Europe Light Commercial Vehicle Trailer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

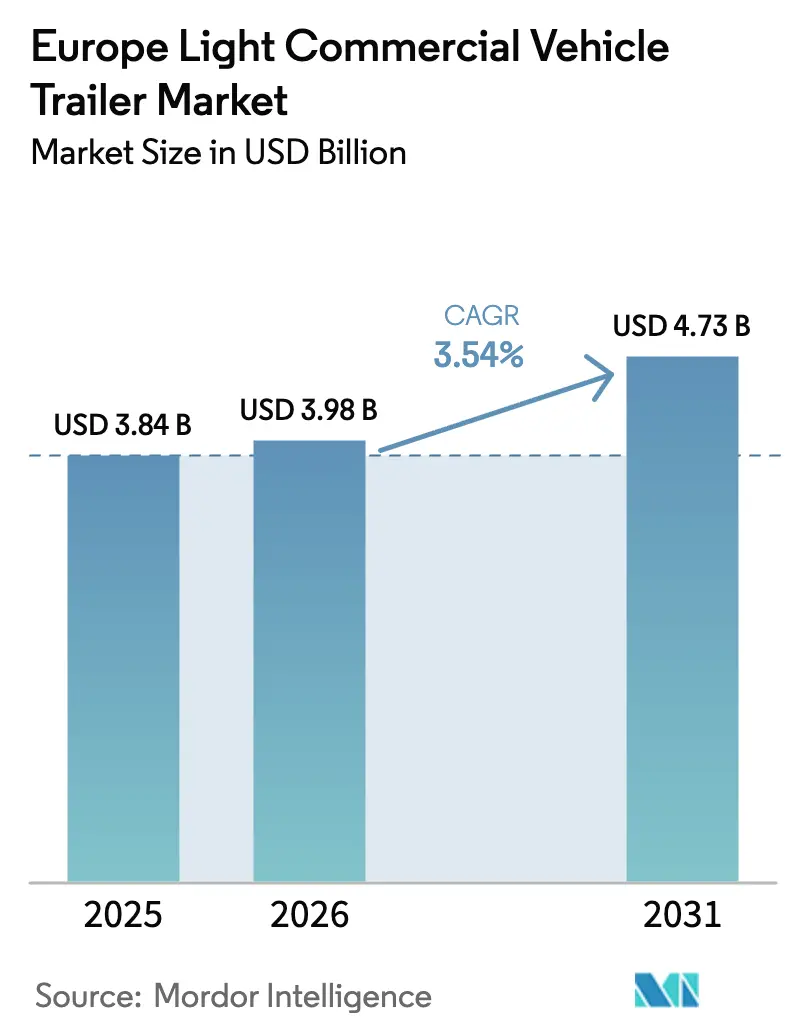

| Base Year Market Size (2025) | USD 3.84 Billion |

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 3.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Light Commercial Vehicle Trailer Market Analysis by Mordor Intelligence

Europe light commercial vehicle trailer market size in 2026 is estimated at USD 3.98 billion, growing from 2025 value of USD 3.84 billion with 2031 projections showing USD 4.73 billion, growing at 3.54% CAGR over 2026-2031. Growth rests on the steady expansion of e-commerce fulfillment networks, tighter CO₂ targets that reward lightweight construction, and urban access rules that push fleet operators toward compact, highly maneuverable trailer formats. Structural upgrades in pan-European micro-fulfillment logistics, rapid cold-chain expansion for pharmaceuticals and perishables, and rising adoption of telematics-enabled fleet management tools deepen market penetration. At the same time, material cost volatility and diesel price swings constrain margins and lengthen replacement cycles, leading many operators to favor leasing over outright purchases. Competitive focus is shifting from basic manufacturing efficiency to integrated digital services and regulatory compliance features that reduce the total cost of ownership.

Key Report Takeaways

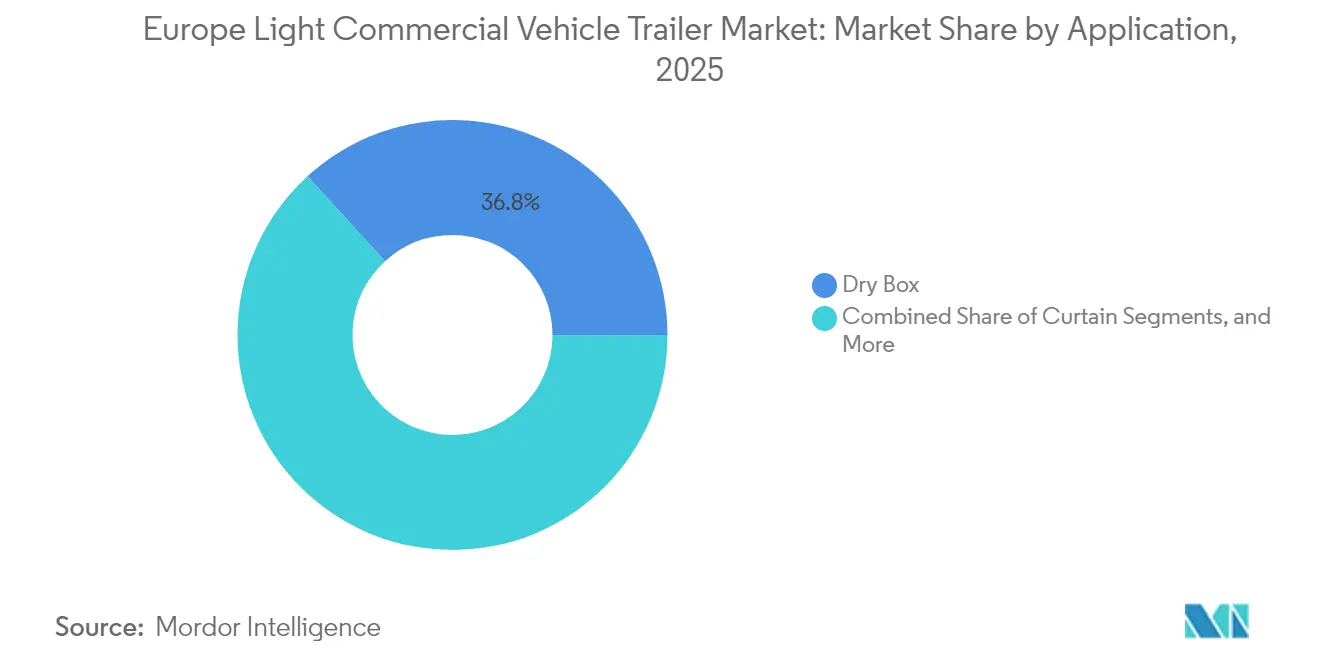

- By application, Dry Box held 36.78% of the Europe light commercial vehicle trailer market share in 2025, while Refrigeration is accelerating at a 7.68% CAGR through 2031.

- By trailer GVWR, units up to 3.5 t captured a 51.85% share of the Europe light commercial vehicle trailer market in 2025 and are projected to grow at a 6.25% CAGR to 2031.

- By axle configuration, tandem-axle designs led with 41.72% of the Europe light commercial vehicle trailer market in 2025, whereas single-axle models recorded the highest projected CAGR of 5.78% through 2031.

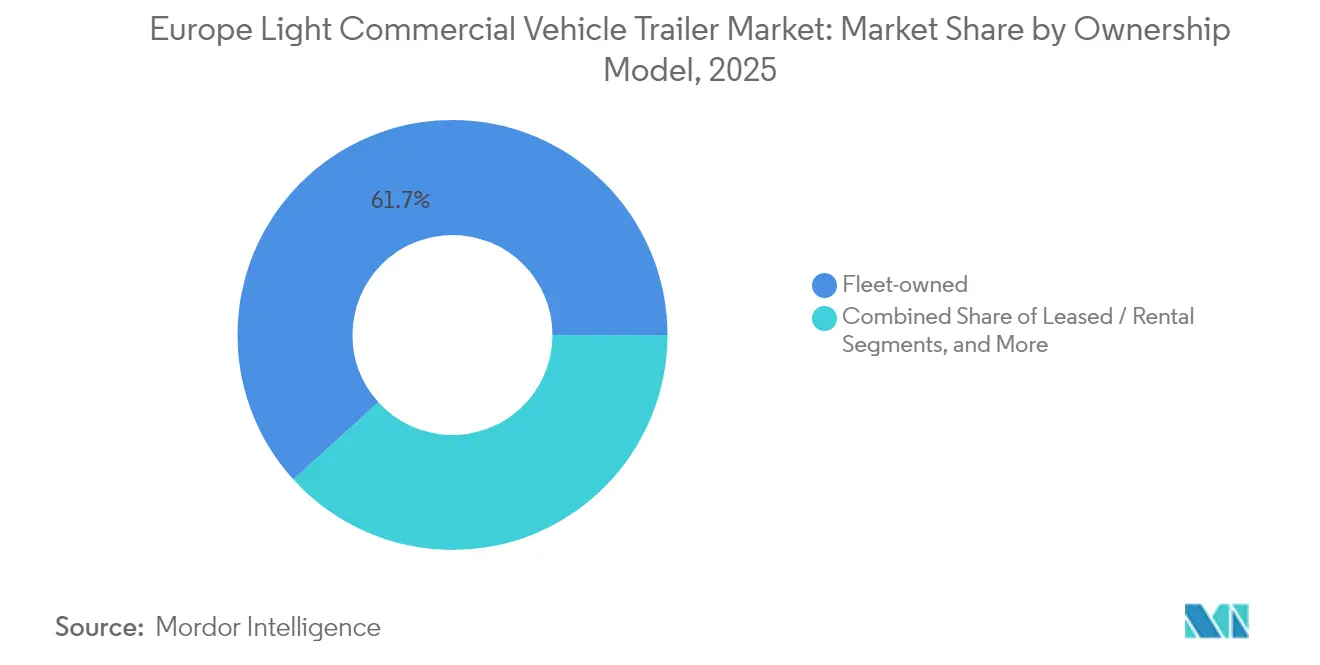

- By ownership model, fleet-owned assets accounted for 61.74% of the Europe light commercial vehicle trailer market in 2025; leased or rental fleets showed the fastest expansion at 5.21% CAGR to 2031.

- By end-user industry, parcel and logistics operators secured 33.88% of the Europe light commercial vehicle trailer market in 2025; food and beverage demand is set to rise at a 5.28% CAGR through 2031.

- By country, Germany retained 25.10% of the Europe light commercial vehicle trailer market in 2025, while Spain is forecast to climb at a 6.37% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Light Commercial Vehicle Trailer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel Boom | +0.8% | Global, with concentration in Germany, Netherlands, United Kindom | Medium term (2-4 years) |

| CO₂ Standards Pushing Lightweight | +0.6% | Europe-wide, strongest in Germany, France, Netherlands | Long term (≥ 4 years) |

| Urban Access Rules Favoring Small Trailers | +0.5% | Major Europe cities, early adoption in London, Paris, Amsterdam | Short term (≤ 2 years) |

| LCV Fleet Electrification Requiring Lightweight Solutions | +0.4% | Northern Europe, Netherlands, Norway, Germany | Long term (≥ 4 years) |

| Pan-EU Micro-Fulfilment Networks Expanding Rapidly | +0.3% | Core Europe markets, spill-over to Eastern Europe | Medium term (2-4 years) |

| OEM-Agnostic Telematics Bundling Trailers | +0.2% | Germany, United Kingdom, France with expansion to Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel-Volume Boom

Surging online sales radically reshape route density and shipment profiles across Europe. Parcel networks now value maneuverability and rapid load-unload capability more than bulk cubic capacity, so fleet managers shift toward curtain-sided and short dry-box formats that fit narrow urban corridors. Micro-fulfillment nodes inside metro areas drive demand for small trailers capable of multiple daily turns. Operators also favor telematics subscriptions that streamline route planning and location-based maintenance, reinforcing the need for digitally enabled trailer platforms.

Tightening CO₂ standards driving lightweight materials

EU Regulation 2019/1242 obliges manufacturers to cut fleetwide CO₂ emissions 15% by 2025 and 30% by 2030 against 2019 baselines[1]“Regulation 2019/1242 on CO₂ Standards,”, European Parliament, europarl.europa.eu. Compliance drives fast adoption of aluminum skins, high-tensile steels, and composite panels that shave 200-300 kg from typical curb weights. Aluminum producer price indices are increasing, sustaining cost pressure even as demand rises. Weight savings also cut toll charges under the revised Eurovignette directive, making lightweight trailers financially attractive despite higher material costs. Ongoing policy discussions to achieve a 90% emission reduction by 2040 further secure the long-run case for lightweight construction.

Urban Delivery-Access Regulations Favoring Small Trailers

Dozens of European cities enforce low-emission or zero-emission zones with weight restrictions limiting heavy rig access. London’s expanded ULEZ and Paris’ ZFE-m rules exemplify this tilt toward lighter equipment. Under Directive 96/53/EC amendments, electric delivery combinations may exceed standard gross weights by 1-2 t without losing urban privileges, encouraging sub-3.5 t trailers matched to electric vans. As cities tighten curfews and loading-bay windows, small trailers able to turn rapidly and park within tight confines offer a tangible operational edge.

Electrification of LCV Fleets Requiring Lightweight Trailer Solutions

Battery packs reduce towing capacity by 200-400 kg relative to diesel counterparts, so fleets migrating toward electric vans require ultra-light, aerodynamically efficient trailers. The International Council on Clean Transportation projects total cost-of-ownership parity for battery-electric urban delivery trucks between 2025 and 2028 in most major EU cities, making electrified fleets commercially viable[2]“Battery-Electric Urban Delivery Trucks TCO Outlook,”, International Council on Clean Transportation, theicct.org. Trailer builders respond with insulated body shells under 800 kg, low-rolling-resistance axles, and integrated power systems for refrigeration or liftgates. Some OEMs also embed charge-through cabling to share grid connections between tractor and trailer, aligning with the Alternative Fuels Infrastructure Regulation that mandates public chargers at 60 km intervals on core TEN-T corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum and Steel Price Surge | -0.4% | Europe-wide, strongest impact in manufacturing hubs Germany, Italy | Short term (≤ 2 years) |

| Volatile Diesel Prices Reducing Fleet CAPEX | -0.3% | Europe-wide, varying by national fuel taxation policies | Short term (≤ 2 years) |

| Supply-Chain Disruptions and Chassis Shortages Persist | -0.2% | Germany, Eastern Europe production corridors | Medium term (2-4 years) |

| Insurance Premiums Rising for Articulated LCV | -0.15% | United Kingdom, Netherlands, high-density urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soaring Aluminum and Steel Prices

Trailer manufacturers grapple with aluminum price swings, tightening margins, and complicating procurement. As raw material costs rise, producers have slightly hiked list prices. Yet, diminished purchasing power among smaller fleet operators curtails the extent of these price hikes, exerting pressure throughout the value chain. Geopolitical events, notably European sanctions on Russian aluminum, have heightened supply constraints. In response, manufacturers are pursuing long-term contracts and diversifying their sourcing, albeit at the cost of added logistical challenges.

Volatile Diesel Costs Reducing Fleet CAPEX

Road freight operators across Central Europe grapple with mounting financial pressures due to fuel price volatility and escalating toll charges. Diesel prices have seen wide fluctuations, influenced by changes in global crude benchmarks and national tax policies. Given that fuel constitutes a significant portion of operating expenses, unexpected price surges compel many carriers to prolong the use of their current vehicles and postpone purchases of new trailers.

In Austria, introducing new toll surcharges and sharp hikes in CO₂-based fees have further squeezed profit margins. Smaller operators, often with limited financial leeway, are increasingly opting for rental models rather than capital-intensive purchases. Without clearer visibility on fuel costs, the sector's investment enthusiasm will likely remain tepid.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Cold Chain Drives Premium Growth

Dry Box bodies retained their workhorse status, holding 36.78% of the Europe light commercial vehicle trailers market share in 2025 and serving general freight from parcel hubs to industrial intermediaries. Curtain-siders remain popular in multipurpose operations demanding side loading, whereas platform and car-carrier variants address niche needs tied to construction and automotive logistics. The premium pricing power of refrigerated trailers offsets higher production costs, making the sub-segment a profit pool for builders with cold-chain expertise.

Refrigeration units contributed the fastest expansion to the European light commercial vehicle trailers market, rising at a 7.68% CAGR through 2031 on the back of booming pharmaceutical and fresh-food demand. The segment benefits from direct-to-consumer grocery platforms and stricter Good Distribution Practice guidelines that specify temperature validation and real-time tracking. New designs such as Schmitz Cargobull’s S.Ko COOL integrate battery-electric refrigeration and solar-assisted chargers, reflecting the convergence of cold-chain requirements with electrification imperatives.

By Trailer GVWR: Urban Access Favors Light Category

Units up to 3.5 t commanded 51.85% of the Europe light commercial vehicle trailers market share in 2025 and are projected to grow at a 6.25% CAGR to 2031, reflecting the strong regulatory push for lighter combinations in congestion-charging zones. These trailers align perfectly with electric vans whose homologated towing limits rarely exceed 1.6 t, and they qualify for lower MAUT distance charges in Germany. Mid-weight trailers between 3.5-7 t maintain balanced payload and volume for regional deliveries, while heavy-duty models above 7 t serve construction and cross-border bulk freight.

Growing metropolitan zero-emission corridors intensify the business case for sub-3.5 t rigs. Fleets also appreciate lower insurance premiums and simpler driver licensing, since many EU states exempt lighter combinations from Class C qualification. Builders offer modular chassis that can be re-rated upward when used outside restricted zones, adding resale flexibility.

By Axle Configuration: Single-Axle Gains Urban Advantage

Tandem-axle bodies hold 41.72 % of the Europe light commercial vehicle trailers market share in 2025. Yet, single-axle trailers notch the highest growth rate at 5.78% through 2031, as city operations require tight turning circles. A single axle cuts tare weight by 120-150 kg, freeing extra payload for parcels or chilled goods. Cost advantages extend to tire wear and brake-service intervals, bringing total ownership savings close to 8% over a five-year lease cycle. New Dutch regulations allow night-time delivery only with noise-optimized equipment, and single-axle designs meet these criteria more easily because of reduced brake and suspension mass.

Multi-axle variants still serve high-density loads like construction panels or modular homes where weight distribution matters. However, tolling schemes that charge per axle further tilt economics toward lighter layouts in general freight.

By Ownership Model: Leasing Flexibility Accelerates

Fleet-owned assets dominated in 2025 with 61.74% of the Europe light commercial vehicle trailers market, but leasing’s 5.21% CAGR through 2031 underscores rising uncertainty over material prices and regulatory trajectories. Long-term leases bundle preventive maintenance, tire replacement, and telematics subscriptions, converting unpredictable costs into fixed monthly fees. Manufacturers also deploy buy-back clauses that guarantee residual values, mitigating depreciation risk when regulations evolve. Large 3PLs now negotiate five-year master leases covering thousands of trailers with shared data dashboards, allowing fine-grained asset rotation between depots.

Rental uptake thrives among seasonal operators in agriculture and retail peaks and small carriers hedging against fuel price volatility. As lightweight composite bodies carry higher up-front prices, capital-intensive ownership gives way to OPEX-oriented leasing that spreads cash obligations.

By End-User Industry: Food Sector Leads Growth

Parcel and logistics networks accounted for 33.88% of the Europe light commercial vehicle trailers market share in 2025, mirroring shopper preferences for next-day delivery and returns processing. However, the food and beverage segment logs the fastest trajectory at 5.28% CAGR through 2031, as grocers and meal-kit providers roll out temperature-certified micro-hubs. Pharmaceutical wholesalers deepen their GDP compliance by adding redundant cooling systems and real-time temperature logs, translating into higher-value equipment orders.

Construction material shippers maintain a solid baseline thanks to public works spending under national recovery plans, while agriculture shows cyclical swings tied to harvest intensity. Retail and FMCG fleets pivot toward omnichannel replenishment, blending store delivery with e-commerce collection points that favor smaller, more frequent loads.

Geography Analysis

Germany anchored 25.10% of the Europe light commercial vehicle trailers market share in 2025, leveraging dense autobahn links and a mature supplier base centered in North Rhine-Westphalia. Facing financial pressures and uncertain operating costs, Haulers are delaying fleet renewals, which softens domestic demand for semitrailers. Registration data highlights a pronounced downward trend, underscoring a widespread trend of postponing replacements. This is especially evident among smaller operators grappling with fuel volatility and narrow profit margins.

Spain is the fastest-growing geography, charting a 6.37% CAGR to 2031. Investments in Mediterranean port logistics and cross-border trade routes with North Africa expand trailer turnover, while EU cohesion funds modernize road links into Castilla-La Mancha and Aragón. Spanish cold-chain warehouses also multiply near Valencia and Barcelona, stimulating refrigerated trailer demand.

Despite a notable rise in business insolvencies in late 2024, France's road transport sector has shown resilience, maintaining stable freight activity. On the other hand, the UK is still wrestling with the administrative challenges posed by Brexit, which have severely limited international logistics. Yet, a boom in domestic parcel deliveries has provided some relief, helping to mitigate the downturn in cross-border trade.

Collectively, the rest of Europe—led by Poland, Czechia, and the Baltics—is capturing growing assembly investment as OEMs diversify away from high-energy-cost Western plants.

Competitive Landscape

Competitive intensity remains moderate. Schmitz Cargobull, riding on its robust production legacy and cutting-edge digital solutions, maintains a significant position in the regional semitrailer market. The company has rolled out integrated telematics solutions by collaborating with platforms such as Webfleet and Frotcom. These innovations boost fleet visibility and operational efficiency and deepen customer loyalty. Furthermore, Schmitz Cargobull's achievement of producing two million axles is a testament to its manufacturing prowess and trustworthiness[3]“Annual Report 2024,”, Schmitz Cargobull, cargobull.com.

KRONE reinforces its position via a telematics alliance with RIO, a subsidiary of Traton, granting live data feeds to joint customers across Germany and Austria. Schwarzmüller invests in its SWIT digital suite, rolling out predictive maintenance algorithms that cut downtime. Medium-sized firms such as Ifor Williams, which gain turnover through livestock and plant trailers specialization, are the least affected by long-haul freight cycles.

Mergers focus on capability expansion: OEMs increasingly view digital services as profit multipliers, so many acquire niche telematics firms to secure recurring revenue streams. The competitive field thus tilts toward a blend of hardware excellence and software ecosystems that lock in customers over multiyear lease contracts.

Europe Light Commercial Vehicle Trailer Industry Leaders

Böckmann Fahrzeugwerke GmbH

Debon Trailers

Humbaur GmbH

Indespension Ltd.

Ifor Williams Trailers Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Sono Solar, a subsidiary of Germany's Sono Group N.V., and Mitsubishi Heavy Industries Thermal Transport Europe (MTTE) launched a solar-powered system for electric trailer refrigeration units (eTRUs), combining MTTE’s TEF1500 eTRU and battery pack with Sono Solar’s photovoltaic modules and charge controller.

- July 2025: Martin Group acquired Montracon to significantly expand its manufacturing capacity, enhance operational capabilities, and strengthen its geographical presence across the United Kingdom and mainland Europe.

Europe Light Commercial Vehicle Trailer Market Report Scope

The Europe Light commercial Vehicle Trailer market is segmented by Application (Curtain, Refrigeration, Dry Box, Tippers, and Other Applications) and Geography

| Curtain |

| Refrigeration |

| Dry Box |

| Flat-bed / Platform |

| Tippers |

| Car Transporter |

| Other Applications |

| Up to 3.5 t |

| 3.5 - 7 t |

| Above 7 t |

| Single-axle |

| Tandem-axle |

| Multi-axle |

| Fleet-owned |

| Leased / Rental |

| Private / Owner-operator |

| Parcel and Logistics |

| Construction and Building Materials |

| Food and Beverage |

| Retail and FMCG |

| Agriculture and Livestock |

| Others |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Denmark |

| Estonia |

| Rest of Europe |

| By Application | Curtain |

| Refrigeration | |

| Dry Box | |

| Flat-bed / Platform | |

| Tippers | |

| Car Transporter | |

| Other Applications | |

| By Trailer GVWR | Up to 3.5 t |

| 3.5 - 7 t | |

| Above 7 t | |

| By Axle Configuration | Single-axle |

| Tandem-axle | |

| Multi-axle | |

| By Ownership Model | Fleet-owned |

| Leased / Rental | |

| Private / Owner-operator | |

| By End-user Industry | Parcel and Logistics |

| Construction and Building Materials | |

| Food and Beverage | |

| Retail and FMCG | |

| Agriculture and Livestock | |

| Others | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Denmark | |

| Estonia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the European light commercial vehicle trailers market?

The European light commercial vehicle trailers market is valued at USD 3.98 billion in 2026 and is forecast to reach USD 4.73 billion by 2031.

Which application segment is growing fastest?

Refrigerated trailers lead growth with a 7.68% CAGR thanks to expanding cold-chain needs in pharmaceuticals and fresh food.

How do EU CO₂ rules influence trailer design?

Regulation 2019/1242 and VECTO measurement link tolls and fleet targets to trailer weight, driving rapid adoption of lightweight materials.

What factors are driving trailer leasing demand?

Material price volatility, electrification uncertainties, and the need for telematics upgrades encourage operators to favor flexible lease arrangements.

Which country offers the highest growth outlook?

Spain shows the highest CAGR at 6.37% through 2031, underscored by port logistics investments and expanding Mediterranean trade flows.

Page last updated on: