD 4.90 B (2024) | Blends multiple smart inhaler configurations and connectivity features, and the inclusion of broader connected respiratory devices can push totals away from embedded dose logging inhalers only. |

The spread in the table is mainly explained by product scope and by the year selected for the stated market value, and those two items can shift totals quickly in a fast growing category. By anchoring the model to treated patient demand, realistic digital penetration, and repeatable ASP assumptions, the resulting number stays traceable and easier to reconcile when readers compare it with other published figures.

Key Questions Answered in the Report

What is the current digital dose inhaler market size?

The market stands at USD 21.41 billion in 2026 and is forecast to reach USD 48.74 billion by 2031.

Which product type leads the digital dose inhaler market?

Metered dose inhalers hold 48.05% market share due to clinical familiarity, although soft-mist inhalers are growing fastest.

How do environmental regulations influence inhaler design?

The EU F-Gas Regulation 2024/573 bans high-GWP propellants, prompting rapid adoption of alternatives like HFO-1234ze(E).

Which region is expected to grow most rapidly?

Asia-Pacific shows the highest CAGR at 19.12% through 2031, driven by rising disease incidence and expanding digital health infrastructure.

What are the main barriers to smart inhaler adoption?

Premium device pricing and complex regulatory-reimbursement pathways limit widespread uptake, especially in price-sensitive markets.

How do smart inhalers improve patient outcomes?

Sensors provide real-time adherence data, AI predicts exacerbations, and remote monitoring reduces emergency visits and hospitalizations.

Page last updated on: