Human Microbiome Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

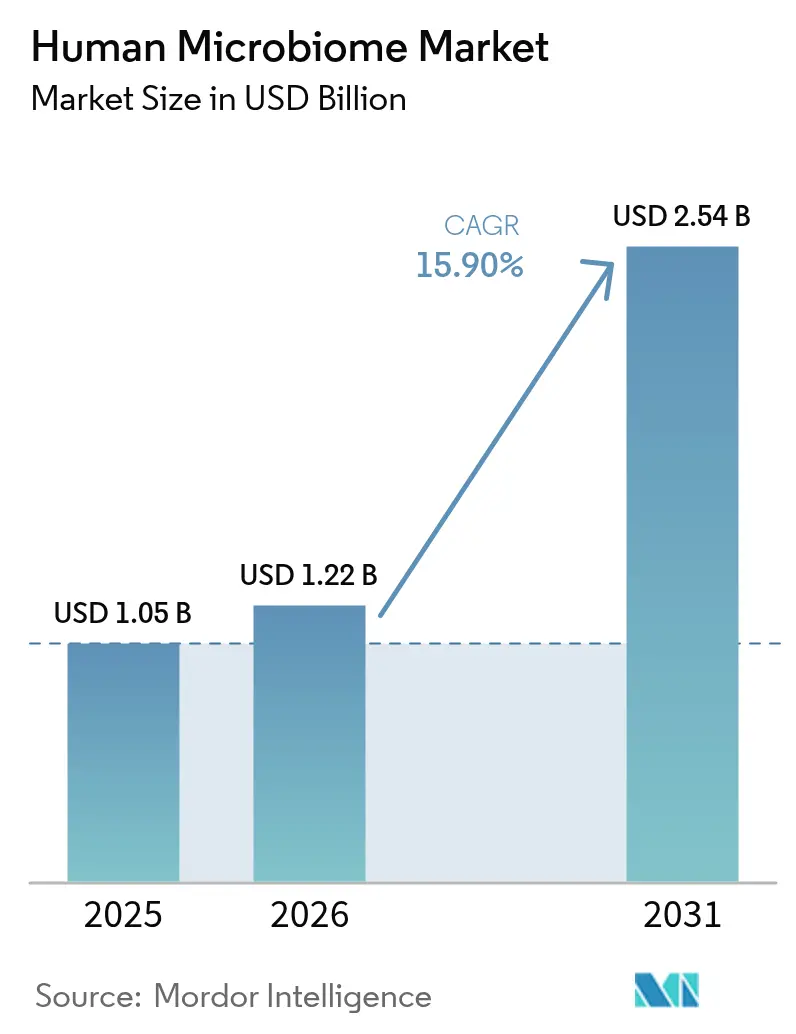

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 15.90% CAGR |

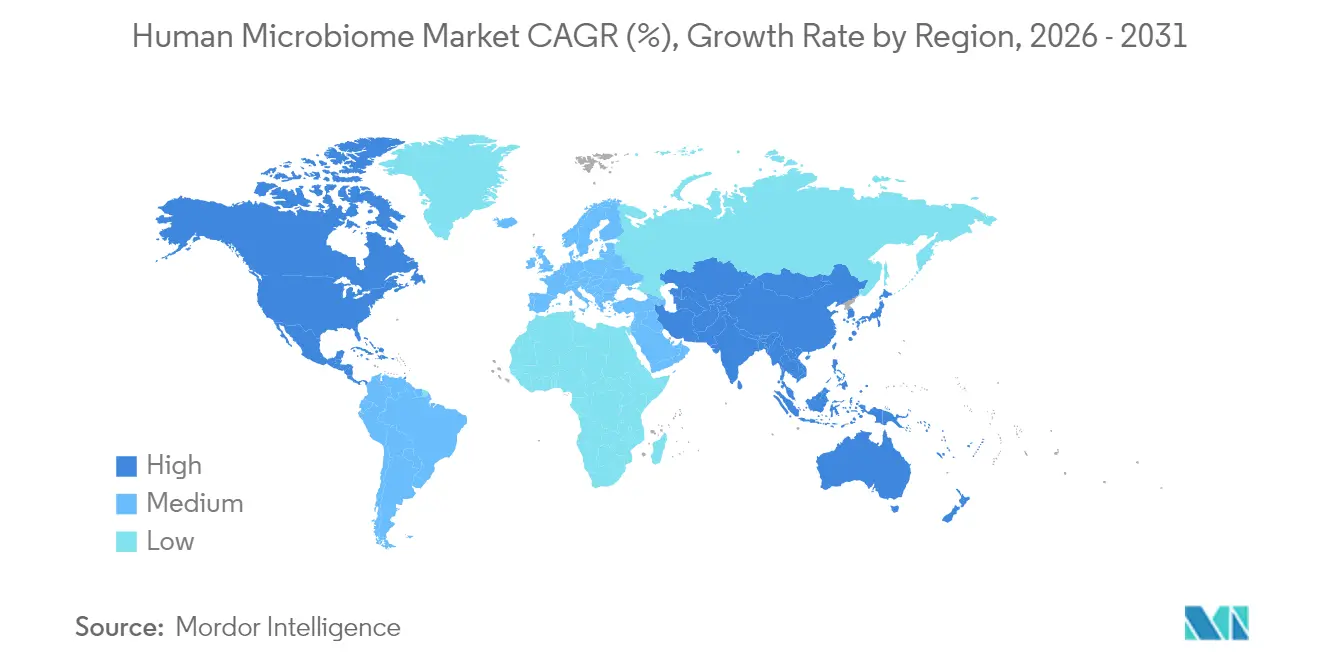

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Human Microbiome Market Analysis by Mordor Intelligence

The human microbiome market size is expected to grow from USD 1.05 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 2.54 billion by 2031 at 15.9% CAGR over 2026-2031. The expansion reflects a decisive shift from exploratory research toward validated therapeutics, spurred by FDA approvals of live biotherapeutic products, accelerating venture funding, and stepped-up pharmaceutical acquisitions. Cost-efficient next-generation sequencing, rising demand for personalized medicine, and growing clinical evidence linking gut microbes to systemic disease are reinforcing the growth trajectory of the human microbiome market. Industry participants are also benefiting from regulatory support for good-manufacturing-practice (GMP) facilities that can produce complex bacterial consortia at commercial scale. Combined, these factors continue to reposition the human microbiome market as a mainstream component of modern drug development and diagnostic practice.

Key Report Takeaways

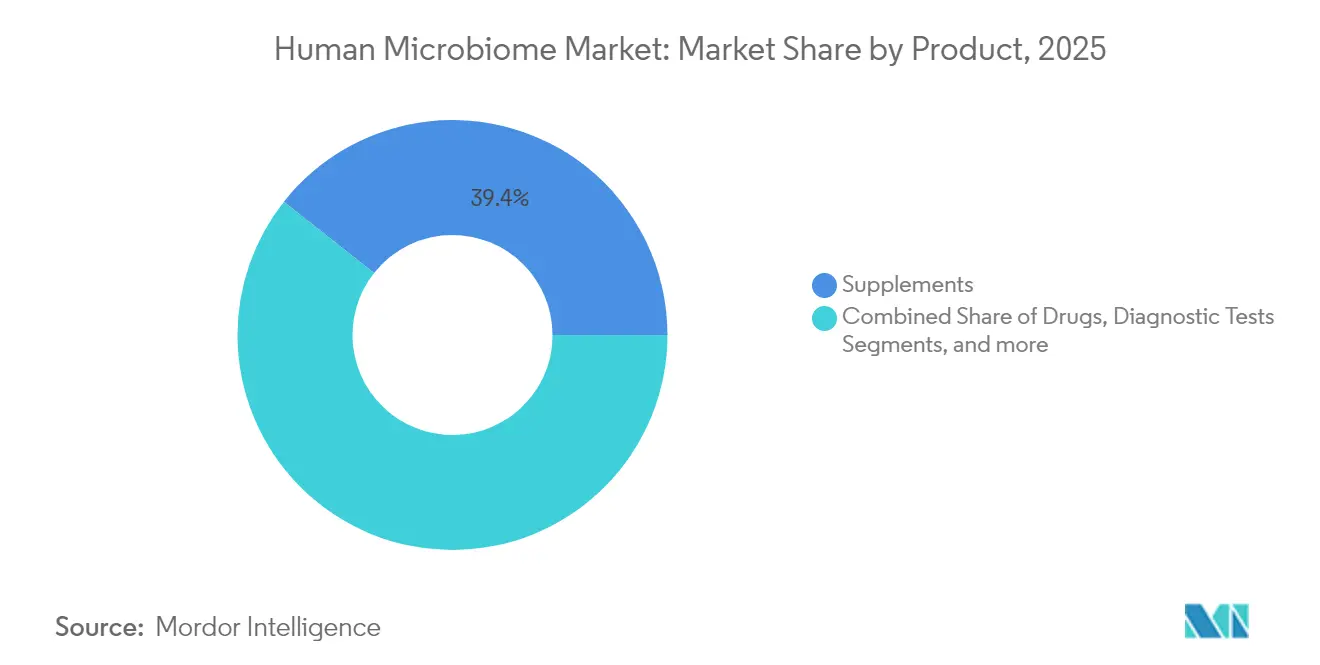

- By product, supplements held 39.35% of the human microbiome market share in 2025, while drugs are projected to record an 17.9% CAGR through 2031.

- By application, therapeutics represented 69.35% of the human microbiome market in 2025, but diagnostics are expected to advance at a 18.8% CAGR through 2031.

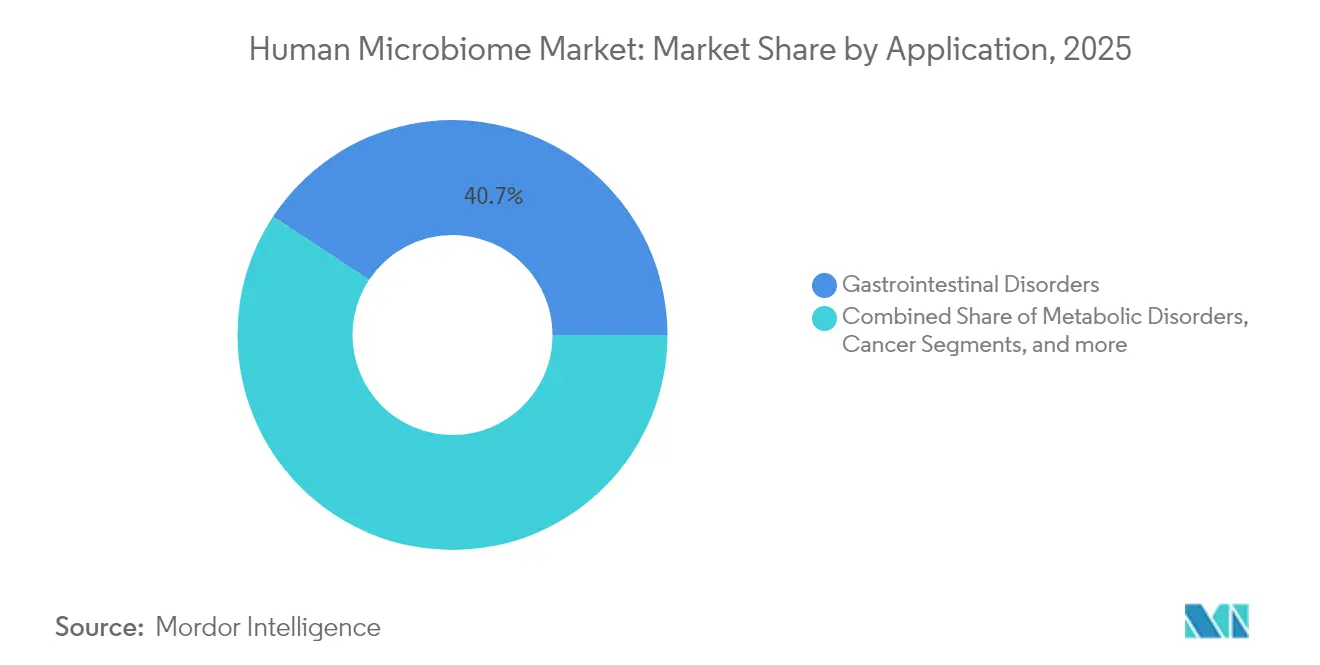

- By disease area, gastrointestinal disorders accounted for 40.72% of the human microbiome market size in 2025, and cancer applications are forecast to grow at a 18.95% CAGR to 2031.

- By end-user, hospitals and clinics captured 47.05% of 2025 revenue, whereas pharmaceutical and biotechnology companies are positioned to expand at an 18.05% CAGR through 2031.

- By geography, North America led with 41.75% of the human microbiome market share in 2025, while Asia-Pacific is projected to post an 18.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Microbiome Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in next-generation sequencing lowering microbiome analysis costs | +2.8% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Rising venture funding for microbiome-based therapeutics | +2.1% | North America & Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expanding Applications in Personalized Medicine | +1.9% | Global, with premium markets leading adoption | Long term (≥ 4 years) |

| Expansion of Direct to Consumer microbiome testing | +1.4% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Pharma–microbiome co-therapy alliances | +1.7% | Global, concentrated in major pharmaceutical hubs | Medium term (2-4 years) |

| Growing awareness about the advantages of microbiome-based products | +1.3% | Global, with varying penetration rates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancements in Next-Generation Sequencing Lowering Microbiome Analysis Costs

Real-time nanopore sequencing devices such as MinION and PromethION have cut per-sample costs by roughly 70%, enabling routine profiling that once required centralized laboratories [1]Tianyuan Zhang, "Nanopore sequencing: flourishing in its teenage years," Journal of Genetics and Genomics, sciencedirect.com. Portable platforms permit point-of-care analysis of gut microflora, accelerating diagnostic turnaround and supporting longitudinal monitoring. Full-length 16S rRNA workflows delivered by PacBio systems further increase taxonomic resolution needed for biomarker discovery. Sequencing expenditures are trending toward the USD 100 threshold, elevating the feasibility of incorporating microbiome checks into chronic-disease management pathways [2]Hyejung Han, "Optimizing microbiome reference databases with PacBio full-length 16S rRNA sequencing for enhanced taxonomic classification and biomarker discovery," Frontiers in Microbiology, frontiersin.org. Hospitals are already piloting regular microbial surveillance for inflammatory bowel disease patients, confirming the clinical relevance of affordable sequencing. Combined, these advances are widening the addressable base of the human microbiome market across both diagnostics and therapeutics.

Rising Venture Funding for Microbiome-Based Therapeutics

Dedicated venture funds and strategic corporate investors allotted record capital to the sector in 2025, catalyzing dozens of seed and Series A rounds in Europe, North America, and East Asia. European developers such as Abolis Biotechnologies secured EUR 35 million to scale biomanufacturing capacity, while public–private initiatives like CARB-X handed out multimillion-dollar grants targeting antimicrobial-resistance applications. Janssen’s Human Microbiome Institute cemented flexible partnership vehicles that enable start-ups to co-develop co-therapy assets with large-scale drug manufacturers [3]Johnson & Johnson, “Human Microbiome Institute Partnerships,” jnj.com . Pharma–microbiome alliances frequently include equity investments tied to predefined milestones, giving young companies funding certainty and mentor access. The resultant capital inflows shorten development timelines, drive talent acquisition, and speed regulatory submissions, reinforcing the upward momentum of the human microbiome market.

Expanding Applications in Personalized Medicine

Clinical platforms that harness microbial signatures to tailor treatment have demonstrated superior outcomes in metabolic and autoimmune disorders, outperforming standardized protocols in controlled trials. AI engines overlap metagenomics with diet logs to generate hyper-personalized nutrition plans that moderate hyperglycemia and hypertension. Multi-omics integration with machine learning refines patient stratification for oncology trials, where baseline gut diversity predicts checkpoint-inhibitor response. Pharmaceutical sponsors now embed microbiome profiling in study designs to allocate participants more efficiently, boosting statistical power while lowering costs. Digital health companions facilitate continuous data upload, allowing clinicians to recalibrate regimens in real time. The growing emphasis on individualized intervention unlocks additional value for the human microbiome market across diagnostics, therapeutics, and monitoring services.

Expansion of Direct-to-Consumer Microbiome Testing

Retail availability through pharmacy chains and e-commerce sites has broadened consumer access to gut microbe testing kits, especially in the United States and Western Europe. Vendors increasingly deliver actionable reports that translate bacterial patterns into diet and lifestyle recommendations, aided by machine-learning interpretation engines. Regulators are tightening oversight to ensure analytical validity; the European Union now distinguishes between wellness tests and in-vitro diagnostics requiring CE marking. Industry groups are developing voluntary quality standards to harmonize methodologies and reporting. As unit prices fall below USD 100, purchase frequency rises, increasing data pools that help refine predictive algorithms. Greater consumer familiarity continues to funnel new users into the broader human microbiome market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardization and Regulatory Guidelines | -3.2% | Global, with varying regional impacts | Medium term (2-4 years) |

| GMP scale-up challenges for live biotherapeutics | -2.1% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Limited Understanding of Complex Microbiome Interactions | -1.8% | Global, with research-intensive regions most affected | Long term (≥ 4 years) |

| Slow patient adoption | -1.4% | North America & Europe primarily, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardization and Regulatory Guidelines

Microbiome therapeutics straddle medicinal-product and transplant regulations, generating policy ambiguity that slows cross-border trials and market launches. Divergent definitions of live biotherapeutic products across the FDA, EMA, and Japan’s PMDA complicate dossier preparation and compromise mutual-recognition ambitions. Analytical discord persists as laboratories deploy varied DNA-extraction, library-prep, and bioinformatics workflows, producing inconsistent readouts that dampen clinician trust. Upcoming European Union rules governing substances of human origin promise eventual harmonization but will not take full effect before 2026. Until global norms converge, companies must budget for region-specific validation studies, raising costs and delaying revenue capture in the human microbiome market.

GMP Scale-Up Challenges for Live Biotherapeutics

Harvesting, formulating, and packaging multi-strain bacterial consortia require sterile single-use fermenters, real-time viability analytics, and cold-chain shipping to preserve potency. Few facilities can reliably deliver phase-appropriate volumes that meet FDA and EMA expectations. Synlogic’s purpose-built site and the University of Chicago Medicine’s academic cGMP hub highlight the capital intensity involved in scaling live biologics. Lyophilization protocols must balance moisture removal with cell integrity, often demanding bespoke cryoprotectants. Disruptions during the COVID-19 pandemic underscored the fragility of specialized reagent supply chains. These production complexities lengthen time-to-market and elevate cost of goods sold, narrowing margins in the human microbiome market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutic Validation Accelerates Drugs Growth

Supplements maintained a 39.35% revenue share in 2025, reflecting longstanding consumer adoption and streamlined regulatory routes. Drugs, however, are on track to register an 17.9% CAGR through 2031, buoyed by landmark approvals such as VOWST and REBYOTA, which showcase clinically proven benefits against recurrent C. difficile infections. Initial roll-out of VOWST generated USD 10.4 million in Q4 2023, validating commercial appetite and emboldening additional filings. Probiotic supplements face mounting scrutiny as authorities delineate dietary products from live biotherapeutic drugs, prompting manufacturers to invest in randomized controlled trials.

Diagnostic assays remain the smallest contributor but attract intensified investment as companion tests become essential for patient stratification in oncology and metabolic trials. Postbiotics and engineered bacterial strains represent emerging niches that may bridge nutraceutical and pharmaceutical spaces. The bifurcation of consumer-grade and prescription-grade offerings underpins diversified revenue streams within the broader human microbiome market.

By Application: Diagnostics Gain Momentum Alongside Therapeutics

Therapeutic use cases accounted for 69.35% of revenue in 2025, yet diagnostics enjoy a forecast 18.8% CAGR to 2031 as sequencing costs plummet and analytical software matures. Hospital networks are piloting stool-based panels that predict response to immuno-oncology agents, improving treatment selection and reimbursement outcomes. Fecal microbiota transplantation remains the archetypal therapeutic model, but pipeline assets now encompass oral capsules, topical formulations, and engineered strains targeting metabolic, autoimmune, and neurologic diseases.

The convergence of end-to-end platforms that combine sampling kits, sequencing services, AI analytics, and targeted interventions promises integrated care pathways. Developers able to link a validated diagnostic to a proprietary therapeutic could capture outsized value across the human microbiome market size.

By Disease Area: Cancer Leads Growth Beyond GI Dominance

Gastrointestinal disorders retained 40.72% of revenue in 2025, supported by extensive clinical data and regulatory approvals. Cancer applications are forecast to expand at a 18.95% CAGR, propelled by studies reporting the conversion of checkpoint-inhibitor non-responders into responders after fecal microbiota transplantation. MD Anderson Cancer Center’s collaboration with Kanvas Biosciences to develop synthetic “super-donor” formulations amplifies commercial prospects.

Metabolic disorders are gaining traction as evidence mounts linking Akkermansia muciniphila abundance to improved insulin sensitivity, while autoimmune applications leverage probiotic-mediated modulation of inflammatory pathways. Central nervous system research is still formative but draws sustained NIH support to probe gut–brain connections. Collectively, these advancements diversify therapeutic pipelines, reinforcing the resilience of the human microbiome market.

By End-User: Pharma & Biotech Companies Accelerate Deployment

Hospitals and clinics generated 47.05% of 2025 sales, reflecting direct administration of transplantation procedures and prescription products. Pharmaceutical and biotechnology sponsors, however, are expected to log an 18.05% CAGR through 2031 as they assume stewardship of clinical-stage assets and expand manufacturing footprints. Nestlé Health Science’s USD 175 million acquisition of VOWST demonstrates willingness to pay for late-phase candidates with clear regulatory pathways.

Academic institutes remain indispensable for mechanistic discovery and early-stage trials; the University of Chicago Medicine’s cGMP facility underpins multiple investigator-initiated studies. Contract research organizations and specialized GMP vendors fill capability gaps in analytics and production. The layered ecosystem sustains a robust pipeline feeding the continually expanding human microbiome market.

Geography Analysis

North America commanded 41.75% of global revenue in 2025, underpinned by FDA guidance, seasoned venture networks, and a critical mass of GMP plants. Early adopter hospitals routinely implement fecal microbiota transplantation for recurrent C. difficile and are piloting diagnostic panels for oncology. Increasing reimbursement clarity supports broader uptake, solidifying the region’s influence on human microbiome market dynamics.

Europe benefits from dense academic clusters and coordinated funding frameworks; the European Commission’s 2025 biotechnology roadmap prioritizes microbial therapeutics for health and sustainability. Yet divergent national oversight regimes slow multicountry trials, keeping manufacturers reliant on expensive parallel submissions. Public–private partnerships such as those in France and the Netherlands supply translational funding that sustains competitiveness.

Asia-Pacific is projected to record an 18.35% CAGR as regulators converge on harmonized standards and local companies pour capital into fermentation and fill-finish capabilities. The JSR-Metagen plant scheduled for 2025 in Japan exemplifies the region’s resolve to nurture domestic production capacity. Partnerships like Zuellig Pharma’s decade-long deal to distribute OMNi-BiOTiC probiotics across Southeast Asia further enlarge the addressable base. China and South Korea expedite commercialization by bundling microbiome projects with national precision-medicine policies. Collectively, these developments broaden global participation in the human microbiome market.

Competitive Landscape

The competitive terrain remains moderately fragmented. Start-ups wield proprietary strain libraries, AI analytics, or synthetic-biology toolkits, while established food and pharma conglomerates leverage capital strength and distribution networks. Nestlé Health Science’s purchase of VOWST and Danone’s acquisition of The Akkermansia Company indicate that multinationals view microbiome therapies as strategic pillars. Seres Therapeutics and Vedanta Biosciences hold pivotal patents covering Clostridium clusters and defined consortia manufacturing, giving them defensible positions in high-value indications.

Novonesis, formed from Novozymes and Chr. Hansen, integrates fermentation expertise with clinical development to create a unified biosolutions platform. AI-first entrants such as 32 Biosciences design bacterial consortia in silico before lab validation, compressing discovery cycles and reducing wet-lab costs. Manufacturing service specialists like Rise Therapeutics supply turnkey GMP production for firms lacking in-house capabilities, monetizing infrastructure scale. Overall, deals focus on de-risking pipelines, accessing commercial plants, and consolidating IP, sustaining a robust yet consolidating human microbiome market.

Human Microbiome Industry Leaders

-

Second Genome Inc

-

Seres Therapeutics

-

Axial Biotherapeutics Inc

-

DuPont

-

Synthetic Biologics.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Metabolon launched a combined metagenomics and metabolite panel to streamline microbiome research workflows.

- January 2025: MaaT Pharma reported positive Phase 3 data for Maat013 in acute GVHD with GI involvement.

- October 2024: Rise Therapeutics secured NIH funding to expand GMP capacity for R-3750 in inflammatory bowel disease.

- May 2024: Vedanta Biosciences dosed the first participant in its global Phase 3 VE303 trial aimed at preventing recurrent C. difficile infection.

Global Human Microbiome Market Report Scope

As per the scope of the report, the human microbiome is a full array of microorganisms (the microbiota) that live in humans. More specifically, the collection of microbial genomes that contribute to a human's broader genetic portrait, or metagenome.

The human microbiome market is segmented by application, disease, and product. By applications, the market is segmented into therapeutics and diagnostics. By disease, the market is segmented into obesity, diabetes, autoimmune disorders, cancer, gastrointestinal disorders, central nervous system disorders, and other diseases. By products, the market is segmented into probiotics, prebiotics, symbiotics and other products. By geography, the global market is segmented into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America). The market report also covers the estimated human microbiome market size and market trends for 17 countries across major regions globally. The report offers the value (in USD billion) for the above segments.

| Drugs | |

| Supplements | Probiotics |

| Prebiotics | |

| Synbiotics | |

| Diagnostic Tests | |

| Other Products |

| Therapeutics |

| Diagnostics |

| Gastrointestinal Disorders |

| Metabolic Disorders |

| Cancer |

| Autoimmune & Inflammatory Diseases |

| Central Nervous System Disorders |

| Other Applications |

| Hospitals and Clinics |

| Pharmaceutical & Biotechnology Companies |

| Research & Academic Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Drugs | |

| Supplements | Probiotics | |

| Prebiotics | ||

| Synbiotics | ||

| Diagnostic Tests | ||

| Other Products | ||

| By Application | Therapeutics | |

| Diagnostics | ||

| By Disease Area | Gastrointestinal Disorders | |

| Metabolic Disorders | ||

| Cancer | ||

| Autoimmune & Inflammatory Diseases | ||

| Central Nervous System Disorders | ||

| Other Applications | ||

| By End-user | Hospitals and Clinics | |

| Pharmaceutical & Biotechnology Companies | ||

| Research & Academic Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the human microbiome market?

The human microbiome market size is USD 1.22 billion in 2026.

How fast is the sector expected to grow?

From 2026 to 2031 the market is forecast to register a 15.9% CAGR.

Which product segment is expanding the quickest?

Drug-based live biotherapeutics are expected to post an 17.9% CAGR through 2031.

Which region will witness the highest growth?

Asia-Pacific is projected to advance at an 18.35% CAGR between 2026 and 2031.

What therapeutic area shows the strongest growth outlook?

Cancer applications are predicted to expand at a 18.95% CAGR during the forecast period.

Who are some leading players to watch?

Seres Therapeutics, Nestlé Health Science, Vedanta Biosciences, and Novonesis are among the key companies shaping the landscape.

Page last updated on: