Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 33.38 Billion |

| Market Size (2026) | USD 37.07 Billion |

| Market Size (2031) | USD 62.69 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

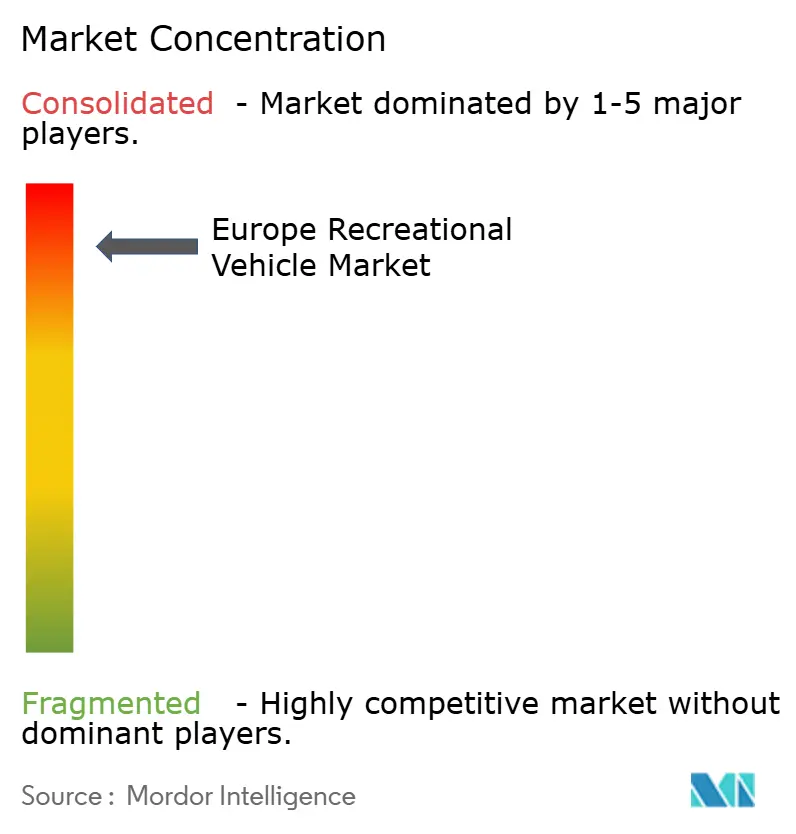

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Recreational Vehicle Market Analysis by Mordor Intelligence

The Europe Recreational Vehicle market size is expected to grow from USD 33.38 billion in 2025 to USD 37.07 billion in 2026 and is forecast to reach USD 62.69 billion by 2031 at 11.08% CAGR over 2026-2031. This robust growth trajectory reflects the sector's resilience following post-pandemic recovery and structural shifts in European leisure patterns. The market's expansion is underpinned by regulatory tailwinds, particularly the EU Parliament's approval of extending B-license eligibility to 4.25-tonne motorhomes by 2028, which will unlock access for millions of additional drivers.

Key Report Takeaways

- By vehicle type, motorhomes led with a 53.72% Europe recreational vehicle market share in 2025, whereas campervans are advancing at an 11.62% CAGR through 2031.

- By propulsion, diesel ICE units commanded a 91.10% share of the Europe recreational vehicle market size in 2025, while battery-electric models are forecast to expand at a 36.91% CAGR to 2031.

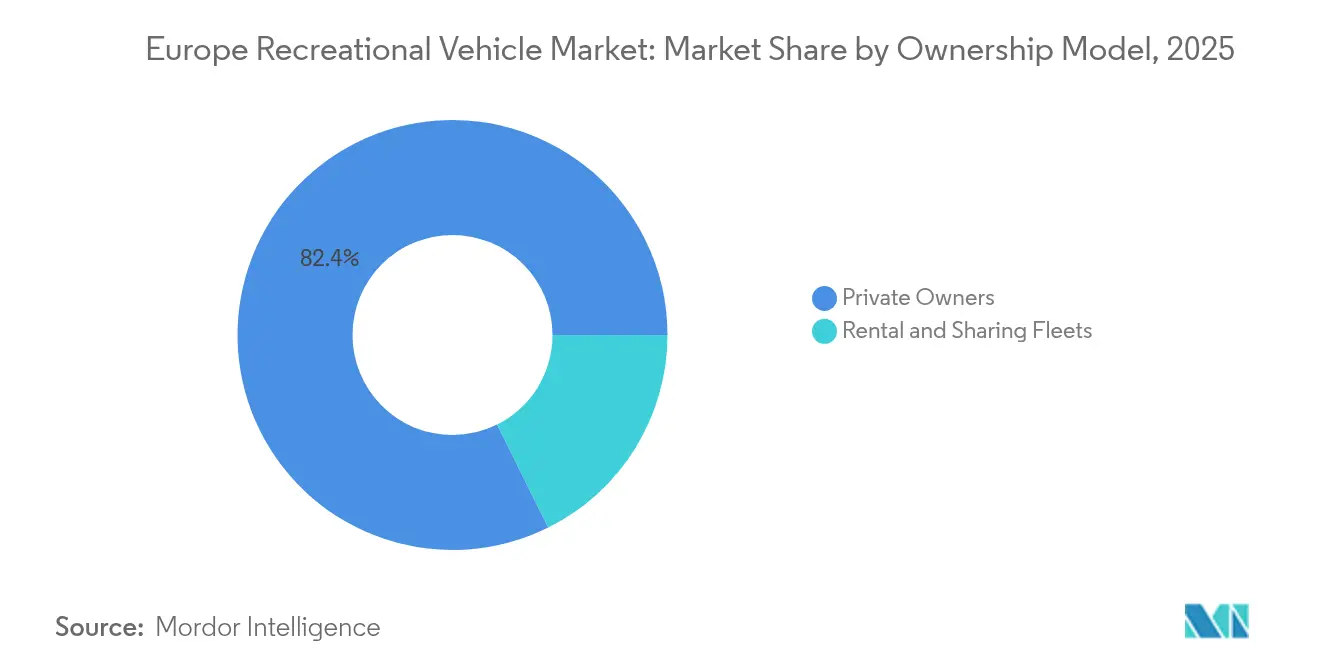

- By ownership model, private owners held 82.35% of the Europe recreational vehicle market size in 2025; rental and sharing fleets represent the fastest trajectory at 13.95% CAGR.

- By sales channel, OEM-franchised dealers accounted for 71.20% of the Europe recreational vehicle market in 2025, yet direct-to-consumer online transactions are set to rise at a 19.05% CAGR.

- By country, Germany captured 27.30% of the Europe recreational vehicle market in 2025, whereas Norway records the highest projected CAGR at 11.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Recreational Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Pandemic Surge in Domestic and Intra-Europe Tourism | +2.8% | Europe-wide, strongest in Germany, France, Scandinavia | Medium term (2–4 years) |

| Rapid Expansion of RV-Sharing and Rental Platforms | +2.1% | Western Europe, expanding into Eastern Europe | Short term (≤ 2 years) |

| Affluent 55–75 Demographic Boosting Premium Demand | +1.9% | Germany, United Kingdom, Netherlands, France | Long term (≥ 4 years) |

| B-License Weight Limit Rising to 4.25 t | +1.7% | EU member states, implementation by 2028 | Medium term (2–4 years) |

| EU B-License Weight Limit Rising to 4.25 t Enabling Larger Floorplans | +1.5% | EU member states | Medium term (2–4 years) |

| “Emergence of Work-From-Anywhere” Digital-Nomad Van Conversions | +1.3% | Europe-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic Surge in Domestic and Intra-Europe Tourism

European camping activity has reached unprecedented levels, with Germany recording 42.9 million camping overnight stays in 2024, representing a 19.9% increase compared to 2019 pre-pandemic levels[1]"New camping record: 42.9 million overnight stays in 2024," Destatis, destatis.de.. This sustained elevation in domestic tourism reflects a fundamental shift in European leisure preferences, where proximity-based travel has evolved from pandemic necessity to preferred lifestyle choice. The trend extends beyond Germany, with Norway's camping sites witnessing a rise in guest nights, marking significant year-over-year growth. The persistence of elevated camping activity well into 2025 suggests this represents structural demand rather than temporary pandemic-driven behavior, particularly as camping accounts for most German guest overnight stays compared to historical levels. This tourism reorientation creates sustained tailwinds for RV demand across vehicle segments, from compact campervans enabling urban-adjacent exploration to larger motorhomes supporting extended domestic touring.

Rapid Expansion of RV-sharing and Rental Platforms

The European RV-sharing ecosystem has matured rapidly. The sector's growth acceleration is evidenced by Roadsurfer securing EUR 30 million from Avellinia Capital in April 2025, specifically for fleet expansion from 8,500 to 10,000 vehicles[2]"Roadsurfer: Munich-based camper travel provider receives 30 million euros for fleet expansion," Starting up, starting-up.de.. This capital deployment reflects institutional recognition that peer-to-peer RV platforms have overcome initial trust barriers and achieved operational scale. Notably, platforms are expanding eastward, with Ruuts targeting Eastern European markets through API integrations, providing access to major European RVs, and addressing previously underserved regions. The sharing economy's penetration into RV ownership patterns creates dual market effects: democratizing access for first-time users while generating utilization-based revenue streams for private owners, effectively expanding the addressable market beyond traditional ownership models.

Ageing but Affluent 55 to 75 Cohort Boosting Premium Demand

The European RV market's premium segment demonstrates remarkable resilience, with manufacturers like Hymer commanding prices from EUR 89,050 for entry-level models to EUR 215,460 for premium Venture S variants. At the same time, Bürstner's Elegance series starts at EUR 161,430[3]"HYMER MOTORHOME RANGES," lowdhams.com. This pricing power reflects sustained demand from Europe's affluent pre-retirement and early retirement demographic, whose purchasing patterns diverge sharply from broader economic pressures affecting younger segments.

The cohort's influence extends beyond unit sales to specification preferences, driving adoption of premium features like Bürstner's iNDUS toilet systems with gray-water reuse technology and Mercedes-Sprinter chassis upgrades. Significantly, this demographic's preference for larger, more sophisticated vehicles aligns with the pending EU B-license expansion to 4.25 tonnes, potentially unlocking additional premium segment growth as regulatory barriers diminish. The segment's stability contrasts with broader market volatility, as evidenced by continued strong performance in luxury categories even as mass-market segments face inventory pressures. Premium manufacturers are capitalizing on enhanced connectivity features, with systems like Bürstner's My Bürstner app providing remote monitoring capabilities that appeal to tech-savvy affluent buyers seeking integrated digital experiences.

EU B-license Weight Limit Rising to 4.25 t Enabling Larger Floorplans

The European Parliament's approval of extending B-license eligibility to 4.25-tonne motorhomes represents a paradigm shift that will fundamentally expand the addressable European RV market by 2028. This regulatory change eliminates a critical barrier that previously required C1 license acquisition for vehicles exceeding 3.5 tons, effectively restricting millions of potential buyers from accessing larger motorhome segments. The impact extends beyond mere weight allowances to enable entirely new vehicle architectures, as manufacturers can now design motorhomes with enhanced living space, larger fresh water tanks, and more comprehensive amenities without forcing customers into commercial licensing categories. Early manufacturer response is evident in new model development, with brands like Dethleffs introducing 4x4 Performance models and enhanced off-road capabilities that leverage the expanded weight envelope. The regulatory alignment across EU member states creates unprecedented market standardization, eliminating the patchwork of national licensing requirements that previously complicated cross-border RV travel. Importantly, the change applies regardless of propulsion type for motorhomes, providing regulatory support for electric RV adoption by accommodating the additional battery weight without licensing penalties. This regulatory modernization positions Europe ahead of other global markets in RV accessibility, potentially accelerating market penetration rates as the expanded licensing framework takes effect.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Purchase and Insurance Costs | –1.9% | Europe-wide, most acute in premium segments | Short term (≤ 2 years) |

| Volatile Interest-Rate-Driven Financing Squeeze | –1.7% | Europe-wide, particularly affecting dealer financing | Short term (≤ 2 years) |

| Oversupply-Led Price Depreciation of 2021–22 Inventory | –1.6% | Germany, France, Italy, Spain | Medium term (2–4 years) |

| Urban Low-Emission Zones Curbing Diesel RV Access | –1.2% | Major metropolitan areas across Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Purchase and Insurance Costs

European RV prices have surged, straining affordability across market segments. This increase stems from supply chain disruptions, chassis shortages, and manufacturers leveraging pandemic-driven demand. Rising insurance premiums, driven by higher replacement values and specialized repair needs, add to the financial burden. Middle-market buyers increasingly opt for used vehicles or rentals, while younger and first-time buyers face barriers, limiting market growth despite strong demand. Even with inventory corrections, persistent high prices highlight structural cost inflation, necessitating income growth or alternative ownership models to sustain accessibility.

Volatile Interest-rate-driven Financing Squeeze

As interest rate fluctuations strain consumer affordability and dealer inventory management, European RV financing faces challenges. Dealers struggle with elevated inventory levels requiring higher working capital at increased borrowing costs, leading to cases like Klinke Caravaning's bankruptcy amid "more cautious buyers" and cooling post-pandemic demand. Financing issues also impact manufacturer-dealer relationships, as higher floor plan costs tighten dealer cash flows and slow inventory turnover.

Major manufacturers, such as Erwin Hymer Group, note that rising interest rates and high inventories create "heavy financing burdens," prompting aggressive discounting. Premium segments face added pressure, with larger loans amplifying interest rate impacts, potentially shifting demand to smaller units or delaying purchases. This credit tightening coincides with efforts to stabilize inventory levels post-pandemic, intensifying supply and demand-side constraints on market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Motorhomes Lead Despite Campervan Surge

Motorhomes maintained their dominant position with a 53.72% share of the Europe recreational vehicle market in 2025, reflecting European consumers' preference for self-contained mobile living solutions that provide comprehensive amenities without external dependencies. The segment's leadership stems from its appeal to the affluent 55-75 demographic, prioritizing comfort and convenience over mobility constraints. However, campervans are experiencing the fastest growth at 11.62% CAGR through 2031, driven by younger demographics embracing van life culture and urban professionals seeking flexible work-travel solutions. Travel and fifth-wheel trailers occupy smaller but stable niches, appealing to consumers who prefer to maintain separate towing vehicles for daily use. Pop-up and folding campers represent the entry-level segment, attracting price-sensitive buyers and seasonal users.

The regulatory environment supports this segmentation evolution, with EU type-approval frameworks under Regulation 2018/858 providing clear pathways for multi-stage vehicle approvals that facilitate campervan conversions while maintaining safety standards. Class A motorhomes command premium pricing but face headwinds from urban low-emission zone restrictions, while Class B campervans benefit from improved urban accessibility and parking flexibility.

By Propulsion and Fuel: Electric Transition Accelerates Despite Diesel Dominance

Diesel ICE powertrains command 91.10% share of the Europe recreational vehicle market in 2025, reflecting the segment's traditional reliance on diesel's superior torque characteristics and fuel efficiency for heavy vehicle applications. Petrol ICE variants maintain a smaller presence, primarily in lighter campervan applications where weight considerations favor gasoline engines. However, battery-electric variants are surging at a 36.91% CAGR through 2031, driven by tightening EU emission regulations and expanding charging infrastructure. Hybrid-electric solutions occupy a transitional position, offering compromise solutions for range-anxious consumers while providing emission benefits for urban access.

Norway leads electric adoption with 96% BEV share in passenger cars, creating spillover effects into commercial and recreational vehicle segments. Manufacturers are investing heavily in electric solutions, with Truma appointing Dr. Joachim Weckwerth from Bosch's Electric Solutions division to lead product development, signaling a strategic commitment to electrification.

By Ownership Model: Sharing Economy Disrupts Traditional Patterns

Private owners account for 82.35% share of the Europe recreational vehicle market in 2025, maintaining dominance through traditional ownership patterns that emphasize personal customization and unrestricted usage flexibility. This segment benefits from emotional attachment factors and the desire for immediate availability that characterizes recreational vehicle ownership psychology. However, rental and sharing fleets are expanding rapidly at a 13.95% CAGR through 2031, fundamentally altering market dynamics through asset utilization optimization and access democratization. The sharing economy's penetration reflects changing consumer preferences toward experience-based consumption rather than asset accumulation, particularly among younger demographics.

Comprehensive insurance frameworks support the ownership model evolution, with platforms offering coverage up to EUR 2 million per rental and 24/7 breakdown assistance, addressing traditional barriers to peer-to-peer sharing. Significantly, the sharing economy's growth creates network effects that benefit the broader market by introducing new users to RV experiences, many subsequently transition to ownership, effectively expanding the total addressable market beyond traditional ownership-only models.

By Sales Channel: Digital Transformation Reshapes Distribution

OEM-franchised dealers maintained a 71.20% share of the Europe recreational vehicle market in 2025, leveraging established relationships, service capabilities, and financing partnerships crucial for high-consideration purchases requiring extensive customer education. Traditional dealers provide essential functions, including trade-in processing, warranty service, and local market presence that digital channels cannot easily replicate. However, direct-to-consumer online sales are accelerating at a 19.05% CAGR through 2031, driven by digital-native consumers' preference for transparent pricing and streamlined purchasing processes. Rental agency networks occupy a growing niche, serving as sales channels and customer acquisition funnels for eventual ownership transitions.

Digital channels particularly benefit from regulatory compliance frameworks under EU Regulation 2018/858, which mandates electronic certificates of conformity and standardized data exchange systems that facilitate online transactions. The channel disruption is most pronounced in campervan segments, where younger buyers demonstrate higher digital adoption rates and reduced reliance on traditional dealer services. Established dealers respond through omnichannel strategies, combining physical showrooms with digital configurators and online financing tools to capture evolving customer preferences while maintaining service differentiation advantages.

Geography Analysis

Germany dominates the Europe recreational vehicle market with a 27.30% share in 2025, supported by the continent's most extensive camping infrastructure and strongest manufacturing base. The country's leadership reflects a deep cultural affinity for outdoor recreation, evidenced by a record-breaking camping overnight stays in 2024. The United Kingdom and France maintain significant positions despite Brexit-related complications and varying regulatory frameworks, with France benefiting from extensive campsite networks and the United Kingdom leveraging strong caravan traditions. Italy and Spain contribute meaningfully through domestic demand and manufacturing capabilities, with Italy introducing new ATECO classifications in 2025 to distinguish between traditional campsites and RV-specific areas.

Norway emerges as the fastest-growing market at 11.92% CAGR through 2031, driven by exceptional economic conditions and cultural preferences for outdoor recreation. The Netherlands demonstrates consistent performance through a compact geography that favors RV tourism and strong purchasing power supporting premium segments. Rest of Europe, including Eastern European markets, presents emerging opportunities as infrastructure development and income growth support market expansion, with platforms like Ruuts specifically targeting these underserved regions through API integrations, providing access to thousands of European RVs. The geographic distribution reflects varying regulatory environments, with EU harmonization under frameworks like Regulation 2018/858 facilitating cross-border trade while national differences in licensing, taxation, and infrastructure continue to influence regional market dynamics.

Competitive Landscape

The European RV market exhibits high concentration with five leading manufacturers controlling the majority of motorhome and caravan sales, creating significant barriers to entry while enabling sustained pricing power. This oligopolistic structure reflects substantial capital requirements for manufacturing scale, dealer network development, and regulatory compliance under EU-type approval frameworks. Strategic patterns emphasize vertical integration, broad distribution networks, and acquisition-driven growth, with companies like Trigano pursuing serial acquisitions of distressed assets to expand market share and manufacturing capabilities.

Technology adoption focuses on connectivity solutions, sustainability features, and manufacturing efficiency improvements rather than fundamental product disruption. Companies are investing in digital integration, exemplified by Bürstner's My Bürstner app providing remote monitoring capabilities and Truma's appointment of former Bosch Electric Solutions leadership to drive electrification initiatives. White-space opportunities exist in electric powertrains, where current offerings remain limited by range and pricing constraints, and in Eastern European markets where established players maintain minimal presence. Emerging disruptors primarily operate in adjacent segments, particularly peer-to-peer rental platforms like Yescapa and Roadsurf, which create alternative value propositions without directly competing in manufacturing. The competitive environment is intensifying due to current inventory corrections and financing pressures, with major players like Erwin Hymer Group potentially accelerating consolidation among smaller manufacturers unable to weather the downturn.

Europe Recreational Vehicle Industry Leaders

-

Thor Industries Inc.

-

Dethleffs GmbH & Co. KG

-

Swift Group Ltd.

-

Knaus Tabbert AG

-

Auto Trail VR LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Renault and German motorhome manufacturer Ahorn Camp introduced a new range of motorhomes and campervans based on the fourth-generation Renault Master. This marks the first exclusive use of the platform by a motorhome brand. The vehicles, produced by Erwin Hymer Group, will be sold through Ahorn Camp branches and Renault's Europe-wide Pro+ dealer network.

- March 2025: Schmitz Cargobull acquired a 48% stake in Polish trailer manufacturer GT Trailers to integrate its superstructure expertise and enhance its market share in high-volume trailer combinations.

Europe Recreational Vehicle Market Report Scope

A recreational vehicle, also known as an RV, is a motor vehicle or trailer with living quarters designed for accommodation. Motorhomes, campervans, coaches, caravans (also known as travel trailers and camper trailers), fifth-wheel trailers, popup campers, and truck campers are examples of RVs.

The European recreational vehicle market is segmented by type and by country. By type, the market is segmented into towable RVs and motorhomes. By country, the market is segmented into Germany, United Kingdom, Italy, France, Netherlands, Spain, Norway, and the Rest of Europe. The report offers the market size in value (USD) and forecasts for all the above segments.

By Type

| Towable RVs | Travel Trailers |

| Fifth-Wheel Trailers | |

| Pop-up/Folding Campers | |

| Motorhomes | Class A |

| Class B (Campervans) | |

| Class C |

By Propulsion and Fuel

| Diesel Internal Combustion Engine |

| Petrol Internal Combustion Engine |

| Hybrid-Electric |

| Battery-Electric |

By Ownership Model

| Private Owners |

| Rental and Sharing Fleets |

By Sales Channel

| OEM-Franchised Dealers |

| Direct-to-Consumer Online |

| Rental Agency Networks |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Norway |

| Rest of Europe |

| By Type | Towable RVs | Travel Trailers |

| Fifth-Wheel Trailers | ||

| Pop-up/Folding Campers | ||

| Motorhomes | Class A | |

| Class B (Campervans) | ||

| Class C | ||

| By Propulsion and Fuel | Diesel Internal Combustion Engine | |

| Petrol Internal Combustion Engine | ||

| Hybrid-Electric | ||

| Battery-Electric | ||

| By Ownership Model | Private Owners | |

| Rental and Sharing Fleets | ||

| By Sales Channel | OEM-Franchised Dealers | |

| Direct-to-Consumer Online | ||

| Rental Agency Networks | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Norway | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe recreational vehicle market by 2031?

The Europe recreational vehicle market is forecast to reach USD 62.69 billion by 2031.

Which vehicle type currently dominates sales?

Motorhomes account for 53.72% of 2025 unit sales, the largest share.

Which country is growing the fastest?

Norway shows the highest growth, with a 11.92% CAGR expected through 2031.

How is electrification affecting product strategies?

Battery-electric RVs, though still niche, are expanding at a 36.91% CAGR, prompting manufacturers to invest heavily in electric HVAC and drivetrain systems.

What regulatory change will most impact demand?

Extending B-license eligibility to 4.25 t motorhomes by 2028 removes a major entry barrier for heavier, amenity-rich models.

Are peer-to-peer rental platforms significant?

Yes, platforms like Yescapa and roadsurfer are growing fleets rapidly, accelerating a significant growth in rental and sharing segments.

Page last updated on: