Electric Boat And Ship Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

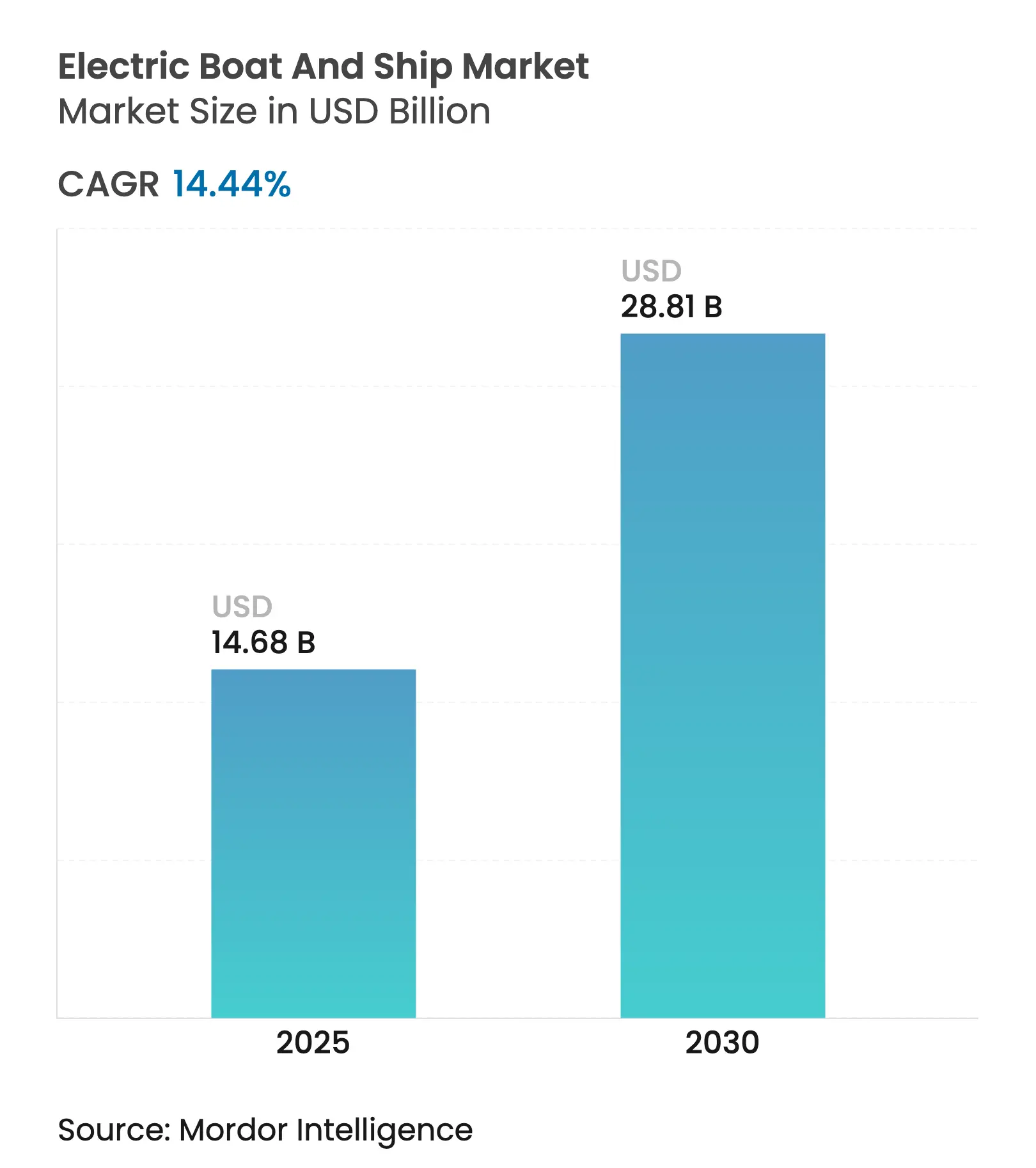

| Market Size (2025) | USD 14.68 Billion |

| Market Size (2030) | USD 28.81 Billion |

| Growth Rate (2025 - 2030) | 14.44 % CAGR |

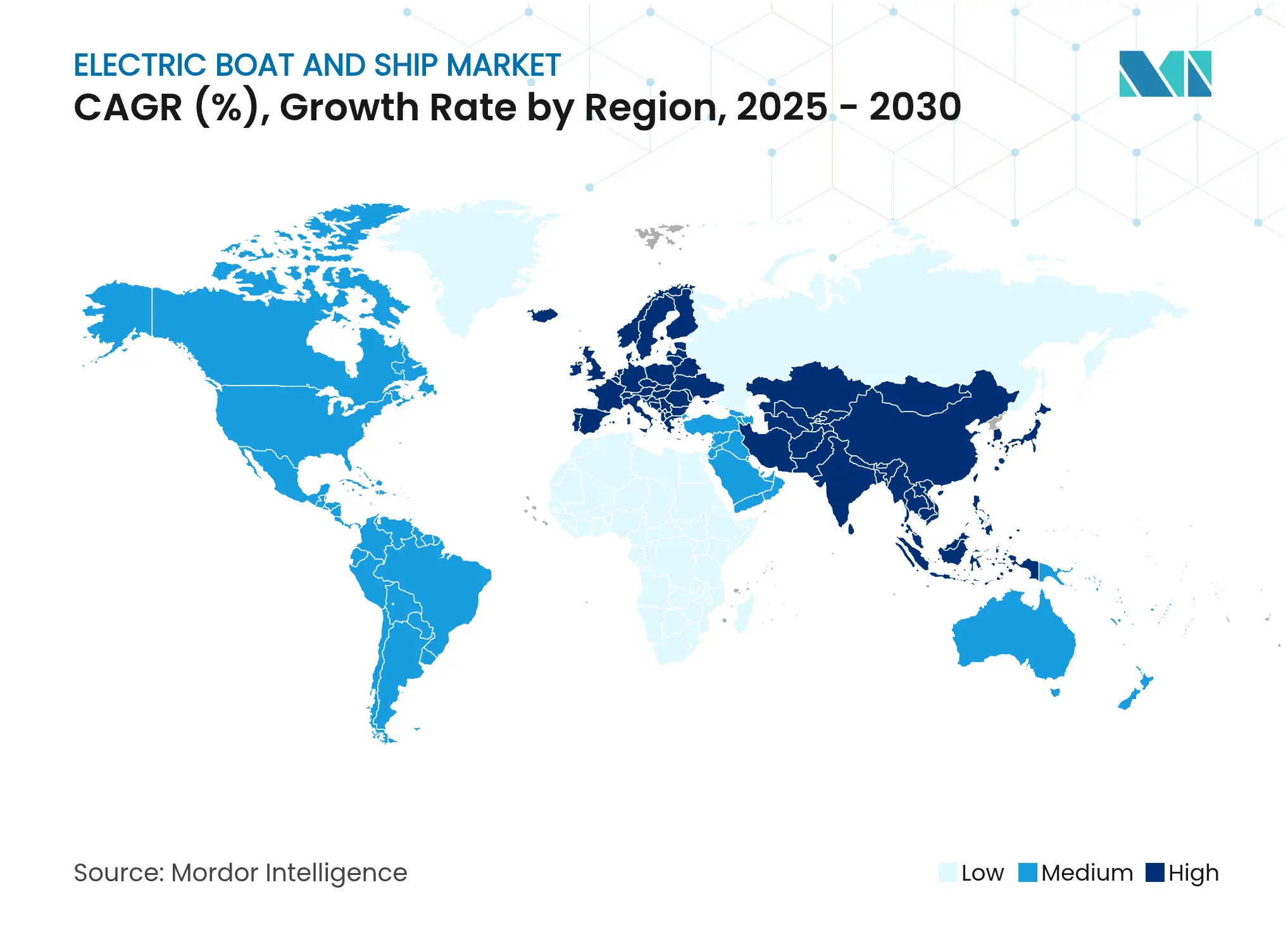

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

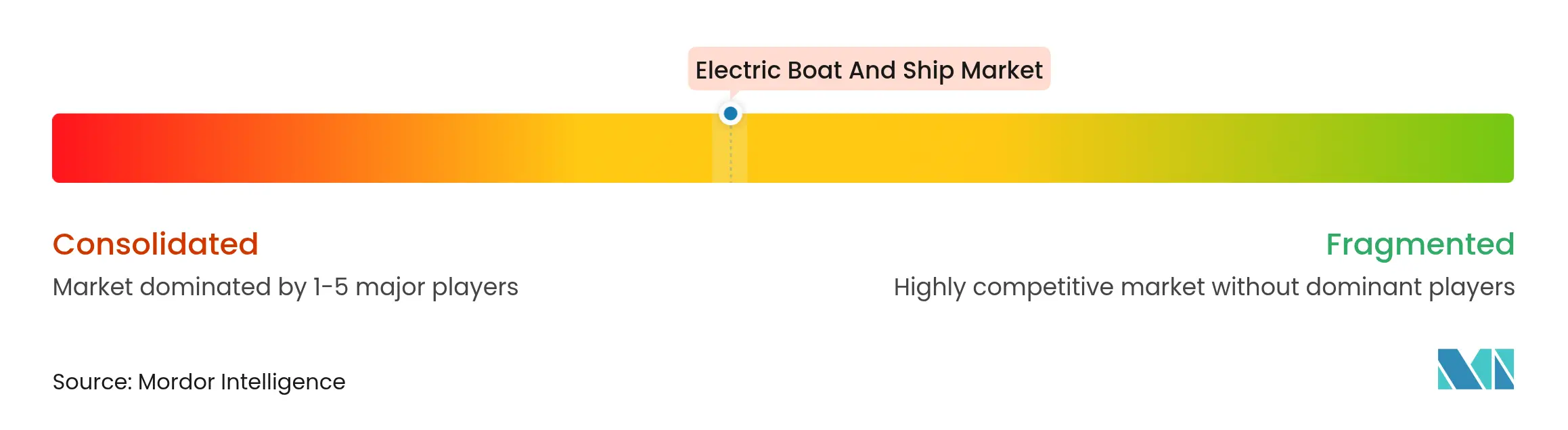

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Electric Boat And Ship Market Analysis by Mordor Intelligence

The electric boat and ship market size is valued at USD 14.68 billion in 2025 and is forecast to reach USD 28.81 billion by 2030, translating into a 14.44% CAGR during the forecast period. Regulatory tailwinds from the International Maritime Organization’s 2025 net-zero framework, joined by national funding programs and the infrastructure scheme, accelerate vessel electrification. Equipment manufacturers are scaling integrated propulsion lines, port authorities are rolling out high-capacity shore-power grids, and battery suppliers commercialize marine-grade solid-state cells. Together, those forces shorten payback periods, expand operational envelopes, and draw new entrants into the electric boat and ship market. Vessel owners that must comply with emission control areas prioritize pure-electric ferries, while container feeders adopt hydrogen-hybrid packages to extend range without diesel backup.

Key Report Takeaways

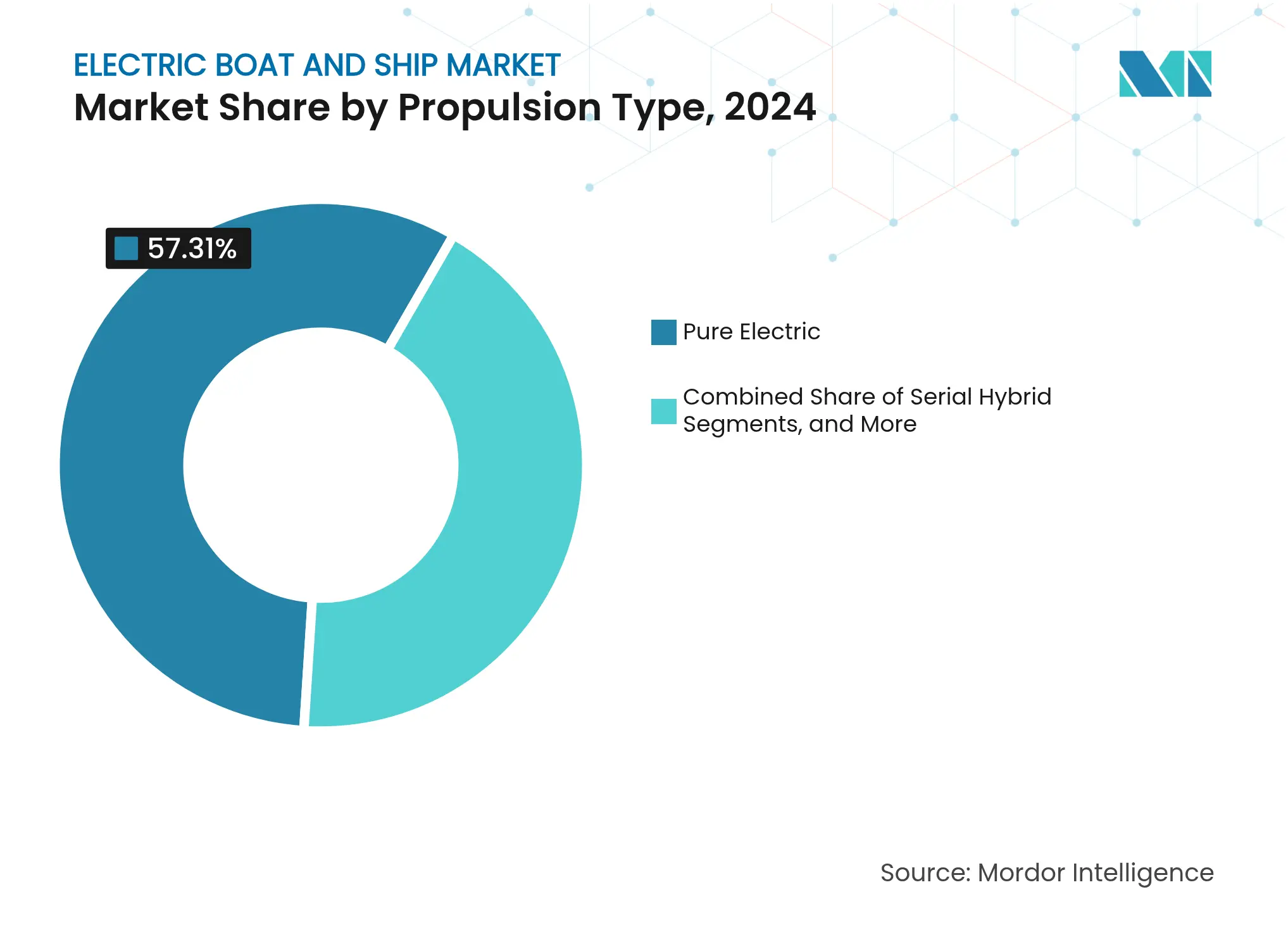

- By propulsion type, pure-electric systems led with 57.31% of the electric boat and ship market share in 2024; hydrogen-hybrid options are projected to expand at a 16.92% CAGR through 2030.

- By battery chemistry, lithium-ion accounted for 72.38% of the electric boat and ship market share in 2024, while solid-state variants are advancing at a 16.71% CAGR to 2030.

- By vessel type, passenger ferries captured 43.29% of the electric boat and ship market size in 2024; cargo and container feeders record the fastest CAGR at 18.37% through 2030.

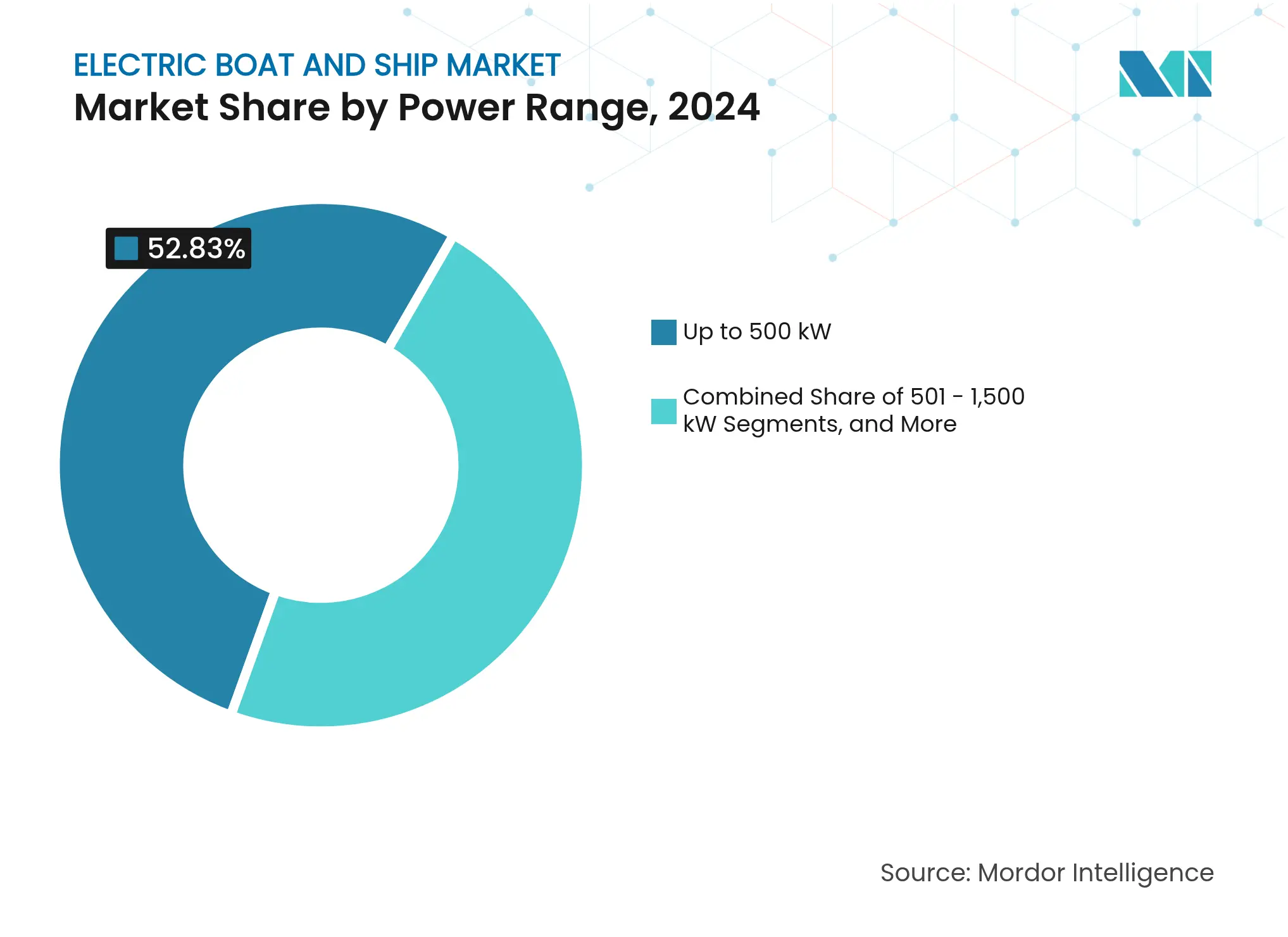

- By power range, units up to 500 kW held 52.83% share of the electric boat and ship market size in 2024, whereas the 1,501–3,000 kW bracket is pacing at an 18.22% CAGR through 2030.

- By hull material, fiberglass hulls dominated with a 45.13% of the electric boat and ship market share in 2024, while advanced composites represent the quickest-rising material segment, with a 16.51% CAGR through 2030.

- By end-use, new-build programs commanded 68.29% of the electric boat and ship market share in 2024; retrofit projects, at 15.72% through 2030.

- By geography, Europe commanded a 37.28% of the electric boat and ship market share in 2024; Asia-Pacific is the fastest-growing region with an 18.72% CAGR to 2030.

Global Electric Boat And Ship Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stricter IMO GHG Targets (MEPC-80) Stricter IMO GHG Targets (MEPC-80) | +2.8% | Global, with early adoption in Europe and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.8% | Geographic Relevance:Global, with early adoption in Europe and North America | Impact Timeline:Medium term (2-4 years) |

Falling Marine-Battery Prices Per kWh Falling Marine-Battery Prices Per kWh | +2.1% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) | |||

Government Subsidies For E-Ferries And Workboats Government Subsidies For E-Ferries And Workboats | +1.9% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Port-Authority Shore-Power MOUs Port-Authority Shore-Power MOUs | +1.6% | Major global ports, concentrated in developed markets | Medium term (2-4 years) | |||

Growing Electric-Leisure Rental Demand Growing Electric-Leisure Rental Demand | +1.4% | Europe and North America coastal regions | Short term (≤ 2 years) | |||

Naval And Coast Guard Decarbonization Budgets Naval And Coast Guard Decarbonization Budgets | +1.2% | NATO countries and developed naval forces | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Stricter IMO GHG Targets

The International Maritime Organization’s binding emissions framework, finalized in 2025, introduces a global fuel standard and pricing mechanism, shifting procurement criteria toward zero-emission propulsion [1]“IMO Net-Zero Framework Adopted in 2025,”, International Maritime Organization, imo.int. Classification societies such as DNV and Lloyd’s Register updated their 2025 rules to ease type approval for battery and hydrogen systems[2]“MEPC-80 GHG Measures and Implications,”, DNV, dnv.com. Early compliance work influences new-build specifications, and complementary seafarer-training guidelines ensure crews can safely operate electric and alternative-fuel vessels. With enforcement beginning in 2028, owners who operate inside emission control areas face direct financial incentives to deploy electric boat and ship market technologies. The regulatory package, therefore, converts electrification from a voluntary sustainability exercise into a core license-to-operate requirement.

Falling Marine-Battery Prices

Battery technology developments are transforming the maritime industry, as reduced costs and enhanced designs make electric propulsion feasible for large vessels. The marine sector benefits from modular battery systems adapted from automotive industry innovations, which enable customizable solutions for maritime applications. Developing solid-state technologies improves energy storage capabilities, increasing vessel range and operational flexibility.

Research institutions are developing new battery chemistries compatible with marine environments to provide sustainable power for auxiliary systems and onboard equipment. Manufacturing innovations include low-temperature processing methods that reduce energy consumption and improve safety compared to conventional high-temperature techniques. These technological improvements reduce the cost difference between electric and diesel-powered vessels, enhancing the economic viability of maritime electrification.

Port-Authority Shore-Power MOUs

Memorandums among ports, utilities, and OEMs are building high-capacity charging corridors. The U.S. Environmental Protection Agency channels Clean Ports funding toward 10-MW shore-power links that cut berthed emissions and supply in-harbor ferries. European ports now require emission-free stays, incentivizing operators to specify battery systems that can fast-charge during turnaround windows. Standardized connectors and automated cable-management rigs reduce compatibility hurdles, allowing route planners to count on predictable charging stops. These infrastructure commitments break the chicken-and-egg cycle, extending the electric boat and ship market beyond pilot harbors into full coastal networks.

Naval and Coast-Guard Decarbonization Budgets

Defense agencies prioritize electric propulsion for noise reduction, thermal-signature suppression, and reduced refueling risk. The U.S. Coast Guard’s interim rules clarify certification processes for patrol craft retrofits, triggering prototype contracts for battery-hybrid cutters. European navies allocate research funds to auxiliary power modules that replace diesel generators during low-speed maneuvers, cutting stack emissions in ecologically sensitive zones. Long acquisition timelines mean technologies proven under military rigor often migrate into commercial tugboats and research vessels later, reinforcing the electric boat and ship industry supply chain with high-reliability components and verified safety cases.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited Operating Range Vs. Diesel Limited Operating Range Vs. Diesel | -2.3% | Global, more pronounced in long-haul routes | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-2.3% | Geographic Relevance:Global, more pronounced in long-haul routes | Impact Timeline:Medium term (2-4 years) |

High Retrofit CAPEX and Class-Society Fees High Retrofit CAPEX and Class-Society Fees | -1.8% | Global, particularly affecting older fleets | Short term (≤ 2 years) | |||

Maritime Battery Fire-Safety Certification Gap Maritime Battery Fire-Safety Certification Gap | -1.4% | Global, with stricter requirements in developed markets | Medium term (2-4 years) | |||

Maritime-Grade Li-Ion Cell Supply Risk Maritime-Grade Li-Ion Cell Supply Risk | -1.1% | Global supply chains, concentrated in Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Operating Range vs. Diesel

Even with 300 Wh/kg lithium-ion packs, electric vessels hold just 3% of diesel’s volumetric energy, restricting routes lacking shore-power nodes. Weather-related hotel-load surges and headwind drag intensify consumption, forcing conservative voyage planning. Laboratory-level 600 Wh/kg solid-state milestones hint at future relief but remain commercially distant. Operators deploy hybrid architectures or keep diesel auxiliaries on board, complicating maintenance regimes. Until megawatt-scale charging becomes routine and battery densities double, range anxiety curbs adoption beyond predictable ferry and harbor assignments.

Maritime Battery Fire-Safety Certification Gap

Thermal-runaway case studies from early ferry deployments pushed regulators to draft new test protocols. Containment, ventilation, and extinguishing systems add weight and complexity, while prototype verification can extend project timelines by 12 months[3]“Interim Policy on Electric Propulsion Systems,”, U.S. Coast Guard, uscg.mil. Insurers levy high premiums without actuarial loss data, raising operating costs. Progress is visible—ABS and Lloyd’s Register released hazard-identification guides in 2025—but certification uncertainty is a deterrent until a harmonized global code emerges.

Segment Analysis

By Propulsion Type: Hydrogen-Hybrid Systems Extend Range

Pure-electric propulsion commanded 57.31% of the electric boat and ship market share in 2024, reflecting maturity for short-haul ferries and harbor craft. Fleet operators appreciate the low vibration, instant torque, and simplified drivetrains that cut maintenance visits. Yet the electric boat and ship market increasingly pairs batteries with proton-exchange-membrane fuel cells to eliminate diesel from 200–600 nautical-mile trades. Hydrogen-hybrid configurations, posting a 16.92% CAGR to 2030, allow mid-voyage refueling in under 20 minutes at emerging bunkering hubs. Fuel-cell stacks between 1 MW and 3 MW supplement a downsized battery, smoothing load spikes and capturing regenerative gains during dynamic positioning. Safety codes demand double-walled tanks and continuous gas monitoring, but classification frameworks issued in 2025 streamline type approval. The operational outcome is a vessel that meets zero-emission mandates yet preserves dispatch flexibility—a combination that explains accelerating orders across passenger, feeder, and offshore-support segments.

Hydrogen-hybrid adoption also shifts component demand. Stack integrators collaborate with motor makers to harmonize voltage windows, while cryogenic onboard storage sparks innovation in carbon-fiber composite cylinders. Shipyards embed modular zoning that isolates gas handling from accommodation spaces, preventing regulatory delays. For suppliers, the hydrogen-ready niche offers margins above commoditized battery packs, and many aim to lock in long-term service contracts covering fuel logistics, compression, and predictive diagnostics. Consequently, the propulsion race pivots on ecosystem partnerships rather than standalone hardware.

Note: Segment shares of all individual segments available upon report purchase

By Battery Chemistry: Solid-state promises higher density

Lithium-ion retained 72.38% of the electric boat and ship market share in 2024 on the strength of mature supply chains and multi-source procurement options. NMC and LFP cathodes balance cost, energy, and safety for most workboats, making them the default bid specification for the electric boat and ship market. Solid-state labs, however, delivered 600 Wh/kg prototypes that survive 1,000 cycles and tolerate temperatures from –10 °C to 60 °C without liquid electrolytes, eliminating gassing risks. Expected commercial release after 2027 underpins a 16.71% CAGR forecast for solid-state penetration. Because marine operators value cycle life and zero-maintenance seals, early adopters negotiate conditional contracts that flip to solid-state once class-society approvals clear.

Lead-acid continues in cost-sensitive barges where weight penalties are manageable, while nickel-metal-hydride packs serve arctic patrol craft needing cold-temperature resilience. Super-capacitors appear as power buffers, absorbing hotel-load spikes and recovering braking energy in crew-transfer vessels. Battery rooms now mandate distributed architecture to segregate chemistries and optimize thermal management, pushing integrators to design universal battery-management software capable of cross-chemistry control. For OEMs, chemistry choice is becoming a strategic differentiator, influencing warranties and residual-value guarantees that underpin financing terms.

By Vessel Type: Cargo feeders surge

Passenger ferries held a 43.29% of the electric boat and ship market share in 2024, thanks to fixed routes and frequent berth time that align with overnight charging. The electric boat and ship market is now expanding into cargo and container feeders, anticipated to record an 18.37% CAGR because emission-free port zones penalize auxiliary engines at berth. Feeders operate 100–400 nautical-mile loops, a sweet spot for 4–8 MWh battery arrays combined with low-drag hulls. Pilot projects in the Baltic and Pearl River Delta demonstrate 25% savings on operating expenses versus diesel once electricity is contracted on time-of-day tariffs.

Leisure boats migrate toward electric for silent cruising and simplified winterization, aided by trailerable fast-chargers and marina solar canopies. Workboats—tugs, pilot cutters, and dredgers—experiment with high-power hybrid drives that deliver instant torque during bollard pulls yet idle emission-free while waiting on station. Defense and patrol craft implement partial electrification for loiter modes, enabling acoustic stealth during reconnaissance. Overall, the vessel-type mosaic illustrates broadening applicability that moves beyond the early ferry niche, anchoring durable growth for the electric boat and ship industry.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Power Range: Mid-Range Gains Momentum

Systems up to 500 kW still dominate at 52.83% of the electric boat and ship market share in 2024, covering water-taxi fleets and day-tour boats. Yet the 1,501–3,000 kW category posts an 18.22% CAGR through 2030, as hybrid-electric tugboats, offshore-supply vessels, and medium tankers request multi-megawatt propulsion. Volvo Penta’s 2025 helm-to-propeller hybrid kit, pairing D13 IPS pods with 160 kW motors, is emblematic of turnkey solutions that lower integration risk. Scaling further, Arc Boats’ 4,000-hp tug design incorporates 6 MWh of batteries, proving that modular racks can satisfy peaks without resorting to diesel standby.

Power-range segmentation affects onboard architecture. Low-power boats favor single-string voltage platforms below 900 V, easing insulation and crew training. Mid-range vessels adopt 1,000–1,500 V DC rings to shrink cable cross-sections and cut copper weight. High-power craft integrate liquid-cooled busbars, active harmonic filters, and redundant energy-management controllers to pass class-society fault-tolerance tests. Component suppliers, therefore, develop scalable sub-assemblies—motors, inverters, and DC-DC converters—that slot into different kilowatt tiers, reducing engineering hours per project and accelerating serial production.

Note: Segment shares of all individual segments available upon report purchase

By Hull Material: Composites Lighten Loads

Fiberglass maintained 45.13% of the electric boat and ship market share in 2024, favored for small craft where tooling amortization is low. However, advanced composites such as carbon-fiber-reinforced polymers expand at a 16.51% CAGR through 2030 because every kilogram saved equals extra battery range. Research at Chalmers University demonstrated that structural batteries with 70 GPa stiffness and 30 Wh/kg energy content integrate storage into the hull skin while stiffening the laminate. Aluminum persists in workboats that demand dent tolerance and field-repair welding. Steel dominates displacement hulls above 100 m length, though designers now incorporate composite superstructures to lower the center of gravity and offset battery mass.

Material choice shapes electromagnetic interference management, grounding schemes, and heat-dissipation strategies critical to battery longevity. Composite hulls require embedded copper mesh or conductive coatings to route stray currents, while steel vessels utilize hull return paths that simplify wiring but raise galvanic corrosion risks. Yard capability becomes a selection criterion as vacuum-infusion ovens or precision milling determine the repeatability of composite laminates. Consequently, hull materials and propulsion packages co-evolve, creating bundled specification pathways in the electric boat and ship market.

By End-Use: Retrofit Demand Gathers Pace Despite New-Build Dominance

New-build programs accounted for a commanding 68.29% of the electric boat and ship market share in 2024, reflecting the preference of operators to specify batteries, power electronics, and fire-safety systems at the design stage when integration costs are lowest. This dominance means the new-build portion contributes to the bulk of the electric boat and ship market size today, reinforcing orderbooks at European and Asia-Pacific yards that now offer electric-ready designs as standard. However, operators with younger diesel fleets face regulatory pressure well before natural replacement dates, prompting a surge of feasibility studies that position retrofit projects as a strategic shortcut to compliance. Yard groups have responded by developing pre-engineered battery rooms and modular cabling kits that compress conversion downtime from months to weeks, lowering revenue disruption for ferry and tug owners.

Retrofit activity expected to grow at15.72% through 2030, advancing on a steeper trajectory than fresh builds because subsidy schemes in Europe and North America explicitly earmark funds for existing tonnage. Classification societies released template approval guides in 2025 that streamline structural analyses and fire-suppression layouts, trimming soft costs that previously stifled retrofits. As lithium-ion pack prices fall below USD 100 per kWh, ROI calculations break even within seven years for vessels with predictable duty cycles, encouraging family-owned fleets to advance. Early successes in converting pilot cutters and harbor tugs are building confidence, and suppliers expect the retrofit slice of the electric boat and ship market to double its share by decade-end as port-side charging networks mature and financing packages become commonplace.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

Geography Analysis

Europe’s 37.28% of the electric boat and ship market share in 2024 stems from longstanding emission control areas, port-side power mandates, and cohesive subsidy frameworks. Scandinavian yards standardize battery rooms, and classification bodies headquartered in the region accelerate approval cycles. Fast-ferry corridors along the Norwegian coast, the Thames, and the Adriatic employ integrated charging berths, feeding follow-on demand in river-cruise retrofits and pilot boats.

Asia-Pacific registers an 18.72% CAGR through 2030, powered by China’s export-oriented shipyards embedding electric options into baseline specifications and Japan’s hydrogen-hybrid demonstrations aligned with national energy-security goals. South Korea’s conglomerate yards pair domestic battery cells with in-house motors, lowering bill-of-material costs. Regional governments pledge green-corridor funding across Yangtze feeder runs and intra-bay ferries, prioritizing the electric boat and ship market within broader industrial policy.

North America leverages Environmental Protection Agency Clean Ports funding and California’s at-berth zero-emission mandates to retrofit harbor fleets. The Middle East and Africa remain nascent but are exploring electric crew vessels for offshore wind farms. Latin America sees early pilots in Brazilian FPSO support craft, signaling gradual but widening global diffusion.

Competitive Landscape

Market Concentration

Industry concentration is moderate. ABB, Wärtsilä, and Siemens Energy exploit legacy customer bases to position turnkey power-train packages, bundling batteries, drives, and remote diagnostics. Their market share edge stems from 24/7 service networks and harmonized spares, assuring operators of uptime in mission-critical ferry schedules. Corvus Energy co-locates pack assembly near Scandinavian yards, reducing logistics overhead and lead-time variability.

Start-ups pursue design-led disruption. Candela’s hydrofoiling hull lowers energy draw by 80%, extending battery range while showcasing consumer-level ride comfort. Arc Boats focuses on high-bollard-pull tugboats, integrating chassis, pack, and software in-house to compress development cycles. Technology differentiation now hinges on energy-management algorithms, thermal-hazard mitigation, and integrated lifecycle services rather than standalone motors or cells.

Strategic alliances proliferate: shipyards sign framework deals with cell manufacturers to guarantee volume, while port authorities contract OEMs for charging infrastructure, ensuring end-to-end interoperability. As regulatory complexity rises, companies offering certification advisory, crew-training modules, and financing toolkits elevate their value proposition. The net result is a layered competitive map where system orchestrators wield influence over component vendors, shaping the trajectory of the electric boat and ship market.

Electric Boat And Ship Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Los Angeles-based startup, Arc Boats, clinched a landmark USD 160 million contract, thrusting electric tugboats into the spotlight of maritime innovation. The substantial agreement with Curtin Maritime marks a pivotal move towards eco-friendly port operations.

- June 2025: Enova, a Norwegian government enterprise, funds seven electric vessels and four charging stations with NOK 362 million (approximately USD36.42 million). This initiative aims to accelerate the adoption of electric mobility in the maritime sector, contributing to reduced emissions and supporting Norway's sustainability goals.

- August 2024: Volvo Penta introduced a pioneering hybrid-electric propulsion package, underscoring its dedication to the evolution of marine technology for both yachts and commercial marine sectors. This distinctive package promises a cohesive hybrid-electric experience, prioritizing user satisfaction. The system facilitates effortless shifts between power modes, boosting performance, comfort, and operational efficiency.

Table of Contents for Electric Boat And Ship Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Drivers

- 4.1.1Stricter IMO GHG Targets (MEPC-80)

- 4.1.2Falling Marine-Battery Prices Per kWh

- 4.1.3Government Subsidies For E-Ferries And Workboats

- 4.1.4Growing Electric-Leisure Rental Demand

- 4.1.5Port-Authority Shore-Power MOUs

- 4.1.6Naval And Coast Guard Decarbonization Budgets

- 4.2Market Restraints

- 4.2.1Limited Operating Range Vs. Diesel

- 4.2.2High Retrofit CAPEX and Class-Society Fees

- 4.2.3Maritime Battery Fire-Safety Certification Gap

- 4.2.4Maritime-Grade Li-Ion Cell Supply Risk

- 4.3Value / Supply-Chain Analysis

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter;s Five Forces

- 4.6.1Bargaining Power of Buyers

- 4.6.2Bargaining Power of Suppliers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value (USD))

- 5.1By Propulsion Type

- 5.1.1Pure Electric

- 5.1.2Serial Hybrid

- 5.1.3Parallel Hybrid

- 5.1.4Hydrogen-Hybrid

- 5.2By Battery Chemistry

- 5.2.1Lithium-ion

- 5.2.2Lead-acid

- 5.2.3Solid-state

- 5.2.4Nickel-based (Ni-MH)

- 5.2.5Super-capacitors

- 5.3By Vessel Type

- 5.3.1Passenger Ferries

- 5.3.2Leisure Boats and Yachts

- 5.3.3Cargo and Container Feeders

- 5.3.4Workboats and Service Vessels

- 5.3.5Defense and Patrol Craft

- 5.4By Power Range (kW)

- 5.4.1Up to 500

- 5.4.2501 - 1,500

- 5.4.31,501 - 3,000

- 5.4.4Above 3,000

- 5.5By Hull Material

- 5.5.1Fiberglass

- 5.5.2Aluminum

- 5.5.3Steel

- 5.5.4Advanced Composites

- 5.6By End-Use

- 5.6.1New-build

- 5.6.2Retrofit

- 5.7By Geography

- 5.7.1North America

- 5.7.1.1United States

- 5.7.1.2Canada

- 5.7.1.3Rest of North America

- 5.7.2South America

- 5.7.2.1Brazil

- 5.7.2.2Argentina

- 5.7.2.3Rest of South America

- 5.7.3Europe

- 5.7.3.1Germany

- 5.7.3.2United Kingdom

- 5.7.3.3France

- 5.7.3.4Italy

- 5.7.3.5Spain

- 5.7.3.6Russia

- 5.7.3.7Rest of Europe

- 5.7.4Asia-Pacific

- 5.7.4.1China

- 5.7.4.2Japan

- 5.7.4.3South Korea

- 5.7.4.4India

- 5.7.4.5Rest of Asia-Pacific

- 5.7.5Middle East and Africa

- 5.7.5.1United Arab Emirates

- 5.7.5.2Saudi Arabia

- 5.7.5.3Turkey

- 5.7.5.4Egypt

- 5.7.5.5South Africa

- 5.7.5.6Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Strategic Moves

- 6.2Market Share Analysis

- 6.3Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4ABB Ltd

- 6.5Corvus Energy

- 6.6Torqeedo GmbH

- 6.7Vision Marine Technologies Inc.

- 6.8Groupe Beneteau

- 6.9Duffy Electric Boat Company

- 6.10Greenline Yachts

- 6.11Hyundai Heavy Industries Co. Ltd.

- 6.12Hanwha Ocean Co., Ltd.

- 6.13Wartsila Corporation

- 6.14Kongsberg Gruppen ASA

- 6.15Siemens Energy (Marine)

- 6.16Yara Marine Technologies

- 6.17Ganz Boats GmbH

- 6.18Domani Yachts

- 6.19Ruban Bleu

- 6.20ElectraCraft Boats

- 6.21Grove Boats SA

- 6.22Quadrofoil

- 6.23Candela Technology AB

- 6.24Oceanvolt

- 6.25Leclanche SA

- 6.26Saft (TotalEnergies)

- 6.27Baltic Yachts

- 6.28Rand Electric Boats

7. Market Opportunities and Future Outlook

Global Electric Boat And Ship Market Report Scope

An electric boat is a form of electric vehicle designed to carry off marine operations by propelling the boat through batteries rather than by fuel. The batteries used in electric boats are similar to the batteries used in electric vehicles. Electric ships are mainly ferries and small passenger ships on inland waterways that sail completely with electricity. They sail only short distances and dock often.

The scope of the report covers segmentation based on propulsion type, battery type, carriage type, and geography. By propulsion type, the market is segmented into hybrid and pure electric. By battery type, the market is segmented into lead-acid, lithium-ion, and nickel-based batteries. By carriage type, the market is segmented into passenger and cargo, and by geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The report also provides market sizing and forecast for all the above-mentioned segments.