Cybersecurity Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

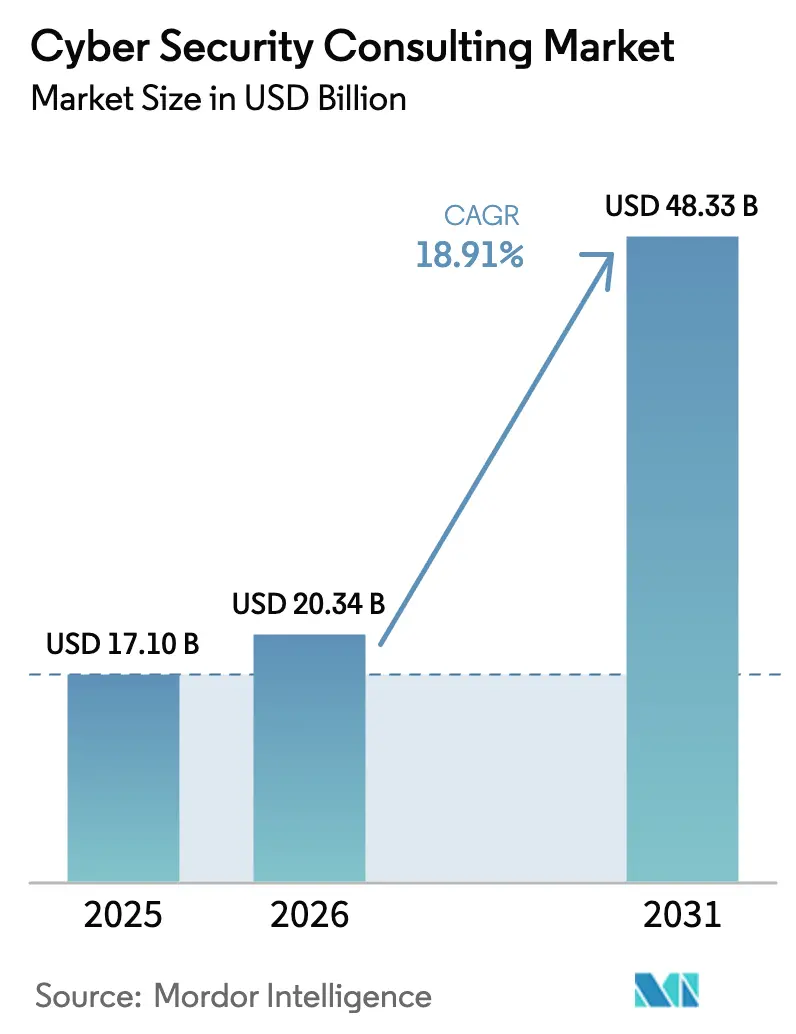

| Market Size (2026) | USD 20.34 Billion |

| Market Size (2031) | USD 48.33 Billion |

| Growth Rate (2026 - 2031) | 18.91% CAGR |

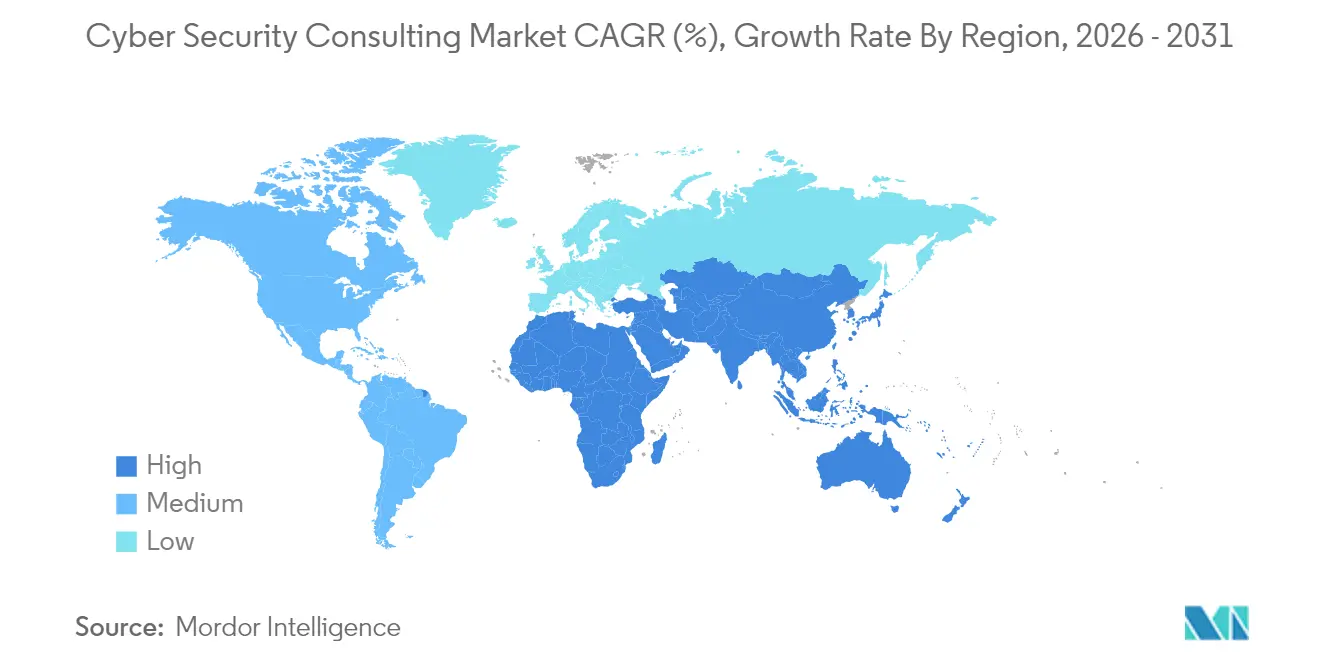

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity Consulting Market Analysis by Mordor Intelligence

The Cybersecurity Consulting Market size was valued at USD 17.10 billion in 2025 and estimated to grow from USD 20.34 billion in 2026 to reach USD 48.33 billion by 2031, at a CAGR of 18.91% during the forecast period (2026-2031). This sharp rise comes from enterprises scrambling to counter quantum-enabled threats, meet ever-tighter disclosure rules, and plug expertise gaps that internal teams cannot fill. Post-quantum cryptography standards released by NIST in August 2024 alone triggered hundreds of large-scale key-management reviews across critical infrastructure and finance[1]National Institute of Standards and Technology, “Post-Quantum Cryptography Standards,” nist.gov. Simultaneously, cyber-insurance underwriters now require third-party audits before binding policies, turning advisory firms into essential gatekeepers for coverage eligibility. Outcome-based engagement models command the fastest growth, expanding 19.7% as boards prefer shared-risk arrangements where consultants must demonstrate measurable gains. Managed Security Services (MSS) accelerate at 19.6% because enterprises cannot staff 24/7 SOCs amid a 4.8 million-person talent gap. Small and Medium Enterprises (SMEs) make the quickest pivot, logging a 20.1% CAGR, even though only 44% deploy more than two cyber controls.

Key Report Takeaways

- By engagement model, outcome-based partnerships expanded 19.35% while retainer contracts secured 50.20% of 2025 revenue from the Cybersecurity Consulting Market.

- By service, Managed Security Services grew fastest at 19.10%, whereas risk assessment kept a 30.70% slice of the Cybersecurity Consulting Market in 2025.

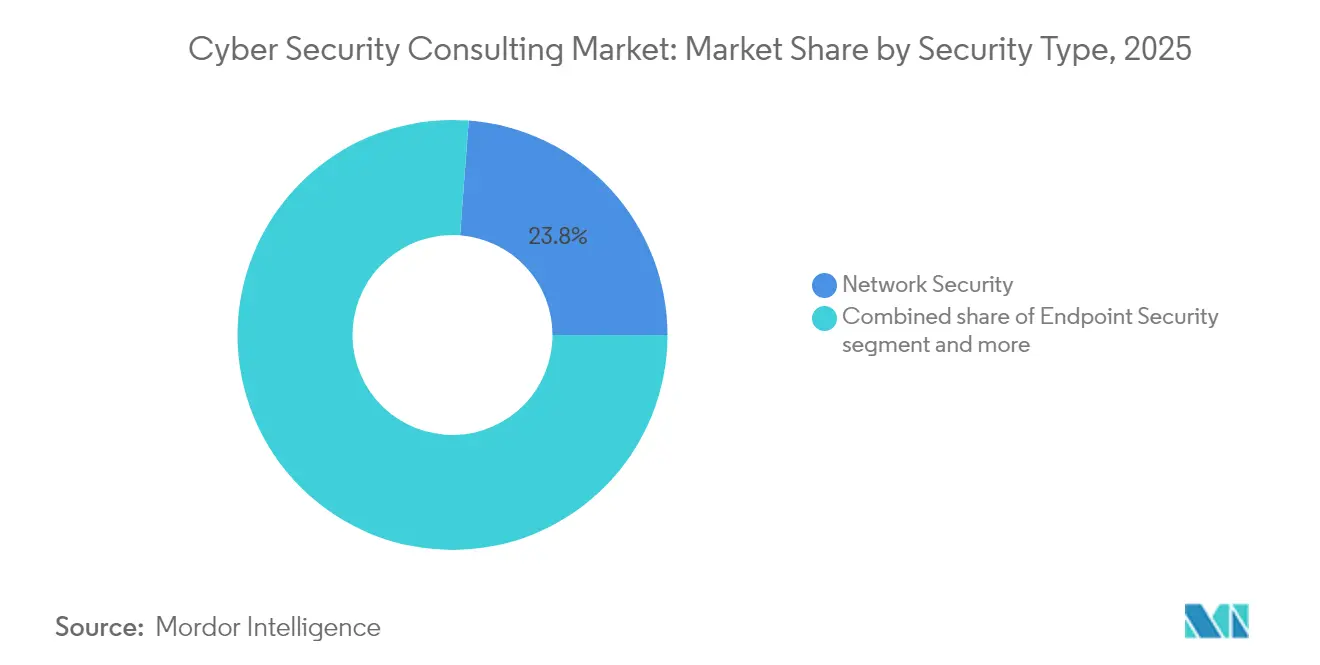

- By security type, network security retained 23.80% of the Cybersecurity Consulting Market share in 2025, but cloud security is forecast to grow at 19.85% CAGR.

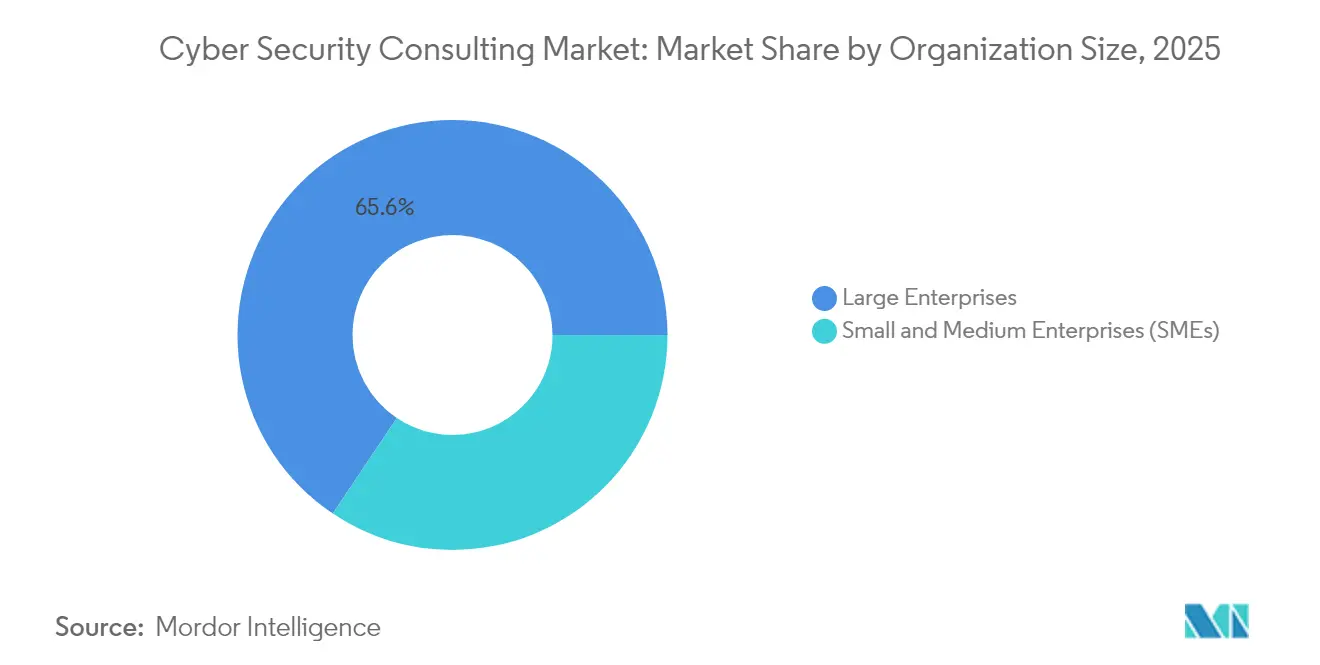

- By organization size, large enterprises controlled 65.60% of the 2025 Cybersecurity Consulting Market; SMEs will advance at a 19.62% CAGR.

- By vertical, BFSI led with a 21.10% Cybersecurity Consulting Market share in 2025, whereas healthcare will post the highest 19.26% CAGR.

- North America generated 37.50% of 2025 revenue; Asia-Pacific is the fastest-growing region at 19.35%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cybersecurity Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency and sophistication of multi-vector attacks | +4.2% | Global; especially North America and Europe | Short term (≤2 years) |

| Escalating global and sector-specific compliance mandates | +3.8% | Global; led by EU and North America | Medium term (2-4 years) |

| Cloud, SaaS and edge adoption widening attack surfaces | +3.5% | Global; concentrated in APAC and North America | Medium term (2-4 years) |

| Cyber-insurance clauses mandating third-party audits | +2.9% | North America and EU; expanding to APAC | Short term (≤2 years) |

| Board-level ESG scoring now factoring data-breach metrics | +2.1% | Global; early adoption in EU and North America | Long term (≥4 years) |

| Quantum-ready encryption road-maps accelerating advisory spend | +1.8% | Global; government and critical infrastructure | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising frequency and sophistication of multi-vector attacks

The volume and complexity of ransomware, supply-chain, and extortion campaigns exploded in 2024, with Verizon logging a 180% rise in vulnerability-led breaches and ransomware representing 32% of all recorded incidents[2]Verizon, “2024 Data Breach Investigations Report,” verizon.com. Median global dwell time tightened to 10 days, down from 16, forcing companies to source 24/7 threat-hunting partners capable of compressing detection‐to-containment cycles. Over half of the victims still learn of incidents from third parties, further validating the external advisory demand. AI-enabled tooling on both attacker and defender sides adds complexity that few in-house teams can manage. Consequently, the Cybersecurity Consulting Market grew as organizations sought incident response retainers that include forensics, crisis communications and regulatory reporting.

Escalating global and sector-specific compliance mandates

Public companies listed in the United States must now report material cyber events within four business days under SEC rules enacted September 2023. Firms also navigate more than 250 privacy laws worldwide, while the TSA’s proposed rules for pipeline and rail operators will cost USD 2.2 billion over ten years. In Europe, the Cyber Europe 2024 exercise mobilized 5,000 practitioners to test cross-border readiness, underscoring how regulators institutionalize tabletop drills. These overlapping mandates extend consulting beyond privacy into export-control, forced-labor compliance and supply-chain integrity, swelling the Cybersecurity Consulting Market.

Cloud, SaaS and edge adoption widening attack surfaces

With 95% of companies migrating to cloud platforms, unseen mis-configurations abound. U.S. Department of Energy data show data-center power consumption could reach 12% of nationwide electricity by 2028, illustrating infrastructure scale and complexity. Edge devices proliferate in industrial settings, and Google’s Threat Horizons report recorded a 50% surge in zero-day exploits during 2024. Meanwhile, 77% of executives in PwC’s Digital Trust survey intend to deploy generative AI for cyber defense despite new model risks. Consultants therefore design zero-trust overlays, harden APIs and build real-time asset inventories, bolstering the Cybersecurity Consulting Market.

Cyber-insurance clauses mandating third-party audits

Premium rates stabilized only because insurers tightened underwriting, demanding MFA, backup testing and external security assessments prior to renewal. Fitch projects the cyber-insurance market will double by 2027, embedding advisory review as a de-facto requirement. Policies now feature “acts of war” exclusions, driving demand for legal-technical guidance on coverage gaps. Engagements that translate control maturity into insurability metrics now represent a material slice of the Cybersecurity Consulting Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of certified cyber talent inflates project costs | -2.8% | Global; most severe in North America and APAC | Short term (≤2 years) |

| High switching costs from incumbent MSSP/tool lock-in | -1.9% | Global; large enterprises | Medium term (2-4 years) |

| Rising carbon-accounting scrutiny on energy-intensive labs | -1.2% | EU and North America; expanding worldwide | Long term (≥4 years) |

| Geopolitical export-control rules limiting cross-border forensics | -0.8% | Global; acute US–China–Russia corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute shortage of certified cyber talent inflates project costs

ISC2’s 2024 workforce study places the global shortfall at 4.8 million practitioners, leaving only 72% of required seats filled. IBM quantifies the cost: firms with shortages incurred average breach losses of USD 4.56 million, versus better-staffed peers. Consulting providers pay premium wages for scarce certifications, a burden ultimately borne by clients, yet demand still outstrips supply, limiting project throughput and tempering total Cybersecurity Consulting Market growth.

Rising carbon-accounting scrutiny on energy-intensive labs

The Department of Energy warns penetration-testing facilities and SOCs contribute meaningfully to rising data-center loads, making them ESG hot spots[3]U.S. Department of Energy, “Data-Center Energy Forecast 2025–2028,” energy.gov. Eaton’s operator survey shows 56% of data-center managers struggling to balance security workloads with sustainability targets. As carbon audits become standard, advisory firms must modernize labs with efficient hardware or risk losing environmentally minded clients, constraining some expansion in the Cybersecurity Consulting Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Type: Cloud consulting drives next-generation demand

Cloud security engagements are projected to grow 19.85% annually, the fastest rate among sub-segments of the Cybersecurity Consulting Market because mis-configured identities and serverless architectures now account for a rising share of breaches. Network security still commands 23.80% of the Cybersecurity Consulting Market share in 2025, yet its perimeter focus erodes under zero-trust policies. Endpoint security benefits from remote-work persistence, while application security gains relevance as DevSecOps integrates testing into CI/CD pipelines. Infrastructure and ICS consulting deepens as OT networks converge with IT, raising safety stakes. Identity and access management sees steady uptake, and quantum-readiness appears as a premium advisory niche following NIST’s PQC standards. All told, diversification across these lines adds resilience to the Cybersecurity Consulting Market.

The Cybersecurity Consulting Market for cloud security is positioned to expand more than threefold by 2030 as SaaS adoption penetrates heavily regulated verticals. Organizations re-platforming ERP workloads confront shadow admin accounts, insecure APIs, and compliance concerns around data residency. Consultants embed cloud-native security posture management, automate infrastructure-as-code scanning, and design least-privilege identity models. Meanwhile, quantum readiness consulting addresses algorithm agility, crypto-asset inventory, and migration timelines. Across legacy environments, network micro-segmentation remains mandatory, yet now integrates with zero-trust brokers rather than firewalls alone. As 5G and edge IoT footprints grow, ICS/OT audits escalate, feeding a separate wave of demand in manufacturing and utilities. The mix of traditional perimeter hygiene and next-gen cloud controls keeps the Cybersecurity Consulting Market robust across enterprise maturity bands.

By Service Type: MSS transforms traditional consulting models

Risk assessment remained the anchor, capturing 30.70% of 2025 spend within the Cybersecurity Consulting Market. Yet Managed Security Services accelerate at 19.10%, matching buyers’ need for continuous monitoring amid workforce shortages. Compliance and audit lines enjoy secular momentum as privacy regimes multiply; threat intelligence and forensics engagements grow with attacker sophistication. Incident response and resiliency planning win budget priority after dwell times compress. Advisory blending cyber-insurance and ESG reporting is nascent but expected to surge as underwriters and rating agencies incorporate security metrics.

A deeper dive shows the Cybersecurity Consulting Market for MSS growth, outpacing traditional project-based work. Buyers cite mean-time-to-detect reductions of 40% after outsourcing to specialist SOCs. Providers embed SOAR automations, curated intelligence feeds and proprietary AI analytics, which in turn elevate barriers to entry. For risk assessment, methodologies increasingly align with NIST CSF 2.0 and ISO/IEC 27001 updates, adding depth and repeatability. Compliance audits now span CCPA, CPRA, GDPR, Schrems II transfer clauses and novel AI-act provisions. Digital forensics has expanded to include mobile malware reverse engineering and blockchain-enabled evidence preservation. Together, these services diversify revenue streams and cushion cyclical swings in the Cybersecurity Consulting Market.

By Engagement Model: Outcome-based partnerships reshape consulting

Outcome-based and shared-risk contracts are the fastest-rising structures inside the Cybersecurity Consulting Market, posting 19.35% CAGR as boards insist on proof of risk reduction rather than deliverable completion. Retainer or subscription deals still furnish 50.20% of 2025 revenue because they guarantee flexible access to scarce skills. Project-based work shrinks proportionally, but persists for targeted migrations or regulatory gap closures.

At scale, outcome contracts tie up to 30% of fees to metrics such as reduced phishing click-through, patching SLAs or regulatory findings closed. They require robust telemetry to calculate baselines and progress, pushing advisors to invest in continuous-assurance tooling. Shared-risk deals may bundle cyber-insurance captives where consultants co-insure a defined loss corridor, aligning incentives even further. As AI automates triage and containment, advisors can more reliably commit to performance guarantees. These dynamics reinforce client retention and lift pricing power, strengthening long-term revenue stability within the Cybersecurity Consulting Market.

By Organization Size: SME adoption accelerates despite constraints

Large enterprises own two-thirds of current revenue, yet SMEs are propelling the fastest lanes of growth in the Cybersecurity Consulting Market. 44% of SMEs employ multifactor authentication, creating a vast addressable gap. Government grants, such as NIST’s USD 1.2 million program funding cybersecurity innovations for 12 small firms, help offset budget barriers.

The Cybersecurity Consulting Market for SME engagements remains modest, but a 19.62% CAGR could lift it by decade-end. Key demand clusters include SOC-as-a-service, policy frameworks prepared for insurance underwriting and baseline cloud posture checks. Consultants succeeding here standardize playbooks, automate reporting and bundle virtual CISO hours. Pricing sensitivity stays acute; hence fixed-fee or subscription offerings dominate. As regulators shift liability onto boards regardless of company size, SMEs increasingly treat cybersecurity like mandatory payroll or accounting services, feeding structural growth in the Cybersecurity Consulting Market.

By Industry Vertical: Healthcare breaches drive consulting urgency

Healthcare and life-sciences present a 19.26% CAGR through 2031 after 677 major breaches in 2024 exposed 182.4 million records. BFSI keeps the biggest slice—21.10% in 2025—because 75% of bank chief risk officers rank cybersecurity as their top concern.

Hospitals battle thin margins: on average, only 13-15% of IT budgets cover security, so they outsource penetration testing, phishing simulations and HIPAA compliance reviews. Financial institutions, by contrast, run multi-year zero-trust road-maps and red-team exercises calibrated to Basel III resilience metrics. Government and defense mandates like FedRAMP High and CMMC 2.0 escalate demand for accreditation consulting. Manufacturing and utilities focus on OT segmentation and IEC 62443 audits, while retail pushes for PCI DSS 4.0 migrations before the March 2025 enforcement window. Education and media firms, traditionally peripheral buyers, now accelerate spending as ransomware hits tuition and advertising revenue. The vertical spread thus insulates the Cybersecurity Consulting Market from macro shocks in any single sector.

Geography Analysis

North America held 37.50% of 2025 revenue, anchored by SEC disclosure rules, 18 state privacy laws, and deep cyber-insurance penetration. Canada’s National Cyber Threat Assessment flags ransomware and state-sponsored espionage as top risks, pressing companies to invest in advisory road maps. Mexico sees heightened demand as USMCA trade scrutiny and cross-border data transfer audits rise, further inflating the Cybersecurity Consulting Market.

Asia-Pacific is the fastest-growing region with a 19.35% CAGR. China enforces data-localization rules, while Japan funds quantum-safe encryption pilots. India’s Big Four affiliates added 3,300 partners as advisory revenue grew 25%, with more than half sourced from tech and cyber contracts. South Korea’s market coalesces around SOC automation, and Australia pushes critical-infrastructure reforms. Collectively, these drivers underpin the Asia-Pacific share of the Cybersecurity Consulting Market.

Europe posts steady gains under GDPR and new NIS2 obligations. Germany mandates industrial SOC certification; the United Kingdom refines post-Brexit DPIA processes; France invests in sovereign cloud and crypto services. ENISA’s Cyber Europe drills institutionalize readiness assessment, requiring advisory help to interpret exercise findings. Russia’s sanctions-driven isolation necessitates a domestic consulting supply, reshaping competitive contours. The diversity of legal regimes means cross-border corporates must orchestrate multi-jurisdiction programs, expanding the regional Cybersecurity Consulting Market.

Competitive Landscape

Private-equity driven consolidation is reshaping the Cybersecurity Consulting Market; EY tallied more than 60% of 2024 MSSP acquisitions backed by financial sponsors. Big Four firms now earn over 50% of India revenue from technology consulting, signalling aggressive pivot toward cyber. CrowdStrike doubled marketplace integrations to 260, emphasizing platform ecosystems. IBM divested QRadar SaaS to Palo Alto Networks, demonstrating strategic refocus on services.

AI integration stands as the sharpest differentiator; vendors weave machine-learning analytics into detection pipelines, raising barriers to entry. Palo Alto’s XSIAM absorbs telemetry across endpoints, firewalls and clouds, allowing consultants to guarantee dwell-time reductions. Quantum-readiness advisory emerges as white-space; CISA’s Roadmap urges federal agencies to inventory cryptographic assets within a year. Environmentally efficient testing facilities grow in importance: Fortinet cut average product power by 61%, courting ESG-focused RFPs.

Regional expansion strategies proliferate: EY acquired Malaysia’s Xynapse to gain identity expertise in ASEAN markets, while Accenture invested in Japanese OT-security boutique NVISIONx. Boutique specialists target niches such as AI model bypass testing and sovereign-cloud resilience. The overall mix of global scale, niche depth and private-equity roll-ups keeps competitive pressure high yet leaves room for differentiated offers, ensuring a dynamic Cybersecurity Consulting Market.

Cybersecurity Consulting Industry Leaders

Accenture PLC

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers International Limited

KPMG International Cooperative

Ernst & Young Global Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Palo Alto Networks announced plans to acquire Protect AI and launched Cortex XSIAM 3.0.

- March 2025: Google attempted to buy Wiz for USD 32 billion.

- February 2025: CrowdStrike introduced agentic AI extensions; SentinelOne launched Purple AI Athena.

- January 2025: Veza raised USD 108 million; Upwind acquired Nyx Security.

- September 2024: FTI Consulting rolled out a National Security unit.

- August 2024: NIST released first PQC standards, Kyber and Dilithium.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cyber security consulting market as fee-based advisory, assessment, and incident-response services that help organizations prevent, detect, and recover from cyber threats, spanning strategy design through post-breach forensics and delivered by specialist consultancies, system integrators, and virtual-CISO practices.

Scope exclusion: Tool resale, fully managed SOC outsourcing, and general IT projects without a material security focus are outside scope.

Segmentation Overview

- By Security Type

- Network Security

- Endpoint Security

- Cloud Security

- Application Security

- Infrastructure/ICS Security

- Identity and Access Management

- Other Security Types (IoT, OT, Quantum-Readiness)

- By Service Type

- Risk Assessment and Management

- Compliance and Audit

- Threat Intelligence and Digital Forensics

- Managed Security Services (MSS)

- Incident Response and Resiliency Planning

- Advisory for Cyber-Insurance and ESG Reporting

- By Engagement Model

- Project-Based

- Retainer / Subscription

- Outcome-Based and Shared-Risk

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecommunications

- Government and Defense

- Retail and E-Commerce

- Manufacturing and Industrial

- Energy and Utilities

- Other Verticals (Education, Media)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed C-level security officers, practice leads at global consultancies, cyber-insurance underwriters, and procurement heads across North America, Europe, Asia-Pacific, and the Middle East. These conversations clarified billable rate trends, average engagement mix, and the pace of outcome-based contracts, which public sources rarely quantify.

Desk Research

Our desk work began with breach disclosure records from sources such as Verizon DBIR, ENISA threat reports, NIST's NVD, and CERT advisories, and then mapped them to commercial demand signals. Industry spend benchmarks from SEC 10-K filings, OECD ICT tables, and association portals like ISACA, FIRST, and Cloud Security Alliance reinforced vertical splits. Company intelligence from D&B Hoovers, news feeds on Dow Jones Factiva, and shipment flows in Volza helped validate regional swings and vendor capacity. The sources quoted illustrate the breadth of public intelligence. Many additional open and subscription datasets were tapped to cross-check numbers and fill gaps.

Market-Sizing & Forecasting

A top-down and bottom-up blend anchors our model. We start with worldwide IT outlay, derive a security budget pool, and apply consulting penetration rates that differ by vertical risk appetite. Supplier roll-ups, selective channel checks, and sampled average day-rate × project duration validate totals. Key variables include annual disclosed breach counts, mandatory compliance spend per employee, cloud workload share, average consulting day rate, cyber-insurance clauses that mandate third-party audits, and regional talent availability. Relationships between these drivers and revenue are estimated through multivariate regression, projected with ARIMA, and stress-tested under optimistic and conservative scenarios. Where supplier data under-reports emerging regions, interpolation based on headcount density and project mix closes the gap.

Data Validation & Update Cycle

Outputs pass a two-level analyst review. Anomalies trigger re-contact with primary respondents and fresh desk checks. We refresh every twelve months, with interim revisions when major regulations or mega breaches materially shift demand.

Why Our Cyber Security Consulting Baseline Commands Reliability

Published estimates often diverge because each firm chooses different scopes, currency treatments, and update cadences. Some fold managed services into consulting totals or apply unverified vendor revenue extrapolations.

Key gap drivers for others include counting MSSP recurring fees, omitting SME demand in developing regions, or using nominal exchange rates without inflation smoothing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.10 B (2025) | Mordor Intelligence | |

| USD 40.00 B (2025) | Regional Consultancy A | Adds integration and managed services, inflates totals using reseller sales |

| USD 21.80 B (2025) | Global Consultancy B | Excludes SMEs in LatAm & MEA, relies solely on vendor revenue samples |

| USD 42.80 B (2024) | Industry Research Group C | Uses broad IT consulting base and nominal FX without inflation adjustment |

The comparison shows that Mordor Intelligence, through disciplined scope selection, variable tracking, and yearly refresh, delivers a balanced and transparent baseline that decision-makers can cite with confidence.

Key Questions Answered in the Report

What is the current value of the Cybersecurity Consulting Market?

The market is valued at USD 20.34 billion in 2026 and is projected to reach USD 48.33 billion by 2031 at a 18.91% CAGR.

Which service line is expanding fastest?

Managed Security Services are growing at 19.10% annually as companies outsource monitoring and incident response.

What is driving the uptake of outcome-based contracts?

Boards demand measurable reductions in breach risk, so they favor engagements linking consultant fees to metrics like dwell-time or audit-finding closure.

Which region shows the highest growth?

Asia-Pacific leads with a 19.35% CAGR, fueled by rising budgets in China, India and Japan.

How does post-quantum encryption influence demand?

NIST’s 2024 PQC standards require new key-management road-maps, spurring a multiyear wave of quantum-readiness consulting.

What is the largest barrier to market growth?

A global shortage of 4.8 million cybersecurity professionals inflates consulting costs and prolongs project timelines.

Page last updated on: