Flexible Intermediate Bulk Container (FIBC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

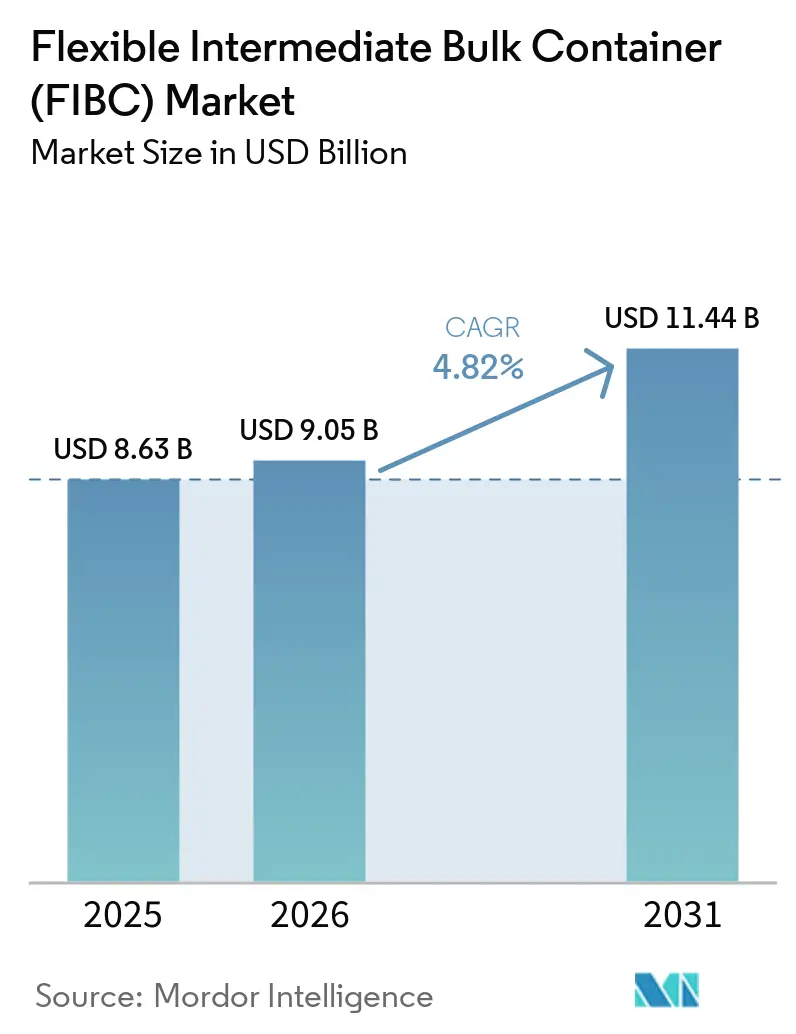

| Market Size (2026) | USD 9.05 Billion |

| Market Size (2031) | USD 11.44 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

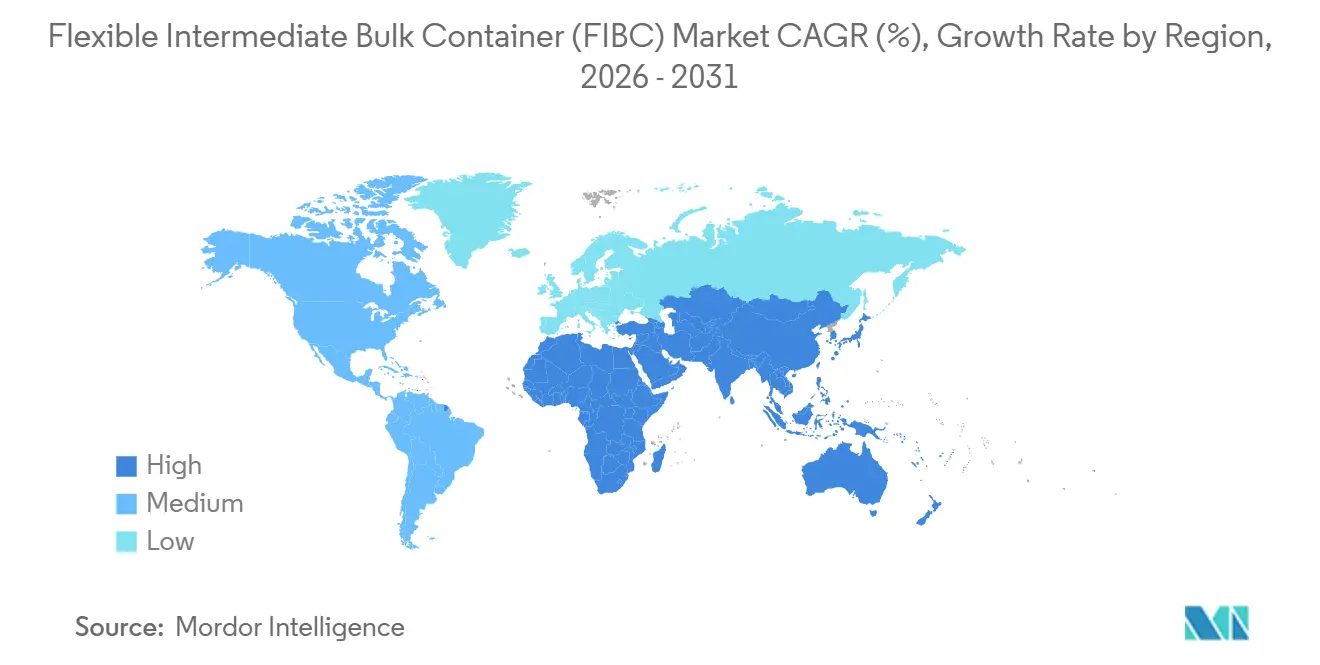

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

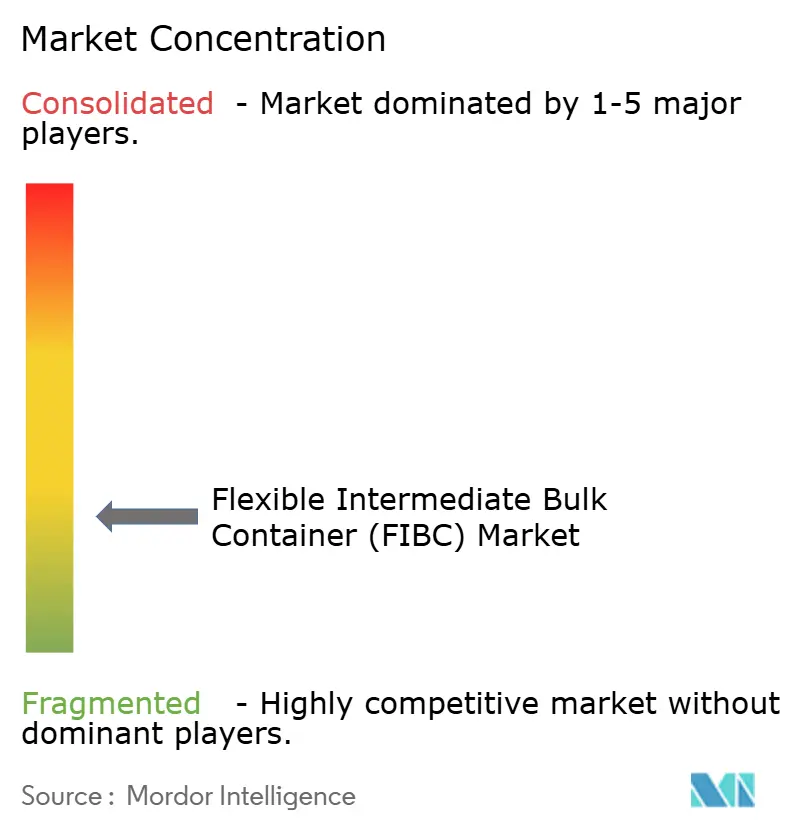

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Intermediate Bulk Container (FIBC) Market Analysis by Mordor Intelligence

The Flexible Intermediate Bulk Container Market size is projected to be USD 8.63 billion in 2025, USD 9.05 billion in 2026, and reach USD 11.44 billion by 2031, growing at a CAGR of 4.82% from 2026 to 2031.

Demand continues to come from chemicals, agriculture, and construction, but stronger growth now comes from sustainable packaging mandates, in-plant automation, and the rapid scale-up of lithium and rare-earth supply chains. North America held the largest flexible intermediate bulk container market share at 38.74% in 2024 on the back of stringent safety rules and sizeable agricultural exports, whereas Asia-Pacific is expanding at 8.12% CAGR through 2030 on the strength of capacity additions in China, India and Southeast Asia. Tightened global hazardous-goods regulations have lifted premium demand for Type C and Type D electrostatic-safe bags, while circular-economy policies accelerate adoption of recycled-content polypropylene variants.

Key Report Takeaways

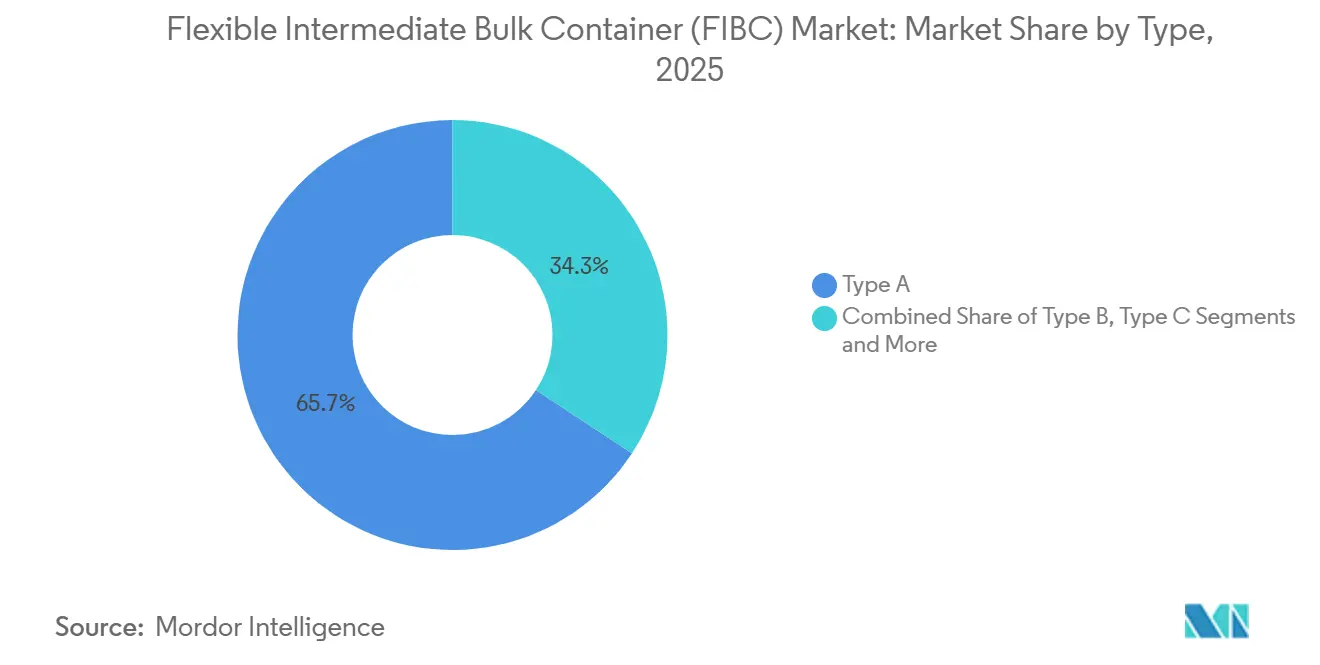

- By type, Type A bags captured 65.74% of flexible intermediate bulk container market share in 2025; Type D bags show the fastest 7.53% CAGR through 2031.

- By design, Baffle/Q-Bag formats led with 34.12% revenue share in 2025, whereas U-Panel designs are projected to grow at 8.28% CAGR to 2031.

- By end-user industry, Chemicals and petrochemicals accounted for 39.88% of the flexible intermediate bulk container market size in 2025, while food and agriculture is advancing at 7.01% CAGR during the forecast window.

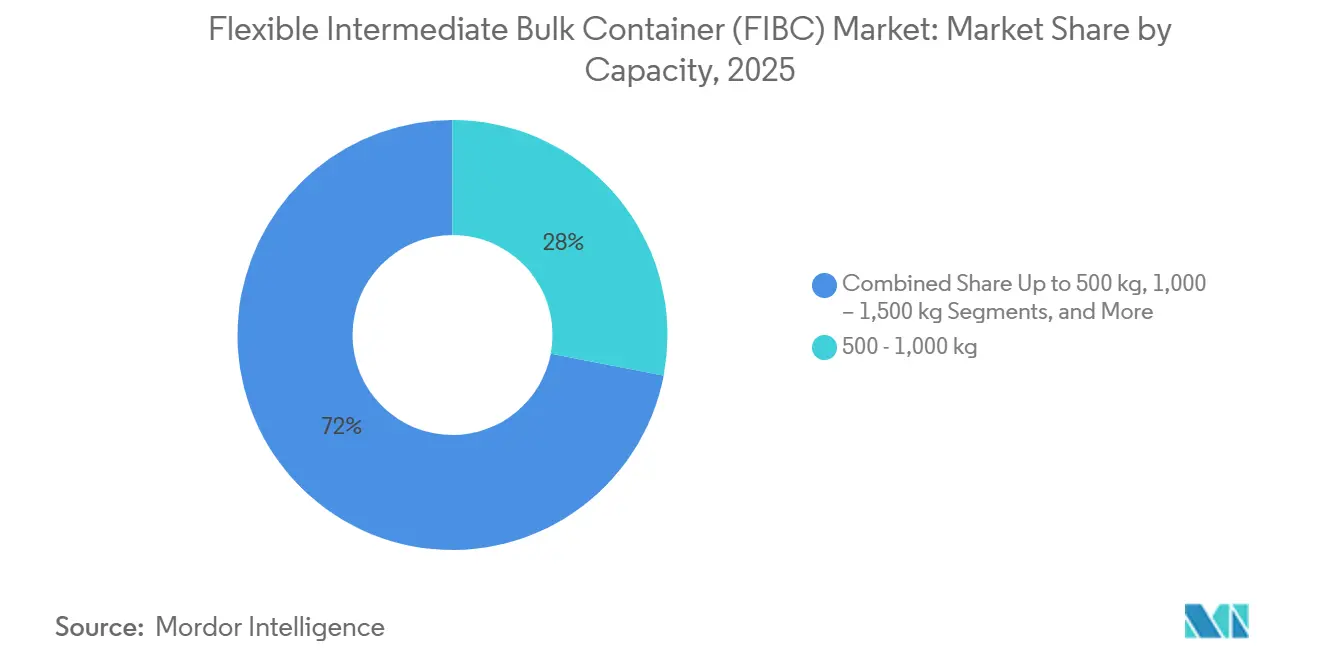

- By capacity, the 500-1,000 kg segment held 28.02% share of the flexible intermediate bulk container market size in 2025; containers above 1,500 kg exhibit a 6.45% CAGR to 2031.

- By material, Virgin polypropylene represented 59.73% share in 2025, but recycled-content PP is the fastest riser at 8.64% CAGR.

- By geography, North America led with 38.25% share in 2025; Asia-Pacific is the quickest climber at 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Intermediate Bulk Container (FIBC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food and agro commodities bulk export boom | +1.2% | Global, with concentration in North America, South America, Asia-Pacific | Medium term (2-4 years) |

| Hazardous-chemical handling regulations boosting demand | +0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| E-commerce fulfilment shift to bulk secondary packaging | +0.6% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Smart-FIBC (IoT/RFID) rollout for real-time traceability | +0.4% | North America, Europe, developed Asia-Pacific markets | Long term (≥ 4 years) |

| Paper and recycled-PP FIBC adoption under circular-economy mandates | +0.7% | Europe, North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Mining super-sack standardisation in lithium and rare-earth supply chains | +0.5% | North America, Australia, South America, select Asia-Pacific regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food and Agro Commodities Bulk-Export Boom

Global reshoring of grain and specialty-crop supply chains is boosting demand for food-grade flexible bulk bags that lower per-unit freight cost and prevent cross-contamination.[1]Food and Drug Administration, “Standards for the Growing, Harvesting, Packing, and Holding of Produce for Human Consumption Relating to Agricultural Water,” federalregister.gov Source: Occupational Safety and Health Administration, “Hazard Communication Standard; Final Rule,” federalregister.gov Updated U.S. agricultural-water rules effective 2024 require tighter produce traceability, pushing exporters toward barcode-ready FIBCs that integrate seamlessly with digital record systems. Countries expanding port infrastructure, such as Brazil and India, are investing in bulk-handling silos designed around FIBC discharge equipment, reinforcing mid-term growth. Commodity-price swings further encourage growers to choose flexible intermediate bulk container market solutions that cut packaging spend while protecting margins. The confluence of food-safety regulation and cost discipline therefore underpins the segment’s resilience.

Hazardous-Chemical Handling Rules Boosting Demand

OSHA’s 2024 alignment with UN GHS revision 7 raises the technical bar for containers that carry flammable powders and solvents. Type C and Type D bags with conductive yarns and CROHMIQ fabrics are now standard at chemical plants, pharmaceutical mixers and lithium-ore processors. Procurement managers are switching from commodity sacks to certified units despite premiums of 20-30%, viewing them as risk-mitigation assets that reduce downtime and insurance exposure. Short 18-month compliance windows have pulled forward orders, keeping utilization high for specialty lines in North America and Europe. The result is a durable uplift in the flexible intermediate bulk container market for electrostatic-safe variants.

E-Commerce Fulfilment Shift to Bulk Secondary Packaging

High-velocity fulfilment centers use FIBCs to feed automated pack-lines with dunnage, void-fill and other consumables, cutting labor touches versus corrugated gaylords.[2]Nanolike, “TankConnect: Turn Your Plastic IBCs into Sustainable, Smart and Connected Tank!” nanolike.com Vertical racking of baffle bags maximizes floor space inside urban warehouses where rents are steep. Robotics-ready U-Panel bags with reinforced loops integrate with gantry pickers, driving an uptick in tailored designs. Europe and Japan, where parcel automation is advanced, lead adoption, while North American 3PLs are piloting similar systems. As online sales continue climbing, the flexible intermediate bulk container market finds a new downstream foothold beyond its traditional industrial base.

Smart-FIBC Rollout for Real-Time Traceability

Embedding RFID in lift loops and lining pockets allows shippers to geolocate, temperature-track and remotely read fill levels of chemical or food ingredients. Early adopters in pharmaceuticals use sensor data to verify cold-chain integrity, while mining firms monitor bag counts at remote sites to optimize resupply. Cloud dashboards and predictive-maintenance alerts reduce fleet losses and product spoilage, adding measurable ROI that offsets sensor cost. Cyber-security and data-standard hurdles persist, restricting penetration to larger enterprises, but falling tag prices will open mass-market opportunities during the long-term horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PP resin price volatility | -0.9% | Global, particularly impacting Asia-Pacific and North America | Short term (≤ 2 years) |

| Stringent static-dissipation certification costs | -0.4% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Ocean-freight container shortages disrupting FIBC supply | -0.6% | Global trade routes, particularly Asia-Pacific to North America/Europe | Short term (≤ 2 years) |

| Growth of rigid-IBC rental pools cannibalising one-way FIBC demand | -0.7% | North America, Europe, developed Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PP Resin Price Volatility

Polypropylene feedstock swings, driven by crude-oil moves and refinery outages, make up 60-70% of bag production cost, undermining smaller converters that lack hedging tools.[3]Plastics Technology, “Prices Up for PE, ABS, PC, Nylons 6 and 66; Down for PP, PET and Flat for PS and PVC,” ptonline.com June 2024 resin drops offered brief relief, yet chronic uncertainty compels buyers to delay blanket orders or renegotiate quarterly. Larger manufacturers offset exposure by backward integrating into resin compounding and accelerating adoption of recycled PP, but mid-tier players face margin squeeze. The short-term drag on the flexible intermediate bulk container market gradually eases as futures-based contracts and recycled feedstocks gain traction.

Growth of Rigid-IBC Rental Pools

Reusable composite bottles mounted in steel cages are winning share in high-turn chemical loops where return logistics exist. Rental providers bundle cleaning, tracking and compliance, yielding lifetime cost savings that outcompete single-trip sacks in regional circuits. Europe’s mature reverse-logistics web and tightening waste rules make the threat most acute, while North America follows with sustainability scorecard pressure. FIBC makers are countering with heavy-duty multi-trip designs and exploring subscription models, yet the cannibalisation narrows opportunities for low-margin one-way products, tempering long-term expansion of the flexible intermediate bulk container market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electrostatic Safety Drives Premium Adoption

Type A containers supplied 65.74% of 2025 demand, underscoring their value positioning across grain, cement and non-flammable chemical flows. Electrostatic-safe Type D bags, however, expand at 7.53% CAGR as lithium-ore refiners and pharmaceutical dryers specify non-grounded solutions to avert ignition risks.

Intensifying regulatory oversight and the absence of external grounding wires position Type D as the premium choice, enabling remote mines and offshore rigs to cut compliance complexity. High-tensile CROHMIQ fabrics have clocked more than 40 million safe trips, validating reliability in harsh environments and reinforcing future gains for the flexible intermediate bulk container market.

By Design Type: Baffle Innovation Optimizes Space Efficiency

Baffle or Q-Bag variants held 34.12% share in 2025 owing to internal panels that stop bulging and unlock higher stack density, a decisive benefit for ship holds and urban DCs. U-Panel sacks track at 8.28% CAGR through 2031, supported by tight dimensional tolerances that mate smoothly with robotized filling frames.

Circular and 4-Panel designs maintain presence where maximum volume or precise discharge is required, yet continual lean-warehouse initiatives favor baffles. Automated facilities scanning pallets welcome the uniform footprint, sustaining the flexible intermediate bulk container market momentum for engineered geometries.

By End-User Industry: Food Safety Regulations Accelerate Agricultural Adoption

Chemicals and petrochemicals contributed 39.88% of revenues in 2025, reflecting the sector’s heavy reliance on certified bags for flammable powders and aggressive solvents. Food and agriculture ranks as the fastest riser at 7.01% CAGR, catalyzed by stricter water-safety and traceability codes that lean toward tamper-evident liners and HACCP-friendly printing.

Produce exporters in South America and Southeast Asia now prefer food-grade FIBCs to slash per-ton freight costs, while millers in the United States retrofit silos with bottom-spout feed for automated flour discharge. The dual pull of safety and volume propels the flexible intermediate bulk container market size within this segment well into the forecast horizon.

By Capacity: Heavy-Duty Applications Drive Large-Container Growth

Mid-range 500-1,000 kg bags matched equipment limits and produced 28.02% of 2025 sales, but >1,500 kg skus post a sturdy 6.45% CAGR as crusher circuits and bulk blend plants chase labor productivity.

Larger sacks oblige thicker tapes, reinforced seams and multi-layered lift loops, innovations that simultaneously push ASPs and spark process upgrades among miners and chemical mixers. Payload maximization against freight caps keeps the flexible intermediate bulk container market advancing into heavier capacities.

By Material/Polymer Type: Sustainability Mandates Accelerate Recycled Content Adoption

Virgin PP dominated with 59.73% share in 2025 because of predictable mechanical properties and broad food-contact clearances. Recycled-content PP races ahead at 8.64% CAGR as eco-scorecards factor into tender awards and carbon-pricing schemes tighten.

Brands such as Red Bull have demonstrated pallet and bag ecosystems built from 100% recycled plastic, curbing container trips by 20% and validating closed-loop economics. Food-grade recycled PP pilot lines under NextLooPP are on the cusp of regulatory review, likely speeding mainstream uptake and reshaping the flexible intermediate bulk container market trajectory toward circular materials.

Geography Analysis

North America generated 38.25% of global revenue in 2025, underpinned by a mature chemical supply chain, high agricultural export volumes, and strict OSHA compliance that favors higher-margin certified bags. The region keeps a stable growth path as asset owners reinvest in smart-packaging retrofits and domestic shale-chemicals output holds firm.

Asia-Pacific records the most rapid 7.78% CAGR due to heavy investment in battery metal refining and broad-based manufacturing expansion. China’s Baotou rare-earth hub, India’s production-linked incentives and Southeast Asia’s agribusiness exports converge to lift regional orders for conductive and high-stack designs. Local producers such as Bulkcorp International scale capacity and secure export contracts, testifying to competitive depth that fuels the flexible intermediate bulk container (FIBC) market.

Europe retains a significant share by pioneering recycled-material specifications under the Green Deal and by deploying reverse logistics that complement multi-trip models. South America benefits from soy, corn and lithium-brine exports that require food-grade or heavy-duty sacks, while the Middle East and Africa gain from petrochemical expansions and infrastructure megaprojects. Regional diversification therefore spreads opportunity across the flexible intermediate bulk container (FIBC) market landscape.

Competitive Landscape

The market shows moderate concentration, led by firms with global plant footprints, in-house resin compounding and accredited test labs. Top players invest in IoT-enabled production lines that self-calibrate tape tension and seam strength, raising throughput while cutting scrap. Continuous improvement secures cost leadership and compliance repeatability, core to winning regulated tenders.

Strategic consolidation is ongoing. Mauser Packaging’s February 2025 purchase of Consolidated Container extends vertical integration into rigid lines and service offerings, illustrating the blurring boundary between flexible and rigid bulk packaging. Greif’s USD 1.8 billion divestiture of its containerboard unit in July 2025 frees capital for high-margin industrial packaging growth.

Emergent challengers focus on rental pools, recycling hubs and data-rich asset-tracking services, pushing incumbents to develop closed-loop programs and subscription models. Sustainable material breakthroughs and smart-bag ecosystems will define the next wave of differentiation in the flexible intermediate bulk container market.

Flexible Intermediate Bulk Container (FIBC) Industry Leaders

Greif Inc.

United Bags Inc.

Rishi FIBC Solutions Pvt Ltd

Plastipak Group

J&HM Dickson Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Greif Inc. agreed to sell its containerboard business to Packaging Corporation of America for USD 1.8 billion.

- March 2025: Mitsui O.S.K. Lines acquired LBC Tank Terminals for USD 1.715 billion to strengthen chemical-logistics service.

- February 2025: Mauser Packaging Solutions bought Consolidated Container Company, widening its industrial packaging platform .

- January 2025: Amcor purchased Phoenix Flexibles in India to boost local capacity for sustainable flexibles.

Global Flexible Intermediate Bulk Container (FIBC) Market Report Scope

The study on the flexible intermediate bulk container market offers an up-to-date analysis of the current regional market scenario, the latest trends and drivers, and the overall market environment. The study tracks the revenue generated from the consumption and sales of flexible intermediate bulk containers offered by the vendors operating in the market.

The FIBC Market is Segmented by type (type A, type B, type C, and type D), design type (U-panel bags, baffle bags, circular bags, 4-side panel bags, and other design types), end user (food and agricultural products, chemical and petrochemical, pharmaceutical, and other end users), and Geography (North America ( United States and Canada), Europe ( United Kingdom, Italy, Germany, France, and Rest of Europe), Asia-Pacific ( China, India, Japan, Australia and New Zealand, and Rest of Asia-Pacific), Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Type A |

| Type B |

| Type C |

| Type D |

| U-Panel |

| Baffle / Q-Bag |

| Circular |

| 4-Panel |

| Other Designs |

| Food and Agriculture |

| Chemicals and Petrochemicals |

| Pharmaceuticals |

| Building and Construction |

| Mining and Minerals |

| Others |

| Up to 500 kg |

| 500 - 1,000 kg |

| 1,000 - 1,500 kg |

| Above 1,500 kg |

| Virgin PP |

| Recycled-content PP |

| UV-stabilized PP |

| Paper-based Composite |

| Bio-based Polymer Blends |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Type | Type A | ||

| Type B | |||

| Type C | |||

| Type D | |||

| By Design Type | U-Panel | ||

| Baffle / Q-Bag | |||

| Circular | |||

| 4-Panel | |||

| Other Designs | |||

| By End-user Industry | Food and Agriculture | ||

| Chemicals and Petrochemicals | |||

| Pharmaceuticals | |||

| Building and Construction | |||

| Mining and Minerals | |||

| Others | |||

| By Capacity | Up to 500 kg | ||

| 500 - 1,000 kg | |||

| 1,000 - 1,500 kg | |||

| Above 1,500 kg | |||

| By Material / Polymer Type | Virgin PP | ||

| Recycled-content PP | |||

| UV-stabilized PP | |||

| Paper-based Composite | |||

| Bio-based Polymer Blends | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the flexible intermediate bulk container market?

The market stands at USD 9.05 billion in 2026 and is projected to reach USD 11.44 billion by 2031 under a 4.82% CAGR trajectory.

Which region leads the flexible intermediate bulk container market?

North America leads with 38.25% share in 2025, helped by strong chemical and agricultural sectors and strict safety regulations.

Which segment is expanding the fastest?

Type D electrostatic-safe bags show the highest 7.53% CAGR as lithium and chemical processors prioritise non-grounded safety solutions.

How are sustainability trends influencing material choices?

Recycled-content polypropylene bags are growing at 8.64% CAGR as brand owners and regulators push circular-economy compliance.

What technological innovations are reshaping the market?

Smart-FIBCs equipped with RFID and IoT sensors are gaining traction, offering real-time tracking and supply-chain transparency.

What risks could restrain future growth?

Volatile polypropylene feedstock pricing and the rise of rigid-IBC rental pools may dampen demand for single-trip FIBCs in certain circuits.

Page last updated on: