Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

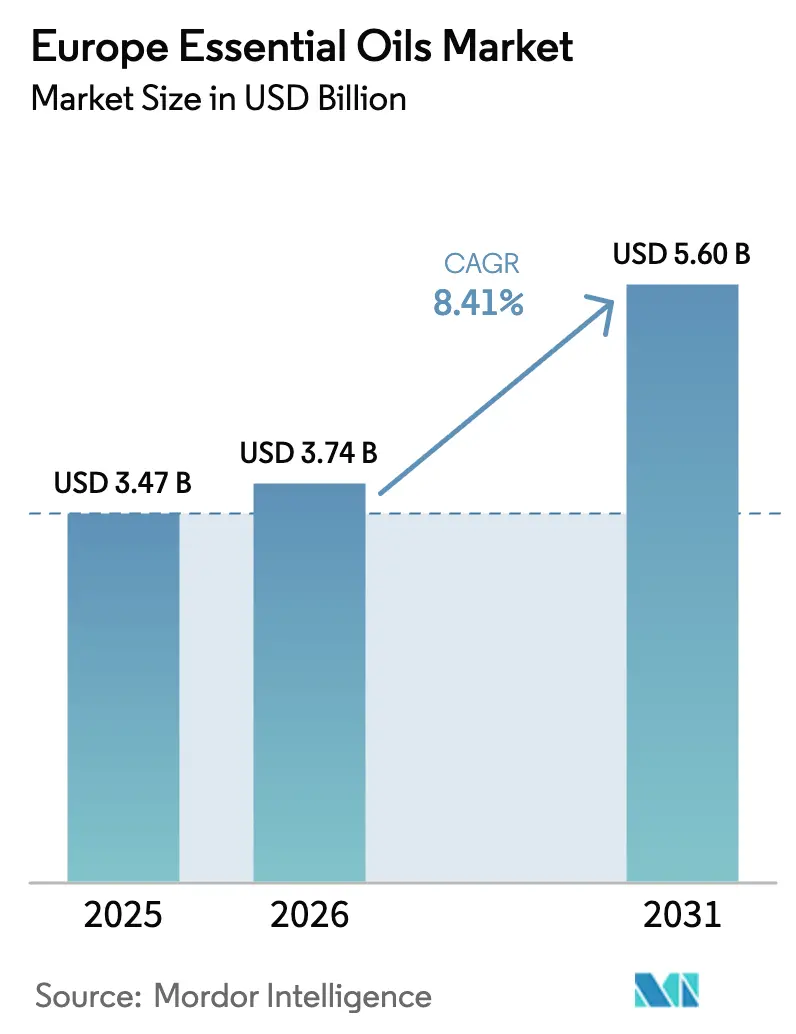

| Base Year Market Size (2025) | USD 3.47 Billion |

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 5.60 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

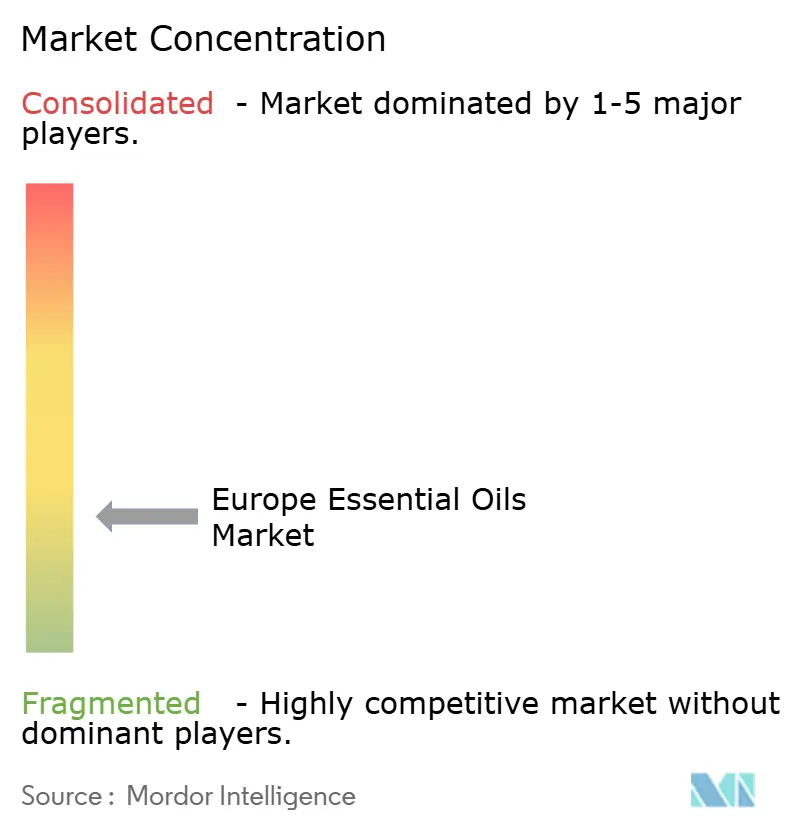

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Essential Oils Market Analysis by Mordor Intelligence

The Europe essential oils market size is expected to grow from USD 3.47 billion in 2025 to USD 3.74 billion in 2026 and is forecast to reach USD 5.60 billion by 2031 at 8.41% CAGR over 2026-2031. This growth is primarily driven by strong demand across industries such as food, cosmetics, pharmaceuticals, and aromatherapy. However, supply shortages caused by droughts in France and pest damage in Provence have increased dependence on imports. Citrus-based oils continue to lead volume growth as they meet clean-label requirements in beverages and household cleaning products, while floral absolutes play a key role in enhancing premium offerings in fine fragrances and high-end skincare products. Market consolidation is becoming evident as companies like DSM-Firmenich, Symrise, Givaudan, and International Flavors & Fragrances (IFF) invest in analytical laboratories and supercritical extraction technologies to ensure access to compliant raw materials. On the other hand, artisanal distillers rely on terroir narratives and organic certifications to maintain competitive pricing. Regulatory developments, including the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH), the Cosmetics Regulation, and the 2023/1545 allergen update, have increased testing costs. This has provided an advantage to fully integrated ingredient suppliers with in-house toxicology expertise and regulatory dossier capabilities. The market is further supported by a strong wellness culture, the growing popularity of spa therapies, and increasing consumer awareness of synthetic additives. These factors collectively drive demand for the natural solutions offered by essential oils, helping to cushion the market against short-term macroeconomic challenges.

Key Report Takeaways

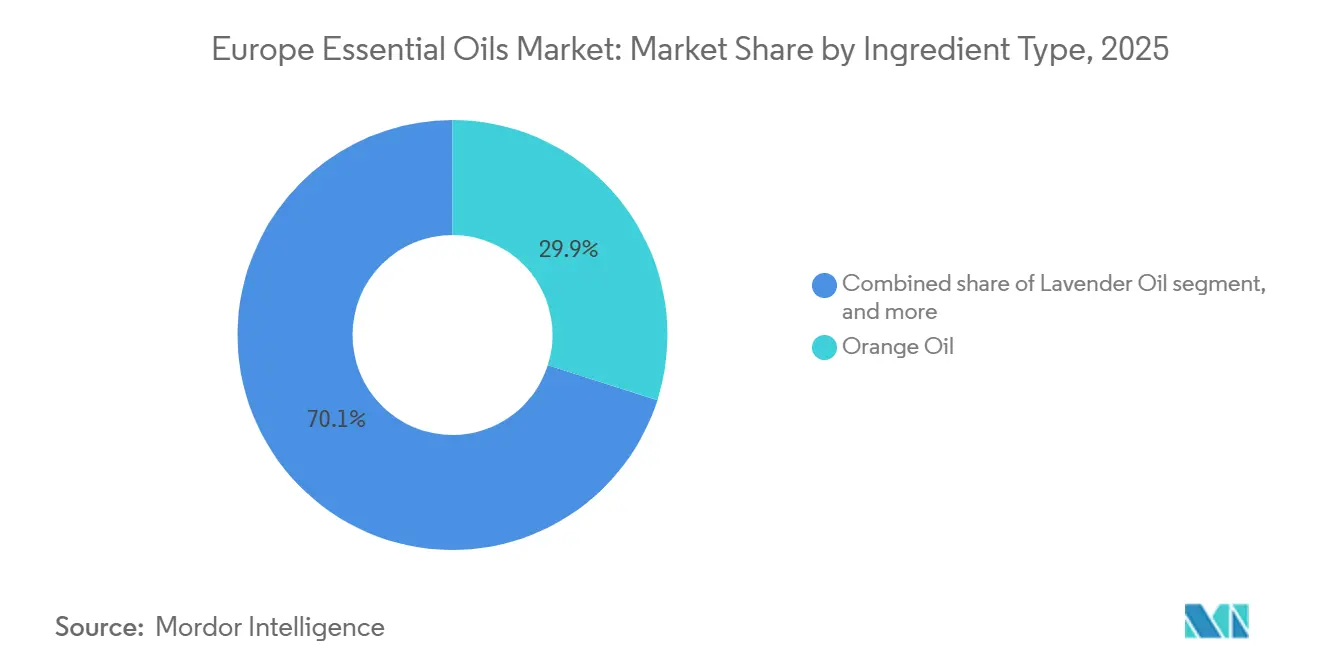

- By ingredient type, orange oil accounted for 29.90% of the Europe essential oil market share in 2025. Geranium oil is projected to grow at a CAGR of 8.72% between 2026 and 2031, representing the fastest growth rate among ingredient types.

- By source, flower-derived oils held a 35.82% share of the Europe essential oil market size in 2025. These oils are expected to grow at a CAGR of 8.94% through 2031, surpassing the growth of all other sources.

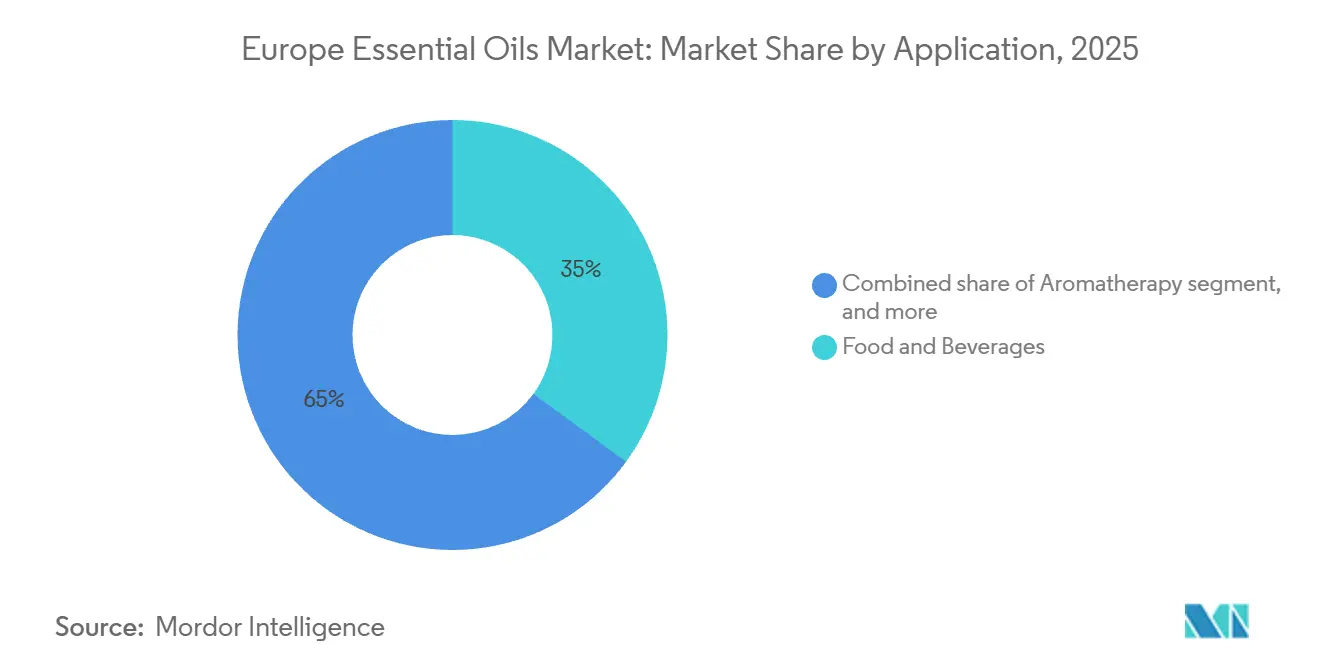

- By application, the food and beverage segment captured a 35.03% revenue share in 2025. This segment is anticipated to grow at a CAGR of 8.45% over the period 2026 to 2031.

- By geography, France accounted for 22.59% of the regional revenue in 2025. Spain is projected to achieve the fastest growth, with a CAGR of 9.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Essential Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and organic ingredients in various industries | +1.8% | Global, with strongest uptake in Germany, France, Netherlands | Medium term (2-4 years) |

| Expansion of spa and wellness centers using essential oil-based therapies | +1.2% | France, Germany, Spain, Italy; Nordic countries for eucalyptus-sauna treatments | Medium term (2-4 years) |

| Shift toward clean-label formulations with plant-derived oils | +1.5% | European Union-wide, particularly United Kingdom, Germany, France, Netherlands | Short term (≤ 2 years) |

| Increased use of essential oils in premium personal care and cosmetics | +1.3% | France, Italy, Germany; luxury-goods hubs | Medium term (2-4 years) |

| Rising health consciousness boosting demand for natural relief products | +1.1% | Germany, Netherlands, United Kingdom; Nordic countries | Short term (≤ 2 years) |

| Growth of organic farming and sustainable sourcing for aromatic crops | +0.9% | France (Provence), Spain (Valencia), Italy (Calabria, Sicily) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and organic ingredients in various industries

Consumer demand for transparency and simpler ingredients is encouraging formulators to replace synthetic additives with botanically derived alternatives. This trend has been further amplified by social media scrutiny of product labels. Organic-certified essential oils now account for approximately 32% of lavandin acreage and 25% of lavender acreage in France, which is significantly higher than the national average of 11% for all crops [1]Source: Chambres d’agriculture France, “Lavender and lavandin production in France,” chambres-agriculture.fr. This demonstrates that growers of aromatic crops are responding to premium pricing opportunities. Beyond cosmetics, this shift is also evident in the food and beverage industry, where natural flavorings derived from citrus, mint, and spice oils are increasingly replacing artificial compounds due to retailer requirements and clean-label certification programs. The European Union's organic production framework, governed by Regulation 2018/848, enforces traceability and restricts synthetic inputs. This creates both barriers to entry and a competitive advantage for certified suppliers. Compliance with ECOCERT (Ecological and Organic Certification) and USDA (United States Department of Agriculture) Organic standards has become essential for accessing premium distribution channels. However, smaller distillers face challenges such as high audit costs and extensive documentation requirements, which has led to a concentration of organic supply among mid-sized cooperatives and vertically integrated flavor producers.

Expansion of spa and wellness centers using essential oil-based therapies

Aromatherapy has evolved from a niche wellness offering to a mainstream feature in the hospitality industry, with European spa operators increasingly integrating essential oils into their signature treatments to enhance guest experiences and justify higher session pricing. Popular oils such as lavender, eucalyptus, and ylang-ylang are widely used, with lavender favored in French and Mediterranean spas for its calming effects, while eucalyptus is commonly utilized in Nordic saunas and hammams (Turkish baths) for its respiratory benefits. The professionalization of aromatherapy training and the expansion of certification programs have reduced liability concerns, enabling spa chains to broaden their essential oil offerings without significant increases in insurance costs. Germany and France, as leaders in spa density and per-capita wellness spending, create concentrated demand hubs that source supplies from Provence lavender estates and Moroccan eucalyptus distillers. This channel also facilitates brand-building, as spa guests frequently purchase retail-sized essential oil bottles for home use, benefiting direct-to-consumer brands and artisanal distillers with engaging brand narratives. Supporting this trend, data from the United Kingdom Spa Association (UKSA) reported a 60% increase in daily spa visits in 2024, reflecting strong consumer interest in physical and emotional well-being [3]Source: The UK Spa Association (UKSA), “State of the Spa Industry Snapshot Survey,” spa-uk.org.

Shift toward clean-label formulations with plant-derived oils

Regulatory developments and retailer mandates are coming together to drive the shift from synthetic flavorings and fragrances to plant-derived alternatives, creating opportunities for essential oil suppliers with strong traceability systems. The European Union's Flavouring Regulation 1334/2008 [2]Source: European Commission, “EU Rules – flavourings,” food.ec.europa.eu, which governs the use of flavorings in food, requires natural flavorings to be derived exclusively from plant, animal, or microbial sources. This regulation provides a competitive advantage for essential oils, as synthetic manufacturers must reformulate to comply. Major food and beverage companies are updating their legacy products to meet clean-label standards, with citrus oils such as orange, lemon, and bergamot replacing artificial citrus flavors in carbonated soft drinks, confectionery, and baked goods. This trend is gaining momentum in countries like the United Kingdom, Germany, and the Netherlands, where retailer private-label programs enforce strict ingredient exclusion lists that prohibit artificial flavorings. The compliance requirements are encouraging smaller formulators to outsource flavor development to specialized firms, which is consolidating purchasing power among a few large buyers. As a result, price competition for commodity oils like orange and lemon has intensified, while niche oils such as geranium and clary sage continue to maintain stable premiums.

Increased use of essential oils in premium personal care and cosmetics

Luxury cosmetics brands are increasingly using essential oils as primary ingredients to justify premium pricing and stand out from mass-market competitors that depend on synthetic fragrances and preservatives. France's Grasse perfumery cluster, which has traditionally specialized in fine fragrances, is now expanding into functional personal-care ingredients. This includes supplying rose, jasmine, and neroli absolutes for anti-aging serums and facial oils that are marketed at price points exceeding EUR 100 per 30 milliliters. In Italy, the natural cosmetics industry, led by brands emphasizing Mediterranean botanicals, has driven demand for bergamot and lemon oils sourced from Calabria and Sicily. These regions benefit from protected geographical indications (IGP), which support premium positioning in the market. The European Cosmetics Regulation 1223/2009 requires safety assessments and allergen labeling but does not impose limits on essential oil concentrations. This allows formulators to use higher levels of essential oils in leave-on products compared to synthetic fragrances. This regulatory difference is creating opportunities for essential oil suppliers to replace synthetic musks and aldehydes. However, ongoing reviews by the Scientific Committee on Consumer Safety (SCCS) regarding allergenic constituents may reduce this flexibility in future regulatory updates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European Union regulatory frameworks increase compliance burden for essential oils | -0.7% | European Union-wide, particularly affecting small-batch producers in France, Italy, Spain | Short term (≤ 2 years) |

| Restrictions on allergenic constituents such as limonene and linalool limit product formulation | -0.5% | European Union-wide, with highest impact in Germany, France, Netherlands | Medium term (2-4 years) |

| Safety concerns regarding dermal irritation and sensitization from undiluted or improperly used oils reduce adoption among risk-averse consumers | -0.3% | Germany, Netherlands, United Kingdom; Nordic countries with high consumer-protection awareness | Short term (≤ 2 years) |

| Issues of adulteration, dilution, and mislabeling harm brand credibility and complicate efforts to establish long-term consumer trust | -0.4% | Global, with particular impact on direct-to-consumer brands in United Kingdom, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent European Union regulatory frameworks increase compliance burden for essential oils

The European Union's regulatory framework, which includes the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH), Classification, Labelling and Packaging (CLP), Cosmetics Regulation 1223/2009, and the Nagoya Protocol on Access and Benefit Sharing, imposes extensive documentation, testing, and labeling requirements. These regulations place a significant burden on small distillers and artisanal producers. For instance, Commission Regulation 2023/1545 has expanded the list of fragrance allergens requiring mandatory labeling from 26 to over 86 substances. This change has forced the reformulation of existing products and increased analytical costs for batch testing. Additionally, REACH registration fees and dossier preparation costs can exceed EUR 50,000 per substance for mid-volume chemicals. Many single-estate distillers are unable to absorb these costs, leading them to exit direct sales and instead supply larger aggregators that can distribute compliance costs across broader portfolios. Furthermore, the Scientific Committee on Consumer Safety's ongoing reviews of terpene peroxides and other oxidation products have created regulatory uncertainty. Some buyers are preemptively delisting oils while awaiting final rulings. This situation benefits vertically integrated flavor-and-fragrance companies with in-house regulatory affairs teams, while independent distillers, lacking the necessary scale, face significant challenges in adapting to the evolving compliance landscape.

Restrictions on allergenic constituents such as limonene and linalool limit product formulation

Limonene and linalool, which are commonly found in citrus and lavender oils respectively, are classified as fragrance allergens under European Union (EU) cosmetics regulations. These regulations require their declaration on product labels when their concentrations exceed 0.001% in leave-on products and 0.01% in rinse-off formulations. This requirement has led some mass-market brands to reduce essential oil concentrations or switch to synthetic alternatives that provide fragrance without exceeding allergen thresholds. Consequently, demand for commodity citrus and lavender oils has declined in price-sensitive market segments. Additionally, the potential for peroxide formation in terpene-rich oils during storage presents further challenges for formulation. For example, oxidized limonene has higher sensitization rates compared to fresh oil. To address this issue, manufacturers have implemented measures such as nitrogen blanketing, refrigerated storage, and accelerated stability testing. Furthermore, guidance from Germany's Federal Institute for Risk Assessment and France's National Agency for the Safety of Medicines and Health Products (ANSM) recommends maximum usage levels for certain oils in cosmetics, effectively creating limits that restrict formulators' flexibility. While these restrictions are less stringent in the fine fragrance market, where higher concentrations of essential oils are traditional and consumers are generally more accepting of allergen exposure, they significantly impact growth potential in the mass-market personal care segment, which represents the largest volume opportunity for essential oil suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Citrus Dominance Meets Floral Premiumization

Orange oil is anticipated to account for a 29.90% market share in 2025, supported by its well-established applications in food flavoring, household cleaning, and aromatherapy. Cold-pressed Valencia and Brazilian oils are commonly used due to their cost efficiency and availability, often preferred over regional-specific characteristics. Geranium oil is expected to grow at a compound annual growth rate (CAGR) of 8.72% through 2031, driven by its increasing use by perfumers as a cost-effective substitute for Bulgarian rose otto. Egyptian and South African geranium oils are becoming more prominent in natural perfumery and premium skincare products.

Lavender oil, despite its strong association with Provence, is facing challenges in maintaining margins due to oversupply and competition from Bulgarian producers. French lavender production decreased by 30% in 2023, primarily due to pest infestations and drought conditions. Peppermint and spearmint oils are witnessing growing demand in pharmaceutical applications, particularly in Germany's Apotheke (pharmacy) channel, where menthol-based topical analgesics and digestive aids are sold at premium prices. Eucalyptus oil continues to be a key ingredient in Nordic spa treatments and over-the-counter (OTC) respiratory remedies, with Australian and Portuguese sources dominating the supply chain.

By Source: Flower-Derived Oils Command Premium Positioning

Flowers accounted for 35.82% of source-based volume in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 8.94% through 2031. This growth is driven by the increasing demand for lavender, rose, jasmine, and geranium in fine fragrances and natural cosmetics. The Appellation d'Origine Protégée for Huile essentielle de lavande de Haute-Provence, which spans 284 communes across Alpes-de-Haute-Provence, Hautes-Alpes, Drôme, and Vaucluse, demonstrates how geographic protection can help sustain premium pricing even in the face of yield fluctuations.

Leaf-derived oils, such as eucalyptus, peppermint, and tea tree, are widely used in pharmaceuticals and aromatherapy. These oils are characterized by lower per-kilogram pricing but higher volume throughput. Bark sources, primarily cinnamon and cassia, encounter supply challenges due to the slow growth of trees and labor-intensive harvesting processes, which limit their overall contribution to market growth. Root-derived oils, including vetiver and ginger, cater to smaller niches in perfumery and natural medicine, with Madagascar and India being the primary production regions.

By Application: Food and Beverage Anchors Volume Growth

Food and beverage applications held a 35.03% market share in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 8.45%. This growth is driven by clean-label requirements and the replacement of synthetic flavorings in accordance with European Union (EU) Regulation 1334/2008. Citrus oils dominate this segment, with orange, lemon, and bergamot oils widely used as natural flavorings in carbonated soft drinks, confectionery, baked goods, and dairy products. The Generally Recognized As Safe (GRAS) status granted by the Flavor and Extract Manufacturers Association (FEMA) for many essential oils supports regulatory approval in food applications, although maximum usage levels vary depending on the oil and product category.

Aromatherapy applications, while smaller in volume, command higher per-kilogram prices due to the emphasis on purity and organic certification. Lavender, eucalyptus, and peppermint oils are key products anchoring retail assortments in this category. Pharmaceutical applications are also expanding in Germany and the Netherlands, where natural medicine is widely accepted, and regulatory frameworks are in place to support the use of essential-oil-based over-the-counter (OTC) remedies.

Geography Analysis

In 2025, France accounted for 22.59% of geographic revenue, driven by Provence's lavender heritage, Grasse's established perfumery cluster, and strong domestic demand for aromatherapy products. Germany, the United Kingdom, and Italy represent mature markets with high per-capita consumption. Growth in these markets is primarily tied to premiumization and the increasing use of natural cosmetics and pharmaceutical applications. The Netherlands plays a key role as a re-export hub, with Rotterdam port managing significant inbound volumes from developing countries, which are then distributed across the European Union (EU). France's lavender sector, however, faces structural challenges, with production declining by 30% in 2023 compared to 2022 due to pest issues and oversupply, resulting in an estimated two years of unsold inventory. Italy's bergamot production in Calabria, which supplies approximately 90% of global output, remains a critical asset for the fine fragrance industry, though climate variability and aging orchards pose risks to long-term supply stability.

Spain is projected to achieve the fastest growth, with a compound annual growth rate (CAGR) of 9.51% through 2031. This growth is fueled by Valencia's expanding organic citrus acreage and increasing export demand. Regional trade data highlights that essential oil exports from Cantabria rose by 41.5% year-over-year in early 2025. Spain's citrus sector is also investing in organic certification and modern distillation infrastructure, positioning the country to capture a larger share of the market as demand for natural flavorings continues to grow.

Poland, Belgium, and Sweden are emerging markets where rising disposable incomes and growing awareness of natural wellness are driving category growth, although volumes remain modest compared to Western Europe. The Rest of Europe category, which includes Eastern European and Balkan countries, is expanding as multinational retailers introduce natural product assortments and local distillers upgrade operations to meet EU quality standards. While these markets are still developing, they show significant potential for future growth.

Competitive Landscape

The European essential oil market is moderately fragmented, with a concentration score of 4 out of 10. This indicates the presence of global flavor-and-fragrance conglomerates, mid-sized ingredient suppliers, and artisanal distillers. In May 2022, DSM (Dutch State Mines) and Firmenich merged to form a combined entity with EUR 11.6 billion in annual revenue and EUR 2.0 billion in Perfumery and Beauty sales. This merger has strengthened their purchasing power and vertical integration, enabling the deployment of supercritical fluid extraction plants in India and the expansion of natural ingredient capacity. Similarly, companies such as Symrise, Givaudan, and International Flavors & Fragrances (IFF) utilize their scale to manage compliance costs, invest in research and development, and establish long-term supply contracts with growers, creating significant barriers for smaller competitors.

Strategic trends in the market emphasize vertical integration, with leading firms acquiring upstream distillation assets and downstream formulation capabilities to maximize margins across the value chain. Opportunities are emerging in blockchain-enabled traceability, as consumer demand for transparency surpasses the current capabilities of supply chains. Additionally, underutilized botanicals like clary sage and helichrysum offer potential for premium pricing due to their limited supply and niche market positioning.

Emerging disruptors in the market include direct-to-consumer brands that leverage social media platforms and subscription models to bypass traditional retail channels. However, their growth is constrained by concerns over product adulteration and the significant capital investment required to establish in-house testing laboratories. Technology adoption varies across the market, with larger players employing advanced tools such as gas chromatography-mass spectrometry, isotope-ratio analysis, and blockchain pilots. In contrast, smaller distillers rely on organoleptic testing and third-party certifications like ECOCERT and USDA Organic. ISO (International Organization for Standardization) standards for essential oils, including ISO 9235 and oil-specific monographs, provide compositional benchmarks but remain voluntary, limiting their effectiveness in addressing adulteration concerns. The competitive landscape is divided into a premium tier, where factors like terroir, organic certification, and protected designations of origin command higher prices, and a commodity tier, where price and availability dominate, with synthetic substitutes putting downward pressure on margins.

Europe Essential Oils Industry Leaders

Givaudan S.A.

Symrise AG

DSM-Firmenich AG

International Flavors & Fragrances, Inc.

Robertet Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Young Living, a company specializing in essential oils and wellness products, launched its sister company Wyld Notes. The new company introduced a collection of five natural fine fragrances that are 100% natural, luxurious, and formulated with transparent ingredients.

- July 2024: Aluxury has expanded its essential oil collection with new 100% pure essential oils. The range includes Sandalwood, Vanilla Oil, Bergamot, Lavender, and Jasmine oils, which are recognized for their wellness properties and quality.

- January 2024: VOYA expanded its product line with three new essential oil scents: Lift, Rest, and Zest. The company develops environments, products, and treatments that enhance physical and mental wellness.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the European essential oils market as the value of all plant-derived volatile oils sold for food, beverage, beauty, pharmaceutical, home-care, and wellness uses, regardless of distribution channel, and priced at the first commercial sale within Europe. The definition follows ISO 9235 guidance and includes citrus, herb, floral, wood, bark, root, and seed oils distilled, cold-pressed, or CO2-extracted in or imported into the region.

Scope exclusion: oils sold strictly as industrial solvents or feedstocks for synthetic aroma chemicals are outside the present scope.

Segmentation Overview

- By Ingredient Type

- Lavender Oil

- Orange Oil

- Eucalyptus Oil

- Peppermint Oil

- Spearmint Oil

- Lemon Oil

- Rosemary Oil

- Geranium Oil

- Tea Tree Oil

- Other Oils

- By Source

- Flowers

- Leaves

- Bark

- Roots

- Others

- By Application

- Food and Beverage

- Aromatherapy

- Pharmaceuticals

- Cosmetics and Personal Care

- Others

- By Geography

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed European distillers, flavor-house formulators, aromatherapists, and specialty ingredient buyers across Germany, France, Spain, the UK, and Poland. These dialogues validated yield assumptions, typical contract prices, and emerging regulatory pain points, and they supplied fresh insight on substitution trends toward synthetic identicals that are rarely captured in secondary material.

Desk Research

We began with publicly available datasets such as Eurostat PRODCOM series 20.53, UN Comtrade import-export codes HS 3301, the European Federation of Essential Oils position papers, CBI trade briefs on cosmetic ingredients, and health-claim registers maintained by the European Commission. Company filings, press releases, and investor decks helped us track capacity additions and average selling prices. To corroborate trade flows and country share, we accessed Statista production panels as well as the D&B Hoovers financials for leading extractors. A variety of peer-reviewed journals on distillation yields and pharmacopoeia updates completed the picture. The sources listed are illustrative; many other references fed our desk analysis.

A second sweep focused on demand indicators, Euromonitor retail sales for natural cosmetics, Eurostat spa visitation numbers, and customs data on orange peels and lavender tops, which grounded the consumption side of the model.

Market-Sizing & Forecasting

A top-down construct starts with production plus net imports, adjusted for inventory churn to derive apparent consumption, which is then split by application using trade-code proxies and retail panel data. Select bottom-up checks, supplier revenue roll-ups and sampled wholesale ASP x volume, help us fine-tune totals and flag anomalies.

Core variables in the forecast include orange-oil feedstock availability, lavender acreage, spa and wellness visit growth, natural cosmetics retail turnover, and EU flavoring approvals. Multivariate regression links these drivers to demand, while scenario analysis tests price-elastic responses. When primary feedback reveals data voids, interpolation ranges are transparently logged and revisited each refresh.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst peer checks, sector-lead sign-off, and automated variance alerts against fresh trade or price prints. We redraw the model annually and issue interim tweaks when currency swings, crop shocks, or legislative changes materially alter the baseline.

Why Mordor's Europe Essential Oils Baseline Stands Up to Scrutiny

Published figures often diverge because providers pick different product baskets, apply unique price mix assumptions, or freeze exchange rates at varying dates. Our disciplined scope, rolling source roster, and yearly refresh mean users receive a value that mirrors real-time European trading conditions.

Key gap drivers include whether citrus terpenes are counted, how aromatherapy channels are sized, and the cadence of model updates. Some studies upscale global numbers by a flat regional share, while others rely on unvalidated producer surveys; Mordor Intelligence instead grounds its view in verified trade statistics that are continually reconciled with field interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.45 B (2025) | Mordor Intelligence | - |

| USD 12.77 B (2024) | Global Consultancy A | Includes fragrances and isolates; applies static EUR-USD rate |

| USD 2.71 B (2025) | Regional Consultancy B | Excludes food-grade citrus oils and uses limited country coverage |

Taken together, the comparison shows that our carefully bounded scope and live-data cadence yield a balanced, decision-ready baseline that clients can trace back to explicit variables and reproducible steps.

Key Questions Answered in the Report

What is the current value of the Europe essential oil market and its forecast for 2031?

The market is valued at USD 3.74 billion in 2026 and is projected to reach USD 5.60 billion by 2031, growing at an 8.41% CAGR.

Which ingredient type leads sales across Europe?

Orange oil heads the ranking with a 29.90% share, owing to its versatility in beverages, household cleaning and aromatherapy.

Why is Spain the fastest-growing country for essential oils in Europe?

Spain is expanding organic citrus acreage and leveraging rising export demand, driving a 9.51% forecast CAGR through 2031.

How do EU regulations affect small essential oil producers?

Compliance with REACH, allergen labeling and safety testing raises costs beyond many small distillers’ resources, nudging them toward bulk supply contracts with larger ingredient houses.

Which application segment will contribute most incremental value over 2026-2031?

Food and beverage applications, propelled by clean-label reforms, are set to add the largest absolute revenue through their 8.45% CAGR.

Page last updated on: