Industrial Metal Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

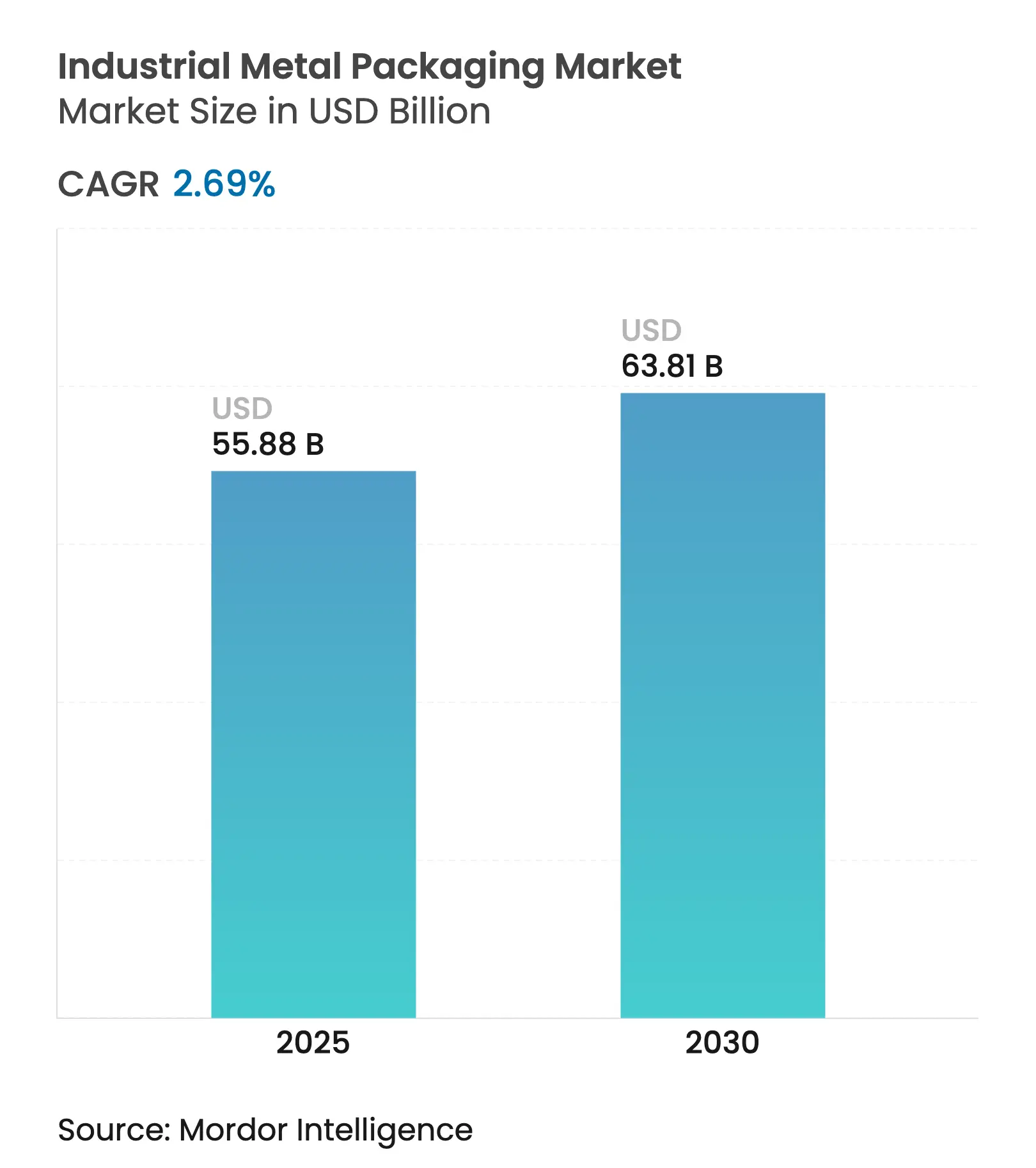

| Market Size (2025) | USD 55.88 Billion |

| Market Size (2030) | USD 63.81 Billion |

| Growth Rate (2025 - 2030) | 2.69 % CAGR |

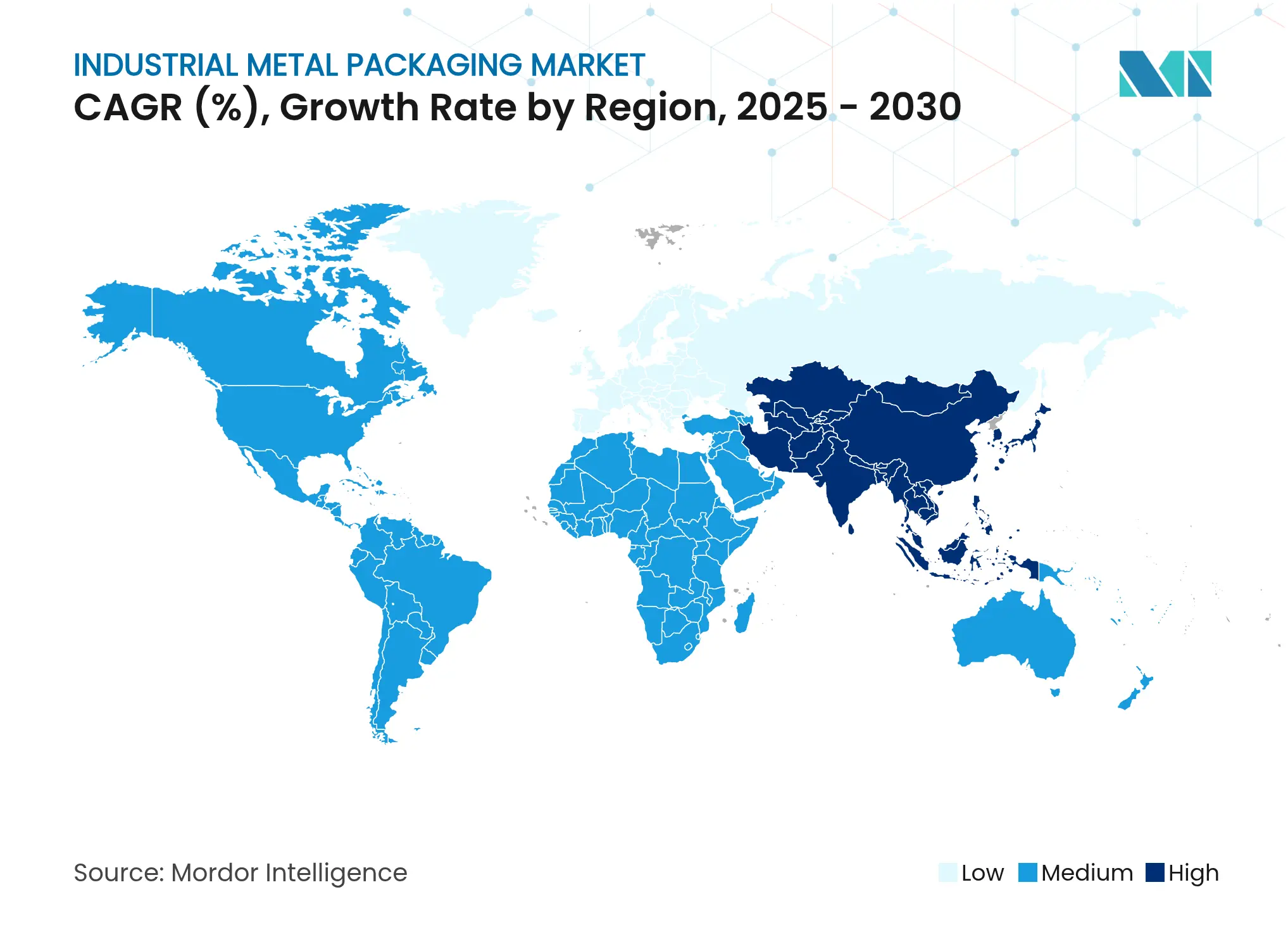

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Industrial Metal Packaging Market Analysis by Mordor Intelligence

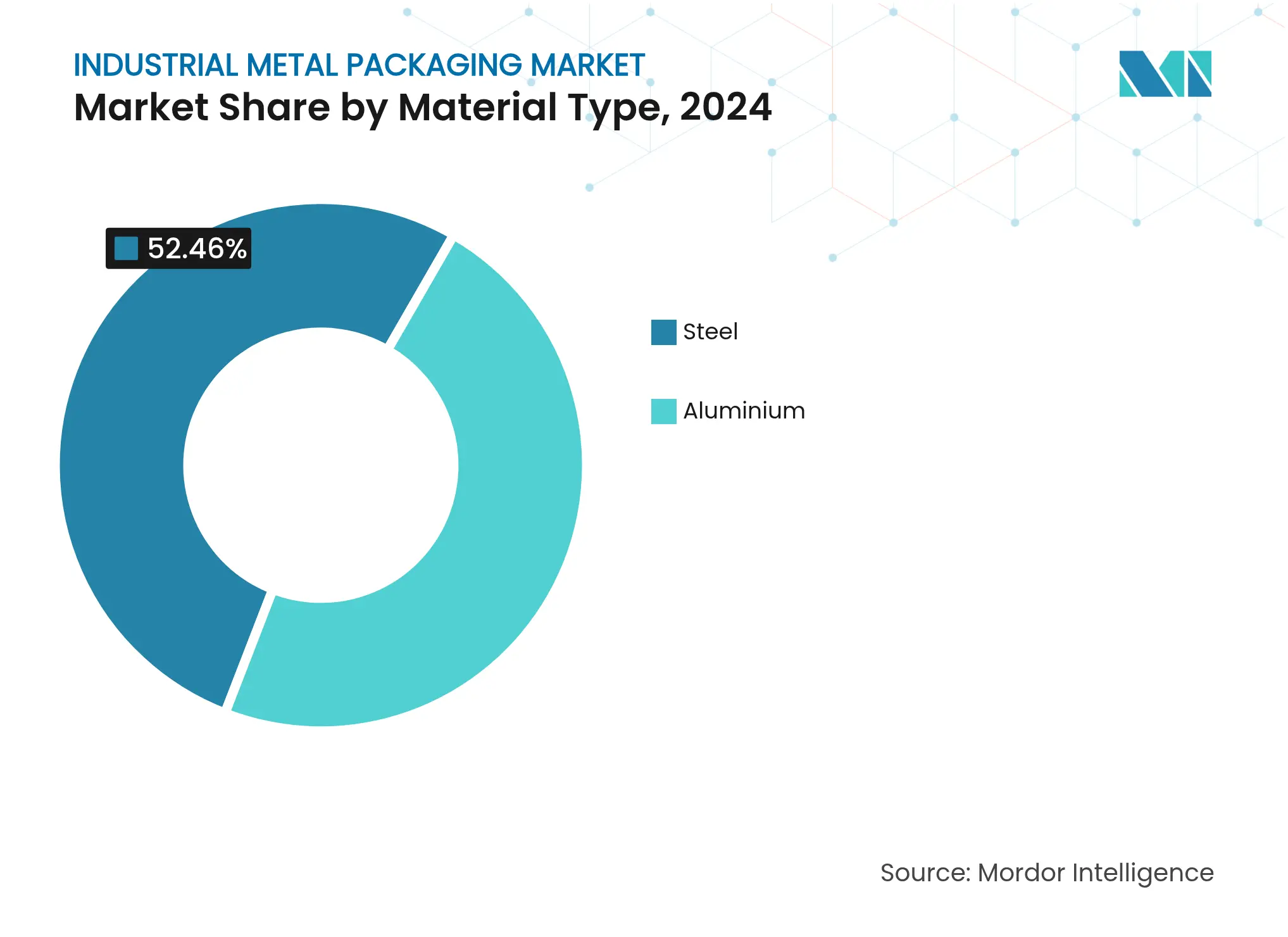

The industrial metal packaging market size reached USD 55.88 billion in 2025 and is forecast to hit USD 63.81 billion by 2030, translating to a steady 2.69% CAGR. This trajectory reflects mounting regulatory scrutiny, raw-material cost swings and new demand from hydrogen logistics and battery-recycling infrastructure. Across 2025, the market’s center of gravity is shifting toward high-pressure, sensor-enabled containers that help users trim mishandling risks and satisfy re-use mandates. Steel keeps the upper hand thanks to its 52.46% 2024 share and unmatched pressure tolerance, while aluminum adoption is curbed by tariffs that lifted unit costs 15–20% in North America. Intermediate Bulk Containers (IBCs) account for 41.67% of global unit demand, and the >1,000 L size band is expanding at a brisk 4.46% CAGR, signalling a clear tilt toward larger unit loads. Regionally, North America commands 32.56% of 2024 sales, but Asia-Pacific is scaling fastest at 6.72% CAGR, buoyed by India’s projected USD 1 trillion chemicals economy by 2040. End-use still leans on chemicals and petrochemicals at 41.35%, yet pharmaceuticals are gathering pace at 6.45% CAGR on the back of biologics capacity additions.

Key Report Takeaways

- By material type, steel led with 52.46% of industrial metal packaging market share in 2024, while its own sub-segment is forecast to grow 3.86% CAGR to 2030.

- By product type, IBCs commanded 41.67% revenue in 2024; shipping barrels and drums are set to post the quickest 5.34% CAGR through 2030.

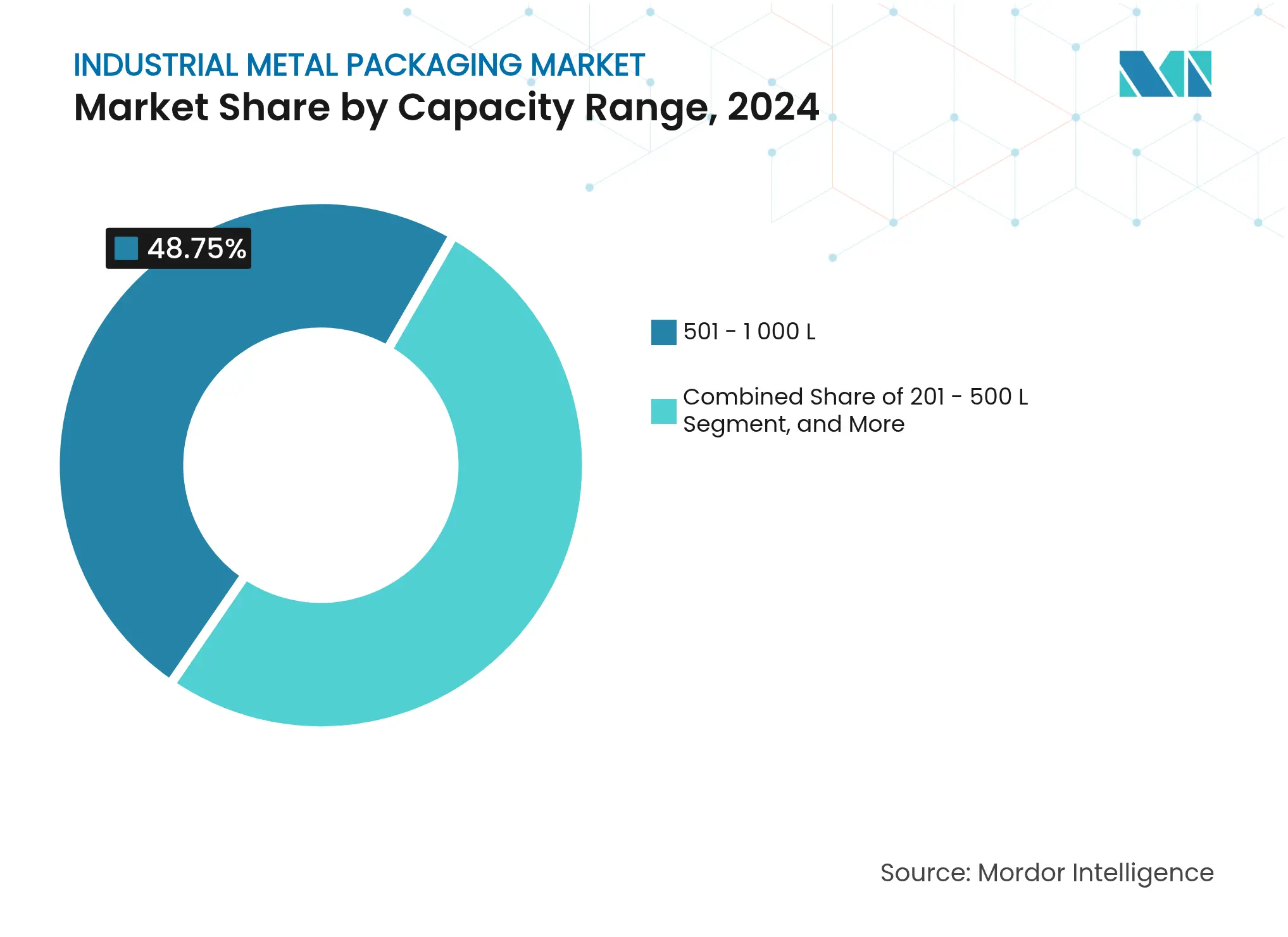

- By capacity, the 501–1,000 L range held 48.75% of industrial metal packaging market size in 2024, but containers above 1,000 L are advancing at a 4.46% CAGR.

- By end-user, chemicals and petrochemicals captured 41.35% share of the industrial metal packaging market size in 2024; pharmaceuticals are progressing at 6.45% CAGR through 2030.

- By geography, North America retained 32.56% of global revenues in 2024, whereas Asia-Pacific is forecast to enlarge its footprint at 6.72% CAGR.

Global Industrial Metal Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Bulk container demand for liquid transport

Bulk container demand for liquid transport

| +0.8% | North America, Europe (global spillover) | Medium term (2–4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

North America, Europe (global spillover)

|

Impact Timeline

:

Medium term (2–4 years)

|

New metal solutions for hazardous materials

New metal solutions for hazardous materials

| +0.6% | Global | Long term (≥ 4 years) | |||

Re-use and recyclability mandates

Re-use and recyclability mandates

| +0.5% | Europe, North America, expanding to APAC | Medium term (2–4 years) | |||

Liquid-hydrogen logistics

Liquid-hydrogen logistics

| +0.4% | North America, Europe, early Japan | Long term (≥ 4 years) | |||

Battery-recycling plant expansion

Battery-recycling plant expansion

| +0.3% | China, Europe, North America | Medium term (2–4 years) | |||

AI-enabled smart-drum rental models

AI-enabled smart-drum rental models

| +0.2% | North America, Europe, pilot APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing demand for bulk container packaging solutions for liquid transportation

Worldwide liquid supply chains now span biofuels, specialty chemicals and liquid hydrogen, all requiring containers that outperform historical petrochemical barrels. The shift to >1,000 L formats growing 4.46% annually underscores consolidation in liquid handling and favors IBCs engineered with IoT load sensors offering ±10% accuracy. Novelis’ multiyear sheet agreement with Ardagh underpins Alabama’s 600,000-ton aluminum plant dedicated to beverage and industrial packaging.

Innovation in metal packaging for storage of hazardous materials

Lithium-ion recycling and advanced chemistries are pushing UN-rated steel IBC demand as Veolia scales plants across three continents. Regulatory tightening, such as the 2024 PHMSA update on compressed-gas receptacles,[1]Federal Register, “Hazardous Materials: Advancing Safety…,” federalregister.gov triggers accelerated R&D in stainless grades resisting -253 °C hydrogen embrittlement.

Rising regulatory emphasis on re-use and recyclability mandates

The EU Packaging and Packaging Waste Regulation obliges full recyclability by 2030, pushing designers toward mono-material steel solutions. Ball targets 85% recycled content and already shipped 107 billion aluminum units in 2023. U.S. Extended Producer Responsibility rules taking force in 2025 project savings of USD 29.8 million each year by internalizing recycling costs.

Surge in liquid-hydrogen logistics requiring high-pressure steel drums

Liquid hydrogen transportation needs vessels validated to 700 bar and cryogenic integrity. Ovako’s Hofors plant uses a 20-MW electrolyzer and showcases fossil-free hydrogen’s industrial adoption. Austenitic stainless provides the ductility and leak-prevention baseline for this segment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Alternate packaging (plastic, composite IBC)

Alternate packaging (plastic, composite IBC)

| -0.7% | Global (cost-sensitive niches) | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Global (cost-sensitive niches)

|

Impact Timeline

:

Short term (≤ 2 years)

|

Volatile aluminum and steel prices

Volatile aluminum and steel prices

| -0.5% | Global, acute in North America | Short term (≤ 2 years) | |||

PFAS phase-out delaying fluorinated linings

PFAS phase-out delaying fluorinated linings

| -0.3% | Europe, North America, global extension | Medium term (2–4 years) | |||

EU data-privacy hurdles in smart tracking

EU data-privacy hurdles in smart tracking

| -0.2% | Europe, global spillover | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Presence of alternate packaging (plastic drums, composite IBCs)

Plastic drums combine lower weight and corrosion neutrality, tempting buyers in non-hazardous verticals. Composite IBCs blend steel cages with polymer inner tanks, trimming freight bills on long routes. Yet metal beats rivals in reuse cycles, high-pressure tolerance and established recycling loops, preserving its role in regulated chemicals.

Volatile aluminium and steel prices

Aluminum hovered near USD 2,600/ton, while steel ranged USD 800–1,000/ton in 2024–2025, squeezing margins and complicating price clauses. North American tariffs inflated costs an extra 15–20%, pushing buyers toward domestic mills or hedging contracts.

Segment Analysis

By Material Type: Steel dominance reinforced by hydrogen applications

Steel captured 52.46% of 2024 revenue, equating to the largest industrial metal packaging market share, and is tracking 3.86% CAGR toward 2030. The material remains critical for pressure vessels in hydrogen logistics, a use case expanding fastest within the industrial metal packaging market. Aluminum’s lighter weight offers freight benefits, but 2025 tariffs inflated delivered costs and shifted stationary storage buyers back to steel.

Recyclability mandates work in steel’s favor, because closed-loop scrap streams are mature inside Europe and North America. Outokumpu’s cryogenic-capable stainless grades extend steel containers into -253 °C hydrogen service, widening the industrial metal packaging market’s addressable high-pressure envelope.

By Product Type: IBCs lead through versatility and compliance

Intermediate Bulk Containers held 41.67% of 2024 turnover, leveraging global UN ratings that simplify cross-border hazmat shipments. Their 5.34% CAGR outpaces drums and barrels, ensuring the industrial metal packaging market remains anchored in modular bulk transport.

UN-rated steel IBCs are central to battery-recycling flows, as shown by Veolia’s investment across three regions. Consumer-oriented innovation also filters in: PepsiCo’s ingredient-chamber patent foreshadows more function-rich metal containers.

By Capacity Range: Large containers drive industrial consolidation

Units from 501–1,000 L delivered 48.75% of spending in 2024, slotting into automated warehouses and ISO container frames. In contrast, the >1,000 L class grows 4.46% each year, mirroring greenfield mega-plants in Asia that design material flow around fewer, larger handling steps.

IoT module cost dilution favors big containers, letting operators embed real-time fill and shock sensing at acceptable unit economics. Regulatory practice also supports larger drums by trimming human contact frequency during hazmat moves, aligning safety with productivity.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Pharmaceuticals accelerate despite chemical dominance

Chemicals and petrochemicals retained 41.35% share of 2024 demand, reaffirming their status as the industrial metal packaging market’s anchor vertical. Yet pharmaceuticals outstrip all other segments at a 6.45% CAGR, propelled by biologics output and more rigorous cold-chain standards.

India’s planned USD 1 trillion chemicals economy will elevate container pull-through, turbo-charging regional production linked to domestic PLI incentives. Coatings, adhesives and sealants for building sites also rely on metal pails where chemical compatibility is vital; Sherwin-Williams’ 2024 acquisition of Henkel’s coating line illustrates strategic positioning.

Geography Analysis

North America controlled 32.56% of global revenue in 2024, anchored by stringent DOT and PHMSA standards that reward high-grade metal containers. Crown Holdings lifted Q1 2025 EPS to USD 1.65 on strong beverage-can volumes and operational gains. Sonoco’s USD 3.9 billion Eviosys takeover cements a continent-wide platform capable of multi-country service.[2]Sonoco Products Company, “Sonoco Completes Acquisition of Eviosys,” sonoco.com Tariff-driven steel and aluminum inflation obliges procurement teams to hedge and localize supply where feasible.

Asia-Pacific is the industrial metal packaging market’s fastest climber at 6.72% CAGR. Chinese aluminum output hit 72.9 million tons in 2024, equivalent to nearly 60% of global smelter production. India’s chemical surge plus Vietnam and Indonesia’s burgeoning manufacturing ecosystems broaden regional container uptake. Japan and South Korea invest heavily in hydrogen pipelines, requiring specialty steel drums that meet 700 bar protocols.

Europe holds firm through advanced regulation and circular-economy orientation. The Packaging and Packaging Waste Regulation compels 100% recyclability, prompting widespread redesign toward monomaterial steel units. Ball’s Alucan buy added Spanish and Belgian factories to satisfy European beverage and industrial demand. The Middle East grows via petrochemical capacity while Africa leans on mining and infrastructure spending for bulk chemical storage. South America remains steady, with Brazil’s beverage-can uplift reflected in Crown Holdings’ earnings.

Competitive Landscape

Market Concentration

Industry consolidation is accelerating as leading suppliers lock in raw-material access and diversify regionally. Sonoco’s Eviosys integration creates a USD 7 billion revenue platform and the world’s largest metal food-can franchise. Ball’s North American network optimization, highlighted by the Florida Can Manufacturing purchase, boosts supply resilience and strip-out freight miles.[3]Ball, “Ball Corporation Further Optimizes North American Network…,” ball.com

Technology leadership is surfacing as a competitive wedge. Real-time condition monitoring and predictive maintenance lower lost loads, fostering sticky long-term contracts in the industrial metal packaging market. Patent filings—such as PepsiCo’s ingredient-chamber can—signal fresh consumer engagement angles translating to industrial formats.

Raw-material hedging and vertical integration remain pivotal. Silgan’s 90% contract coverage insulated its USD 3.1 billion 2023 Metal Containers division from commodity swings. Novelis grew FY 2025 net income 14% to USD 683 million despite elevated scrap prices, underscoring how scale and recycling know-how underpin margins.

Industrial Metal Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Novelis posted FY 2025 net income of USD 683 million, up 14% year-over-year.

- April 2025: Crown Holdings raised full-year EPS guidance after Q1 2025 diluted EPS hit USD 1.65.

- March 2025: Ovako commissioned a 20-MW electrolyzer to create fossil-free hydrogen for steel heating.

- February 2025: Ball bought Florida Can Manufacturing to sharpen North American supply efficiency.

Table of Contents for Industrial Metal Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing demand for bulk container packaging solutions for liquid transportation

- 4.2.2Innovation in metal packaging for storage of hazardous materials

- 4.2.3Rising regulatory emphasis on re-use and recyclability mandates

- 4.2.4Surge in liquid-hydrogen logistics requiring high-pressure steel drums

- 4.2.5Expansion of battery-recycling plants needing UN-rated steel IBCs

- 4.2.6AI-enabled smart-drum rental models lowering total cost of ownership

- 4.3Market Restraints

- 4.3.1 Presence of alternate packaging (plastic drums, composite IBCs)

- 4.3.2Volatile aluminium and steel prices

- 4.3.3PFAS phase-out delaying fluorinated drum linings

- 4.3.4EU data-privacy rules complicating smart-container tracking

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

- 4.8Impact of Geopolitical Scenario on the Market

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material Type

- 5.1.1Aluminium

- 5.1.2Steel

- 5.2By Product Type

- 5.2.1Intermediate Bulk Containers (IBCs)

- 5.2.2Shipping Barrels and Drums

- 5.2.3 Bulk Containers (Pails, Kegs, etc.)

- 5.3By Capacity Range

- 5.3.1 ≤200 L

- 5.3.2 201 – 500 L

- 5.3.3 501 – 1 000 L

- 5.3.4 >1 000 L

- 5.4By End-user Industry

- 5.4.1Food and Beverage

- 5.4.2Chemicals aand Petrochemicals

- 5.4.3Pharmaceuticals

- 5.4.4Building and Construction

- 5.4.5Other End-user Industry

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Greif Inc.

- 6.4.2Mauser Packaging Solutions

- 6.4.3Balmer Lawrie & Co. Ltd

- 6.4.4 ENVASES Öhringen GmbH

- 6.4.5 SCHÄFER Werke GmbH

- 6.4.6Sicagen India Ltd

- 6.4.7Time Mauser Industries Pvt Ltd

- 6.4.8THIELMANN Portinox Spain SA

- 6.4.9Snyder Industries Inc.

- 6.4.10American Keg Co. (BLEFA Beverage Systems)

- 6.4.11Lancaster Container Inc.

- 6.4.12P. Wilkinson Containers Ltd

- 6.4.13Bison IBC Ltd

- 6.4.14Colep Packaging (RAR Group)

- 6.4.15Peninsula Drums

- 6.4.16JFE Container Co. Ltd

- 6.4.17CPMC Holdings Ltd

- 6.4.18Ardagh Metal Packaging SA

- 6.4.19Crown Holdings Inc.

- 6.4.20Ball Corporation

- 6.4.21Tata Steel Packaging

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Industrial Metal Packaging Market Report Scope

For storage and transportation, industrial metal packaging includes bulk packaging solutions such as drums, IBCs, and other bulk containers made from steel or aluminum. These solutions provide exceptional durability and protection, making them the preferred container for industries that prioritize product integrity.

The industrial metal packaging market is segmented by material type (aluminum and steel), product type (IBCs, shipping barrels and drums, and bulk containers [pails and kegs]), end-user industry (food & beverage, chemicals and pharmaceuticals, oil and petrochemicals, building and construction, and automotive), and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, Spain, and Rest of Europe], Asia-Pacific [China, Japan, India, Vietnam, Thailand, Australia and New Zealand, and Rest of Asia Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [Saudi Arabia, South Africa, Egypt, United Arab Emirates, and Rest of the Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.