Infrastructure Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

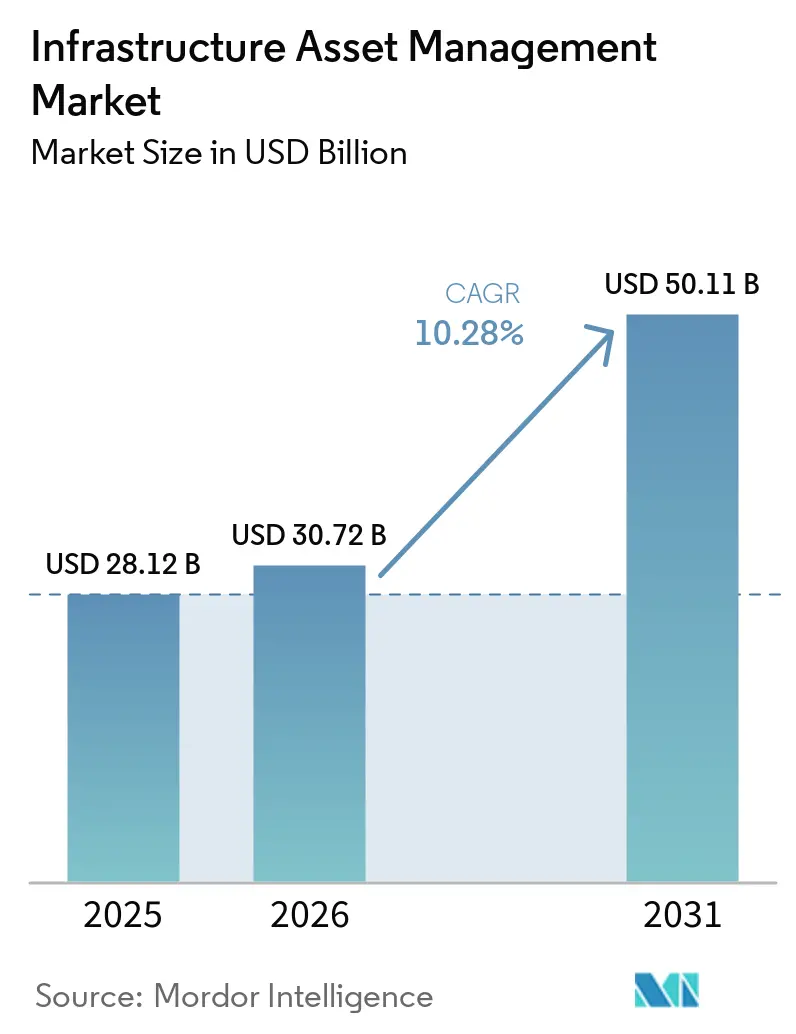

| Market Size (2026) | USD 30.72 Billion |

| Market Size (2031) | USD 50.11 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

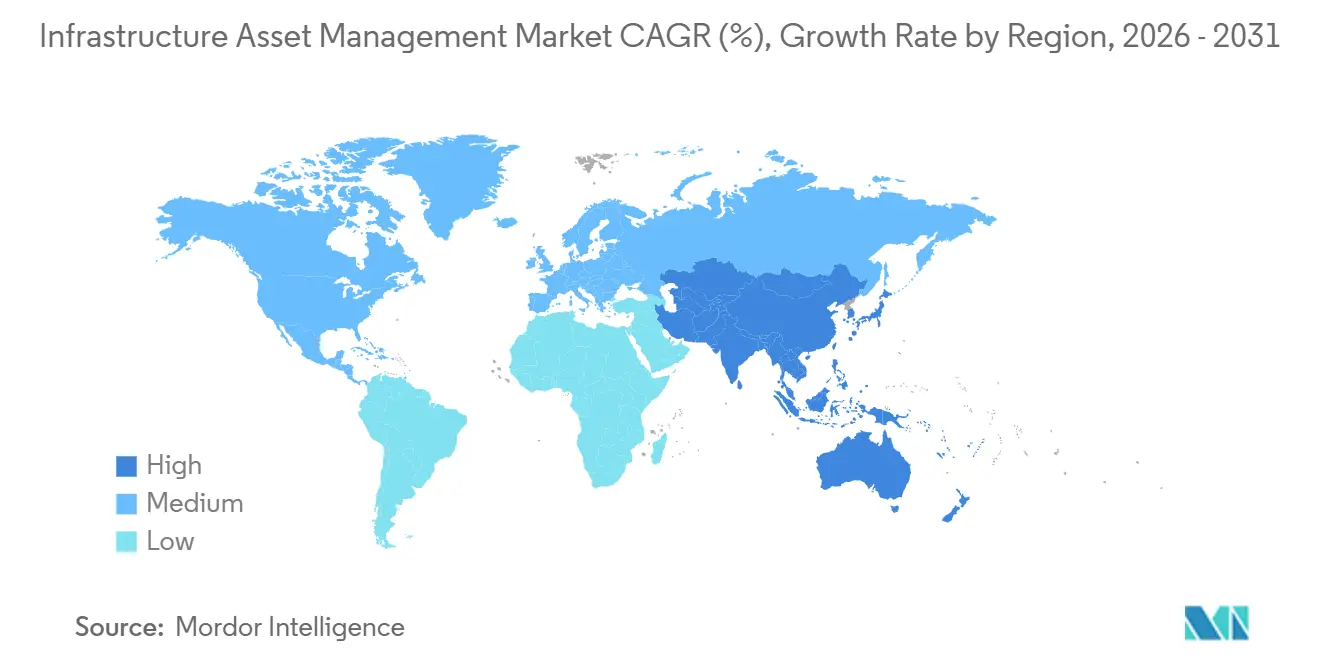

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infrastructure Asset Management Market Analysis by Mordor Intelligence

The infrastructure asset management market size is expected to increase from USD 28.12 billion in 2025 to USD 30.72 billion in 2026 and reach USD 50.11 billion by 2031, growing at a CAGR of 10.28% over 2026-2031. Growth remains tied to a basic cost reality because owners cannot defer maintenance, inspection, and renewal decisions for long without increasing failure risk and replacement expense. Public spending has improved in several major economies, yet the funding gap across aging transport, water, and energy networks is still large enough to keep digital asset planning high on investment agendas. Demand is also widening from core software into implementation, consulting, and managed services because many asset owners do not have the internal teams needed to configure analytics-heavy platforms. Cloud deployment is gaining ground because it reduces hardware burden and supports faster use of geospatial data, condition data, and workflow automation across distributed infrastructure portfolios. At the same time, adoption is being shaped by implementation cost, legacy interoperability issues, cybersecurity readiness, and national data-location rules that favor localized service models over fully standardized global rollouts.

Key Report Takeaways

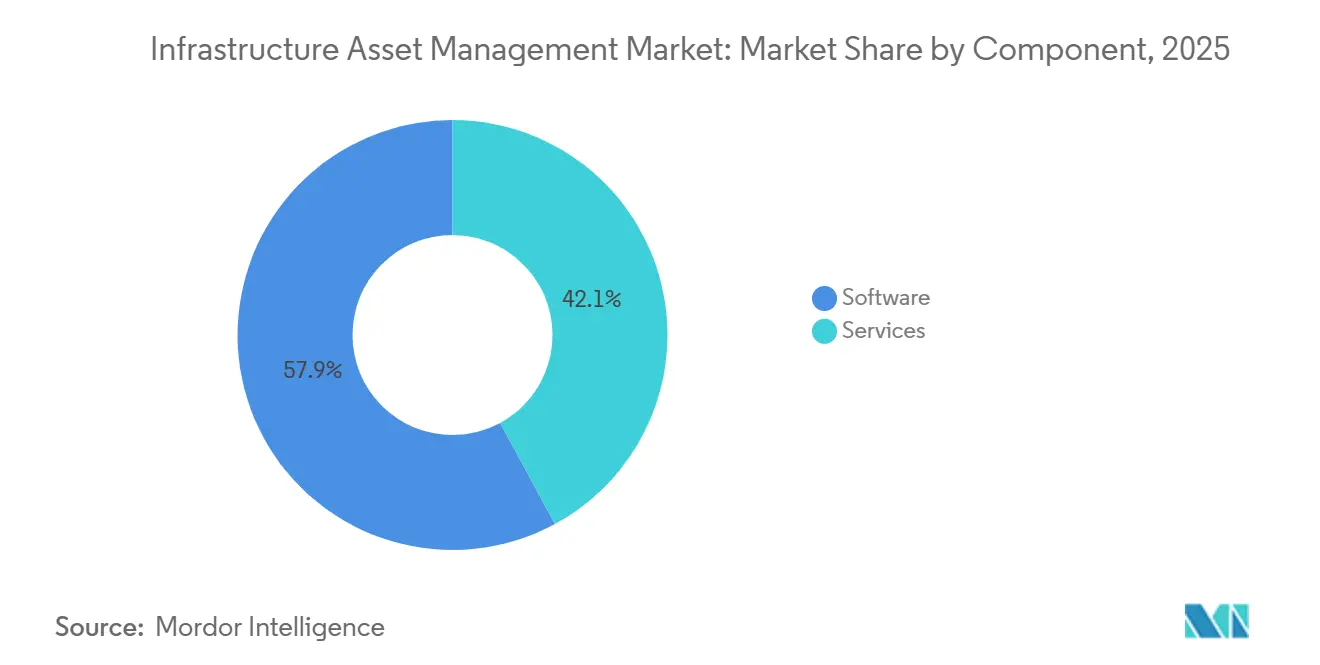

- By component, software held 57.91% share in the infrastructure asset management market in 2025, while services are projected to expand at an 11.62% CAGR through 2031.

- By asset management function, operational asset management held 40.87% share in the infrastructure asset management market in 2025, while strategic asset management is projected to grow at a 10.78% CAGR through 2031.

- By deployment model, cloud-based deployment held 62.77% share in the infrastructure asset management market in 2025, while the same segment is projected to expand at an 11.88% CAGR through 2031.

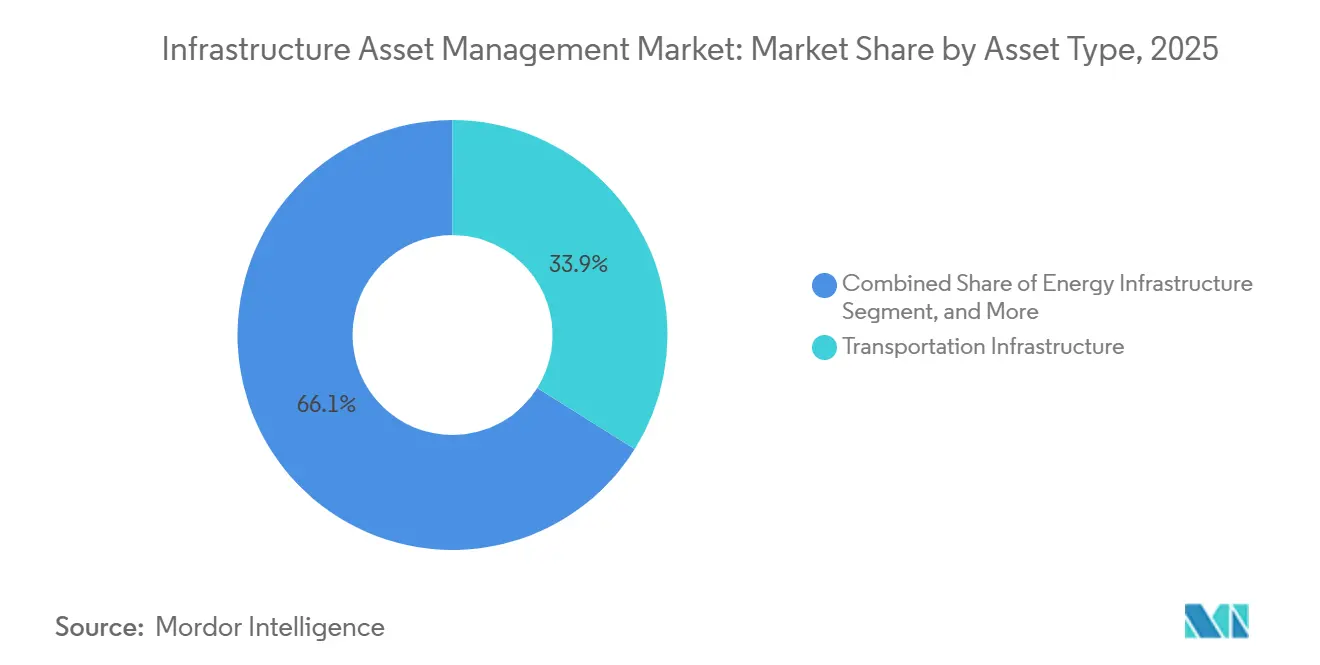

- By asset type, transportation infrastructure held 33.89% share of the infrastructure asset management market in 2025, while energy infrastructure is projected to advance at an 11.14% CAGR through 2031.

- By end user, government and municipal authorities held 36.01% share of the infrastructure asset management market in 2025, while utilities operators are projected to grow at a 10.93% CAGR through 2031.

- By geography, North America held 37.56% of the infrastructure asset management market share in 2025, while Asia-Pacific is projected to expand at a 10.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infrastructure Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Infrastructure Renewal and Lifecycle Cost Pressure | +3.5% | Global, with concentrated near-term impact in North America and Western Europe | Short term (≤ 2 years) |

| Predictive Maintenance and Condition Monitoring Adoption | +2.2% | Global, early deployment in North America, Japan, Germany, and fast follower activity in India and China | Medium term (2-4 years) |

| Smart Infrastructure and Modernization Spending | +1.8% | APAC core, with spill-over to Middle East and Africa and South America | Medium term (2-4 years) |

| Cloud and GIS-Centric Platform Adoption | +1.2% | North America and EU, with accelerating uptake in APAC and Middle East and Africa | Short term (≤ 2 years) |

| Resilience-Mandated Asset Planning for Extreme Weather | +0.8% | North America, EU, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Lead Service Line and Utility Network Inventory Compliance | +0.5% | North America, primarily the United States, with early regulatory influence across the EU and APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Infrastructure Renewal And Lifecycle Cost Pressure

A large share of infrastructure spending still falls after commissioning, which keeps the infrastructure asset management market closely tied to maintenance planning rather than optional IT budgets. The American Society of Civil Engineers reported a USD 3.7 trillion U.S. funding gap across 18 infrastructure categories over the next decade, which shows that current spending is still not enough to close renewal needs.[1]American Society of Civil Engineers. “ASCE Report Card Gives U.S. Infrastructure Highest-Ever ‘C’ Grade, Stresses Need for Sustained Investment to Support Economic Growth.” March 25, 2025. asce.org The same ASCE work also showed that sustained investment improves condition and economic outcomes, which supports the case for earlier intervention rather than deferred replacement.[2]American Society of Civil Engineers. “Investment Pays.” Infrastructure Report Card. Accessed May 21, 2026. infrastructurereportcard.org Pew Charitable Trusts found that U.S. state and local governments carried nearly USD 105 billion in deferred road and bridge maintenance by 2023, and that backlog reinforces the need for better inspection sequencing and repair prioritization across the infrastructure asset management market. That cost pattern favors platforms that can rank assets by risk, condition, and lifecycle consequence before failures move from manageable repair to costly replacement. The infrastructure asset management market is therefore benefiting from a shift in buyer focus from simple recordkeeping toward tools that guide capital timing, field work, and long-term renewal logic.

Predictive Maintenance And Condition Monitoring Adoption

Predictive maintenance is moving further into the infrastructure asset management market because operators now have stronger reason to link live asset data with work planning and failure prevention. A March 2026 paper in Applied Sciences described open frameworks that connect industrial condition monitoring data with large language model workflows, which reflects the broader move toward adaptive analysis in monitoring environments.[3]Di Maggio, Luigi Gianpio. “Predictive Maintenance MCP: An Open-Source Framework for Bridging Large Language Models and Industrial Condition Monitoring via the Model Context Protocol.” Applied Sciences 16, no. 6, March 15, 2026. doi.org This matters because asset owners need systems that can interpret streaming equipment data in a usable way rather than just store it. In practice, the infrastructure asset management market is gaining from the operational value of earlier fault detection, lower unplanned downtime, and clearer maintenance prioritization across rail, utility, and water assets. The same standards-driven shift is also making buyers more attentive to data architecture, cybersecurity, and traceability before they scale condition-based programs across large portfolios. As a result, the infrastructure asset management market is moving toward platforms that combine monitoring, work orders, analytics, and compliance documentation in one operating environment.

Smart Infrastructure And Modernization Spending

Public modernization programs are widening the addressable base for the infrastructure asset management market because digital controls are now being planned alongside physical construction. China’s policy direction on resilient cities and new urban infrastructure called for wider digital transformation of urban systems, including stronger use of sensing and data tools in new projects. In 2026, China also directed RMB 2.55 trillion, approximately USD 352 billion, toward infrastructure investment with priorities that included smart computing, urban renewal, and water network digitalization. The Institute for Sustainable Infrastructure said in late 2025 that digital twins can defer major grid spending globally by extending asset life and improving intervention timing, which supports a broader operating case for digital asset tools. These programs strengthen the infrastructure asset management market because they move digital oversight from a retrofit choice to a design-stage requirement. They also widen the role of software vendors and service partners that can support infrastructure data models over the full asset lifecycle.

Cloud And GIS-Centric Platform Adoption

Cloud and geospatial integration are changing the architecture of the infrastructure asset management market because buyers increasingly want one location-based system that links condition, risk, work history, and capital plans. Autodesk said in April 2026 that it had standardized Info360 Asset on Esri ArcGIS as the sole GIS system of record, which reflects a market-wide shift toward unified geospatial data environments.[4]Autodesk, “Autodesk Deepens Esri Integration Across Info360 Asset and Insight,” One Water Blog, autodesk.com This is important because GIS is no longer treated as a separate mapping layer in the infrastructure asset management market and is instead becoming the operating backbone for network visibility and asset context. Cloud delivery is also helping operators move faster on upgrades, integrations, and remote collaboration across dispersed infrastructure portfolios. Bentley’s FedRAMP Moderate authorization for ProjectWise and OpenGround in April 2026 showed that secure cloud-based digital twin environments can now meet federal-grade requirements for infrastructure programs. Together, these shifts are pushing the infrastructure asset management market toward SaaS and hybrid models that support AI workflows, regulated data handling, and a stronger geospatial foundation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Integration Costs | -1.40% | Global, most acute in emerging markets and SME-dominated public-sector portfolios in South America and Middle East and Africa | Medium term (2-4 years) |

| Legacy System and Data Interoperability Complexity | -1.00% | Global, with concentrated impact in North America and Europe where legacy EAM systems are deeply embedded | Long term (≥ 4 years) |

| Cybersecurity and Multi-Regulation Compliance Burden | -0.60% | North America and EU, with spill-over to APAC and Middle East and Africa | Medium term (2-4 years) |

| Public-Sector Skills and Procurement Bottlenecks | -0.40% | Global, most severe in local and regional governments across all geographies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation And Integration Costs

Implementation cost remains a real brake on the infrastructure asset management market because software licenses are only one part of the total project burden. Many deployments require links across GIS, billing systems, field mobility tools, and operating environments, and this stretches project scope well beyond a standard enterprise software rollout. Public-sector buyers are especially exposed because procurement cycles are slow and capital budgets are often split across departments with different priorities. That makes the infrastructure asset management market harder to penetrate for smaller municipalities and utilities that do not have dedicated internal teams to manage staged rollouts and data migration. The effect is often delayed procurement, a narrower project scope, or phased adoption that captures only part of the expected value. This cost barrier is one reason services are gaining share in the infrastructure asset management market, since outside partners are often needed just to get platforms into production.

Legacy System And Data Interoperability Complexity

Legacy technology remains a persistent challenge for the infrastructure asset management market because many owner-operators still run older operational systems that were not designed for real-time data exchange. OECD reported that 28% of central government department systems in the United Kingdom were still classified as legacy in 2024, which shows how slow modernization can be even in mature public institutions. This matters even more in infrastructure settings where SCADA, historian systems, and field controls often depend on proprietary logic and uneven data quality. The infrastructure asset management market cannot fully realize AI-led planning if asset history, timestamps, and event data remain trapped in disconnected systems. Oracle’s April 2026 release of new Primavera Unifier AI capabilities also underlined how much value depends on structured workflows, audit trails, and clean integration across ERP, EAM, and scheduling systems. Until that legacy backlog is reduced, the infrastructure asset management market will continue to face slower adoption in the most complex installed environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Reshapes The Revenue Mix

Software retained a 57.91% share in 2025, which kept the infrastructure asset management market centered on enterprise platforms that already sit inside large public and utility portfolios. Software accounted for 57.91% share of the infrastructure asset management market size in 2025, and that lead reflected the entrenched role of platforms such as IBM Maximo, SAP S/4HANA EAM, Bentley AssetWise, and Oracle Primavera Unifier in large asset owner environments. The software layer remains essential because it acts as the system for asset records, work orders, inspection history, risk scoring, and capital planning across long-lived infrastructure networks. In practical terms, buyers still start with software because it sets the data model that every other service and workflow will use.

Services are forecast to grow at an 11.62% CAGR from 2026 to 2031, which shows how much execution complexity is now shaping the infrastructure asset management market. Hitachi launched “Social Infrastructure Maintenance powered by Lumada” in February 2026 to bring together more than 40 digital maintenance solutions across roads, bridges, tunnels, water, and power systems, which signaled a stronger vendor focus on lifecycle service delivery. IBM Consulting also announced Process Studio in May 2026 to convert legacy standard operating procedures into agent-ready AI workflows, reinforcing the shift toward service-led modernization around installed platforms. The infrastructure asset management industry is therefore seeing advisory work move upstream, implementation stay spend-intensive, and managed services gain appeal where public clients lack internal digital teams. This service mix is changing the revenue structure of the infrastructure asset management market without weakening software’s role as the anchor layer.

By Asset Management Function: Capital Planning Ascends As Strategic Priority

Operational asset management held a 40.87% share in 2025, which shows that most spending in the infrastructure asset management market still follows day-to-day reliability and field execution needs. That lead is logical because transport, water, energy, and building operators must keep assets available every day, and operational workflows are where work orders, inspection cycles, and maintenance schedules are actively used. Tactical asset management remains the middle layer because it helps coordinate maintenance planning and resource allocation over the medium term. Even so, the current demand base still leaned toward execution visibility over long-range capital modeling.

Strategic asset management is projected to grow at a 10.78% CAGR from 2026 to 2031, making it the fastest-growing function in the infrastructure asset management market. The American Water Works Association stated in 2026 that U.S. drinking water systems need USD 90.2 billion in annual investment through 2050 against current spending of USD 33.6 billion, which forces utilities to make long-horizon capital decisions with stronger analytical support. Veolia’s digital twin deployment for Atlanta’s combined sewer system showed how model-based planning can improve intervention timing and avoid environmental penalties in complex urban networks. AIVALIX also reported in May 2026 that its AI-driven planning demonstration cut total man-hours for water utility asset planning by 61% versus standard practice, highlighting the labor value of stronger planning tools. The infrastructure asset management industry is therefore moving beyond maintenance execution alone and giving more weight to tools that shape multi-decade capital programs.

By Deployment Model: Cloud Dominance Intensifies Amid Sovereignty Constraints

Cloud-based deployment held a 62.77% share in 2025, and cloud-based deployment also represented the fastest-growing part of the infrastructure asset management market at an 11.88% CAGR through 2031. Cloud captured 62.77% share of the infrastructure asset management market size in 2025 because operators increasingly want lower hardware overhead, faster upgrades, and stronger support for distributed teams. This dual lead is notable because it shows the market is not just moving to the cloud, but still finding new value there through AI, geospatial integration, and quicker rollout models. It also reflects the limits of on-premises environments for buyers that want to scale analytics across many field locations and asset classes.

SAP’s 2025 Cloud ERP Private FPS01 release added geospatial-enabled maintenance notifications, linear asset support, and IoT-driven asset performance management, which kept cloud delivery at the front of product innovation rather than treating it as a basic hosting option. Bentley’s FedRAMP Moderate authorization in April 2026 further showed that cloud environments can satisfy strict security requirements in federal infrastructure programs. At the same time, sovereignty rules are still shaping the infrastructure asset management market because some operators need domestic hosting or hybrid architectures for sensitive operational data. Japan’s NEC and IFS partnership around a domestically hosted IFS Cloud Kaname service reflected that need for local control under national security-oriented data rules. This is why the infrastructure asset management market is expanding through cloud-first models without eliminating the role of hybrid and compliant local deployment structures.

By Asset Type: Grid Electrification Elevates Energy Infrastructure Demand

Transportation infrastructure held a 33.89% share in 2025, which made it the largest asset type in the infrastructure asset management market. Transportation led because road, bridge, rail, and airport systems already carry deep maintenance backlogs and dense regulatory reporting demands. The scale of rehabilitation needs remains large in roads and bridges, and that keeps transport agencies among the most consistent buyers of condition tracking, work management, and capital planning tools. The infrastructure asset management market continues to benefit from this segment because transport networks combine long asset lives with high public visibility and clear cost penalties when maintenance slips.

Energy infrastructure is projected to grow at an 11.14% CAGR from 2026 to 2031, which makes it the fastest-growing asset type in the infrastructure asset management market. The European Commission earmarked EUR 170 billion, approximately USD 192 billion, for grid digitalization through 2030, which supports rising demand for asset monitoring and planning across transmission and distribution systems. China also directed major infrastructure funding toward digital urban and utility systems in 2026, which supports the case for faster rollout of asset visibility tools in energy and network operations. Digital and critical infrastructure is also moving into focus as high-density compute assets, energy systems, and facilities are treated as strategic infrastructure that requires continuous lifecycle oversight. That broadening asset base is expanding the reach of the infrastructure asset management market beyond traditional transport and utility categories.

By End User: Utilities Lead On Investment Urgency Despite Government Scale

Government and municipal authorities held a 36.01% share in 2025, which made them the largest end-user group in the infrastructure asset management market. That position reflected the scale of public asset ownership across roads, water systems, buildings, lighting, and local utility networks. The National League of Cities said in 2026 that more than 1,600 U.S. cities had secured nearly USD 12.7 billion in federal infrastructure funding by mid-2026, which supported public-sector budgets for digital asset oversight. Government buyers remain central to the infrastructure asset management market because they carry broad, aging portfolios and face growing reporting obligations across multiple agencies.

Utilities operators are projected to grow at a 10.93% CAGR from 2026 to 2031, which points to the strongest investment urgency among end users in the infrastructure asset management market. EPA rules on lead service line replacement and related inventory requirements are pushing utilities to strengthen asset records, replacement planning, and compliance reporting over long network lifecycles. AVEVA and IFS announced a strategic partnership in May 2026 to connect real-time operational data with maintenance history, crew capacity, and investment priorities, which directly matched utility needs for faster decision cycles across distributed assets. Diriyah Company’s use of IBM Maximo Application Suite on a USD 63.2 billion Saudi project also showed that large private infrastructure operators are adopting the same enterprise-grade systems once associated mainly with government owners. This demand mix leaves government largest by installed scale, while utilities increasingly set the pace for new adoption across the infrastructure asset management market.

Geography Analysis

North America held 37.56% of the infrastructure asset management market share in 2025, which made it the largest regional contributor. The region benefits from a large installed base of enterprise EAM platforms and a dense policy environment that links infrastructure funding to performance, reporting, and compliance activity. ASCE’s 2025 report card showed that U.S. infrastructure conditions improved but still carried a major long-term funding gap, which keeps digital planning tools relevant across transport, water, and public works portfolios. The EPA’s lead and copper rule improvements, along with federal infrastructure grants secured by more than 1,600 municipalities by mid-2026, are also supporting procurement of software and services across the infrastructure asset management market.

Europe held the second-largest regional share in 2025, and the infrastructure asset management market there is being shaped by aging assets, decarbonization programs, and strong compliance expectations. The European grid digitalization agenda, supported by EUR 170 billion, approximately USD 192 billion, through 2030, gives the region a clear utility-centered demand base for data-driven asset oversight. Companies serving Europe are also being pushed to align with stricter cybersecurity and data-governance requirements, which raises the value of built-in compliance and auditability in platform design. Bentley argued in May 2026 that Europe’s infrastructure renewal path increasingly depends on connected data and AI-enabled workflows, which reflects the region’s need to rebuild at scale without losing delivery discipline.

Asia-Pacific is projected to grow at a 10.61% CAGR from 2026 to 2031, which makes it the fastest-growing regional part of the infrastructure asset management market. China’s 2026 infrastructure investment plan and earlier resilient city guidance are pushing digital controls, sensing, and network visibility deeper into new infrastructure programs. Japan is also moving on workforce-led modernization, with Hitachi packaging social infrastructure maintenance solutions and SoftBank partnering to embed generative AI and IoT in operational workflows. South Korea, Australia, and Southeast Asia add to that momentum through public digitalization programs, while South America and the Middle East and Africa are emerging demand nodes tied to new project pipelines and smart-city development. Peru’s February 2026 Corredor Sur digital governance pilot showed that South America is moving toward more structured adoption of integrated asset oversight across road, port, and rail concessions.

Competitive Landscape

The infrastructure asset management market remains moderately consolidated at the enterprise tier, where IBM, Bentley Systems, SAP, Oracle, Siemens, Schneider Electric, and Hexagon shape buying standards for large infrastructure portfolios. At the same time, the mid-market remains more fragmented because IFS, Tyler Technologies, Brightly Software, AssetWorks, Accruent, and ServiceNow compete in narrower verticals and project scopes. This split keeps the infrastructure asset management market competitive on both product breadth and delivery model, especially when buyers compare platform depth against implementation cost. Pricing pressure on implementation fees also persists because large vendors increasingly face cloud-native specialists and sector-focused challengers in municipal, utility, and facilities environments.

A common strategic pattern in the infrastructure asset management market is platform convergence. Bentley launched Infrastructure Cloud Connect to bring ProjectWise, AssetWise, and iTwin into one connected environment with AI-driven search, which reinforced the push toward a shared data layer across the asset lifecycle. SAP used its May 2026 Sapphire cycle to outline a new field service and asset management solution with Joule AI agents and autonomous maintenance scheduling for later 2026 availability. Oracle also extended Primavera Unifier in April 2026 with AI-enabled workflow automation, summarization, and audit chronologies, which showed how vendors are trying to combine capital program control with compliance-ready execution. Partnerships and portfolio moves are also redefining the infrastructure asset management market. AVEVA and IFS said in May 2026 that their Continuous Asset Decision Intelligence offering would connect live operational data with maintenance history and investment priorities, which strengthens their position against longer-established large-contract rivals.

Siemens launched Asset Performance Advanced in May 2026 and also expanded its industrial AI operating system in 2026, showing how a hardware-rooted company is pushing further into recurring software and managed service revenue. Hexagon’s agreement to acquire Waygate Technologies in April 2026 widened its reach in inspection and asset integrity workflows, which supports a stronger lifecycle position in regulated infrastructure settings. IBM, meanwhile, is reinforcing service-led stickiness around installed software through workflow automation and AI transformation tools, which helps it protect position in the infrastructure asset management market even as the field broadens.

Infrastructure Asset Management Industry Leaders

Bentley Systems, Incorporated

SAP SE

IBM Corporation

Oracle Corporation

Hexagon AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Siemens launched Asset Performance Advanced, an AI-powered managed service within the Building X ecosystem designed for autonomous building operations. The service integrates predictive and prescriptive intelligence with AI-enabled workflows, targeting improved asset lifecycle reliability and reduced operational costs.

- May 2026: AVEVA and IFS announced a strategic technology partnership to launch Continuous Asset Decision Intelligence, connecting real-time operational data with enterprise maintenance history, crew capacity, and investment priorities to enable portfolio-level risk-ranked capital decisions. The solution targets utilities, energy, construction, and mining sectors and provides a time-stamped, auditable evidence chain for regulatory compliance.

- May 2026: Siemens completed delivery of the first of 1,200 D9 electric freight locomotives to Indian Railways, marking the activation of one of the largest single infrastructure asset management contracts in South Asia. The deployment requires end-to-end maintenance planning integration across Siemens' enterprise asset management platform.

- May 2026: Autodesk joined the Water-AI Nexus Advisory Council at the Water Environment Federation, formalizing its commitment to AI-supported water infrastructure management. SA Water in Australia, Aguas de Alicante in Spain, and Orange County Sanitation District in the United States were cited as active implementation cases integrating Autodesk's digital twins with real-time operational workflows.

Global Infrastructure Asset Management Market Report Scope

The Infrastructure Asset Management Market covers software and services used to plan, monitor, maintain, and optimize physical infrastructure assets such as roads, bridges, railways, utilities, pipelines, and public buildings. It helps owners and operators manage the full asset lifecycle, from acquisition and condition assessment to maintenance, renewal, and disposal, with the goal of improving performance and reducing lifecycle cost.

The Infrastructure Asset Management is Segmented by Component (Software and Services), Asset Management Function (Strategic Asset Management, Operational Asset Management, and Tactical Asset Management), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Asset Type (Transportation Infrastructure, Energy Infrastructure, Water and Wastewater Infrastructure, Buildings and Facilities Infrastructure, and Digital and Critical Infrastructure), End User ( Government and Municipal Authorities, Utilities Operators, Transportation Agencies and Concessionaires, Engineering and Construction Firms, Industrial and Private Infrastructure Operators), Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa) The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Consulting and Advisory Services |

| Implementation and Integration Services | |

| Managed Services and Support Services |

| Strategic Asset Management |

| Operational Asset Management |

| Tactical Asset Management |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Transportation Infrastructure |

| Energy Infrastructure |

| Water and Wastewater Infrastructure |

| Buildings and Facilities Infrastructure |

| Digital and Critical Infrastructure |

| Government and Municipal Authorities |

| Utilities Operators |

| Transportation Agencies and Concessionaires |

| Engineering and Construction Firms |

| Industrial and Private Infrastructure Operators |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Software | |

| Services | Consulting and Advisory Services | |

| Implementation and Integration Services | ||

| Managed Services and Support Services | ||

| By Asset Management Function | Strategic Asset Management | |

| Operational Asset Management | ||

| Tactical Asset Management | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Asset Type | Transportation Infrastructure | |

| Energy Infrastructure | ||

| Water and Wastewater Infrastructure | ||

| Buildings and Facilities Infrastructure | ||

| Digital and Critical Infrastructure | ||

| By End User | Government and Municipal Authorities | |

| Utilities Operators | ||

| Transportation Agencies and Concessionaires | ||

| Engineering and Construction Firms | ||

| Industrial and Private Infrastructure Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the infrastructure asset management space?

The infrastructure asset management market size is expected to rise from USD 28.12 billion in 2025 to USD 30.72 billion in 2026 and reach USD 50.11 billion by 2031, at a 10.28% CAGR over 2026-2031.

Which component leads revenue generation in infrastructure asset management?

Software led in 2025 with a 57.91% share, reflecting the central role of enterprise platforms in asset records, work orders, and lifecycle planning.

Why are utilities becoming a faster-growing buyer group?

Utilities operators are projected to grow at a 10.93% CAGR through 2031 because of grid reliability rules, lead service line replacement requirements, and the need for verified network inventory data.

Which deployment model is expanding the fastest?

Cloud-based deployment held the largest share at 62.77% in 2025 and is also the fastest-growing deployment segment, supported by lower hardware overhead and easier analytics scaling.

Which asset type is creating the strongest new demand?

Transportation remained the largest asset type in 2025 with 33.89% share, but energy infrastructure is expected to grow fastest at an 11.14% CAGR through 2031 as grid digitalization expands.

Which region is strongest today and which one is growing fastest?

North America led with 37.56% share in 2025, while Asia-Pacific is forecast to record the fastest growth at a 10.61% CAGR through 2031.

Page last updated on: