North America Rigid Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

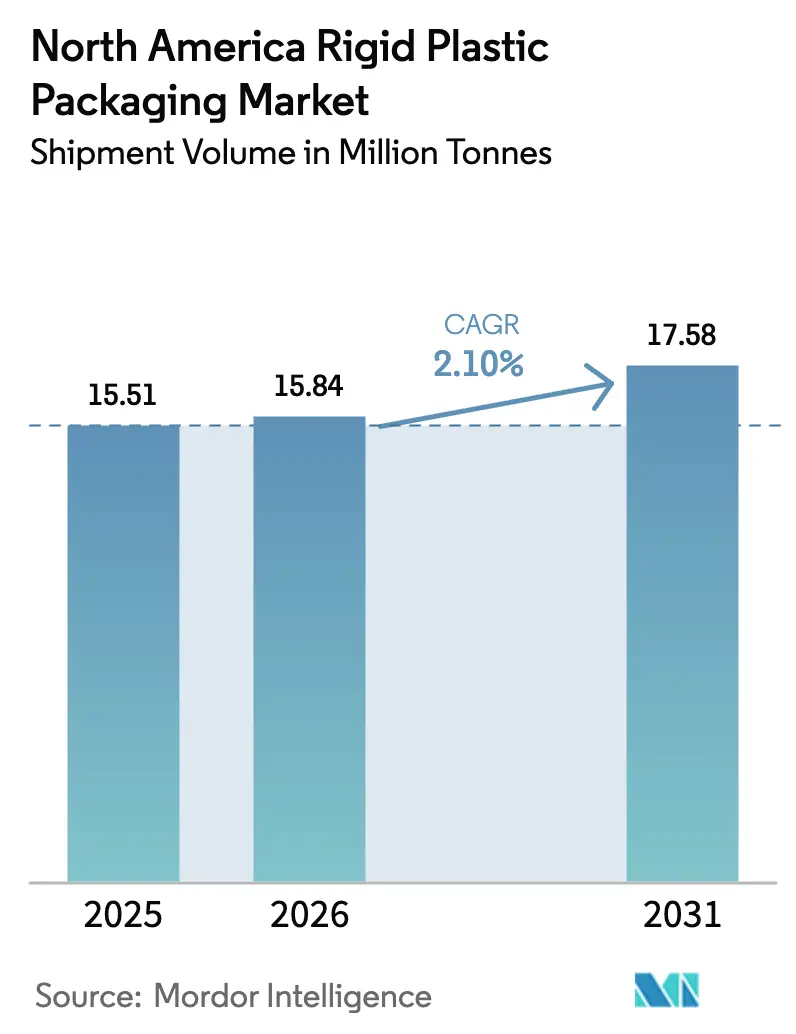

| Base Year Market Size (2025) | 15.51 Million tonnes |

| Market Volume (2026) | 15.84 Million tonnes |

| Market Volume (2031) | 17.58 Million tonnes |

| Growth Rate (2026 - 2031) | 2.10% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Rigid Plastic Packaging Market Analysis by Mordor Intelligence

The North America rigid plastic packaging market size is expected to grow from 15.51 million tonnes in 2025 to 15.84 million tonnes in 2026 and is forecast to reach 17.58 million tonnes by 2031 at 2.10% CAGR over 2026-2031. Petrochemical capacity reallocations from fuels to polymers are lowering resin input costs, enabling producers to defend margins even as sustainability and regulatory pressures intensify. Brand-owner commitments to higher recycled content, rapid e-commerce adoption, and automation investments in molding lines collectively sustain moderate tonnage growth. Competitive dynamics remain fragmented because mid-sized converters retain strong customer relationships, while multinationals press scale advantages in feedstock sourcing and technology deployment. Across end-user sectors, beverages, food, and pharmaceuticals dominate demand, yet growth accelerates most sharply in healthcare packaging as biologics and specialty drugs proliferate.

Key Report Takeaways

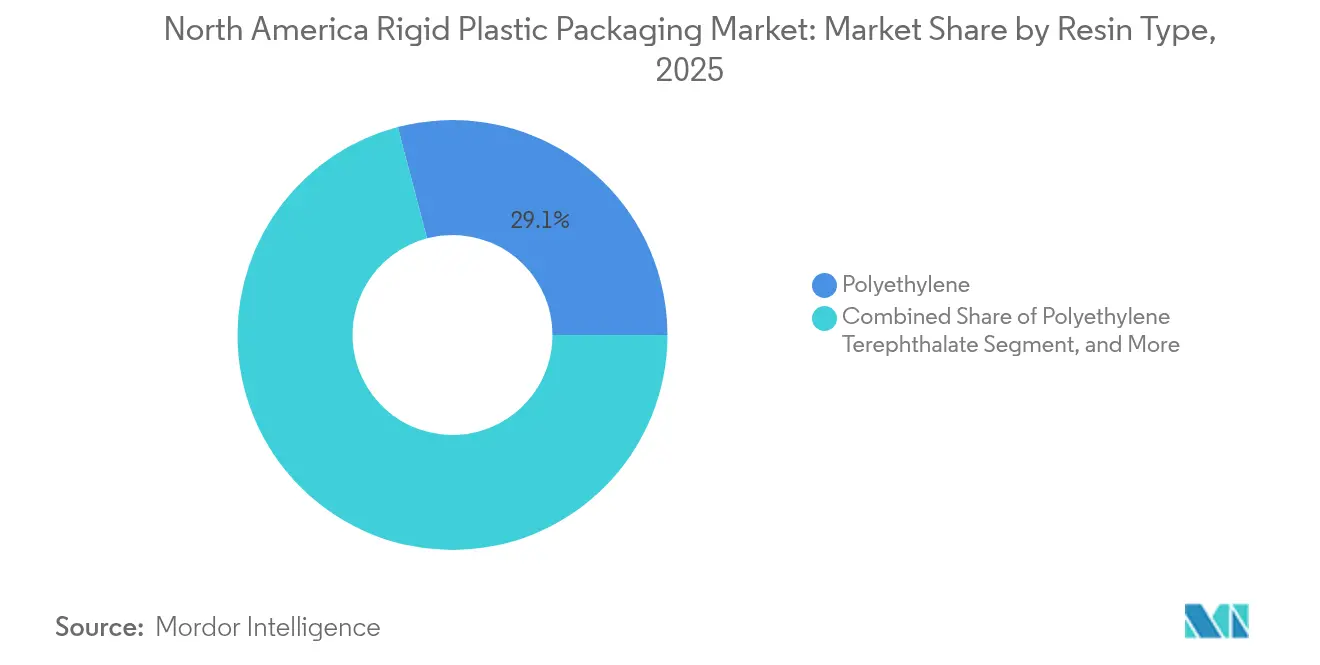

- By resin type, polyethylene held 29.10% of the North America rigid plastic packaging market share in 2025; polyethylene terephthalate is advancing at a 3.72% CAGR through 2031.

- By product type, bottles and jars captured 45.10% revenue share in 2025; caps and closures are forecast to expand at a 3.1% CAGR to 2031.

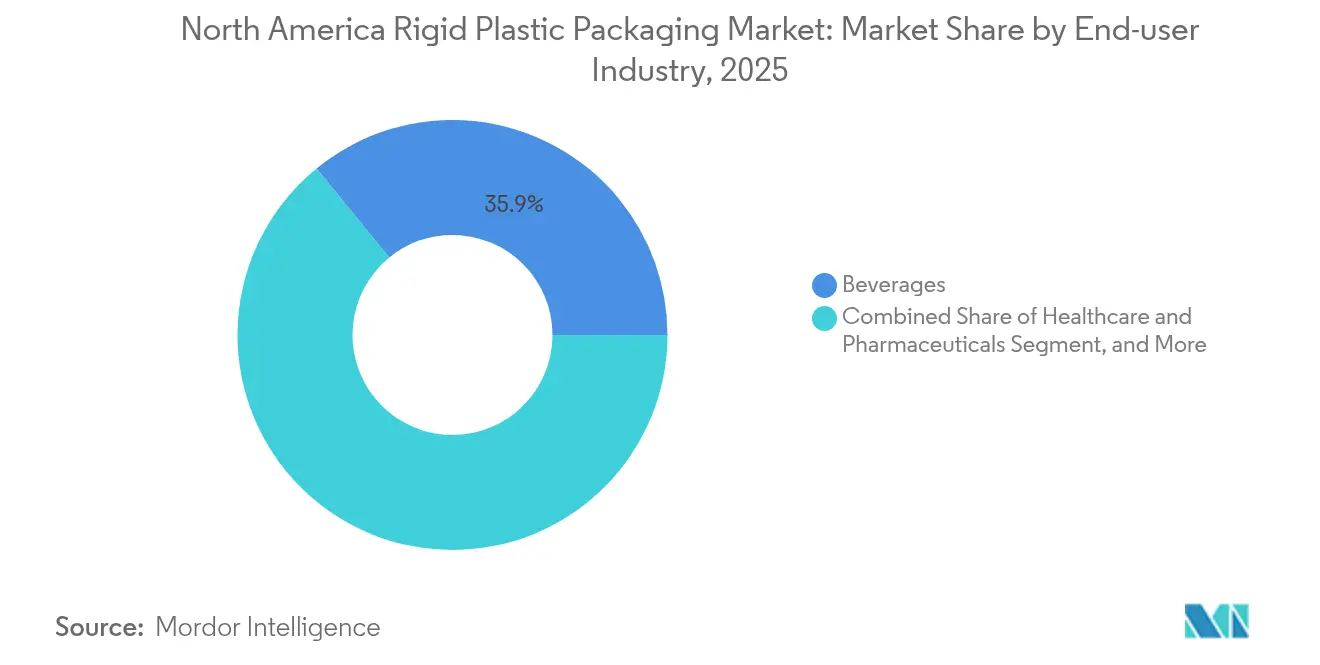

- By end-user industry, beverages led with 35.90% of the North America rigid plastic packaging market size in 2025; healthcare and pharmaceuticals are growing fastest at 4.74% CAGR through 2031.

- By manufacturing process, injection molding accounted for 25.40% share in 2025; thermoforming posts the highest projected CAGR at 3.6% to 2031.

- By country, the United States dominated with 71.10% share in 2025, while Mexico records the highest 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing FMCG penetration boosts demand | +0.8% | North America, strongest in Mexico and US South | Medium term (2-4 years) |

| PET bottle sustainability programs accelerate rPET procurement | +0.6% | US and Canada, regulatory-driven | Long term (≥ 4 years) |

| Expansion of e-commerce and D2C channels raises protective-packaging needs | +0.4% | North America, urban concentration | Short term (≤ 2 years) |

| FDA migration-limit revisions spur barrier-coating investments | +0.3% | US market, food contact applications | Medium term (2-4 years) |

| AI-enabled defect-detection lowers scrap rates and widens profit pools | +0.2% | US and Canada, technology-advanced facilities | Long term (≥ 4 years) |

| NA petro-chemical capacity shift from fuels to polymers keeps resin prices competitive | +0.1% | North America, Gulf Coast concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing FMCG Penetration Drives Volume Expansion

Rising disposable income and urbanization in Mexico and the US South are broadening modern retail footprints and lifting demand for packaged food and beverages. National convenience-store chains drive high product turnover, requiring rigid containers that protect freshness during longer shelf cycles.[1]U.S. Census Bureau, “Economic Census Manufacturing Data,” CENSUS.GOV Brand owners favor polyethylene and polypropylene bottles for oil, sauces, and household goods because material cost stability supports predictable unit economics. Large retailers also promote private-label ranges, stimulating smaller production runs that benefit from flexible injection and blow-molding equipment. The combined effect of more SKUs and higher per-capita consumption underpins baseline growth in the North America rigid plastic packaging market. FMCG penetration therefore offsets sluggish demand in mature categories such as carbonated soft drinks.

PET Bottle Sustainability Programs Accelerate rPET Procurement

Major beverage companies have pledged minimum recycled content thresholds often 25% or higher by 2030, catalyzing investment in food-grade rPET capacity. Collection systems improved, lifting the regional PET bottle recycling rate to 27.9% in 2024. Producers such as Plastipak and ALPLA responded by expanding depolymerization and purification lines, helping brand owners meet voluntary and legislative targets. Recycled resin trades at a premium to virgin PET, but volume commitments enable long-term offtake contracts that de-risk capital spending. As rPET adoption grows, converters differentiate through contamination control and traceability audits demanded by beverage clients. These sustainability programs are now a structural driver of the North America rigid plastic packaging market

E-Commerce Growth Intensifies Protective-Packaging Requirements

Direct-to-consumer shipments expose products to multiple handling points, heightening breakage risks for liquids, supplements, and cosmetics. Rigid bottles with thicker wall sections and tamper-evident closures mitigate this risk and align with Amazon’s Frustration-Free Packaging guidelines. Healthcare brands shipping temperature-sensitive products adopt molded polyethylene containers that integrate passive cooling elements, ensuring efficacy over extended transit times. The requirement for barcode compatibility and in-box presentation value further pushes suppliers to add labeling and design capabilities in-house. Consequently, specialized SKUs destined for e-commerce fulfilment centers are increasing their share of the North America rigid plastic packaging market

FDA Migration-Limit Revisions Drive Barrier Technology Investment

In 2024, the FDA updated guidance on specific migration limits for food-contact substances, tightening rules for acidic and high-fat products. Rigid packaging suppliers responded by deploying plasma-enhanced coatings and multilayer structures that block mineral oil hydrocarbons and reduce oxygen ingress. These technologies extend shelf life for sauces, ready-to-eat meals, and baby foods, giving adopters a competitive edge with grocery partners. Compliance projects often coincide with plant upgrades that include inline spectrometry tools to verify barrier performance, raising capital requirements and barriers to entry. The need for proven migration performance cements long-term demand for high-specification containers within the North America rigid plastic packaging market.[2]U.S. Food and Drug Administration, “Food Contact Substance Regulations,” FDA.GOV

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward flexible and paper-based formats | -0.4% | North America, consumer goods focus | Medium term (2-4 years) |

| Volatile virgin-resin feedstock prices | -0.3% | North America, petrochemical-dependent regions | Short term (≤ 2 years) |

| Shortfall of food-grade PCR supply caps recycled-content adoption | -0.2% | US and Canada, beverage industry concentration | Long term (≥ 4 years) |

| State-level EPR fees squeeze low-margin rigid formats | -0.1% | US state-level, California and Northeast focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flexible and Paper-Based Format Competition Intensifies

Environment-conscious consumers perceive single-use rigid plastics as less sustainable than lightweight pouches or emerging fiber-based solutions. Brand owners responding to retailer scorecards convert selected SKUs such as dry snack packs and seasoning mixes to laminates or coated paperboard. Packaging machinery suppliers now offer multimodal filling lines, lowering switching costs between rigid and flexible formats. Nevertheless, rigid packaging retains functional advantages where impact resistance, stack strength, or tamper evidence is critical, limiting share erosion to specific categories. The competitive tension suppresses price-increase headroom for converters in the North America rigid plastic packaging market.

Feedstock Price Volatility Creates Cost Pressures

Though overall resin capacity is growing, unplanned cracker outages and geopolitical events can still trigger 15% quarter-to-quarter price swings for polypropylene and polyethylene. Smaller converters operating on thin margins struggle to pass through surcharges swiftly, compressing cash flow. Hedging instruments exist but require financial expertise and minimum volumes, favoring integrated multinationals. Persistent volatility incentivizes lightweighting programs and alternate material exploration, but such redesigns entail capital expenditure and qualification timelines. These dynamics temper profit expansion across the North America rigid plastic packaging industry during high-price cycles

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: PET Growth Outpaces Traditional Polyolefins

Polyethylene commanded the largest 29.10% share in 2025, reflecting entrenched processing infrastructure and versatile performance. Beverage, household, and industrial chemical producers rely on high-density grades for chemical resistance and rigidity. The North America rigid plastic packaging market size for polyethylene reached 4.51 million tonnes in 2025, yet its forward CAGR trails that of PET. PET’s 3.72% CAGR benefits from recyclability credentials and clarity prized by beverage brands. Recycled-content mandates accelerate food-grade rPET use, creating premium niches for suppliers with advanced decontamination reactors. Polypropylene retains specialized roles in hot-fill and microwaveable containers, while polystyrene’s decline continues due to municipal bans. Emerging bio-based resins appear in pilot volumes, appealing to premium cosmetic lines. Overall, resin diversification is rising but polyolefins and PET will remain core pillars of the North America rigid plastic packaging market.

Ongoing R&D focuses on barrier additives and chain-extension chemistries that enable higher recycled content without compromising mechanical properties. Converters collaborate with resin producers to qualify new grades under FDA 21 CFR regulations for food contact, shortening commercialization timelines. Such partnerships embed resin suppliers deeper into customer value chains, supporting stable demand even as material circularity expectations climb

By Product Type: Caps and Closures Lead Innovation-Driven Growth

Bottles and jars represented 45.10% of 2025 shipments, aligned with long-standing filling and distribution systems across beverages, sauces, and personal care. Their entrenched tooling bases and compatibility with existing labeling lines safeguard share within the North America rigid plastic packaging market. Trays and tubs serve ready-meal and dairy applications that demand rigidity to prevent deformation during microwave heating. Intermediate bulk containers support chemicals and lubricants thanks to stack strength, while drums cater to bulk transport.

Caps and closures exhibit the fastest 3.1% CAGR, propelled by heightened safety and convenience needs. Child-resistant mechanisms, dose-control droppers, and tethered closures to meet single-use-plastic directives drive design complexity and raise average unit revenue. Smart closures integrating NFC chips enter pilot scale in premium spirits, providing authenticity verification. Converters invest in multi-component molding and post-mold assembly automation to capture this high-value segment. As a result, caps and closures gain strategic prominence inside the North America rigid plastic packaging market.

By End-User Industry: Healthcare Drives Premium Growth

Beverages dominated at 35.90% share in 2025, with bottled water, functional drinks, and alcoholic beverages underpinning volume. Carbonated soft drinks maintain relevance, yet flavor innovations in sparkling water and energy segments support incremental bottle demand. Across food applications, sauces, condiments, and dairy require oxygen and light barriers that favor multilayer rigid containers.

Healthcare and pharmaceuticals post the strongest 4.74% CAGR because biologics, diagnostic kits, and self-administration devices need high-precision plastic packaging. USP <661.2> standards govern extractables and leachables, directing material selection toward medical-grade polypropylene and cyclic olefin copolymers. Aging demographics and telehealth trends boost demand for unit-dose blister packs and oral-solid bottles shipped direct to consumers. As regulators encourage child-resistant and senior-friendly designs, rigid formats hold functional advantages over flexible pouches, lifting their share of the North America rigid plastic packaging market.

By Manufacturing Process: Thermoforming Gains from Efficiency Improvements

Injection molding held 25.40% share in 2025 owing to capability to produce intricate geometries and threaded finishes essential for closures and medical components. High-cavitation molds coupled with all-electric presses achieve short cycle times and tight tolerances. The method therefore anchors high-volume beverage and household chemical supply chains.

Thermoforming records the leading 3.6% CAGR as processors target lightweight tray and clamshell applications. Advances in infrared heating and servo-controlled form-cut-stack systems cut energy consumption, making the process cost-competitive for medium-run volumes. Rapid tool changeovers enable SKU proliferation demanded by grocery retail. Blow molding continues to dominate monolayer PET bottles, while compression molding finds niche use in specialty closures. Process digitalization via IoT sensors and predictive analytics elevates uptime, reinforcing manufacturing competitiveness across the North America rigid plastic packaging industry.

Geography Analysis

In the United States, extensive petrochemical feedstock stemming from shale gas production sustains globally competitive polyethylene pricing, anchoring domestic conversion volumes. Large converters leverage automation and proximity to multinational brand owners to secure multiyear contracts. FDA rule updates on food-contact migration accelerate adoption of advanced barrier technologies, providing differentiation for innovation-oriented suppliers.

Mexico’s demographic tailwinds and expanding organized retail spur rigid container uptake in sauces, dairy, and personal-care categories. State-level incentives for recycled-content production encourage joint ventures between local recyclers and international resin producers. Logistics corridors linking central Mexico to Texas foster efficient bidirectional trade in preforms and closures, embedding Mexican plants within the broader North America rigid plastic packaging market ecosystem.

Canada’s high per-capita income fuels steady demand for premium beverages and nutraceuticals. Federal targets for 90% recycling of plastic beverage containers by 2029 stimulate investment in deposit-return infrastructure. Converters differentiate through post-consumer resin certification and carbon-neutral manufacturing claims, resonating with eco-conscious consumers. Health Canada’s risk-based review process influences material and additive choices, favoring suppliers with robust toxicological data packages

Competitive Landscape

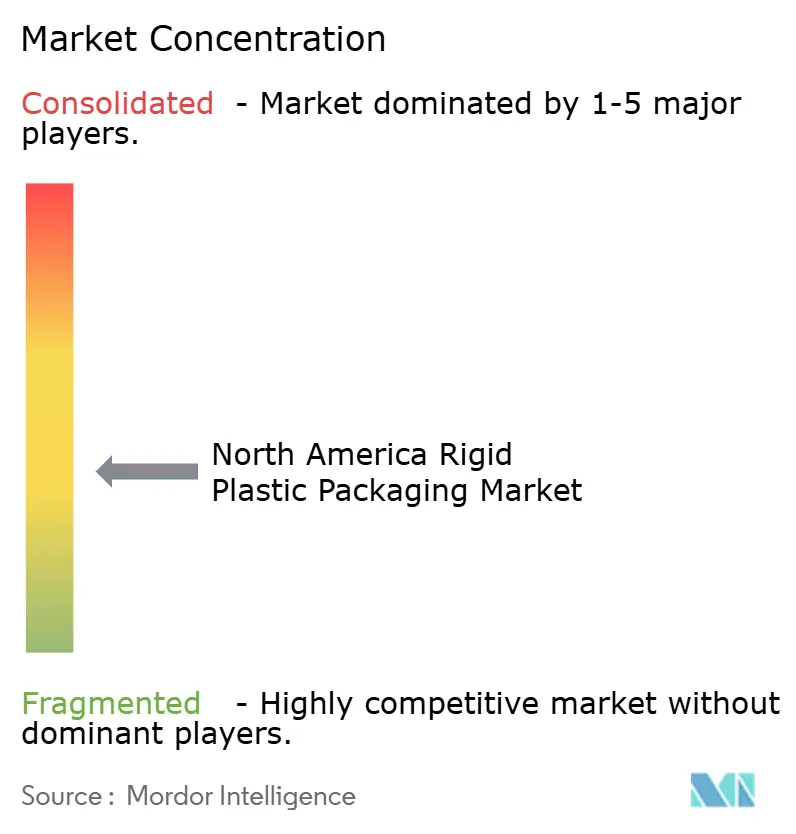

The market remains moderately fragmented; the top five suppliers hold an estimated 38% combined share, leaving ample space for regional specialists. Amcor, Berry Global, and Plastipak operate integrated resin-to-packaging chains, securing raw-material certainty and cost efficiencies. These firms co-develop lightweight bottle platforms with beverage giants to meet performance and sustainability targets. Regional players such as TricorBraun excel in design services and agile order fulfillment, earning loyalty among craft beverage and personal-care brands.

Strategic moves concentrate on capacity expansion, recycled-content integration, and smart-packaging technologies. The 2024 Amcor–Berry Global merger created a global rigid packaging powerhouse with broad resin know-how and a diversified customer base. ALPLA’s USD 75 million rPET upgrade broadened food-grade resin availability, while Gerresheimer’s USD 45 million injection blow-molding expansion addresses rising biologic drug demand. Patents filed at the USPTO for AI-enabled inspection platforms and enzymatic recycling indicate future competitive arenas.[3]U.S. Patent and Trademark Office, “Packaging Technology Patent Database,” USPTO.GOV Suppliers anticipate regulatory tightening and consumer scrutiny, embedding circular-economy principles into long-range capital planning across the North America rigid plastic packaging market.

North America Rigid Plastic Packaging Industry Leaders

-

Sonoco Products Company

-

ALPLA Group

-

Plastipak Holdings Inc.

-

Polytainers Inc.

-

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Amcor finalized an USD 8.43 billion merger with Berry Global, uniting complementary rigid packaging portfolios.

- November 2024: ALPLA Group invested USD 75 million to grow rPET capacity at North American plants.

- October 2024: Polyplex Corporation commissioned a USD 100 million PET film line in Virginia, adding regional supply security.

- September 2024: Origin Materials partnered with beverage majors to scale bio-based PET caps via a USD 50 million program.

North America Rigid Plastic Packaging Market Report Scope

The study tracks the demand for rigid plastic packaging materials across various end-user industries, such as food, foodservice, beverage, healthcare, personal care, cosmetics, industrial, building and construction, and automotive. Rigid plastics can be of different grades and different material combinations based on the type of product being packed, like polyethylene, polypropylene, polyvinyl chloride, polyethylene terephthalate, and bio-plastics.

The North American rigid plastic packaging market is segmented by resin type (polyethylene (PE) (low-density polyethylene (LDPE) & linear low-density polyethylene (LLDPE) and high-density polyethylene (HDPE)), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), and other resin types), product type (bottles and jars, trays and containers, caps and closures, intermediate bulk containers (IBCs), drums, pallets, and other product types), end-user industry (food (candy & confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products), foodservice (quick service restaurants (QSRs), full service restaurants (FSRs), coffee and snack outlets, retail establishments, institutional, hospitality, and others foodservice sectors), beverages, healthcare, cosmetics and personal care, industrial, building and construction, automotive, and other end-user industries), and country (the United States and Canada). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

| Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polyethylene Terephthalate | |

| Polypropylene | |

| Polystyrene and EPS | |

| Other Resin Type |

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Other Product Types |

| Food | Candy and Confectionery |

| Dairy and Frozen | |

| Meat, Poultry and Seafood | |

| Other Food Types | |

| Beverage | |

| Healthcare and Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Industrial Chemicals | |

| Building and Construction | |

| Other End-user Industry |

| Injection Moulding |

| Blow Moulding |

| Thermoforming |

| Compression Moulding |

| Extrusion |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Resin Type | Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polyethylene Terephthalate | ||

| Polypropylene | ||

| Polystyrene and EPS | ||

| Other Resin Type | ||

| By Product Type | Bottles and Jars | |

| Trays and Containers | ||

| Caps and Closures | ||

| Intermediate Bulk Containers (IBCs) | ||

| Drums | ||

| Other Product Types | ||

| By End-user Industry | Food | Candy and Confectionery |

| Dairy and Frozen | ||

| Meat, Poultry and Seafood | ||

| Other Food Types | ||

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Industrial Chemicals | ||

| Building and Construction | ||

| Other End-user Industry | ||

| By Manufacturing Process | Injection Moulding | |

| Blow Moulding | ||

| Thermoforming | ||

| Compression Moulding | ||

| Extrusion | ||

| Other End-user Industries | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America rigid plastic packaging market in 2026?

It stands at 15.84 million tonnes and is forecast to reach 17.58 million tonnes by 2031.

Which resin grows fastest in regional rigid packaging?

Polyethylene terephthalate leads with a 3.72% CAGR through 2031, driven by recycled-content mandates.

Why are caps and closures attracting investment?

They post the highest 3.1% CAGR as brand owners demand tamper evidence, child resistance, and smart features.

What drives Mexico’s rapid demand growth?

Expanding food processing capacity and middle-class consumption lift rigid container usage at a 4.05% CAGR.

How are converters improving margins?

AI-enabled vision systems cut scrap up to 20%, boosting equipment effectiveness and reducing material waste.

Which end-user segment shows premium growth?

Healthcare and pharmaceuticals climb at 4.74% CAGR due to stringent quality norms and biologics expansion.

Page last updated on: