FMCG Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

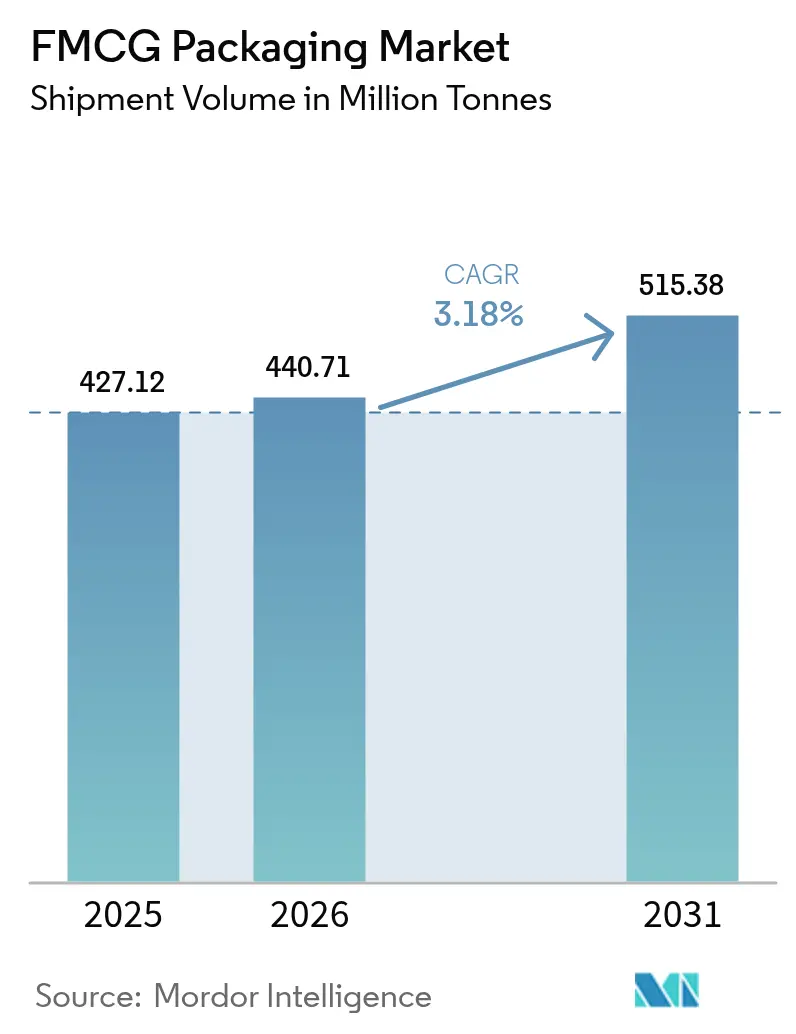

| Market Volume (2026) | 440.71 Million tonnes |

| Market Volume (2031) | 515.38 Million tonnes |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

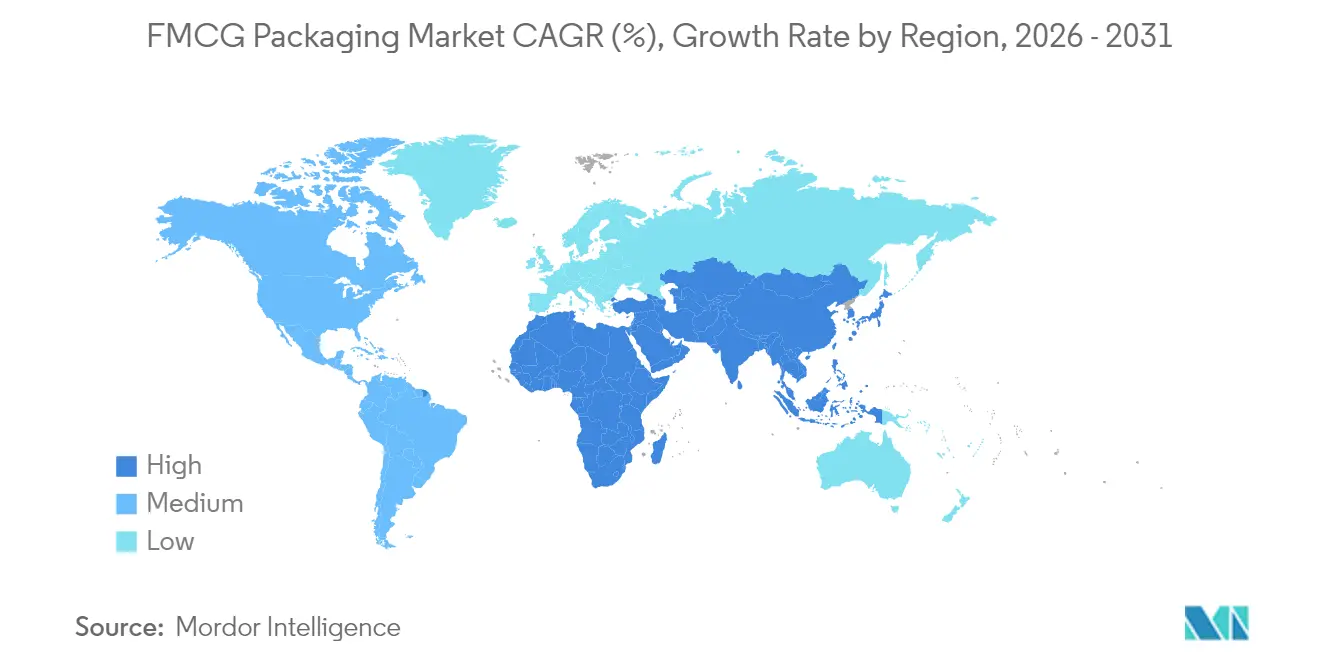

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

FMCG Packaging Market Analysis by Mordor Intelligence

The FMCG packaging market size was valued at 427.12 million tonnes in 2025 and estimated to grow from 440.71 million tonnes in 2026 to reach 515.38 million tonnes by 2031, at a CAGR of 3.18% during the forecast period (2026-2031). Growth rests on steady household demand for packaged essentials, expanding e-commerce volumes, and policy measures that reward recyclable and refillable solutions. Large converters are redesigning formats to trim material use and freight costs while protecting goods that travel through longer, more complex supply chains. Bio-based substrates and chemical-recycled resins are moving from pilot to commercial scale, yet plastics remain indispensable in high-barrier and lightweight roles. Regional demand is led by Asia-Pacific thanks to rapid urbanization and small-household purchasing, while Middle East and Africa (MEA) offers the quickest tonnage expansion as modern retail spreads.

Key Report Takeaways

- By region, Asia-Pacific held 45.21% FMCG packaging market share in 2025; MEA is projected to grow at a 6.48% CAGR to 2031.

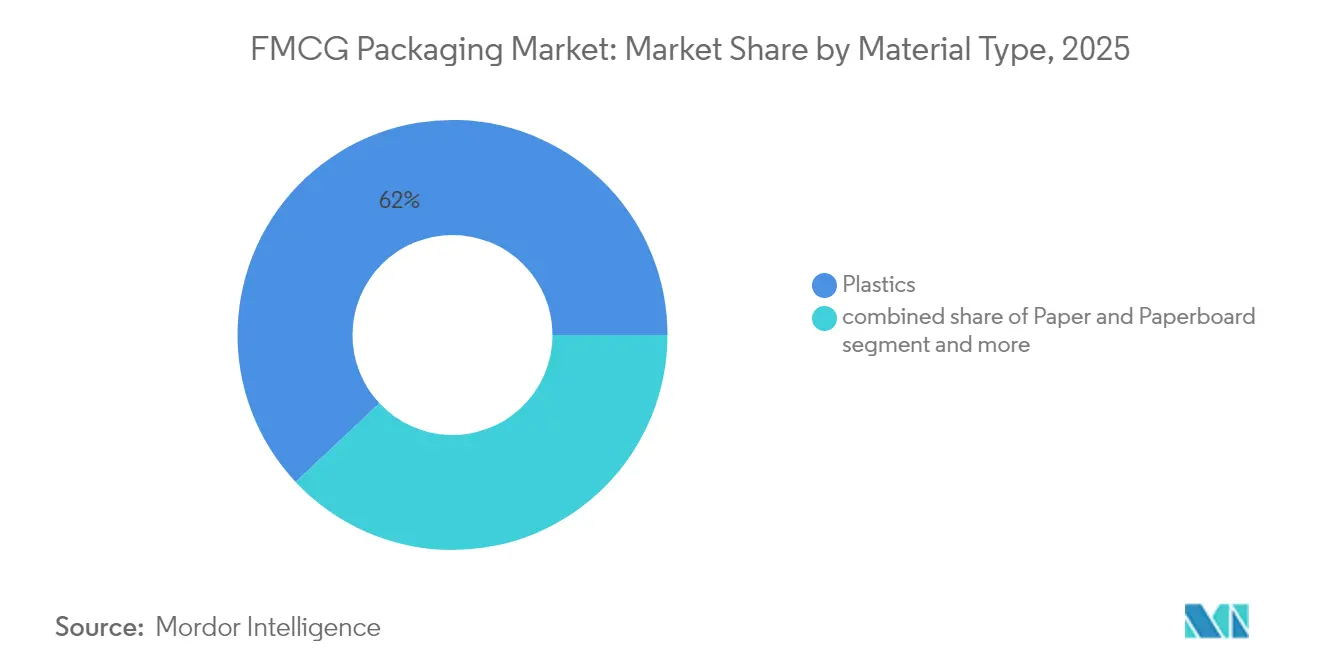

- By material type, plastics commanded 61.98% of the FMCG packaging market size in 2025; bio-based and compostable materials are set to expand at 6.73% CAGR through 2031.

- By packaging type, flexible formats led with 54.12% revenue share in 2025, whereas the same segment is forecast to post a 6.22% CAGR to 2031.

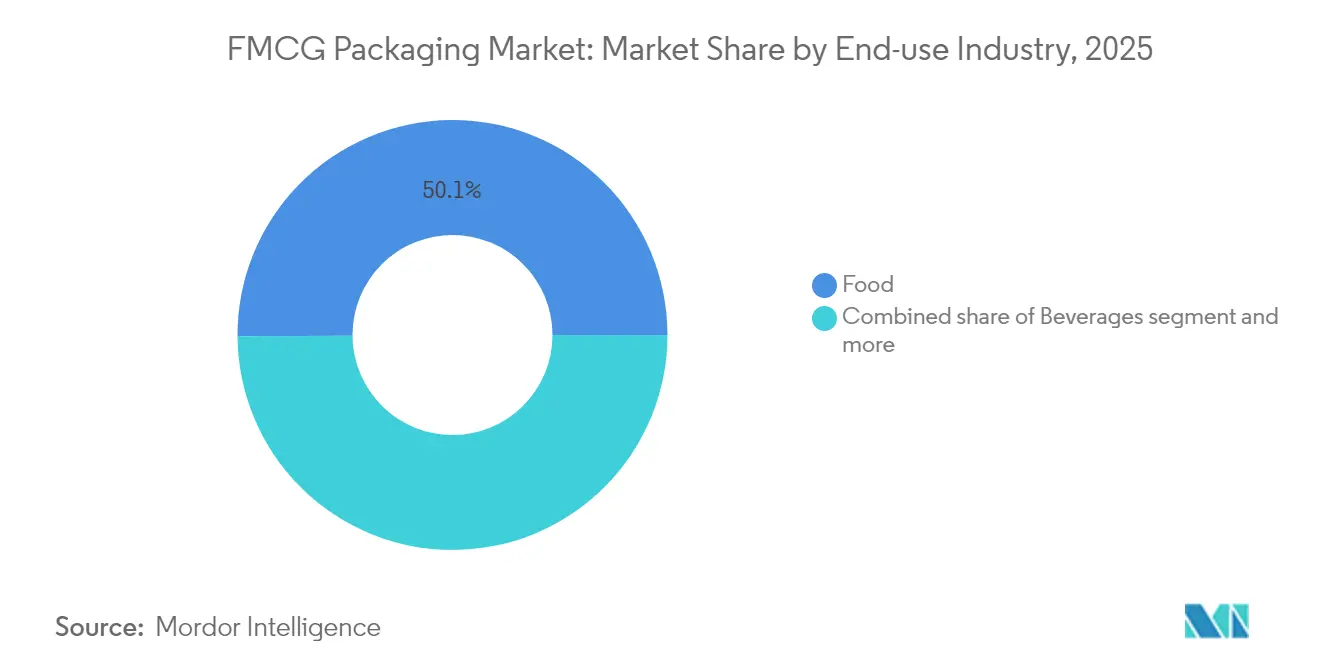

- By end-use industry, food accounted for 50.10% share of the FMCG packaging market size in 2025, while pharmaceuticals and healthcare are advancing at 5.43% CAGR to 2031.

- By distribution channel, direct sales represented 55.92% of 2025 revenue; indirect sales are forecast to rise at a 4.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global FMCG Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of E-commerce Requiring Protective, Lightweight Packs | 0.8% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Urban Single-Serve Consumption Boom in Asia Boosting Convenience Formats | 0.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| RTD Beverage Surge Driving High-Barrier Pouch Adoption | 0.6% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Premiumisation in Personal-Care Triggering Smart and Decorative Packs | 0.5% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Cold-Chain Expansion in Emerging Markets Raising Multilayer Film Usage | 0.4% | APAC & MEA, with selective Latin America penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of E-commerce Requiring Protective, Lightweight Packs

Online retail now frames design briefs around parcel durability, dimensional weight limits, and friction-free returns. Brand owners specify cushioned mailers, air-column pouches, and fit-to-size cartons that slash void space and freight spend. Packaging plants add digital print lines so each shipper can carry scannable codes that confirm authenticity or trigger replenishment services. Smart indicators that reveal impact or temperature misuse are becoming standard on premium categories, a trend reinforced by parcel insurers who offer lower premiums for traceable packs. These needs keep flexible films and corrugated board in high demand and encourage resin suppliers to accelerate drop-in recycled grades that retain mechanical properties. [1]Source: Packaging Dive, “Green Bay Packaging to invest $1B in Arkansas kraft linerboard mill,” packagingdive.com

Urban Single-Serve Consumption Boom in Asia Boosting Convenience Formats

Rising numbers of single-person households and congested commutes in China, India, and Southeast Asia spur uptake of portion-controlled pouches, cups, and sachets. Manufacturers are automating high-speed fill-seal lines to reach price points competitive with bulk packs while trimming food waste from partially used larger units. Retailers dedicate premium shelf space to resealable snack packs and ready-to-eat meals sized for one, pushing converters to enhance barrier layers that keep contents fresh until the last serving. Growth spills into home-care and personal-care items, where refill pods and travel-friendly minis fit hectic urban lifestyles. Demand for laminates that couple easy-tear openings with drop-resistance underpins a notable slice of incremental Asian capacity additions.

RTD Beverage Surge Driving High-Barrier Pouch Adoption

Functional and dairy-alternative drinks thrive on convenience and ambient stability. To lock in flavor and nutrients without refrigeration, producers specify multilayer films with oxygen-scavenging layers and aluminum-free barriers compatible with recycling streams. The format also supports cold-chain expansion in emerging markets, where reliable chillers remain scarce. Brand owners experiment with spout-pouches that allow on-the-go sipping, and digital inks enable limited-edition graphics that build social-media buzz. Equipment suppliers respond with modular filling systems that swap between metallized and transparent webs, granting operational flexibility amidst SKU proliferation. Resulting demand lifts orders for EVOH and bio-based tie-layers across Europe and North America.

Premiumisation in Personal-Care Triggering Smart and Decorative Packs

Skin-care, hair-care, and fragrance brands compete on shelf presence, prompting intricate embossing, metallization, and connected-pack features that tell ingredient provenance stories. NFC tags let consumers check product authenticity or engage in loyalty programs, while light-weight glass-look PET bottles lower carbon footprints versus traditional flint glass. Luxury labels still insist on tactile closures and matte soft-touch labels; suppliers therefore co-develop recyclable over-sleeves and water-based varnishes that achieve premium aesthetics without foil laminates. Growing male grooming segments in Western Europe and the US adopt functional airless pumps that protect sensitive active ingredients, further lifting demand for multilayer polypropylene components

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resin Price Volatility Creating Planning Uncertainty | -0.4% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

| Recycling-Infrastructure Deficit in Developing Nations | -0.3% | APAC & MEA emerging markets, selective Latin America | Long term (≥ 4 years) |

| Single-Use-Plastic Bans Dampening Conventional Flexibles | -0.2% | Europe & select North American jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resin Price Volatility Creating Planning Uncertainty

Fluctuating crude-oil and naphtha benchmarks upset quarterly contract negotiations, prompting converters to hedge feedstock or accelerate substitution toward recycled and bio-based grades. Smaller firms lacking scale struggle to absorb spikes, which compress margins and slow capital investment. Sudden shortages of specialty additives, often linked to geopolitical events, force ad-hoc reformulations that risk downtime and customer penalties. In response, multinationals diversify sourcing and lock in multi-year supply pacts, while financial teams roll out cost-pass-through clauses keyed to industry indices. Such turbulence favors producers with integrated resin assets and strong working-capital positions.

Single-Use-Plastic Bans Dampening Conventional Flexibles

Europe’s Packaging and Packaging Waste Regulation mandates recyclability and minimum recycled content, pushing PVC shrink sleeves and PS yogurt cups toward phase-out. Parallel schemes in the United Kingdom introduce disposal fees that penalize hard-to-recycle laminates. Brand owners pivot to mono-material PE or PP films, but doing so can raise oxygen ingress, thereby demanding improved barrier coatings. Retailers add “recycle-ready” scorecards to vendor audits, elevating the strategic importance of design-for-recycling. While the rules squeeze margins on conventional flexibles, they create a runway for papers with dispersion barriers, compostable films, and refill systems now trialing across grocery chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Dominance Faces Sustainable Disruption

Plastics maintained a 61.98% share of the FMCG packaging market in 2025, reflecting unmatched strength-to-weight ratios and broad processability. Bio-based and compostable grades, though still niche, are expanding at 6.73% CAGR as converters commercialize PLA and PHA blends with enhanced oxygen and moisture barriers. Rigid metals find favor in premium beverage lines for infinite recyclability, and paperboard gains share where dry food or personal-care formats permit fiber-based walls. The FMCG packaging market continues to favor polyethylene and polypropylene in flexible laminates thanks to cost efficiency, but chemical recycling, now scaling in North America and Europe, promises high-quality post-consumer resins that moderate virgin demand. Innovations in reactive coating lines let paper cups hold acidic juices without plastic liners, opening another pathway for plastics displacement.

Plastics suppliers counter sustainability pressures by launching certified-circular PE and PP grades derived from pyrolysis oil, giving brand owners a drop-in route to lower emissions while retaining incumbent converting lines. The FMCG packaging market size for bio-based resins is projected to surpass 8.23 million tonnes by 2031 as governmental green-procurement rules take hold. Meanwhile, aluminum’s light-weight advantage in aerosol cans and pet-food trays aligns with refill stations that prefer robust formats surviving multiple cycles. Glass stays relevant where taste neutrality is prized, yet weight and breakage limit its volume share. Overall, material choice now hinges on balancing functional performance, regulatory compliance, and total carbon impact rather than unit price alone.

By Packaging Type: Flexible Solutions Drive Innovation

With a 54.12% share in 2025, flexible formats dominate the FMCG packaging market and are tracking a 6.22% CAGR to 2031. Brand owners value lower material-to-product ratios, high graphics potential, and pack-out efficiency that allows more units per pallet. The shift to e-commerce adds demand for mail-friendly pillow packs and multi-layer sachets that endure automated sortation without extra void fill. Continuous-motion horizontal form-fill-seal (HFFS) lines supply snack and confectionery categories at speeds exceeding 1,500 packs per minute, highlighting the operational gains that recursive format optimisation delivers.

Rigid options still command niches where structure and reclosability are critical. PET bottles retain leadership in carbonated soft drinks, while glass jars project premium cues in gourmet sauces. Hybrid “rigid-in-flexible” pouch designs with molded caps combine both worlds, slicing weight by up to 70% versus equivalently sized glass containers. The FMCG packaging market size for rigid formats is forecast to post low-single-digit growth, reflecting saturation in mature categories but fresh opportunities in refillable personal-care dispensers. Equipment builders now offer modular filler blocs that handle fitment pouches, jars, and bottles on one line, letting converters hedge against demand swings across formats.

By End-use Industry: Food Dominance Meets Pharma Growth

Food applications generated 50.10% of 2025 tonnage as grocery chains push longer ambient shelf life to curb shrink. Active-ingredient sachets that absorb oxygen, or liner sheets infused with antimicrobial agents, illustrate how packaging anchors waste-reduction strategies. Beverage players upgrade to aseptic cartons and retort pouches to tap rising demand for dairy alternatives and functional drinks that must remain stable without cold-chain. The FMCG packaging market size for pharmaceuticals and healthcare is expanding at 5.43% CAGR, propelled by insulin, vaccine, and biosimilar launches that impose strict sterility and traceability needs.

Cold-chain investments in Asia and MEA elevate multilayer films that manage moisture while permitting rapid heat transfer in blast freezers. In parallel, personal-care launches embrace airless pumps and mini tubes tailored to travel restrictions and subscription services. Household-care concentrates in refill pouches lower plastic use and shipping weight, aligning with corporate carbon pledges. Across industries, smart labels that log temperature or tampering events provide extra assurance for regulators and insurers. These converging trends encourage converters to widen material portfolios and co-develop applications with brand R&D teams.

By Distribution Channel: Direct Sales Evolve Toward Omnichannel

Direct sales captured 55.92% of 2025 volume as global FMCG groups relied on long-term supply contracts with integrated packaging majors. These ties favor joint innovation on machinery upgrades and closed-loop resin sourcing. Nevertheless, the FMCG packaging market sees indirect channels—distributors, printers, and online brokers—accelerating at 4.53% CAGR as small and medium brands outsource purchasing to concentrate on marketing. E-commerce marketplaces specify frustration-free guidelines that strip away excess layers and replace gloss laminates with mono-material films.

Omnichannel fulfillment requires packs that navigate warehouse automation yet deliver an engaging unboxing moment on arrival. Hence liners, tear tapes, and self-sealing flaps become critical functional add-ons. Third-party logistics providers increasingly bundle kitting and custom printing, shifting some influence over packaging specifications downstream. The FMCG packaging industry therefore invests in cloud platforms that link artwork revision, ordering, and tracking so that every stakeholder works off the same data set. Over the forecast period, competition between direct and indirect routes will hinge on service flexibility as much as on unit cost.

Geography Analysis

Asia-Pacific generated 45.21% of 2025 shipments, positioning the region as the anchor of the FMCG packaging market. China and India supply mammoth domestic demand and serve export flows, leveraging clusters of integrated resin crackers, film extruders, and converting plants. Urban micro-kitchens and on-the-go eating habits fuel single-serve pouch uptake, while national plastic-reduction mandates accelerate trials of paper-based flexibles. Rising disposable incomes enable trading-up to premium personal-care formats, deepening per-capita packaging intensity. Government-backed cold-chain corridors in India and Southeast Asia unleash further need for insulated shippers and tamper-evident seals.

North America follows with a stable share rooted in broad e-commerce penetration and advanced corrugated capacity. The Smurfit-WestRock merger, valued at USD 20 billion, exemplifies the push for scale to dilute fixed costs and fund circular-economy R&D. Investments such as Green Bay Packaging’s USD 1 billion kraft linerboard mill in Arkansas strengthen domestic supply security and expand lightweight liner offerings. United States state regulations on recycled content in beverage containers catalyze PET reclaim projects, pushing local converters to lock in rPET feedstock. Canada and Mexico gain from near-shoring that relocates consumer-goods filling lines closer to core demand.

Europe’s mature market taps innovation to meet its stringent recyclability targets under the Packaging and Packaging Waste Regulation. Germany and France upgrade MRFs and chemical-recycling pilots to satisfy minimum recycled-content thresholds, while brand owners redesign individual packs to pass “sort-ability” tests. Premium confectionery chooses fiber-based wrapping with bio-barriers, and UK supermarkets roll out refill trials that test shopper uptake of returnable pouches. These initiatives stabilize overall tonnage but shift value toward higher-spec materials and linked digital services.

Middle East and Africa register the fastest 6.48% CAGR, albeit from a lower base, as organized retail expands and population growth drives packaged staples. Gulf states invest in state-of-the-art flexible plants that supply both domestic fast-food chains and export orders. South Africa and Kenya attract mobile filling units for milk and juice cartons that extend shelf life in areas lacking refrigeration. Foreign direct investment from European and Asian groups introduces multilayer extrusion technology, lifting local capabilities.

South America offers steady upside as economic reforms in Brazil and Colombia revive consumer spending. Regional fiber availability supports cost-competitive corrugated, and sugar-cane-based bio-PE capacity in Brazil gives global brands a renewable-content narrative. Tariff structures still influence plant-location decisions, nudging converters to adopt multinational footprints that straddle Mercosur and Pacific Alliance blocs.

Competitive Landscape

The FMCG packaging market remains fragmented with numerous regional specialists. The Smurfit-WestRock tie-up combines boxboard, corrugated, and containerboard assets across four continents, aiming to unlock logistics and R&D synergies. Kimberly-Clark’s USD 2 billion multi-site US expansion demonstrates how brand owners vertically integrate select packaging lines to safeguard supply and accelerate innovation. Meanwhile, Hotpack Global’s USD 100 million New Jersey plant exemplifies foreign entrants establishing local manufacturing to shorten lead times and reduce currency risk.

Technology leadership drives differentiation. American Packaging Corporation’s Utah Center of Excellence houses proprietary flexographic presses that deliver short-run, high-graphic pouches suited to personalized marketing. Graphic Packaging’s fully automated Texas facility integrates AI-driven quality control, trimming waste and energy use while shortening order-to-ship cycles. Active patenting in barrier chemistries and digital watermarking signals ongoing rivalry in both material science and data-rich traceability.

Sustainability pressures open lanes for smaller innovators. Lactips’ water-soluble films and start-ups offering paper-based spouted pouches secure pilot programs with multinational beverage groups. Chemical-recycler partnerships between resin majors and waste-management firms promise near-virgin quality recyclate, a capability likely to redraw supplier hierarchies once commercial scale is reached. Over the outlook period, successful players will marry circular-design credentials with cost-efficient global networks.

FMCG Packaging Industry Leaders

Amcor plc

Ball Corporation

Mondi Group

Sealed Air Corporation

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Green Bay Packaging invested USD 1 billion to expand its Arkansas kraft linerboard mill, adding high-efficiency boilers and doubling lightweight liner capacity

- June 2025: Tetra Pak and Cayuga Milk Ingredients completed a USD 270 million aseptic-packaging expansion in New York, creating 150 jobs and adding shelf-stable carton capability

- May 2025: Hotpack Global confirmed a USD 100 million plant in New Jersey to produce sustainable disposables for North American food-service markets

- May 2025: Kimberly-Clark outlined a USD 2 billion US manufacturing build-out, including a new Ohio facility and South Carolina upgrades, projected to create 900 skilled roles

Global FMCG Packaging Market Report Scope

The FMCG packaging market centers on crafting and supplying packaging solutions for Fast-Moving Consumer Goods (FMCG). These goods encompass everyday essentials like food, beverages, personal care items, household products, and over-the-counter healthcare items, frequently purchased at relatively low costs. Packaging is vital for safeguarding and preserving products, branding, marketing, and regulatory standards. Consumer behavior trends, technological advancements, sustainability regulations, and the demand for innovative and convenient packaging solutions drive the market.

The FMCG packaging market is segmented by material type (paper and paperboard, plastic, metal, and glass), by application (food, beverages, cosmetics and personal care, pharmaceuticals, and household care and other applications), and by Geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, Spain, and Rest of Europe], Asia [China, India, Japan, South Korea, Australia and New Zealand and Rest of Asia], (Latin America [Brazil, Mexico, Columbia and Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of the Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Paper and Paperboard | |

| Plastics | Polyethylene (LDPE/HDPE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Other Plastics (PVC, PS,etc) | |

| Metal | |

| Glass | |

| Bio-based and Compostable Materials |

| Flexible Packaging | Pouches and Bags |

| Films and Wraps | |

| Other Flexible Packaging | |

| Rigid Packaging | Bottles and Jars |

| Cans | |

| Trays and Containers | |

| Other Rigid Packaging |

| Food |

| Beverages |

| Personal Care and Cosmetics |

| Household Care Products |

| Pharmaceuticals and Healthcare |

| Other End-use Industry |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Paper and Paperboard | ||

| Plastics | Polyethylene (LDPE/HDPE) | ||

| Polypropylene (PP) | |||

| Polyethylene Terephthalate (PET) | |||

| Other Plastics (PVC, PS,etc) | |||

| Metal | |||

| Glass | |||

| Bio-based and Compostable Materials | |||

| By Packaging Type | Flexible Packaging | Pouches and Bags | |

| Films and Wraps | |||

| Other Flexible Packaging | |||

| Rigid Packaging | Bottles and Jars | ||

| Cans | |||

| Trays and Containers | |||

| Other Rigid Packaging | |||

| By End-use Industry | Food | ||

| Beverages | |||

| Personal Care and Cosmetics | |||

| Household Care Products | |||

| Pharmaceuticals and Healthcare | |||

| Other End-use Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current FMCG packaging market size?

The FMCG packaging market reached 440.71 million tonnes in 2026 and is projected to hit 515.38 million tonnes by 2031.

Which region leads the FMCG packaging market?

Asia-Pacific leads with 45.21% share in 2025 due to its large consumer base and manufacturing scale.

What material dominates global FMCG packaging demand?

Plastics account for 61.98% of 2025 volume, although bio-based alternatives show the fastest growth.

Which packaging format is growing quickest?

Flexible packaging is expanding at a 6.22% CAGR, driven by material efficiency and e-commerce suitability.

Why is the pharmaceutical sector important for future growth?

Cold-chain expansion and stricter regulatory needs push pharmaceutical and healthcare demand at a 5.43% CAGR through 2031.

Page last updated on: