Wooden Pallet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

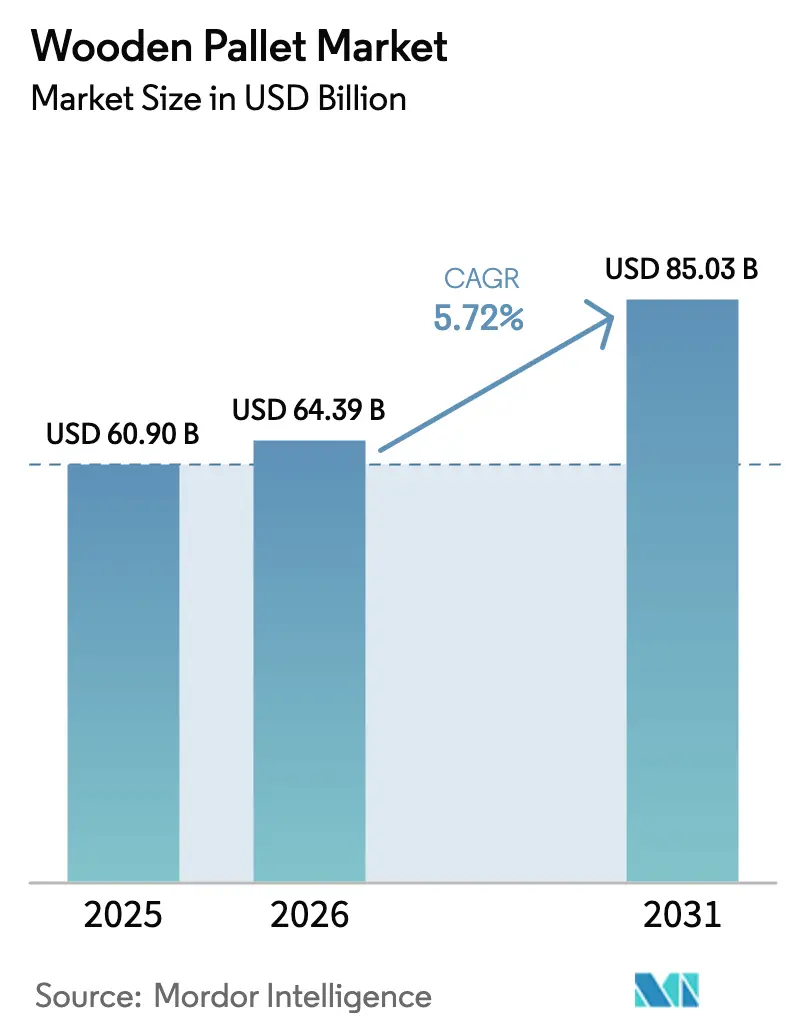

| Market Size (2026) | USD 64.39 Billion |

| Market Size (2031) | USD 85.03 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

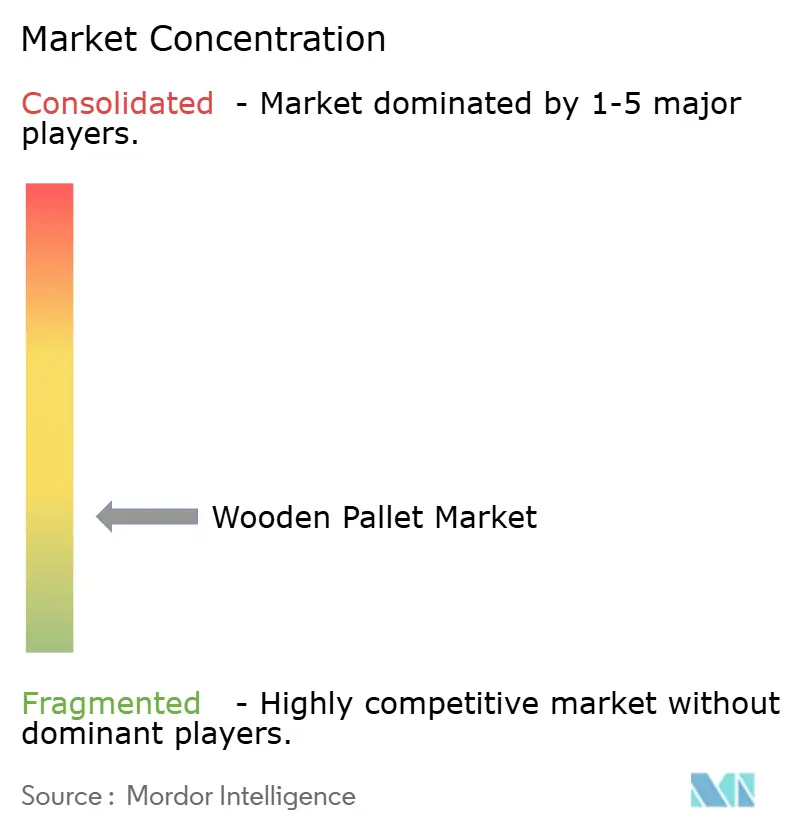

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wooden Pallet Market Analysis by Mordor Intelligence

The wooden pallet market size is expected to grow from USD 60.9 billion in 2025 to USD 64.39 billion in 2026 and is forecast to reach USD 85.03 billion by 2031 at 5.72% CAGR over 2026-2031. This trajectory reflects steady demand from global trade corridors, heightened phytosanitary enforcement, and deepening automation in logistics hubs. Softwood still anchors volume, yet recycled and engineered wood alternatives gain share as circular-economy mandates tighten. ISPM-15 heat-treatment capacity remains an industry linchpin, especially for cross-border food shipments, while proliferating e-commerce across Asia-Pacific forces lightweight designs that lower last-mile cost. Concurrently, Lacey Act scrutiny in North America rewards fully documented timber supply chains, prompting vertical integration and digital traceability investments. Automation-ready block pallets attract premium pricing in high-bay warehouses, and pooling ecosystems proliferate in free-trade zones, compressing ownership costs for manufacturers and retailers.

Key Report Takeaways

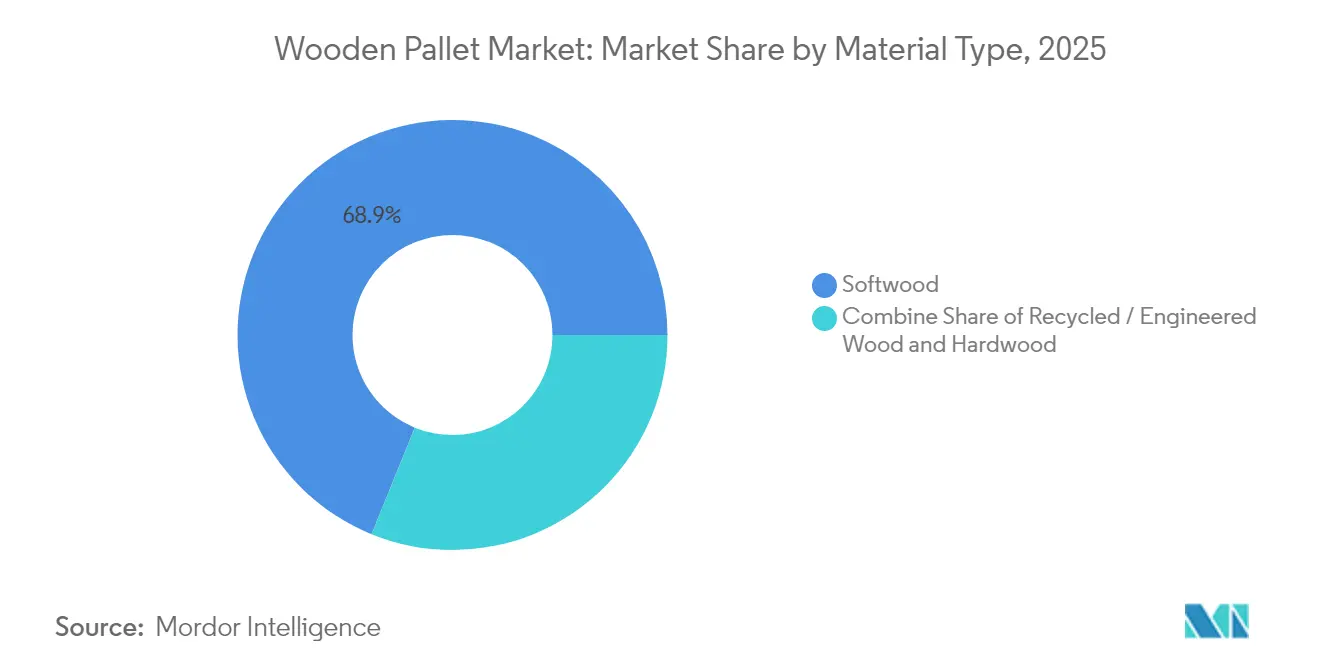

- By material type, softwood led with 68.85% of wooden pallet market share in 2025, while recycled and engineered wood is projected to expand at 7.19% CAGR through 2031.

- By treatment, heat treatment captured 52.05% share of wooden pallet market size in 2025 and is advancing at 7.48% CAGR through 2031.

- By product type, stringer pallets maintained 53.92% share of wooden pallet market size in 2025; block pallets are forecast to grow at 6.74% CAGR through 2031.

- By end-user industry, food and beverages held 33.10% share of wooden pallet market size in 2025, while pharmaceuticals and healthcare is projected to rise at 8.01% CAGR through 2031.

- By geography, Asia-Pacific dominated with a 41.20% revenue share in 2025, whereas the Middle East and Africa region is set to record the fastest 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wooden Pallet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-driven need for cost-optimized last-mile packaging in Asia | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2–4 years) |

| Surge in inter-continental citrus and meat exports requiring ISPM-15 compliant pallets | +0.8% | Global, concentrated in major export hubs | Long term (≥ 4 years) |

| Tightening US-Canada Lacey Act enforcement favoring certified wood-based solutions | +0.6% | North America, indirect impact on global suppliers | Medium term (2–4 years) |

| Retailers’ shift to “fit-for-purpose” SKU-specific pallets in EU grocery chains | +0.4% | Europe, expanding to developed markets | Short term (≤ 2 years) |

| Automation-ready four-way entry demand from high-bay warehouses (Nordics, DACH) | +0.3% | Nordic & DACH regions, spreading to automated markets | Medium term (2–4 years) |

| Growth of pallet-pooling ecosystems across GCC free-trade zones | +0.2% | Middle East, potential expansion to Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce-driven need for cost-optimized last-mile packaging in Asia

Asia-Pacific’s 41.64% stake in the wooden pallet market underscores how regional e-commerce alters pallet specifications. Urban delivery density pushes retailers to favor lighter yet durable pallets that can cycle rapidly through automated sortation centers and cramped retail backrooms. Concurrent cross-border parcel flows compel universal ISPM-15 compliance, so manufacturers experiment with engineered wood that sheds weight without compromising load ratings. This pivot dovetails with omnichannel fulfilment models where the same pallet must tolerate robotic handling in mega-hubs and manual offloading in neighborhood stores. As a result, hybrid stringer-block designs gain traction, reducing materials by up to 12% while maintaining four-way entry functionality.

Surge in inter-continental citrus and meat exports requiring ISPM-15 compliant pallets

Phytosanitary watchdogs credit ISPM-15 with cutting borer infestation at ports by 36–52%. [1]Robert A. Haack, “Effectiveness of ISPM 15 on Reducing Wood Borer Infestation Rates,” PLoS ONE, journals.plos.org Exporters of perishables accept higher pallet treatment costs to avoid shipment rejection, driving the wooden pallet market toward greater certified capacity. Heat-treatment providers capable of real-time temperature logging win multi-year contracts from agri-exporters in Brazil, South Africa, and Spain. Compliance barriers also coax smaller sawmills into co-op models that pool kilns and auditing fees, spreading overhead. With bilateral trade pacts embedding phytosanitary chapters, heat-treated pallets remain the default for inter-continental produce flows well past 2030.

Tightening US-Canada Lacey Act enforcement favoring certified wood-based solutions

Recent prosecutions totaling USD 42 million highlight the financial sting of false timber declarations. [2]National Wooden Pallet and Container Association, “Lacey Act Declaration Requirements for Wood Packaging,” palletcentral.com To mitigate risk, multinationals map supply chains down to forest stand level, integrating RFID tags that cross-reference chain-of-custody certificates when pallets exit sawmills. Canadian wildfire damage-induced supply gaps have cut regional softwood output 25% since 2020, nudging buyers southward into the US Southeast where Lacey documentation requirements remain strict. These dual forces propel the wooden pallet market toward integrated sourcing models, encouraging mergers between lumber mills and pallet fabricators.

Retailers’ shift to “fit-for-purpose” SKU-specific pallets in EU grocery chains

European grocers now dictate bespoke pallet footprints that match automated depalletizers and shelf-ready cartons. Ocado’s nine-block, four-way entry specification illustrates the trend. Manufacturers capable of quick tooling changeovers secure premium contracts, while standardized pooling fleets struggle to justify non-uniform asset returns. The outcome is a tiered wooden pallet market where high-velocity SKUs travel on custom pallets and low-velocity goods continue on classic Euro or stringer designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating lumber price volatility post-2023 wildfire seasons in Canada | -1.1% | North America, global supply chain impacts | Short term (≤ 2 years) |

| Rising regulatory pushback on fumigation chemicals in EU and Oceania | -0.4% | Europe & Oceania | Medium term (2–4 years) |

| Proliferation of reusable plastic pallets in pharma cold-chain in the Nordics | -0.3% | Nordic countries | Long term (≥ 4 years) |

| Limited availability of heat-treatment kiln capacity in Sub-Saharan Africa | -0.2% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating lumber price volatility post-2023 wildfire seasons in Canada

The 2023 fire season released 2.2 billion tons of carbon and wiped out vast Spruce-Pine-Fir acreage, sending prices to USD 550 per thousand board feet in March 2025. Smaller mills without futures hedges struggle to quote steady pallet prices, prompting some buyers to pivot to Southern Yellow Pine. Variable density, however, complicates pallet design tolerances, pushing quality-conscious customers toward larger integrated suppliers able to certify performance despite raw-material substitution.

Rising regulatory pushback on fumigation chemicals in EU and Oceania

Methyl bromide’s phase-out under EU rules forces shippers to heat-treat or explore sulfuryl fluoride alternatives. [3]Federal Agency for the Safety of the Food Chain, “Wood Packaging Material (EU Rules),” fasfc.beHeat-treatment bottlenecks raise lead times during peak export windows, and some perishables shift temporarily to costly plastic pallets when kiln slots run short. Manufacturers across Poland and Spain accelerate kilns expansion, but environmental impact assessments lengthen permitting cycles, delaying relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Softwood pallets dominate but recycled wood gains traction

Softwood pallets carried 68.85% of 2025 shipments due to low weight and mature sawmill networks. Their carbon-sequestering credentials, showcased by Nature’s Packaging campaigns, continue to appeal to eco-audit teams. However, recycled and engineered options now show a 7.19% CAGR, driven by European landfill diversion directives and corporate net-zero commitments. Agriculture-waste solutions such as corn-stover boards debut in Iowa in 2025, signalling material diversification.

Elevated lumber prices accelerate recycled uptake, as remanufactured cores cost 10–15% less than new-wood equivalents. Meanwhile, heavy-duty niches still turn to hardwood for 2-metric-ton loads in metal-fabrication plants. Across the wooden pallet market, procurement briefs increasingly blend cost, load rating, and carbon impact, prompting portfolio approaches where a single shipper might deploy softwood for bulk beverages, recycled cores for intra-plant loops, and hardwood for capital equipment exports.

By Product Type: Block pallets benefit from automation requirements

Stringer styles retained a 53.92% share in 2025, anchored by legacy handling equipment across North American grocery distribution. Yet block designs grow at 6.74% CAGR, dovetailing with high-bay automation rollouts. EPAL’s QR-enabled Euro pallet, launched 2024, couples block geometry with digital ID to lower loss rates.

Warehouses upgrading to shuttle-based retrieval mandate four-way entry to maximize cube utilization, nudging procurement guidelines toward block standards. Consequently, pooling providers renegotiate asset mixes, trimming stringer output by 5% annually while expanding block fleets. In emerging Asian markets, cost sensitivity still props up stringer orders, but localization clauses in robotics contracts suggest a gradual pivot, ensuring both designs coexist through 2030.

By End-user Industry: Pharma and healthcare outpace food and beverages

Food and beverages claimed 33.10% of shipments in 2025 thanks to high-turnover SKUs requiring cost-efficient transport. The wooden pallet market now witnesses pharma and healthcare accelerating at 8.01% CAGR as biologics and vaccine supply chains expand. Studies from the Institute for Wood Technology Dresden highlight wood’s antibacterial activity being 13-times higher than H1 plastic pallets, reinforcing suitability for sterile zones.

Cold-chain nodes deploy certified heat-treated pallets with moisture-resistant coatings to comply with Good Distribution Practice audits. Transportation & warehousing loggers ride the surge of parcel volumes, while automotive remodels pallet specs each fiscal year in response to weight-reduction programmes. Across the wooden pallet industry, segment diversification insulates suppliers from single-sector volatility, underpinning resilient revenue growth.

By Treatment: Heat treatment entrenched as global compliance norm

At 52.05% share in 2025, heat-treated inventory firmly commands export lanes, rising 7.48% through 2031. APHIS port data show continuing seizure of untreated pallets, nudging shippers to pay the USD 2–3 extra for kiln certificates cbp.gov. Methyl bromide fumigation survives only where kiln capacity is inaccessible or product moisture tolerance is low.

Kiln capacity shortages, particularly in Sub-Saharan Africa, delay shipments, prompting multi-stakeholder efforts to deploy modular electric kilns powered by solar mini-grids. Domestically destined goods in the US and China still run untreated when regulations allow, but rising state-level biosecurity bills hint at shrinking tolerance for untreated lumber, suggesting heat treatment’s grip will only tighten.

Geography Analysis

Asia-Pacific generated a 41.20% revenue slice for the wooden pallet market in 2025, reflecting dense manufacturing clusters and double-digit e-commerce penetration. Chinese parcel operators, handling 120 million orders daily, specify four-way entry pallets with sub-19 kg tare weights. India’s government-led logistics corridors further expand demand, while Japan pushes mixed-material pallets that pair softwood decks with plastic blocks for seismic stability.

North America commands value through advanced pooling and stringent compliance. US tariffs that can lift effective Canadian lumber costs by 39.5% accelerate domestic sourcing, and automation expenditure of USD 2.1 billion in 2025 fortifies block-pallet adoption. Europe’s standardization culture keeps EPAL volumes high; however, Brexit complexities necessitate dual-certificate pallets for cross-Channel trade, adding administrative lead time. Nordic automation pioneers enforce ±1 mm tolerance on pallet openings, a spec now echoed in German contracts.

The Middle East and Africa post the fastest 7.22% CAGR as GCC free-trade zones pivot into global consolidation points. Dubai-Riyadh shuttle lanes depend on pooling depots that sharpen asset turns to 4.2 trips per month. Yet, Sub-Saharan exporters still struggle with kiln scarcity, relying on costly imported pallets. South America trails but shows promise, with Mercosur’s harmonized pallet codes trimming customs wait-times by 18%, sparking investment in Brazilian and Argentine facilities.

Competitive Landscape

The wooden pallet market exhibits moderate fragmented; top global pooling firms pair scale with technology while thousands of regional mills cater to proximity-driven demand. CHEP deploys 550,000 autonomous trackers across 30 countries, cutting loss claims by 12% and reinforcing price premiums. 48forty Solutions, spun from CHEP Recycled in March 2025, manages 90 million pallets through 225 facilities, dominating North American refurbishment.

Vertical integration gains momentum: UFP Industries pours capex into automation that halves labor hours per pallet and shields margins against wage inflation. Patent filings for RFID-embedded lumber show innovators eyeing full pallet-level IoT integration. Digitally native platforms such as MagicPallet match surplus and shortage locations inside closed user groups, shrinking empty runs. Regional specialists, for instance PGS Group in Europe, bank on PEFC-certified softwood and fast response times, sustaining niche leadership against global giants.

Smaller mills hedge lumber volatility with multi-year log contracts and invest in kiln expansion, positioning themselves as compliant alternatives to uncertified imports. Meanwhile, sustainability credentials evolve into table stakes: Brambles sourced 100% sustainable timber by 2024 and planted 1.7 million trees, signaling a future where ESG audits influence tender outcomes more than upfront unit cost.

Wooden Pallet Industry Leaders

Falkenhahn AG

CHEP (Brambles Limited)

EXZOD India Private Limited

UFP Industries, Inc.

NEFAB Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CornBoard Manufacturing began constructing a USD 15 million Iowa plant to produce waste-based pallets.

- March 2025: CHEP Recycled completed its transformation into 48forty Solutions, forming North America’s largest pallet management network.

- February 2025: UFP Industries announced new automation investments alongside Q1 2025 earnings.

- November 2024: Brambles divested CHEP India to LEAP India for USD 85 million .

Global Wooden Pallet Market Report Scope

A wooden pallet is typically a form of tertiary packaging that facilitates the handling and transporting of goods and information with labeling and convenience. These pallets are the most common base for the unit load, including the pallet and the goods stacked atop it. They are typically secured by stretch wrap, strapping, shrink wrap, adhesive, pallet collar, and other stabilization means. The wooden pallet market encompasses the qualitative analysis of new and new wood pallets already circulating globally. The countries listed are dynamic based on the current demand status, supply, regulations, and other factors.

The wooden pallet market is segmented by material type (hardwood and softwood), end-user industry (transportation & warehousing, food & beverages, pharmaceuticals, retail, manufacturing, and other end-user industries), and geography (North America [United States and Canada], Europe [France, Germany, Italy, Spain, United Kingdom, and Rest of Europe], Asia-Pacific [China, India, Japan, Australia & New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, Egypt, South Africa, and Rest of Middle East and Africa]). The report offers market forecasts and volume sizes for all the above segments.

| Hardwood |

| Softwood |

| Recycled/ Engineered Wood |

| Stringer Pallets |

| Block Pallets |

| Euro Pallets |

| Custom / Specialty Pallets |

| Transportation and Warehousing |

| Food and Beverages |

| Pharmaceuticals and Healthcare |

| Retail and E-commerce |

| Manufacturing (Automotive, Chemicals, etc.) |

| Other End-user Industry |

| Heat-Treated (ISPM-15) |

| Methyl-Bromide Fumigated |

| Untreated / Recycled |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Hardwood | ||

| Softwood | |||

| Recycled/ Engineered Wood | |||

| By Product Type | Stringer Pallets | ||

| Block Pallets | |||

| Euro Pallets | |||

| Custom / Specialty Pallets | |||

| By End-user Industry | Transportation and Warehousing | ||

| Food and Beverages | |||

| Pharmaceuticals and Healthcare | |||

| Retail and E-commerce | |||

| Manufacturing (Automotive, Chemicals, etc.) | |||

| Other End-user Industry | |||

| By Treatment | Heat-Treated (ISPM-15) | ||

| Methyl-Bromide Fumigated | |||

| Untreated / Recycled | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current wooden pallet market size and growth outlook?

The wooden pallet market size is USD 64.39 billion in 2026 and is forecast to reach USD 85.03 billion by 2031, exhibiting a 5.72% CAGR over 2026-2031.

Which material type leads sales in the wooden pallet market?

Softwood pallets lead with a 68.85% share, although recycled and engineered wood variants are expanding at 7.19% CAGR.

Why are block pallets gaining momentum?

Block pallets support four-way entry, essential for automated high-bay warehouses, and are projected to grow at 6.74% CAGR due to rising automation investments.

Which end-user sector is the fastest-growing?

Pharmaceuticals and healthcare show the quickest expansion at 8.01% CAGR, driven by strict cold-chain and hygiene requirements.

Which region offers the highest growth potential for wooden pallet suppliers?

The Middle East and Africa region is set to record the highest 7.22% CAGR, buoyed by expanding free-trade zones and infrastructure projects.

Page last updated on: