Microbiome Therapeutics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

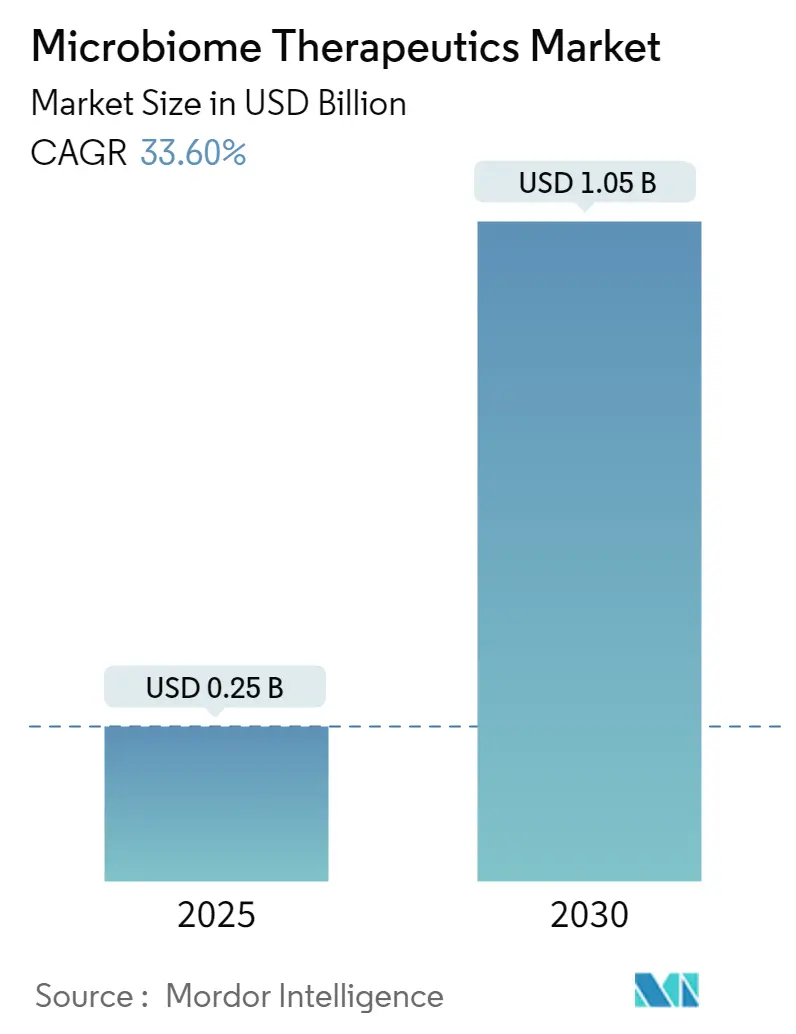

| Market Size (2025) | USD 0.25 Billion |

| Market Size (2030) | USD 1.05 Billion |

| Growth Rate (2025 - 2030) | 33.60% CAGR |

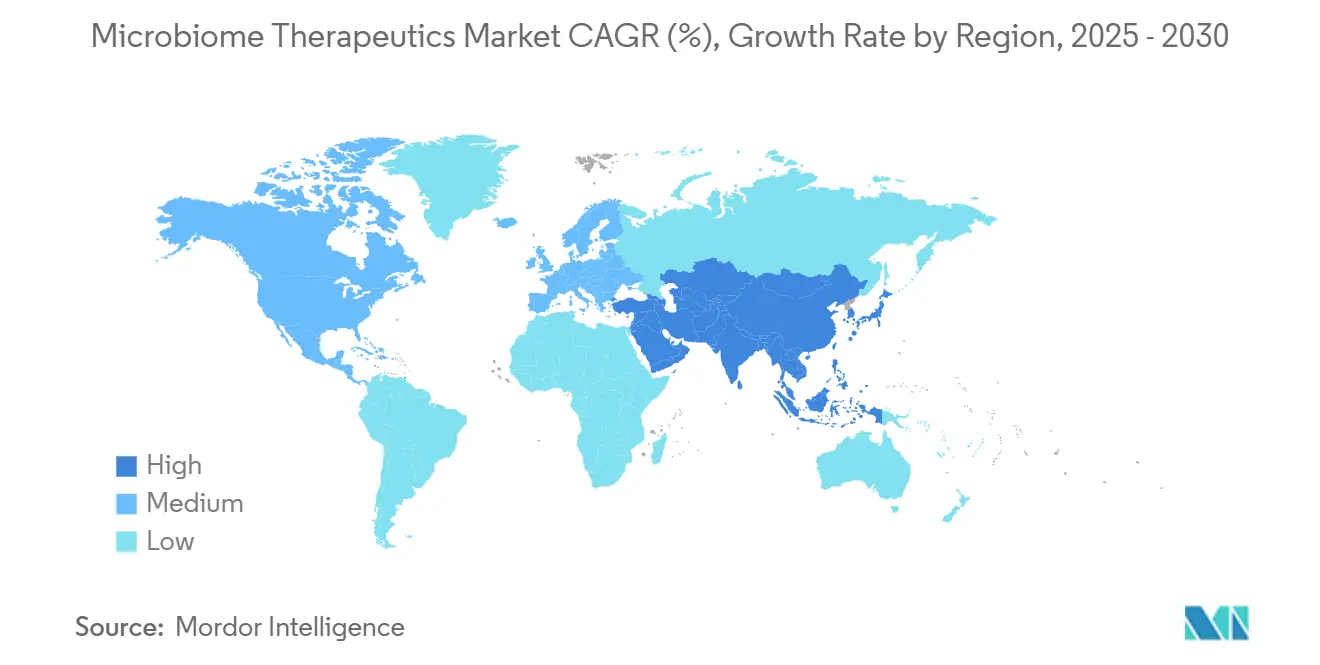

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

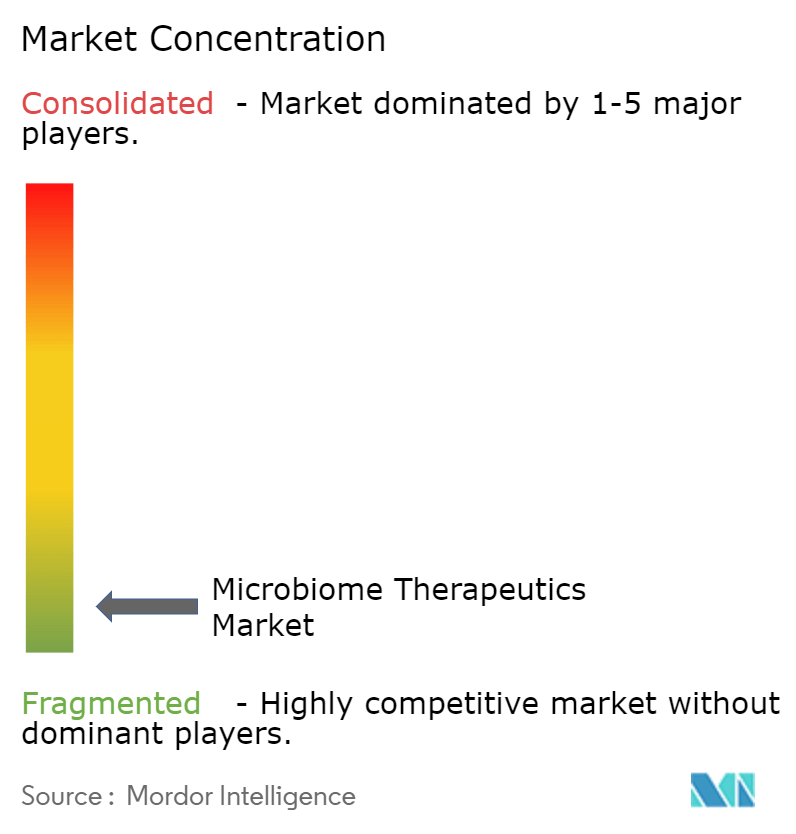

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microbiome Therapeutics Market Analysis by Mordor Intelligence

The microbiome therapeutics market recorded a value of USD 0.25 billion in 2025 and is forecast to reach USD 1.05 billion by 2030, advancing at a robust 33.6% CAGR. This rapid expansion reflects a maturation phase in which live biotherapeutic products, once confined to research settings, are gaining commercial traction following landmark regulatory approvals. Capital flows into the field surpassed USD 500 million in 2024 and continue to rise as investors align with the clear U.S. Food and Drug Administration pathway and parallel guidance emerging in Japan and Europe. Companies are prioritizing scalable oral formulations that reduce hospital dependence, while precision‐editing consortia and phage‐engineered therapies promise disease-specific solutions. Supply chain investment has accelerated, yet cGMP costs and ultra-cold logistics remain critical constraints, encouraging strategic partnerships with contract manufacturing organizations. Commercial momentum is similarly fueled by hospitals eager to cut readmission penalties tied to recurrent C. difficile infection and by payers that now recognize durable cost savings in inflammatory and metabolic disease management.

Key Report Takeaways

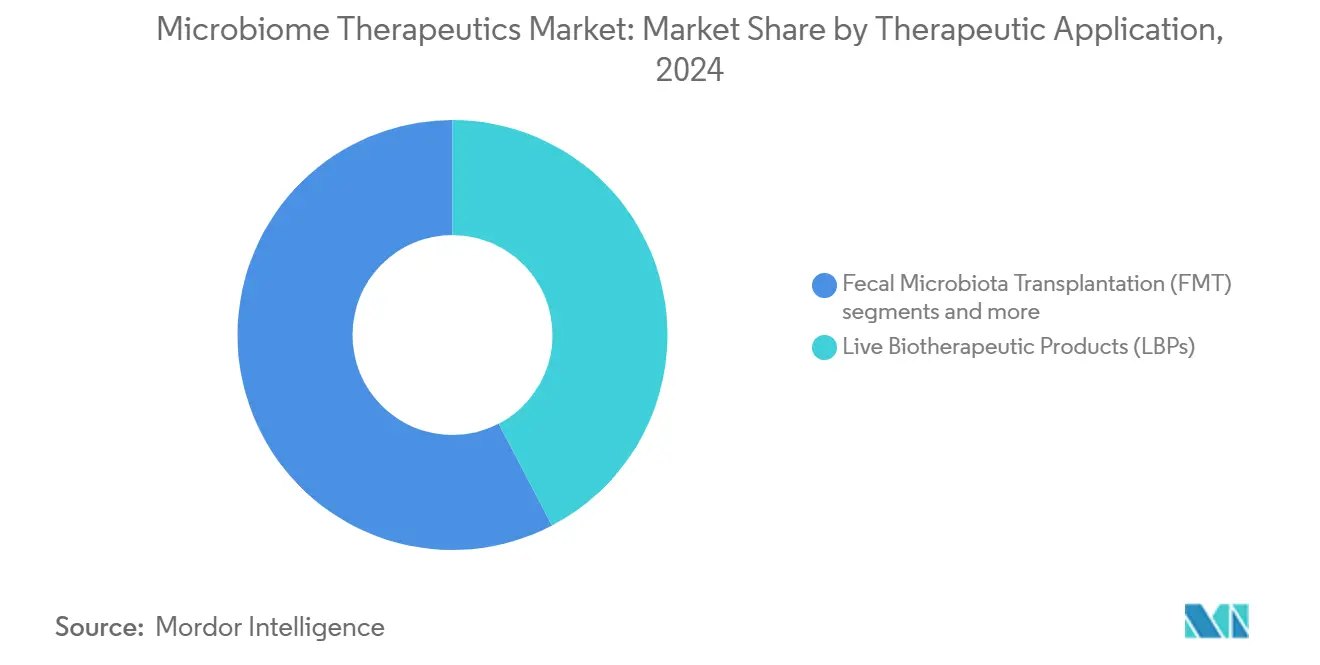

By therapeutic approach, live biotherapeutic products led with 42.34% of microbiome therapeutics market share in 2024; phage-/CRISPR-engineered consortia are projected to grow at a 35.65% CAGR from 2025 to 2030.

By application, recurrent C. difficile infection held 38.45% share of the microbiome therapeutics market size in 2024, while oncology applications are forecast to expand at a 36.33% CAGR through 2030.

By microbiome target site, the gut segment dominated with 83.06% share in 2024; skin applications show the fastest growth at 37.02% CAGR to 2030.

By route of administration, colonoscopic delivery commanded 41.39% revenue share in 2024, yet oral capsules are advancing at a 37.73% CAGR.

By geography, North America contributed 48.61% revenue share in 2024, whereas Asia-Pacific is expected to log a 38.45% CAGR through 2030.

Global Microbiome Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA approvals of Rebyota and VOWST | +5.0% | North America, spillover to EU & APAC | Short term (≤ 2 years) |

| Accelerating venture capital and Big-Pharma deals | +4.0% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Declining sequencing and bioinformatics costs | +3.4% | Global, early uptake in developed markets | Long term (≥ 4 years) |

| Hospital push to curb rCDI readmissions | +2.7% | North America and Europe | Short term (≤ 2 years) |

| Engineered-microbe toolkits | +3.0% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Payer recognition of long-term savings | +2.4% | North America and Europe | Medium term |

| Source: Mordor Intelligence | |||

FDA approvals validate regulatory pathway

The FDA’s clearance of Rebyota in 2022 and VOWST in 2023 opened the first reproducible route for live biotherapeutic products, proving that complex microbial consortia can meet stringent pharmaceutical standards. VOWST demonstrated 90.5% recurrence-free outcomes at eight weeks, anchoring clinical confidence. These approvals significantly reduced perceived development risk, enabling companies to justify USD 100–200 million late-stage programs and prompting global regulators—including the European Medicines Agency and Japan’s PMDA—to draft parallel guidance. Dedicated manufacturing facilities expanded in the United States and Europe, with CMOs such as Arranta Bio ramping cGMP capacity to serve emerging pipelines. The clarity has thus accelerated investigational new drug filing rates and compressed commercialization timelines across the microbiome therapeutics market.

Accelerating VC funding and Big-Pharma partnerships

Venture capital commitments topped USD 500 million in 2024, a 40% year-over-year rise, as investors prioritized platforms with multi-indication potential. Nestlé Health Science’s acquisition of VOWST™ rights underscored Big-Pharma appetite and signaled an expectation of mainstream uptake. Strategic alliances frequently bundle clinical assets with exclusive manufacturing slots, reflecting demand for scarce fermentation capacity. Partnerships now emphasize artificial-intelligence-enabled discovery and strain-level intellectual property portfolios, positioning the microbiome therapeutics market for continued deal activity through 2030.

Rapid drop in next-generation sequencing and bioinformatics costs

Whole-genome sequencing prices fell from USD 10,000 per sample in 2020 to below USD 1,000 by 2024, while computational costs dropped 60%, democratizing in-house profiling and patient stratification. The accessibility of shotgun metagenomics empowers mid-size biotechs to iterate bacterial consortia rapidly, informs personalized dosing, and feeds machine-learning models that predict host-microbe pharmacodynamics. These advances lower trial costs and heighten likelihood of clinical success across the microbiome therapeutics market.

Hospital demand to curb rCDI readmissions and penalties

Hospitals risk penalties approaching USD 43,000 for every recurrent C. difficile case under U.S. Medicare rules, a powerful incentive to adopt therapies that slash recurrence below 10%. Formularies now prioritize live biotherapeutics that cut average length of stay, improve quality metrics, and reduce surgical interventions. Early adoption has been strongest in gastroenterology units but is broadening to oncology wards where immunotherapy synergy is under study. As healthcare systems pivot to value-based care, reimbursement frameworks increasingly favor microbiome interventions with demonstrable downstream savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unsettled global regulatory standards | −2.7% | Europe, Asia-Pacific, Latin America | Medium term (2-4 years) |

| cGMP manufacturing & cold-chain costs | −2.0% | Global | Long term (≥ 4 years) |

| Public “ick factor” toward fecal products | −1.3% | Global, higher in conservative markets | Short term (≤ 2 years) |

| Limited long-term safety data | −1.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Unsettled global regulatory standards for live biotherapeutics

The European Medicines Agency is still finalizing stability and potency criteria, extending approval timelines by 18–24 months for several candidates. Asia-Pacific adds complexity: China requires local trials, and Latin American authorities lack harmonized guidelines. Sequential, rather than simultaneous, launches inflate development budgets and slow revenue realization within the microbiome therapeutics market.

cGMP manufacturing and cold-chain costs for live organisms

Building a dedicated facility can exceed USD 100 million, while temperature-controlled logistics can inflate delivered cost by 20–30%. Scarce third-party capacity forces start-ups into expensive long-term contracts or joint ventures. Batch variability, viability testing, and regulatory documentation further erode margins until volumes reach scale, tempering profitability projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Approach: Live biotherapeutics spearhead adoption

Live biotherapeutic products captured 42.34% of 2024 revenue, anchored by the first FDA-approved drugs and supported by defined strain manufacturing that assures consistency. Their established profile eases hospital pharmacy inclusion and secures payer coverage, reinforcing a virtuous cycle of uptake across the microbiome therapeutics market. Fecal microbiota transplantation retains utility for acute interventions, yet payers favor standardized capsules that reduce infection risk. Probiotic/prebiotic combination therapeutics fill a transitional niche, often sold direct-to-consumer while sponsors seek drug-labeling upgrades. Synbiotics and postbiotics circumvent cold-chain hurdles, enabling penetration in regions lacking robust logistics. Microbiome-derived metabolites, though early-stage, attract pharmaceutical interest due to small-molecule familiarity and scalable chemistry.

Concurrently, intellectual-property strategies differ: live biotherapeutic sponsors focus on manufacturing know-how, whereas phage therapy developers rely on genomic patents. Manufacturing flexibilities also diverge; engineered microbes require stringent containment but lower biomass volumes, while whole-stool products need large-scale donors and screening. These nuances shape capital allocation and partnership models, with big pharma preferring platform technologies that de-risk multi-indication expansion.

By Application: Oncology moves from proof-of-concept to pipeline priority

Recurrent C. difficile infection stood at 38.45% share in 2024, serving as the commercial beachhead for the microbiome therapeutics market. Real-world data show a drop in 30-day readmissions from 24% to under 8%, reinforcing health-system demand. Oncology represents the fastest-growing use, advancing at 36.33% CAGR as consortia synergize with checkpoint inhibitors and mitigate immune-related adverse events. Phase 2 readouts in melanoma and colorectal cancer have spurred multi-center trials, and pharma partners view microbiome modulation as a companion diagnostic opportunity.

Beyond these anchors, inflammatory bowel disease trials leverage defined strains to restore mucosal homeostasis, while metabolic disorder programs seek to modulate insulin sensitivity through bile-acid signaling. Neurological applications gain support from gut-brain axis data, with Parkinson’s and autism studies entering Phase 1.

Geography Analysis

North America generated 48.61% of 2024 revenue, benefiting from the earliest approvals, substantial venture funding, and integrated healthcare systems that reward infection-control innovations. Medicare reimbursement codes introduced in 2024 underpin payer confidence, while Canada’s single-payer provinces add volume through formulary inclusion. University-based spin-outs located in Boston, San Diego, and Toronto funnel discoveries into local cGMP incubators, reinforcing a tight innovation loop within the microbiome therapeutics market.

Europe trails in absolute revenue but commands a sophisticated research base. Germany and the United Kingdom anchor manufacturing hubs, leveraging bioprocess expertise and generous R&D tax credits. Regulatory lag curbs near-term launches, yet EMA harmonization is expected by 2027, unlocking pent-up demand. Nordic nations pilot payer-driven risk-sharing agreements that could set a regional template for chronic-disease indications.

Asia-Pacific is the fastest-growing territory, posting a projected 38.45% CAGR through 2030. Japan’s Pharmaceuticals and Medical Devices Agency adopted FDA-centric definitions in 2024, prompting domestic conglomerates to license Western platforms. China’s vast patient pools accelerate trial recruitment, while Hainan province’s Boao Lecheng zone expedites early-access schemes. South Korea’s biologics leadership extends to live microbial fermentation; Australia offers adaptive trial infrastructure attractive to early-stage sponsors. Collectively, these dynamics are expected to push the microbiome therapeutics market share of Asia-Pacific to 26% by 2030, up from 14% in 2024.

Competitive Landscape

The ecosystem features 99 active developers, yet leadership is coalescing around firms with approved products and vertically integrated facilities. Seres Therapeutics capitalized on first-mover status by in-licensing Bacillota spores and securing Nestlé Health Science as commercialization partner. Ferring Pharmaceuticals complements its obstetrics franchise with microbiome assets, leveraging existing cold-chain expertise. Vedanta Biosciences pursues synthetic consortia spanning infectious, autoimmune, and oncology paths. Collectively the top five companies held 41% of 2024 revenue, suggesting moderate concentration across the microbiome therapeutics market.

Emerging disruptors adopt precision approaches. BiomX acquired Adaptive Phage Therapeutics to broaden its individualized phage libraries, targeting cystic fibrosis and diabetic osteomyelitis. MaaT Pharma uses pooled donor material standardized by artificial intelligence to treat graft-versus-host disease, reporting a pivotal trial win in 2025. Start-ups focusing on synthetic biology engineer microbes to secrete therapeutic enzymes or block inflammatory cytokines, courting partnerships that offset expensive manufacturing build-outs.

Strategic themes include exclusive CMO slots, integrated companion diagnostics, and region-specific alliances that navigate regulatory uncertainty. With scale-up costs topping USD 50 million for a cGMP plant, capital-rich incumbents could absorb smaller peers, pointing to consolidation that will reshape the microbiome therapeutics market by decade-end.

Microbiome Therapeutics Industry Leaders

OpenBiome

Seres Therapeutics

Locus Biosciences, Inc.

Finch Therapeutics Group, Inc

Intralytix, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nestlé Health Science finalized the purchase of global VOWST™ rights from Seres Therapeutics

- March 2025: BiomX Inc. acquired Adaptive Phage Therapeutics, expanding its personalized phage arsenal

Global Microbiome Therapeutics Market Report Scope

As per the scope of the report, microbiome therapeutics are utilized in engineering the gut microbiome using additive, subtractive, or modulatory therapy with an application of native or engineered microbes, bacteriophages, and bacteriocins. The microbiome therapeutics market is segmented into therapy type, application, and geography. By therapy type, the market is segmented into fecal microbiota transplantation (FMT) and microbiome drugs. By application, the market is segmented into clostridium difficile(C.diff) Infection, Crohn’s disease, inflammatory bowel disease, diabetes, and others (obesity and oncology). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (in USD) for the above segments.

| Live Biotherapeutic Products (LBPs) |

| Fecal Microbiota Transplantation (FMT) |

| Probiotic / Prebiotic Combination Therapeutics |

| Synbiotics & Postbiotics |

| Phage-/CRISPR-Engineered Consortia |

| Microbiome-Derived Metabolite Drugs |

| Recurrent C. difficile Infection (rCDI) |

| Inflammatory Bowel Disease (IBD) |

| Metabolic Disorders (Obesity, Diabetes) |

| Oncology (Immuno-Oncology adjuncts) |

| Neurological Disorders (Autism, Parkinson’s, etc.) |

| \Others (Liver, Dermatology, etc.) |

| Gut |

| Skin |

| Oral |

| Vaginal |

| Respiratory |

| Others |

| Oral Capsules |

| Enema/Liquid Suspension |

| Colonoscopic Delivery |

| Nasogastric/PEG Tube |

| Topical/Dermal |

| North America |

| United States | Canada |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Therapeutic Approach | Live Biotherapeutic Products (LBPs) | |

| Fecal Microbiota Transplantation (FMT) | ||

| Probiotic / Prebiotic Combination Therapeutics | ||

| Synbiotics & Postbiotics | ||

| Phage-/CRISPR-Engineered Consortia | ||

| Microbiome-Derived Metabolite Drugs | ||

| By Application | Recurrent C. difficile Infection (rCDI) | |

| Inflammatory Bowel Disease (IBD) | ||

| Metabolic Disorders (Obesity, Diabetes) | ||

| Oncology (Immuno-Oncology adjuncts) | ||

| Neurological Disorders (Autism, Parkinson’s, etc.) | ||

| \Others (Liver, Dermatology, etc.) | ||

| By Microbiome Target Site | Gut | |

| Skin | ||

| Oral | ||

| Vaginal | ||

| Respiratory | ||

| Others | ||

| By Route of Administration | Oral Capsules | |

| Enema/Liquid Suspension | ||

| Colonoscopic Delivery | ||

| Nasogastric/PEG Tube | ||

| Topical/Dermal | ||

| North America | ||

| By Geography | United States | Canada |

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the microbiome therapeutics market?

The microbiome therapeutics market reached USD 0.25 billion in 2025 and is forecast to expand to USD 1.05 billion by 2030.

Which therapeutic approach dominates this field?

Live biotherapeutic products lead, holding 42.34% of 2024 revenue due to established FDA approvals and scalable manufacturing.

Why are oncology applications growing so quickly?

Combination trials show that select microbial strains enhance checkpoint-inhibitor efficacy and reduce toxicities, driving a 36.33% CAGR in oncology revenue.

Which region is expected to grow the fastest?

Asia-Pacific is projected to post a 38.45% CAGR through 2030, supported by regulatory harmonization in Japan and large-scale trials in China.

Page last updated on: