Airless Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

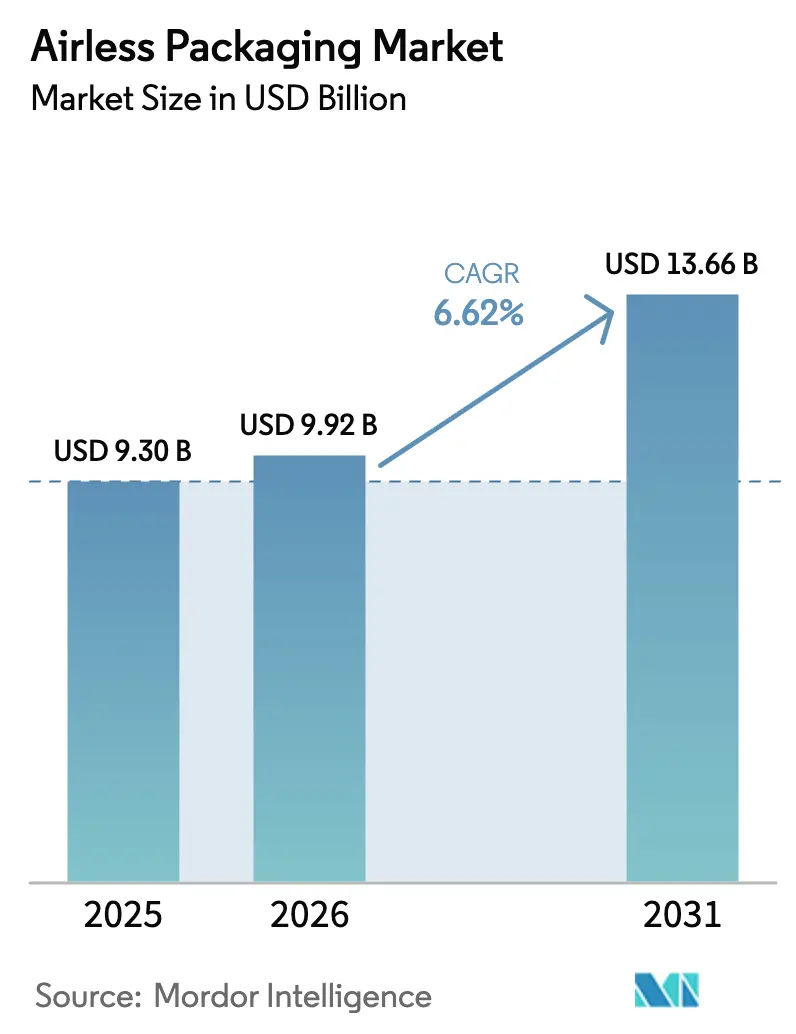

| Market Size (2026) | USD 9.92 Billion |

| Market Size (2031) | USD 13.66 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airless Packaging Market Analysis by Mordor Intelligence

The airless packaging market size in 2026 is estimated at USD 9.92 billion, growing from 2025 value of USD 9.30 billion with 2031 projections showing USD 13.66 billion, growing at 6.62% CAGR over 2026-2031. Growth reflects the migration of air-exclusion technology from niche, high-end uses to a broad set of consumer and healthcare applications. Brands see measurable gains in shelf-life, product integrity, and perceived value, which supports premium pricing while curbing returns arising from leakage or contamination. The pivot toward e-commerce accentuates these benefits because leak-proof dispensing reduces costly shipping failures. At the same time, policy moves such as the United States Food and Drug Administration’s phase-out of PFAS grease-proofing agents and the European Union’s Packaging and Packaging Waste Regulation are steering capital toward mono-material, recyclable pump designs that meet stricter material bans and end-of-life rules.[1]U.S. Food and Drug Administration, “FDA, Industry Actions End Sales of PFAS Used in US Food Packaging,” fda.gov

Key Report Takeaways

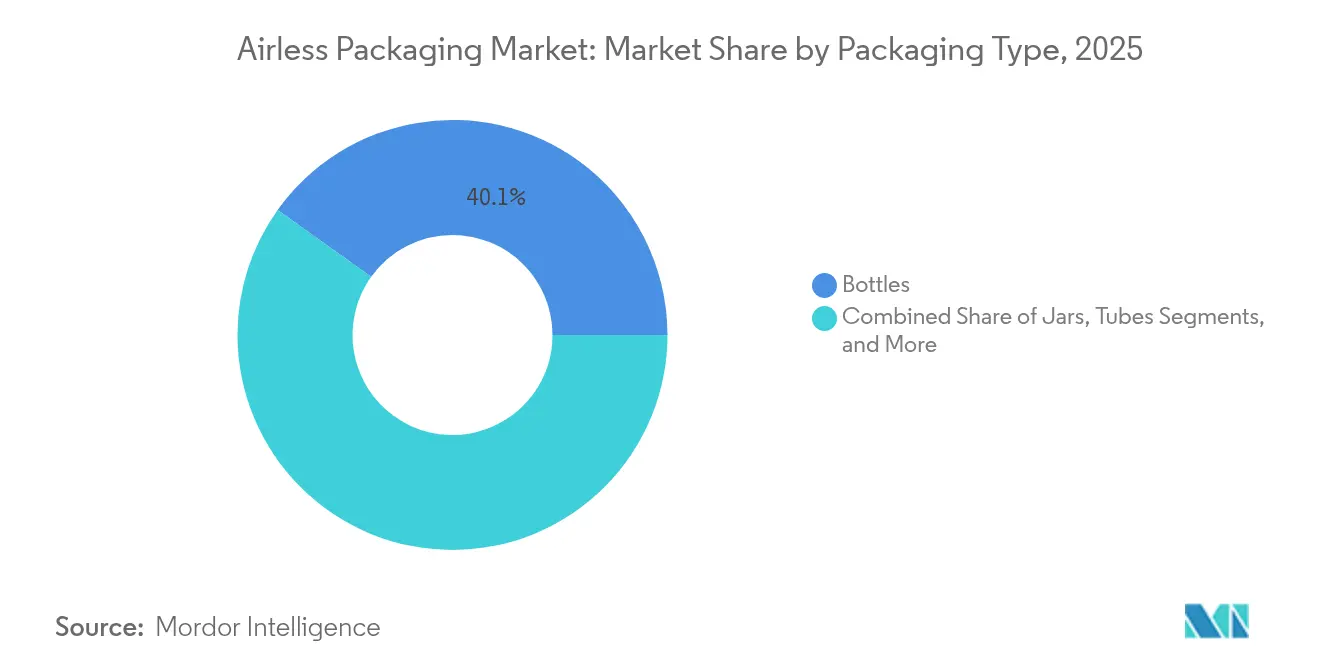

- By packaging type, bottles commanded 40.12% of the airless packaging market share in 2025, whereas bags and pouches are projected to grow at a 9.05% CAGR through 2031.

- By dispensing system, pumps held 45.10% share in 2025; dual-chamber systems are set to deliver an 8.72% CAGR to 2031.

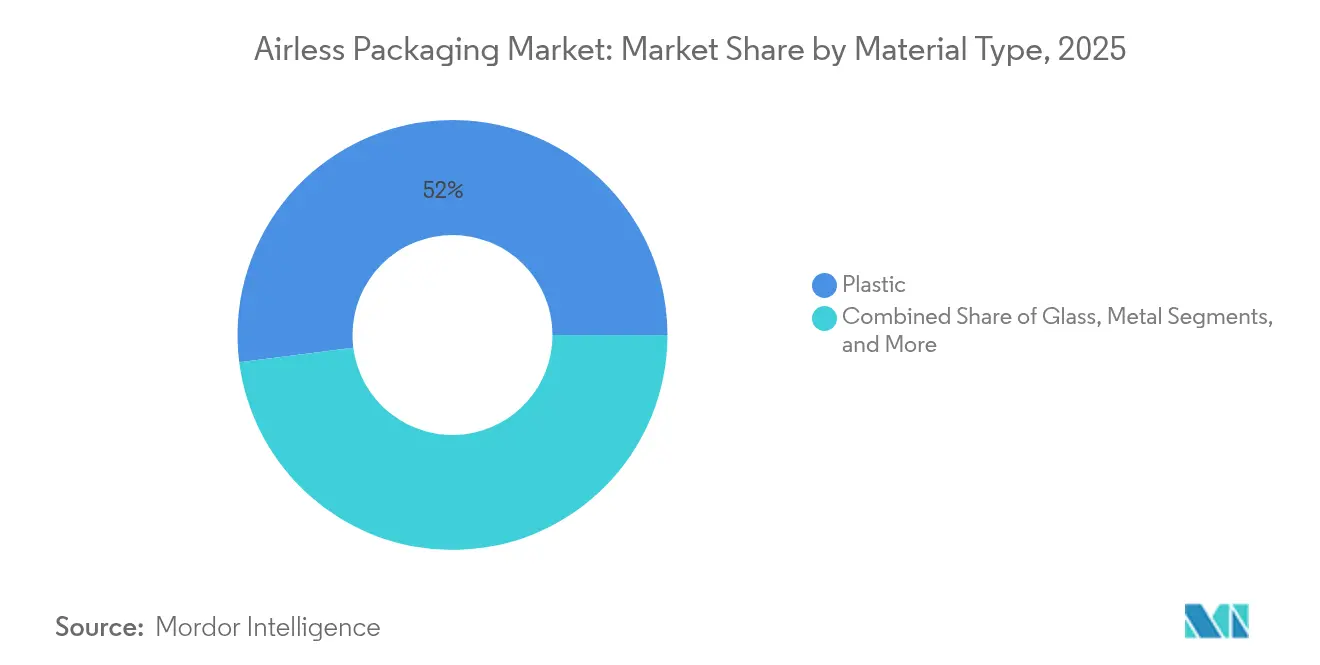

- By material type, plastic accounted for 52.02% share in 2025, while paperboard/laminates will register a 8.95% CAGR during the forecast window.

- By end-user industry, cosmetics and personal care led with 38.12% share in 2025, and pharmaceuticals are poised for a 9.7% CAGR by 2031.

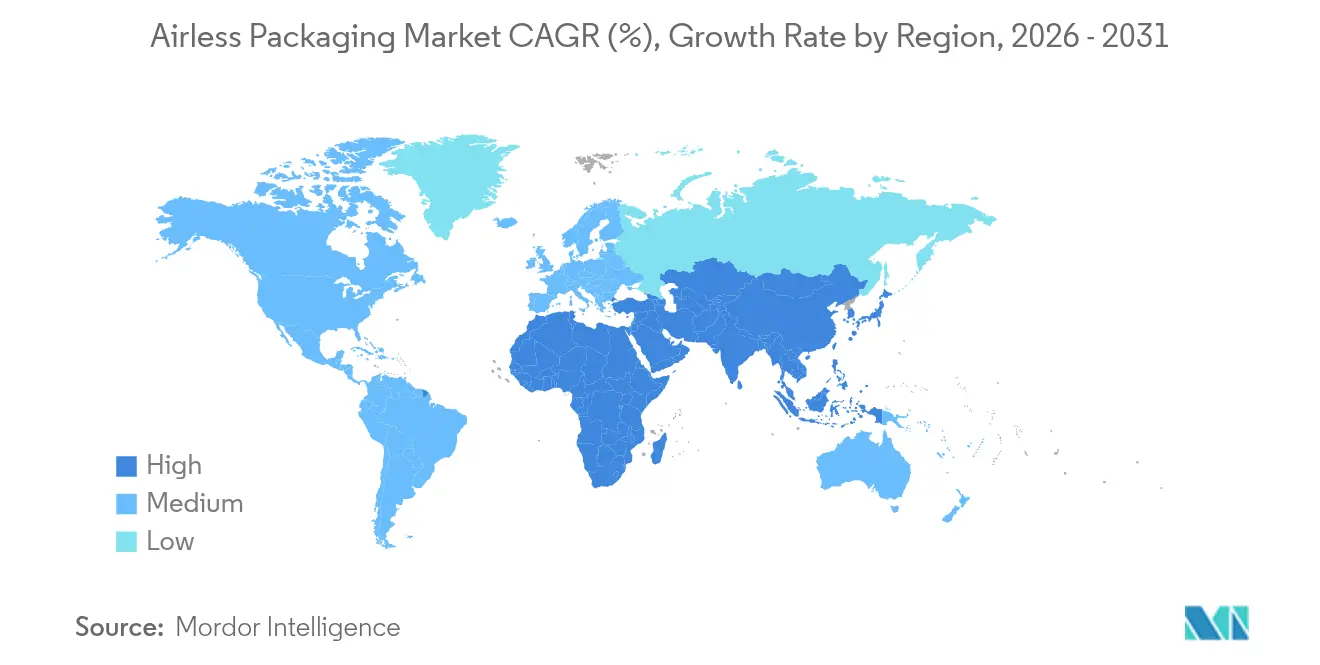

- By geography, North America captured 34.20% revenue share in 2025; Asia-Pacific is forecast to advance at a 9.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Airless Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in premium cosmetics and personal-care launches | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of e-commerce logistics for leak-proof packs | +1.5% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Adoption in pharma for preservative-free formulations | +1.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Shift to mono-material PCR mandates by global CPGs | +1.0% | EU-driven, spreading to North America | Medium term (2-4 years) |

| Refillable tokenization programmes by luxury brands | +0.7% | North America & Europe luxury markets | Long term (≥ 4 years) |

| AI-enabled precision dosing pumps | +0.5% | North America & APAC tech-forward markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Premium Cosmetics and Personal-Care Launches

Luxury and prestige beauty labels have moved decisively toward air-exclusion pumps to protect sensitive formulations from oxidation. L’Oréal’s #JoinTheRefillMovement illustrates the strategic value of combining refillability with airless protection; the company notes material savings of 66% for plastic and 73% for glass when consumers adopt the refill modules. Brands such as Kjaer Weis have embedded the dispenser itself into the luxury narrative, positioning material reduction as an aspirational benefit rather than a compromise. The linkage between formulation stability and anti-aging claims sustains premium price points, encouraging producers to design increasingly sophisticated actuator and valve geometries. As a result, cosmetic launches serve as a showcase for integrated aesthetic and functional innovation that quickly migrates into mass and masstige ranges.

Expansion of E-Commerce Logistics for Leak-Proof Packs

Online retail has sharpened tolerance for damage, leakage, and incomplete filling. Brand owners consequently specify vacuum-sealed or check-valve pumps that remain functional from fulfillment center to consumer doorstep. Aptar’s High-Dose All Plastic Pump, which delivers 3.5 cc per stroke while qualifying for Amazon’s ISTA-6 standard, embodies this focus on drop-resistance and secure closures. Dimensional-weight pricing further favors compact bottle silhouettes with integrated pistons that evacuate every last gram of product, reducing both postage and wastage. Pharmaceuticals benefit in parallel because tight sealing maintains sterility in cold-chain or ambient shipping lanes. As e-commerce penetration rises, leak-proof assurance is becoming a non-negotiable baseline, locking in future demand for the airless packaging market.

Adoption in Pharma for Preservative-Free Formulations

Biologic drugs and sensitive dermatological preparations demand microbial integrity without relying on traditional preservatives. Air-exclusion pumps maintain sterility for multi-dose therapies at home, which improves adherence in chronic care. In 2024, Aptar’s partnership with SHL Medical on connected auto-injectors highlighted the integration of airless barriers with digital adherence monitoring. The broader sustainable pharmaceutical packaging segment is forecast to reach USD 372.19 billion by 2034, underscoring how compliance and patient-safety mandates channel capital toward barrier technology. As formularies shift to cold-chain gene and cell therapies, demand for rugged, tamper-evident pumps intensifies, supporting long-run growth in the airless packaging market.

Shift to Mono-Material PCR Mandates by Global CPGs

Regulators and brand pledges are converging on high post-consumer recycled (PCR) content and PFAS bans. Amcor’s 100% PCR PET bottle for multivitamins verified that recycled resins can meet oxygen-barrier needs even in moisture-sensitive formats.[2]Amcor, “First PET Container for Ritual Multivitamins Made from 100% PCR,” amcor.com The EU’s 2026 PFAS ceiling accelerates the move toward polyolefin-only constructions that simplify sorting streams. Estée Lauder already reports 71% of units as recyclable, refillable, or recoverable, confirming executive-level commitment to design-for-recycling. For the airless packaging market, mono-material pumps that deliver comparable barrier performance yield a first-mover edge as EPR fees escalate for multi-layer formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher unit cost versus conventional packs | -1.2% | Global, particularly price-sensitive APAC markets | Short term (≤ 2 years) |

| Recycling complexity of multi-material designs | -0.8% | EU and North America with strict recycling mandates | Medium term (2-4 years) |

| PFAS barrier-coating restrictions | -0.6% | North America & EU regulatory markets | Medium term (2-4 years) |

| Supply-chain risk for precision spring components | -0.4% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost Versus Conventional Packs

Vacuum pistons, precision springs, and tight-tolerance cylinders push airless bills-of-materials well above standard flip-top tubes. Volatile polypropylene and polyethylene pricing magnifies the differential; March 2025 commodity resin spikes added 12-20% to input costs in North America, partly due to new tariffs on Canadian and Mexican supply lines. Mass-market personal-care firms consequently hesitate to migrate entire stock-keeping units to airless pumps. Nonetheless, total-cost-of-ownership analyses show that reduced product returns, longer shelf-life, and fewer preservatives can offset the upfront premium over a product’s life cycle, hinting at medium-term parity.

Recycling Complexity of Multi-Material Designs

Traditional pumps combine polyolefins, elastomers, metal springs, and silicone valves, which elude mechanical recycling sorters. This complexity incurs rising EPR fees in jurisdictions such as Germany and France. Aptar’s SimpliCycle valve and Future mono-material pump are promising responses, yet adoption remains niche because commercial lines must re-tool to run single-resin assemblies. Until supply chains pivot, municipalities continue to divert most multi-part pumps to energy-from-waste, eroding brand sustainability claims and slowing the airless packaging market uptake in regions with strict diversion targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Bottles Lead Premium Applications

Bottles generated the largest revenue contribution, representing 40.12% of the airless packaging market in 2025. The format accommodates a wide viscosity range and allows aesthetic differentiation through tinted glass or metallized collars. Bags and pouches, while only a fraction of sales, are the quickest climber at 9.05% CAGR owing to material efficiency and squeeze-out performance that leaves less than 2% residual product. The airless packaging market size for bags and pouches is forecast to widen markedly in personal-care refills, where lightweight flexible walls slash transportation emissions. Lumson’s square TAG ELECTA demonstrates how flexible pouches can mimic rigid bottle ergonomics while maintaining vacuum function.

In emerging markets, single-dose sachets gradually convert to mini-pouch vacuum systems that avoid preservatives and improve dosing accuracy. The transition benefits contract fillers that can swap between rigid and flexible lines without overhauling filling heads, thereby lowering changeover costs. Jars preserve relevance in premium creams because tactile interaction supports high unit pricing, yet their 2026-2031 growth lags bottles and pouches. Tubes sustain pharmaceutical demand, especially for dermatology gels requiring pin-point application. Overall, continued innovation in elastomer-free pistons and laser-welded seams ensures each format captures distinct functional and branding niches within the broader airless packaging market.

By Dispensing System: Pumps Dominate Through Reliability

Pumps maintained 45.10% revenue share in 2025, underscoring user familiarity and low failure rates even after 50,000 actuation cycles. Droppers command loyalty for precise ophthalmic and dermal doses, though their unit share is capped by manual dexterity requirements. Twist-and-clicks broaden accessibility for arthritic users, while push buttons suit mass products where one-hand operation is desirable. Dual-chamber designs represent the standout growth story at 8.72% CAGR because they separate reactive ingredients until the moment of application, safeguarding potency for vitamin C serums and combination drug therapies.

The airless packaging market size linked to dual-chamber systems is forecast to scale rapidly in dermatological prescription blends that combine antibiotic and retinoid reservoirs. Complexity shields incumbents because assembly involves multiple ultrasonic and heat-weld steps, raising entry barriers. Refillable mechanisms, once niche, are gaining momentum as luxury houses pair cradle-to-cradle pledges with deposit-return loops. Closed refill loops also deepen consumer loyalty by tying refill pods to proprietary actuator heads, effectively locking share of bathroom-shelf real estate.

By Material Type: Plastic Leads Sustainability Transition

Plastic composites delivered 52.02% revenue share in 2025, anchored by design freedom, drop resistance, and compatibility with multi-piece actuator stacks. The category now straddles virgin, mechanically recycled, and chemically recycled grades to satisfy PCR quotas. Paperboard and laminate substrates, while presently modest, clock a 8.95% CAGR as barrier coatings allow oxygen-sensitive lotions to survive on retail shelves. The airless packaging market share for paperboard containers is projected to jump among European direct-to-consumer beauty lines that integrate unbleached kraft sleeves with bio-based valves.

GualaPack’s mono-material polypropylene laminate pouch showcases progress in sealing science, marrying recyclability with evaporative protection.Glass retains strong affinity for high-purity or aromatherapy SKUs where inertness outweighs weight penalties. Metal’s role narrows to precision spring components and specialized aerosols but could expand if aluminum bottle shells gain traction as refillable assets in closed-loop spa or hospitality settings. Material diversification balances performance, cost, and disposal mandates, fueling incremental gains across the airless packaging market.

By End-User Industry: Cosmetics Drives Innovation

Cosmetics and personal care accounted for 38.12% sales in 2025 and continue to incubate design patents that migrate to adjacent fields. High-viscosity serums exploit piston compression to evacuate dense emulsions without air ingress, maintaining organoleptic qualities until the last dose. Pharmaceutical demand is scaling faster at 9.7% CAGR as regulatory approvals for biologics prompt stricter contamination safeguards. The airless packaging market size serving pharmaceuticals is expected to expand as at-home self-administration regimens become standard of care in oncology and diabetes management.

Food applications remain niche, limited to premium condiments and infant purées where zero-contamination assurance justifies higher unit prices. Homecare aerosols and surface-care sprays investigate propellant-free continuous dispense chambers from start-ups such as GreenSpense, which promise greenhouse-gas abatement. Industrial sectors, including lubricants and adhesives, explore robust pump-in-bottle cartridges that cut exposure to moisture-induced polymerization. As each vertical fine-tunes functional requirements, cross-pollination of actuator, piston, and valve engineering sustains a diverse innovation pipeline inside the airless packaging market.

Geography Analysis

North America led the airless packaging market with 34.20% revenue share in 2025. Demand stems from sophisticated healthcare delivery, a large premium beauty segment, and regulatory scrutiny that penalizes PFAS coatings. United States-based fillers benefit from deep e-commerce penetration, which values leak-proof fulfillment readiness. The airless packaging market size in Canada advances steadily as authorities align recycling labeling with California’s SB 343 standards, nudging converters toward mono-material pump launches. Mexico’s maquiladora corridor supports cost-optimized assembly for cross-border beauty exports.

Europe ranked second in 2025, underpinned by uniform rules under the upcoming Packaging and Packaging Waste Regulation. Germany remains the volume hub for pharmaceutical contract packaging, while France and Italy house luxury cosmetics groups that adopt refill pods and paperboard wraps early. Market volumes pivot toward recyclable polypropylene and PET pumps as extended producer responsibility fees rise. Post-Brexit United Kingdom manufacturers continue to harmonize with EU directives to safeguard access to continental distribution, so British fillers invest in PFAS-free barrier layers that dovetail with European specifications.

Asia-Pacific is the fastest-advancing territory at 9.1% CAGR through 2031. China’s burgeoning middle class values efficacy and authenticity, boosting uptake of vacuum serum dispensers in cross-border direct-mail channels. Japan’s technical prowess fosters ultra-compact actuator miniaturization displayed at CITE JAPAN 2025, while domestic beauty labels showcase algae-based active formulations that rely on strict oxygen exclusion. South Korea exports K-beauty travel sizes that employ dual-airless sachet packs for single-week routines. Australia, though a smaller base, codifies recycled-content mandates that encourage local fillers to experiment with paper-laminate pouches. Collectively, rising disposable incomes, digital commerce, and regional raw-material availability propel enduring growth in the airless packaging market.

Competitive Landscape

Competition is moderate, with scale conferring material-sourcing leverage and R&D depth. AptarGroup, Albéa, and Silgan sustain leadership through global manufacturing footprints and a cadence of pump platform updates. Aptar posted USD 887 million in Q1 2025 sales, lifted by high-demand proprietary drug-delivery pumps. Albéa exploits vertical integration from plastic resin through decoration to accelerate custom launches for indie beauty brands. Silgan’s trigger sprayers complement its rigid plastics portfolio, offering cross-selling synergies into home and personal care.

Strategic combinations are redrawing boundaries. The announced Amcor–Berry Global all-stock merger will pool mono-material barrier film expertise with global converting capacity, creating a formidable integrated player. Kolmar Korea’s acquisition of Yonwoo aligns formulation know-how with actuator manufacture, shortening time-to-market for bespoke Korean beauty sets. Ball Corporation’s inorganic push into impact-extruded aluminum offers new substrate alternatives as refillable metal bottles gain traction in European spas.

Emerging firms secure footholds via focused technologies. GreenSpense markets a propellant-free continuous dispenser suited to viscous creams, capturing sustainability-led buyers. Lumson and GualaPack invest in hybrid pouch-in-bottle constructs that blend ergonomic rigidity with flex-pack efficiency. These challengers slash development cycles by 3-6 months using modular tooling and digital printing, enabling rapid private-label rollouts. As regulators tighten recyclability metrics, first movers delivering mono-material or refill systems are likely to outpace slower incumbents, shaping competitive intensity in the airless packaging market.

Airless Packaging Industry Leaders

AptarGroup Inc.

Albea Services S.A.S

Silgan Holdings Inc.

Lumson S.p.A

HCP Packaging Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Luxury Cosmetic Solutions Investments acquired a majority stake in Eurovetrocap S.p.A., pairing molded-glass expertise with advanced pump designs for prestige skin-care lines.

- June 2025: Ball Corporation completed its takeover of Alucan to expand recyclable aluminum packaging capacities across Spain and Belgium.

- May 2025: AptarGroup recorded USD 887 million Q1 sales, citing demand for air-exclusion drug-delivery devices within its pharmaceutical division.

- March 2025: TricorBraun agreed to purchase Veritiv Containers, widening its North American rigid-packaging scope for personal-care customers.

Global Airless Packaging Market Report Scope

Airless packaging is a method of storing products by keeping air out to preserve the product's quality. Increasing demand for airless packaging among numerous cosmetic brands is projected to augment sales of airless packaging. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The airless packaging market is segmented by packaging type (Bottles, Jars and Tubes), by dispensing systems (Pumps, Dropper and Twist & Clicks), by material (Plastic and Glass) and by geography (North America, Europe, Asia Pacific, South America and Middle East & Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Bottles |

| Jars |

| Tubes |

| Bags and Pouches |

| Other Packaging Type |

| Pumps |

| Droppers |

| Twist and Clicks |

| Push Buttons |

| Dual-Chamber Systems |

| Refillable Mechanisms |

| Plastic (PP, PET, etc.) |

| Glass |

| Metal |

| Paperboard / Laminates |

| Cosmetics and Personal Care |

| Pharmaceutical and Healthcare |

| Food and Beverages |

| Homecare and Industrial |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Packaging Type | Bottles | ||

| Jars | |||

| Tubes | |||

| Bags and Pouches | |||

| Other Packaging Type | |||

| By Dispensing System | Pumps | ||

| Droppers | |||

| Twist and Clicks | |||

| Push Buttons | |||

| Dual-Chamber Systems | |||

| Refillable Mechanisms | |||

| By Material Type | Plastic (PP, PET, etc.) | ||

| Glass | |||

| Metal | |||

| Paperboard / Laminates | |||

| By End-user Industry | Cosmetics and Personal Care | ||

| Pharmaceutical and Healthcare | |||

| Food and Beverages | |||

| Homecare and Industrial | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the airless packaging market?

The airless packaging market size is USD 9.92 billion in 2026 and is projected to hit USD 13.66 billion by 2031.

Which region leads global demand?

North America leads with 34.20% revenue share in 2025 thanks to strong pharmaceutical and premium beauty consumption.

Which segment is growing fastest by packaging type?

Bags and pouches show the fastest growth at a 9.05% CAGR because of their lightweight, material-efficient designs.

Why are dual-chamber systems expanding quickly?

They keep reactive ingredients separate until the point of use, driving an 8.72% CAGR as brands offer fresh-mix formulations.

How are sustainability rules affecting materials?

EU and U.S. PFAS restrictions and PCR targets are pushing converters toward mono-material pumps and higher recycled resin content.

What keeps costs higher than standard packaging?

Precision components, multi-step assembly, and resin price swings add premium, although life-cycle savings on waste and returns offset part of the upfront cost.

Page last updated on: