Global Single Use Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

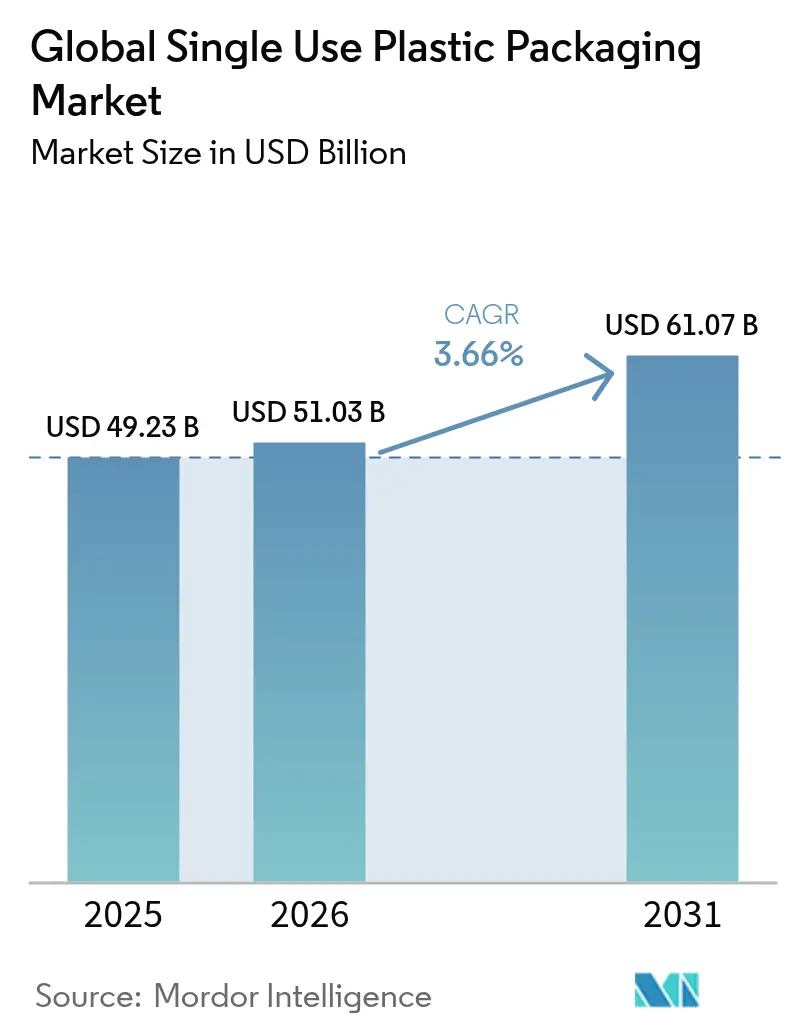

| Market Size (2026) | USD 51.03 Billion |

| Market Size (2031) | USD 61.07 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

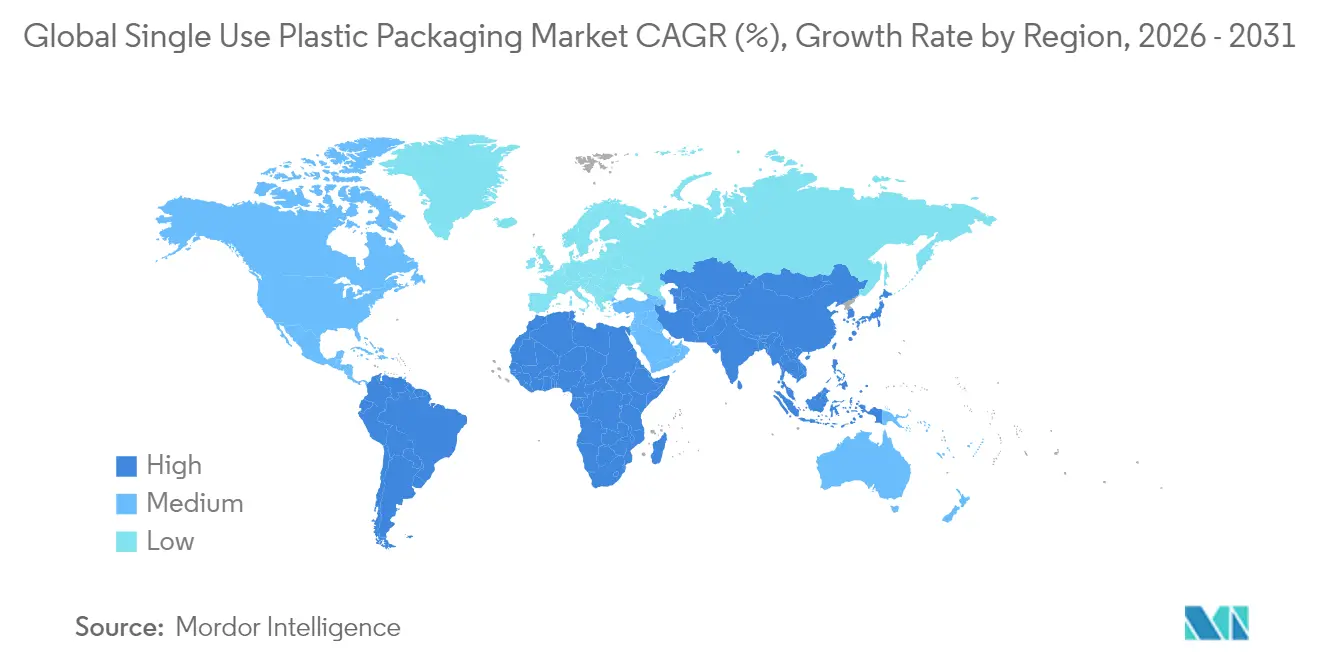

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Single Use Plastic Packaging Market Analysis by Mordor Intelligence

The single-use plastic packaging market size is expected to grow from USD 49.23 billion in 2025 to USD 51.03 billion in 2026 and is forecast to reach USD 61.07 billion by 2031 at 3.66% CAGR over 2026-2031. This outlook captures the sector’s ability to balance tightening regulations with indispensable roles in food safety, pharmaceutical protection and e-commerce fulfillment. Growing demand for ready-to-eat meals, sterile healthcare supplies and logistics-ready formats continues to underpin baseline consumption even as recycled-content mandates and design-for-recycling rules reshape material selection. Scale economies created through recent mega-mergers allow leading suppliers to deploy capital toward circular-economy technologies and to meet diverse regulatory requirements more efficiently. Meanwhile, brand owners emphasize mono-material designs, lightweighting and tethered closures to comply with EU and North American directives without sacrificing performance. Resin price swings linked to crude oil remain a cost variable, but long-term procurement contracts and recycling investments help blunt volatility.

Key Report Takeaways

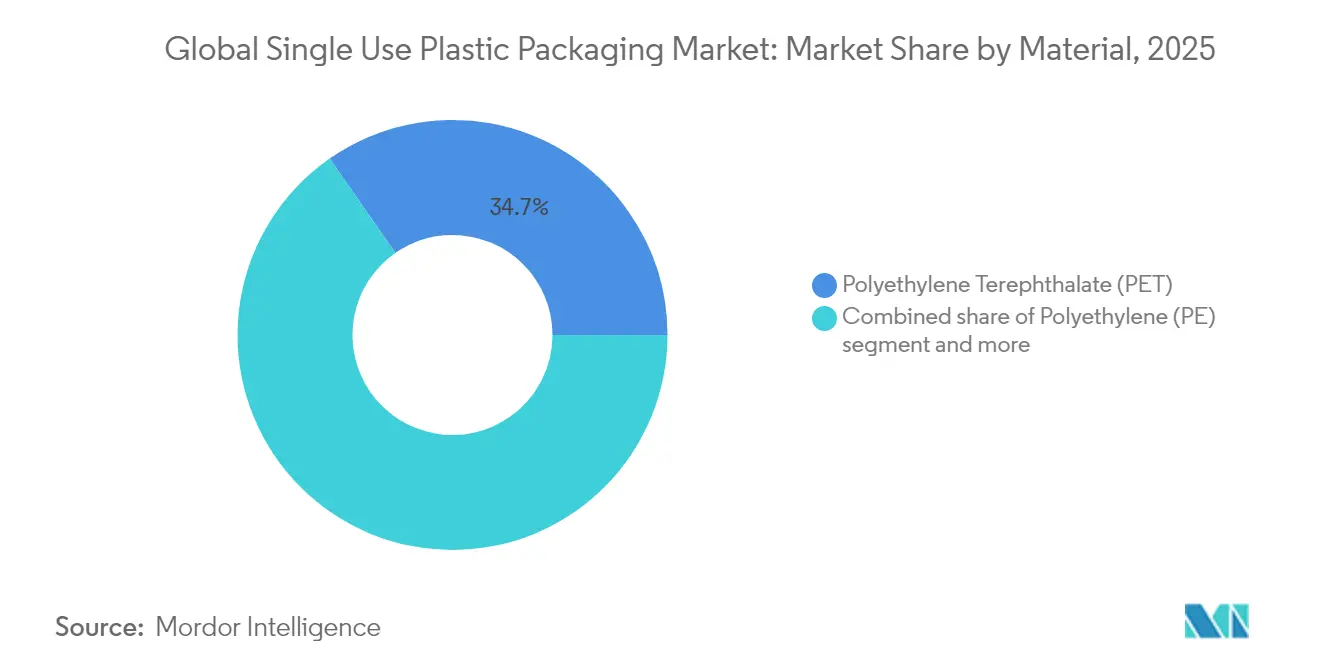

- By material, PET led with 34.68% of the single-use plastic packaging market share in 2025; it also records the fastest 6.95% CAGR to 2031.

- By product type, bottles commanded 30.12% share of the single-use plastic packaging market size in 2025, while pouches and sachets advance at a 4.98% CAGR through 2031.

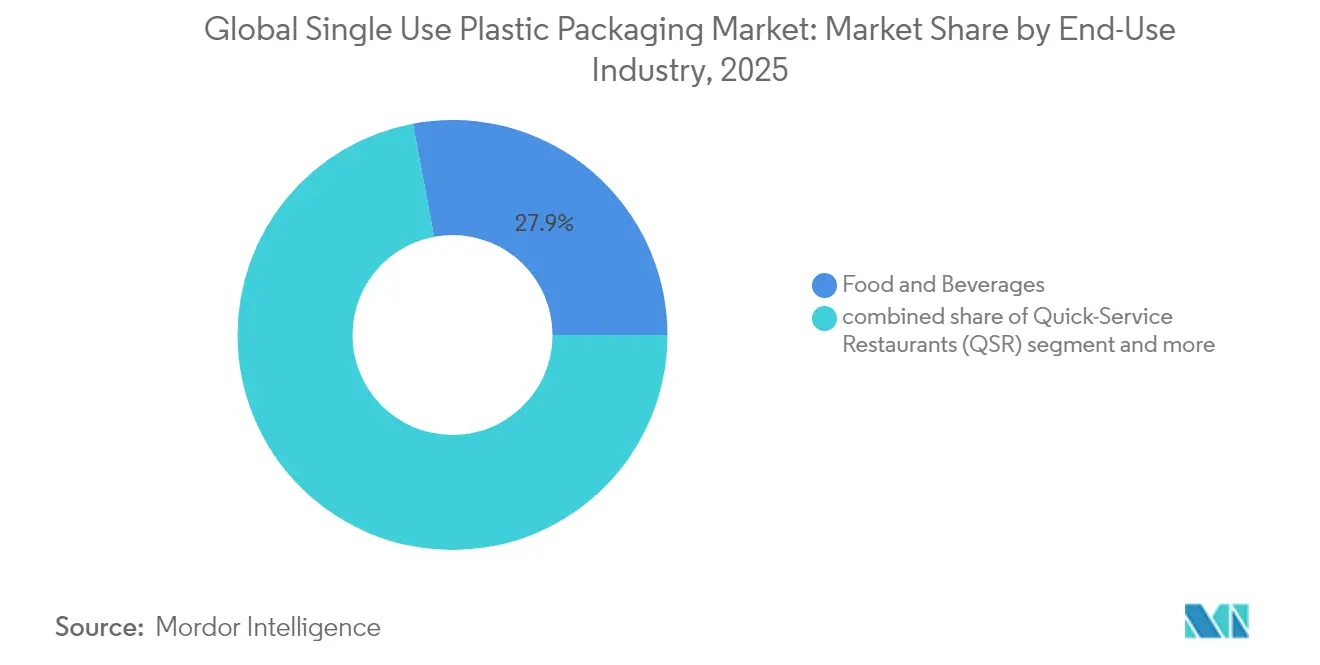

- By end-use industry, food and beverages remained dominant at 27.95% revenue share in 2025; healthcare and pharmaceuticals expand at a 4.65% CAGR to 2031.

- By distribution channel, direct sales held 56.10% share in 2025, whereas indirect channels post a 4.52% CAGR through 2031.

- By geography, Asia-Pacific accounted for 39.85% of the single-use plastic packaging market size in 2025; the Middle East & Africa is projected to grow at 5.45% CAGR to 2031.

- Amcor, Berry Global and Novolex–Pactiv Evergreen together represented 27% of global revenue in 2024, reflecting a moderately concentrated arena.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single Use Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| App-based Food-Delivery Boom in Asian Megacities | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| EU Tethered-Cap Rule Accelerating Mono-Material PET Adoption | +0.6% | Europe, spillover to North America | Short term (≤ 2 years) |

| RTD Functional Beverages Spurring Lightweight Barrier Pouches in North America | +0.5% | North America, expanding to Global | Medium term (2-4 years) |

| India's Pharma Blister Outsourcing Surge | +0.4% | APAC core, export-driven global impact | Long term (≥ 4 years) |

| Tourism-Led Bottled-Water Demand Spike in GCC | +0.3% | Middle East, tourism-dependent regions | Short term (≤ 2 years) |

| Urban China Cold-Chain Expansion Driving EPS Trays | +0.4% | China, extending to Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

App-based Food-Delivery Boom in Asian Megacities

Indonesia, Thailand and Vietnam continue to report double-digit growth in digital food-delivery transactions, elevating demand for leak-proof, temperature-retentive packs that survive motorcycle logistics. [1]Source: Asian Development Bank, “Digital Entrepreneurship in Food Delivery Industry in Indonesia,” adb.org Jakarta operators now allocate 15-20% of order value to packaging, prompting suppliers to engineer stackable designs that cut spillage and enhance brand visibility. A widening base of single-person households favors smaller portions, spurring mini-tub and two-compartment formats. Delivery-platform standardization simplifies SKUs and aids scale economies, while local governments encourage post-use collection schemes that feed emerging recycling infrastructure. These converging forces lift volume yet accelerate the switch to mono-material laminates to ease downstream sorting.

EU Tethered-Cap Rule Accelerating Mono-Material PET Adoption

Europe’s July 2024 tethered-cap mandate has driven rapid conversion of bottling lines; Coca-Cola alone invested EUR 150 million across 40 sites and achieved 95% consumer acceptance. [2]Source: European Commission, “Directive (EU) 2019/904 on Tethered Caps,” eur-lex.europa.eu Suppliers respond with tethered closures that mate seamlessly to virgin, recycled and bio-PET bottles, boosting capture rates and reinforcing PET’s recycling advantage. California will follow by 2027, creating a de-facto global standard that favors producers able to retrofit at scale. Origin Materials’ cross-compatible caps showcase how regulation spurs differentiated product features such as enhanced ergonomics and tamper evidence.

RTD Functional Beverages Spurring Lightweight Barrier Pouches

North America’s functional-drink category benefits from FDA-cleared barrier coatings that permit 30–40% material weight savings over rigid PET while extending shelf life to 18 months. [3]Source: U.S. Food and Drug Administration, “Barrier Coating Approvals 2024,” fda.gov Brands exploit this headroom to shrink carbon footprints and freight bills. Amcor’s vacuum-paneled 16 oz bottle illustrates parallel progress in rigid formats, though pouch systems now capture energy-drink line extensions seeking premium, resealable options. Material suppliers invest in multi-layer films integrating bio-PE, unlocking compatibility with existing recycling streams.

India’s Pharma Blister Outsourcing Surge

Indian CDMOs booked USD 25.4 billion in pharma exports during 2024, and blister packs are central to meeting regulated-market stability and traceability norms. Mold-Tek’s new facilities add 10,000 tonnes of capacity for alu-alu and PVC-free formats, mirroring broader migration toward higher-value healthcare packaging. Government production-linked incentives and serialization rules reinforce long-term blister demand while motivating investments in cleanroom-grade printing and moisture-barrier enhancements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Easy Availability of Substitutes | -0.9% | Global, particularly Europe and North America | Medium term (2-4 years) |

| EU SUP Directive Pushing Brands to Fiber Substitutes | -0.6% | Europe, spillover to global brands | Short term (≤ 2 years) |

| Crude-Linked Resin Price Volatility | -0.7% | Global, manufacturing-intensive regions | Short term (≤ 2 years) |

| US State-Level Bans on Cutlery and Straws | -0.4% | North America, potential global influence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Easy Availability of Substitutes

Fiber-based lids, molded-pulp trays and bio-derived films erode demand where barrier rigor is moderate. McDonald’s Taiwan removed plastic lamination from menus in 2025, saving 86 t of resin annually and preserving 10,000 trees. EU rules requiring recyclability by 2030 accelerate brand pilots of compostable meat trays containing 54% wood cellulose. Dry-molded fiber technology introduced by Dart Container in North America cuts energy use by 80%, improving cost competitiveness against legacy EPS. As tooling migrates, the single-use plastic packaging market faces intensified competition in low-temperature or short-life applications.

Crude-Linked Resin Price Volatility

Polyethylene and polypropylene posted sequential 6-cent-per-pound swings in 2025 amid weaker export demand and talk of 25% tariffs on Canadian and Mexican imports. Such gyrations compressed Berry Global’s margins by USD 120 million in 2024, triggering formula-price contracts and spot-buy caution. PET moved counter-cyclically on bottle-grade shortages, widening spread risk. Larger converters hedge via multi-year feedstock agreements and invest in recycled-content streams that decouple cost bases from virgin resin indices, yet smaller firms struggle with working-capital strain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PET Strengthens Its Circular Advantage

PET captured 34.68% of the single-use plastic packaging market share in 2025 and is expected to widen its lead at a 6.95% CAGR as bottle-to-bottle loops mature. Europe’s 30% recycled-content order for beverage bottles underpins premium demand for rPET flake, prompting investments like Ganesha Ecopet’s 42,000 t pa expansion to meet local brand quotas. Recyclability, barrier clarity and tethered-cap compatibility combine to cement PET’s role in beverage and personal-care aisles.

Polyethylene and polypropylene remain workhorses in films, bags and closures thanks to versatility and cost, yet growth lags as regulators target harder-to-recycle multi-layer laminates. Polystyrene loses share in food service due to bans, while bio-based polymers gain niche traction where performance demands align with compostability mandates. Tech giants push chemical recycling pilots, but until scale and economics converge, PET retains its pragmatic superiority in the single-use plastic packaging market.

By Product Type: Flexible Formats Accelerate

Bottles retain the largest revenue slice at 30.12% in 2025, benefiting from tethered-cap rollouts and on-the-go hydration trends. Even so, pouches and sachets outpace at 4.98% CAGR, driven by functional drinks, condiments and personal-wash refills. FDA-approved ultra-thin barrier films help brands shed 30% of pack weight while preserving shelf stability, making pouches the go-to for portion control and e-commerce.

Clamshells, trays and cups navigate mixed signals: retail produce favors rPET thermoforms, while quick-service eateries trial fiber bowls to satisfy local ordinances. Films and wraps enjoy e-grocery tailwinds but confront recyclability gaps, prompting consortium efforts to standardize mono-material PE structures. Across formats, design-for-recycling becomes a core selection criterion, steering capital toward solutions compatible with curbside collection in leading regions.

By End-Use Industry: Healthcare Spurs Premium Demand

Food and beverages anchored 27.95% of 2025 revenue, yet healthcare and pharmaceuticals present the fastest-rising opportunity with a 4.65% CAGR. Stringent sterility, moisture-barrier and track-and-trace requirements pull through materials such as cyclic olefin polymers and high-barrier blister lids. India’s CDMOs secure western regulatory approvals, multiplying export-grade blister line installations and reinforcing bilateral supply flows.

Meanwhile, restaurant channels pivot to delivery-centric SKUs that demand heat retention and spill prevention. Personal-care brands deploy flexible refill packs and solid concentrates, shaving plastics intensity but raising complexity for recyclers. Industrial shippers, notably in chemicals and lubricants, explore PCR content drums and IBCs to hit corporate carbon pledges, keeping a diversified demand base for the single-use plastic packaging market.

By Distribution Channel: Hybrid Models Emerge

Direct sales dominate with 56.10% share as brand owners lean on converters for co-design and rapid prototyping. The consolidated Amcor-Berry entity fields 400 plants, deepening turnkey appeal for multinationals. Yet indirect channels grow 4.52% CAGR, propelled by digital procurement portals that simplify spot orders for standardized SKUs. Amazon Business logged 45% y-o-y packaging material growth in 2024, spotlighting the ease-of-purchase trend.

Regional distributors enhance value via inventory management, localized regulatory guidance and recycled-content certification audits. Hybrid go-to-market structures surface: suppliers nurture direct key accounts for complex applications while leaning on distributors for mid-tier customers across emerging markets.

Geography Analysis

Asia-Pacific’s 39.85% slice of the single-use plastic packaging market reflects the region’s manufacturing heft, urban population growth and expanding middle class. China’s packaging sector generated RMB 2.3 trillion in output during 2024, supported by e-grocery and cold-chain investment waves that demand EPS and rPET solutions. India adds momentum through blister exports and food-delivery growth, while Southeast Asia posts 35% e-commerce transaction expansion that lifts protective mailer demand.

North America exhibits mature but dynamic conditions shaped by state-level bans and recycled-content quotas. California’s extended producer responsibility law influences brand specifications nationwide, pushing 30% PCR PET targets ahead of federal guidelines. Investments in mechanical and chemical recycling proliferate; Amcor entered a multiyear mechanically-recycled PE deal to secure feedstock continuity.

Europe remains the regulatory vanguard, with the Single-Use Plastics Directive, PPWR and tethered-cap law steering global design templates. Compliance costs drive consolidation yet also catalyze innovation in mono-material flexible structures and molded-fiber keepsake lids.

The Middle East & Africa lead growth at 5.45% CAGR through 2031. Saudi Arabia’s Vision 2030 tourism strategy lifted visitor arrivals 56% in 2024, fueling bottled-water packaging spikes; Masafi invested AED 120 million in capacity enhancements to serve hospitality contracts. Infrastructure mega-projects such as NEOM expand demand for protective and barrier materials able to withstand desert logistics stresses, incentivizing suppliers to site recycling hubs regionally.

Latin America delivers pockets of expansion, notably Brazil where packaging production rose 8% in 2024. Currency fluctuations and uneven regulation temper foreign investment, but local processors upgrade equipment to tap the single-use plastic packaging market opportunity in cross-border e-commerce.

Mordor Intelligence provides coverage of the global single use plastic packaging market across other key regional markets, including Europe, Asia, North America, and Latin America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Industry concentration rose after Amcor’s USD 8.43 billion union with Berry Global and Novolex’s USD 6.7 billion merger with Pactiv Evergreen, creating two giants controlling a quarter of global revenue. Scale affords leverage in resin procurement and the capital to deploy advanced recycling, smart-pack labeling and AI-driven quality assurance. The Federal Trade Commission green-lit both deals, citing the need for investment heft to meet sweeping sustainability mandates.

Mid-tier players pursue specialization: Sealed Air batteries R&D on ultra-light barrier films and automation to carve higher-margin niches, targeting USD 140–160 million annual savings under its CTO2Grow program. Huhtamaki’s Blueloop initiative channels EUR 100 million toward 100% recyclable portfolios that cater to European compliance first, then global rollout.

Technology forms a second battleground. Patent filings in smart packaging jumped 40% in 2024 as companies integrate NFC tags, QR codes and freshness sensors that guide sorting or deliver consumer engagement. Vertical integration into PET reclamation and chemical recycling grows: ExxonMobil evaluates an USD 8.6 billion PE plant embedded with advanced pyrolysis to close loops. Competitive emphasis thus shifts from pure tonnage to closed-loop credibility, regulatory fluency and data-rich functionality.

Global Single Use Plastic Packaging Industry Leaders

Amcor plc

Huhtamaki Oyj

Sealed Air Corp.

Dart Container Corp.

Novolex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amcor closed its merger with Berry Global, projecting USD 650 million annual cost synergies

- April 2025: Novolex and Pactiv Evergreen completed a USD 6.7 billion combination, forming North America’s second-largest packaging supplier

- April 2025: Mid South Extrusion announced a USD 12.5 million PE film expansion in Louisiana, adding 15,000 t capacity

- February 2025: Ganesha Ecopet lifted bottle-to-bottle PET recycling to 42,000 t pa across two new lines

Global Single Use Plastic Packaging Market Report Scope

Single-use plastic packaging refers to disposable containers, wrappers, and other packaging materials made from plastic designed to be used only once before being discarded or recycled. These items are typically used for food, beverages, consumer goods, and various other products, serving the purpose of protection, preservation, and convenience during transportation and storage. Single-use plastic packaging encompasses many products, including plastic bags, food containers, beverage bottles, cutlery, straws, and packaging films. These materials are often lightweight, cost-effective, and provide excellent barrier properties against moisture, oxygen, and contaminants.

The single-use plastic packaging market is segmented by material (polylactic acid [PLA], polyethylene terephthalate [PET], polyethylene [PE], and other material types), product type (bottles, bags and pouches, clamshells, trays, cups and lids, and other product types), end user (quick-service restaurants, full-service restaurants, institutional, retail, and other end users), and geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Columbia, and Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Polyethylene Terephthalate (PET) |

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polystyrene (PS) |

| Other Materials |

| Bottles |

| Pouches and Sachets |

| Clamshells |

| Trays, Cups and Lids |

| Films and Wraps |

| Other Product Types |

| Quick-Service Restaurants (QSR) |

| Full-Service Restaurants (FSR) |

| Food and Beverages |

| Healthcare and Pharmaceutical |

| Personal Care and Cosmetics |

| Other End-Use Industry |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Polyethylene Terephthalate (PET) | ||

| Polyethylene (PE) | |||

| Polypropylene (PP) | |||

| Polystyrene (PS) | |||

| Other Materials | |||

| By Product Type | Bottles | ||

| Pouches and Sachets | |||

| Clamshells | |||

| Trays, Cups and Lids | |||

| Films and Wraps | |||

| Other Product Types | |||

| By End-Use Industfy | Quick-Service Restaurants (QSR) | ||

| Full-Service Restaurants (FSR) | |||

| Food and Beverages | |||

| Healthcare and Pharmaceutical | |||

| Personal Care and Cosmetics | |||

| Other End-Use Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the single-use plastic packaging market?

The single-use plastic packaging market size stands at USD 51.03 billion in 2026.

Which material leads the single-use plastic packaging market?

PET leads, holding 34.68% share in 2025 and expanding at a 6.95% CAGR through 2031.

Why are pouches growing faster than bottles?

Pouches cut material weight by up to 30%, meet convenience demands and comply with emerging recycling-friendly mono-material designs, driving a 4.98% CAGR.

Which region grows the fastest in single-use plastic packaging?

The Middle East and Africa records the highest 5.45% CAGR thanks to tourism and infrastructure projects that elevate bottled-water and food-service demand.

How do regulations impact the single-use plastic packaging industry?

EU tethered-cap and recycled-content rules, plus U.S. state bans, push companies toward mono-material PET, fiber substitutes and higher recycled content, reshaping product design and material sourcing.

Who are the major players after recent consolidations?

Amcor–Berry Global and Novolex–Pactiv Evergreen now account for roughly one-quarter of global revenue, leveraging scale to invest in circular-economy technologies and satisfy multinational brand requirements.

Page last updated on: