Fruit Pectin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

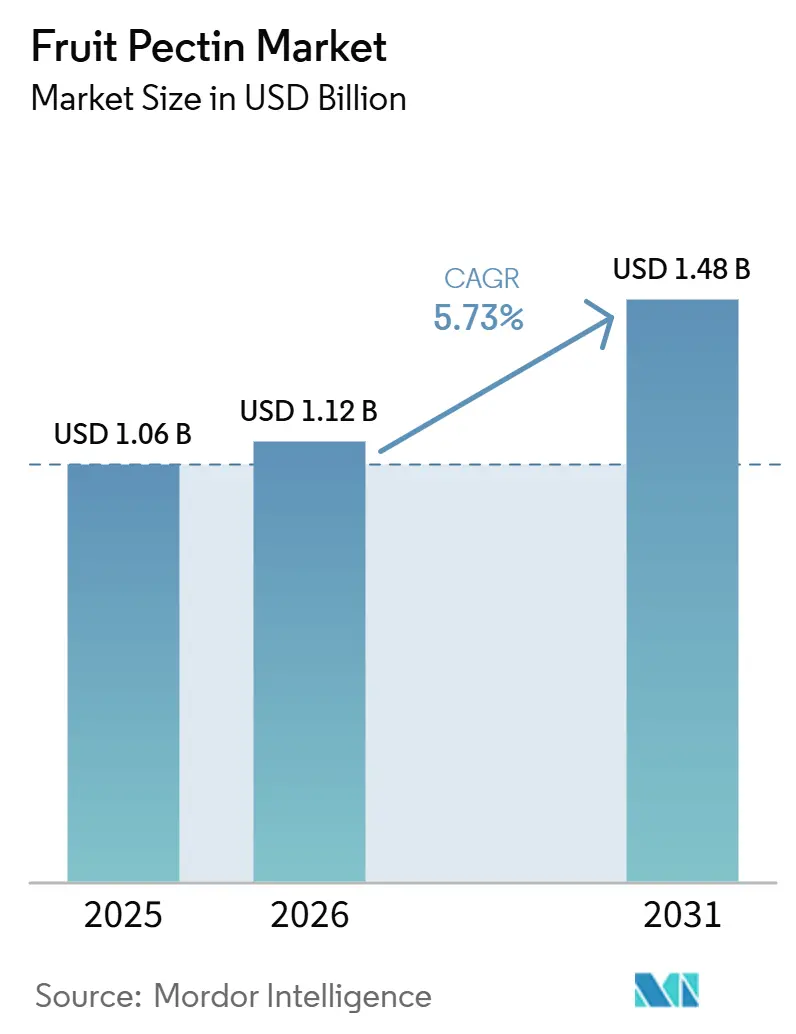

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

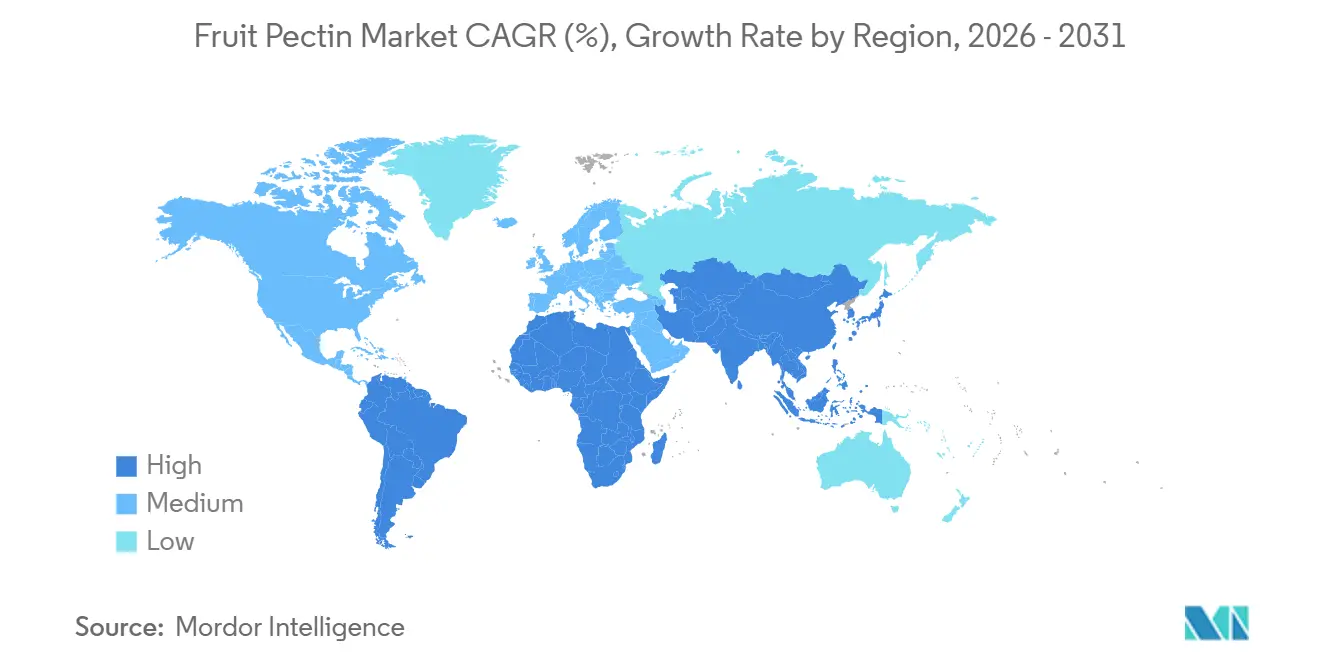

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

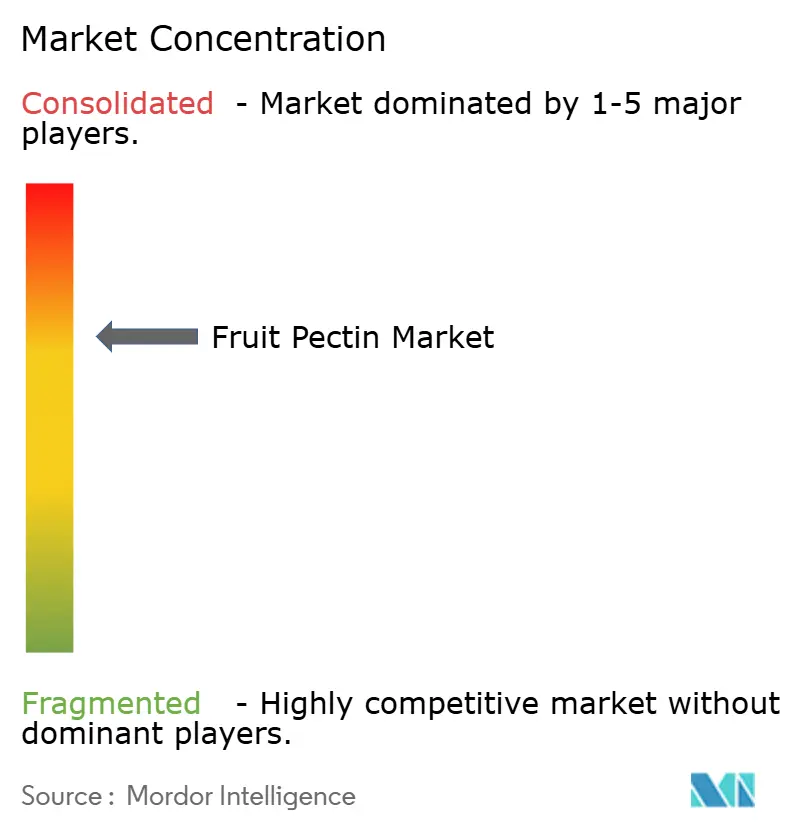

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruit Pectin Market Analysis by Mordor Intelligence

The fruit pectin market size is expected to increase from USD 1.06 billion in 2025 to USD 1.12 billion in 2026 and reach USD 1.48 billion by 2031, growing at a CAGR of 5.73% over 2026-2031. The market is being driven by several factors, including the rising demand for clean-label products, growing interest from the pharmaceutical industry in pH-responsive gel matrices, and advancements in green extraction technologies. These factors are expanding the applications of pectin beyond traditional uses like jams and jellies. By source, citrus fruits remain the primary raw material, forming the backbone of the supply chain due to their high pectin content. In terms of type, low-methoxyl pectin is gaining popularity, aligning with consumers' increasing preference for reduced-sugar products. Regarding applications, the pharmaceutical sector is emerging as a significant growth area, with pectin used in innovative drug-delivery systems and other medical applications. The market is moderately consolidated, with a few key players dominating the competitive landscape.

Key Report Takeaways

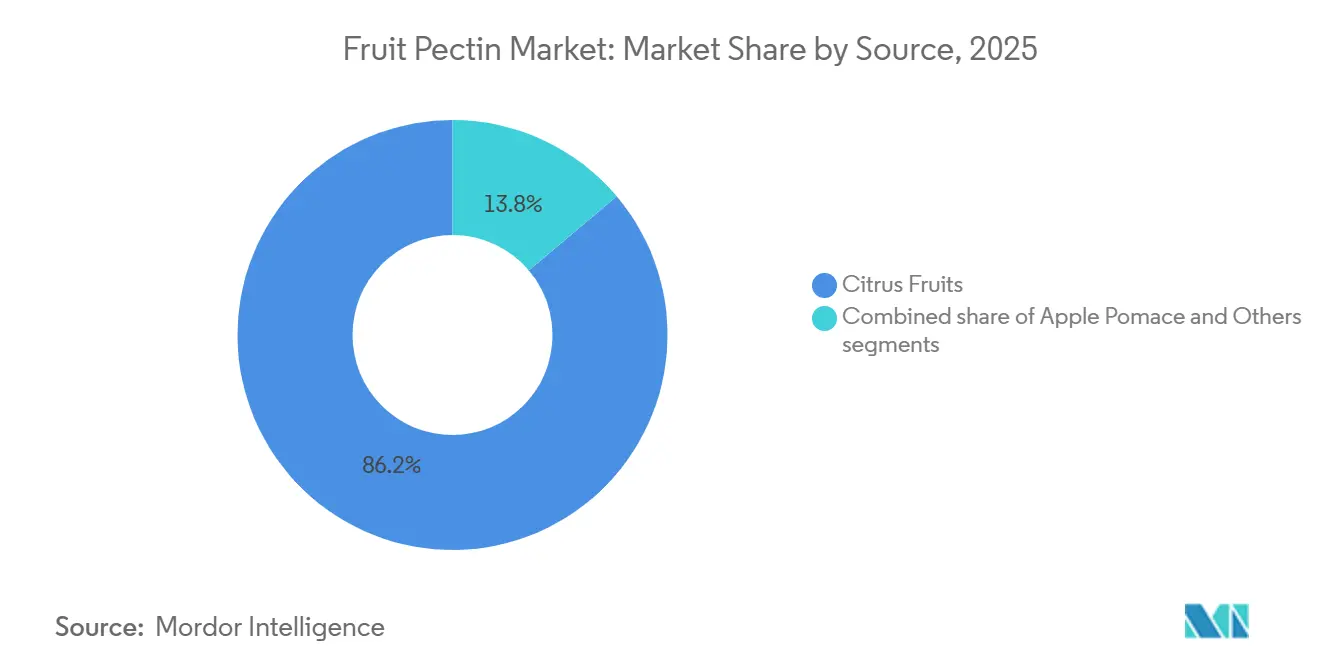

- By source, citrus peels commanded 86.17% of the fruit pectin market share in 2025, whereas apple pomace is projected to expand at a 7.54% CAGR between 2026 and 2031, the fastest among raw-material sources.

- By type, high-methoxyl grades accounted for 67.53% of the 2025 fruit pectin market size, while low-methoxyl grades are forecast to grow at a 6.45% CAGR through 2031.

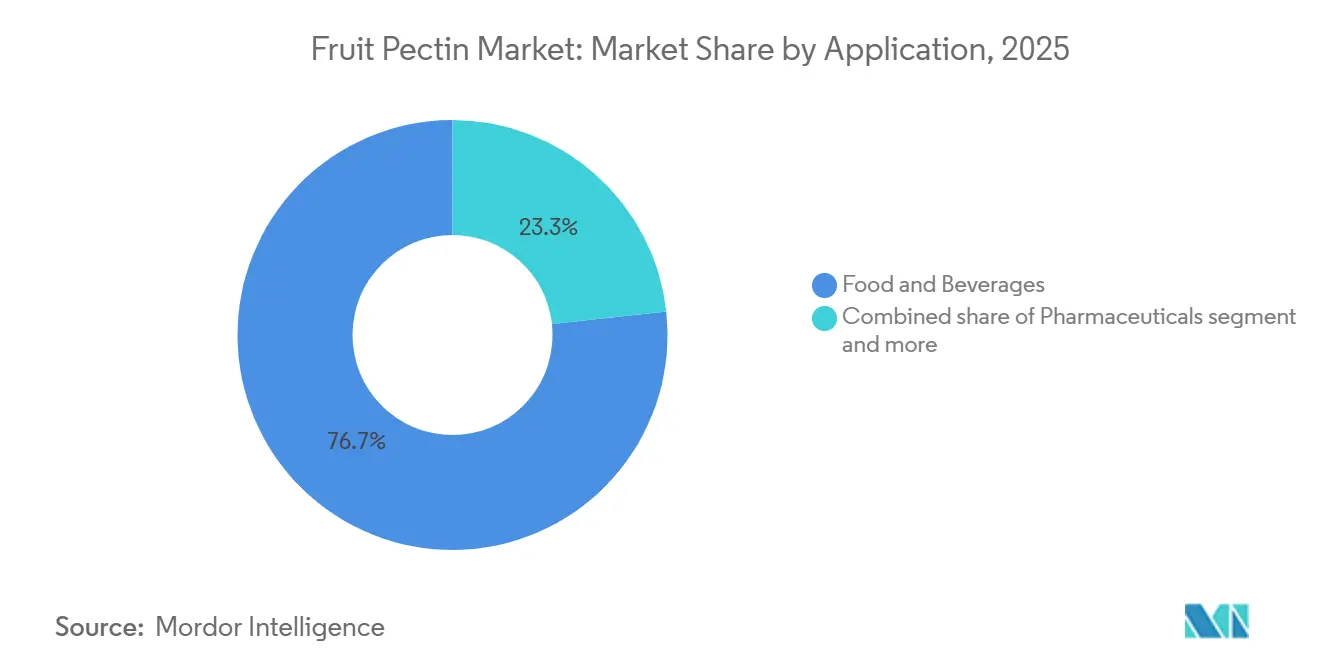

- By application, food and beverages led the fruit pectin market in 2025, with a 76.74% share; pharmaceuticals are the fastest-growing application, with a 6.27% CAGR to 2031.

- By geography, Europe led with 43.11% fruit pectin market share in 2025, and Asia-Pacific registered the highest 7.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fruit Pectin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for low-sugar, sugar-free, and functional food products | +1.2% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Popularity of fruit-based beverages and ready-to-eat products | +1.0% | Global, strongest in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Consumer preference for clean-label and natural ingredients | +0.9% | North America and Europe, expanding to urban Asia-Pacific markets | Medium term (2-4 years) |

| Advancements in extraction and processing technologies | +0.7% | Global, led by European and North American Research and Development hubs | Long term (≥ 4 years) |

| Increasing consumer awareness of digestive health and dietary fiber intake | +0.8% | Global, particularly strong in North America and Australia | Medium term (2-4 years) |

| Expanding applications in pharmaceuticals and personal care products | +0.6% | Asia-Pacific and North America, with niche growth in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for low-sugar, sugar-free, and functional food products

The growing demand for low-sugar, sugar-free, and functional food products is significantly driving the global fruit pectin market. According to the International Food Information Council (IFIC) Food and Health Survey 2025, around 62% of United States consumers are concerned about their sugar intake. Among them, 24% are extremely concerned, while 39% are somewhat concerned[1]Source: International Food Information Council, "2025 IFIC Food and Health Survey", ific.org. This indicates a clear shift toward healthier eating habits. To meet this demand, manufacturers are increasingly using low-methoxyl pectin, which can reduce added sugar by up to 50% while maintaining the desired texture in products like jams, fruit yogurts, and bakery fillings. Additionally, pectin is classified as a soluble dietary fiber, which supports health-related claims on product packaging. This aligns with regulatory requirements and the growing consumer preference for clean-label and natural ingredients, further boosting its adoption in the food industry.

Increasing consumer awareness of digestive health and dietary fiber intake

Growing consumer awareness of the importance of digestive health and dietary fiber intake is driving the global fruit pectin market. Pectin, a natural soluble fiber, plays a vital role in improving gut health, aiding digestion, and managing cholesterol levels. These benefits make it an ideal ingredient for functional food products. According to Frontiers in 2025, the recommended daily fiber intake is 25 grams for women and 38 grams for men under 51 years old[2]Source: Frontiers Org, "Association Between Dietary Fiber Intake and Abesity in US Adults", frontiersin.org. However, many individuals fall short of these recommendations, creating a significant gap in fiber consumption. To address this, food manufacturers are increasingly adding fiber-rich ingredients such as pectin to a range of products, including beverages, dairy products, and snacks. The growing demand for clean-label and health-focused products is further boosting the use of pectin across various industries. This trend highlights the expanding role of pectin in meeting consumer preferences for healthier and more functional food options.

Consumer preference for clean-label and natural ingredients

The increasing demand for clean-label, natural ingredients is a key driver of the global fruit pectin market. Pectin, extracted from citrus peels and apple pomace, aligns with growing consumer preferences for products without artificial additives and supports clear, transparent labeling. According to the International Food Information Council (IFIC) Food and Health Survey 2025, approximately 53% of United States consumers actively review ingredient lists when shopping, underscoring the importance of using familiar, natural ingredients in products[3]Source: International Food Information Council, "2025 IFIC Food and Health Survey", ific.org. Furthermore, pectin can obtain certifications such as Non-GMO and organic, making it a more attractive option compared to synthetic thickeners. This alignment with clean-label trends has significantly boosted its use across food and beverage applications, including jams, jellies, and dairy products, as well as in emerging areas such as plant-based and reduced-sugar formulations.

Expanding applications in pharmaceuticals and personal care products

The growing use of fruit pectin in pharmaceuticals and personal care products is a major driver of the global market. In the pharmaceutical sector, pectin is being used in advanced drug delivery systems, such as gastro-retentive formulations. These systems allow medications to be released slowly over up to 12 hours, helping patients adhere to their treatment plans more effectively. Meanwhile, in the personal care industry, especially in Asian beauty markets, pectin is gaining popularity for its natural, film-forming properties. It is being incorporated into biodegradable, plant-based products, aligning with the rising demand for sustainable, eco-friendly solutions. These specialized applications are expanding pectin's role beyond its traditional use in food products, significantly boosting demand across various industries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and extraction costs compared to synthetic alternatives | -0.5% | Global, most acute in regions with limited citrus/apple processing infrastructure | Short term (≤ 2 years) |

| Competition from alternative hydrocolloids such as gelatin, carrageenan, and xanthan gum | -0.4% | Global, particularly in price-sensitive emerging markets | Medium term (2-4 years) |

| Price volatility of raw materials due to climate conditions | -0.6% | South America and Mediterranean Europe, with spillover to global supply chains | Short term (≤ 2 years) |

| Regulatory variations across regions regarding food additives and labeling | -0.3% | Global, with divergent standards in Asia-Pacific, Middle East and Africa, and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from alternative hydrocolloids such as gelatin, carrageenan, and xanthan gum

Competition from other hydrocolloids, such as gelatin, carrageenan, and xanthan gum, is a significant challenge for the fruit pectin market. These alternatives offer specific benefits, such as improved texture, better stability, and higher efficiency, often requiring smaller quantities to achieve desired results. This makes them appealing to manufacturers, especially in cost-sensitive industries. In applications such as confectionery and dairy, these substitutes are often preferred for their proven performance and cost-effectiveness. To stay competitive, pectin suppliers are developing blended and enhanced formulations. However, these efforts can sometimes compromise pectin's clean-label appeal, which is a key factor for differentiation in certain markets. As a result, pectin faces limitations in maintaining its unique position in some end-use applications.

High production and extraction costs compared to synthetic alternatives

High production and extraction costs remain a significant challenge for the fruit pectin market. Producing pectin depends on raw materials like citrus peels and apple pomace, which are seasonal and need to be processed quickly to avoid spoilage. This adds complexity to the supply chain. Furthermore, the extraction process, which involves acid treatment and purification, requires substantial energy and resources, further driving up costs. As a result, pectin is more expensive compared to synthetic or alternative hydrocolloids. This price difference makes it difficult for manufacturers, especially in cost-sensitive regions like emerging markets, to adopt pectin widely. Despite its appeal as a natural and clean-label ingredient, the high costs limit its broader use in various applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Citrus Commands the 2025 Landscape

Citrus-based raw materials hold a dominant position in the fruit pectin market, contributing to 86.17% of the market share in 2025. This dominance is primarily due to the abundant availability of citrus peels, especially from orange and lemon processing industries, which provide high pectin yields at a lower cost. Citrus-derived pectin is widely preferred by food and beverage manufacturers because of its consistent quality and excellent gelling properties. Additionally, the well-established supply chain for citrus-based pectin further strengthens its market leadership across regions.

On the other hand, apple-derived pectin is gradually gaining traction and is expected to grow at a CAGR of 7.54% between 2026 and 2031. The increasing demand for clean-label and naturally sourced ingredients has boosted the use of apple pomace as a sustainable raw material for pectin production. Apple-based pectin is particularly popular in premium and specialty applications due to its unique functional properties and its perception as a more natural alternative. Although smaller in market share compared to citrus-based pectin, this segment is anticipated to see steady growth as consumer preferences shift toward sustainable and natural products.

By Type: High-Methoxyl Still Dominant

High-methoxyl (HM) pectin remains the leading type in the fruit pectin market, holding 67.53% of the total market share in 2025. Its popularity stems from its widespread use in traditional products such as jams, marmalades, and other high-sugar fruit-based items, where it helps create a gel-like texture. Manufacturers prefer HM pectin because it works well with high-sugar formulations and delivers consistent results. This makes it a key ingredient in the large-scale production of processed fruit products, ensuring its continued dominance in the market.

In contrast, low-methoxyl (LM) pectin is experiencing steady growth and is expected to grow at a CAGR of 6.45% through 2031. The rising demand for low-sugar, reduced-calorie, and diabetic-friendly food products is driving this growth, as LM pectin can form gels without relying heavily on sugar. It is increasingly used in functional foods, dairy products, and health-focused formulations, catering to the growing consumer preference for healthier options. As a result, LM pectin is gaining more attention and is becoming an important choice for manufacturers targeting health-conscious consumers.

By Application: Food Leads, Pharma Rises

The food and beverages segment is the largest contributor to the global fruit pectin market, accounting for 76.74% of the total market share in 2025. This dominance is primarily due to the widespread use of pectin as a gelling, thickening, and stabilizing agent in products such as jams, jellies, dairy products, and baked goods. Its ability to enhance texture and improve product stability makes it a preferred choice for manufacturers. Additionally, the growing demand for processed and convenience foods further drives the adoption of pectin in this segment, as consumers increasingly seek ready-to-eat and shelf-stable products.

The pharmaceutical segment, while smaller, is expected to grow steadily at a 6.27% CAGR between 2026 and 2031. This growth is fueled by the rising use of pectin in drug delivery systems, wound care products, and as a dietary fiber supplement. Pectin’s natural origin, safety, and compatibility with medical formulations make it an attractive ingredient for pharmaceutical and nutraceutical applications. As consumers become more health-conscious and seek functional ingredients in their products, the role of pectin in the pharmaceutical sector is anticipated to expand significantly in the coming years.

Geography Analysis

Europe was the largest market for fruit pectin in 2025, accounting for 43.11% of total revenue. The region’s leadership is driven by its strong focus on clean-label products and strict food safety regulations, which have boosted the demand for high-quality pectin in food applications. Additionally, Europe benefits from well-established manufacturing facilities and efficient supply chains, ensuring a steady flow of pectin to meet market needs. These factors have solidified Europe’s position as a key player in the fruit pectin market.

The Asia-Pacific region is expected to grow at the fastest rate, with a projected CAGR of 7.25% through 2031. This growth is fueled by increasing urbanization, rising demand for convenience foods, and the expanding use of processed fruit products. Emerging economies in the region are witnessing shifting dietary preferences and rapid development of the retail sector, creating significant opportunities for pectin applications. Both food and non-food industries in Asia-Pacific are likely to adopt pectin at a higher rate, contributing to the region’s rapid market expansion.

North America is anticipated to see steady growth, driven by consumers' growing preference for clean-label, low-sugar products. South America plays a critical role in the global supply chain as a major supplier of raw materials, particularly citrus peels used in pectin production. Meanwhile, the Middle East and Africa are emerging markets where demand is gradually increasing due to the growth of food processing industries. Together, these regions contribute to a balanced global market, with both established and developing markets shaping the overall demand for fruit pectin.

Competitive Landscape

The fruit pectin market is moderately consolidated, with a few large global companies and several mid-sized players competing. Major companies like Tate & Lyle and DSM-Firmenich have expanded their market presence through acquisitions and by broadening their product portfolios. These companies offer a wide range of products, enabling food manufacturers to source multiple ingredients from a single supplier. This strategy not only improves their global reach but also enhances their ability to efficiently meet the diverse needs of various industries.

Mid-sized companies, such as Ceamsa and Krishna Pectins, also play a significant role in the market. These firms focus on sourcing raw materials locally, maintaining flexible production processes, and building strong customer relationships. By offering tailored solutions and responding quickly to market demands, they successfully cater to niche segments. This balance between global leaders and regional players creates a competitive, dynamic market environment in which both types of companies contribute to overall growth.

Advancements in technology and regulatory requirements also shape the competitive landscape of the fruit pectin market. Companies are investing in innovative extraction methods and developing new products to improve efficiency and expand the range of applications for pectin. At the same time, strict quality and safety regulations, especially in developed regions, make it challenging for new entrants to compete. These factors ensure that the market remains competitive while maintaining a stable structure, driven by innovation and compliance with industry standards.

Fruit Pectin Industry Leaders

-

Herbstreith & Fox GmbH

-

Cargill Inc.

-

International Flavors & Fragrances (IFF)

-

Tate & Lyle PLC

-

DSM-Fermenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSM-Firmenich increased its stake in Yantai DSM Andre Pectin Company Limited from 75% to 90.5% by acquiring an additional 15.5% of shares, strengthening its position in the specialty food ingredient market. Andre Pectin, a leading producer of apple and citrus pectin, continues to have 9.5% of shares held by Rich Spring Holdings Limited.

- March 2025: Cargill introduced a cost-effective pectin replacer designed as an alternative to expensive pectin used in gummies and jellies, targeting value-conscious consumers in India. This innovation, showcased alongside bake-stable fillings and other functional blends, highlights Cargill's commitment to delivering versatile, high-quality solutions for the evolving food industry.

- November 2024: Tate & Lyle completed its acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business with enhanced capabilities in natural ingredients such as pectin and specialty gums.

Global Fruit Pectin Market Report Scope

Fruit pectin is a natural soluble fiber found in the cell walls of fruits, commonly used as a gelling agent in jams, jellies, and food products. The global fruit pectin market is segmented into source, type, application, and geography. Based on the source, the market is classified into citrus fruits, apple pomace, and others. Based on type, the market is classified into high-methoxyl pectin and low-methoxyl pectin. Based on application, the market is classified into food and beverages, pharmaceuticals, beauty and personal care, and other applications. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Citrus Fruits | Orange |

| Lemon Peel | |

| Others | |

| Apple Pomace | |

| Others |

| High Methoxyl Pectin |

| Low Methoxyl Pectin |

| Food and Beverages |

| Pharmaceuticals |

| Beauty and Personal Care |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Citrus Fruits | Orange |

| Lemon Peel | ||

| Others | ||

| Apple Pomace | ||

| Others | ||

| By Type | High Methoxyl Pectin | |

| Low Methoxyl Pectin | ||

| By Application | Food and Beverages | |

| Pharmaceuticals | ||

| Beauty and Personal Care | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the fruit pectin market by 2031?

It is forecast to reach USD 1.48 billion, expanding at a 5.73% CAGR from 2026-2031.

Which raw material dominates commercial pectin production?

Citrus peel provided 86.17% of global supply in 2025, anchored by Brazil and Spain.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to post a 7.25% CAGR on rising demand for convenience beverages and dairy alternatives.

Why are low-methoxyl pectins gaining traction?

They gel with calcium instead of sugar, enabling reduced-sugar products that comply with global sugar-tax regimes.

Page last updated on: