Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

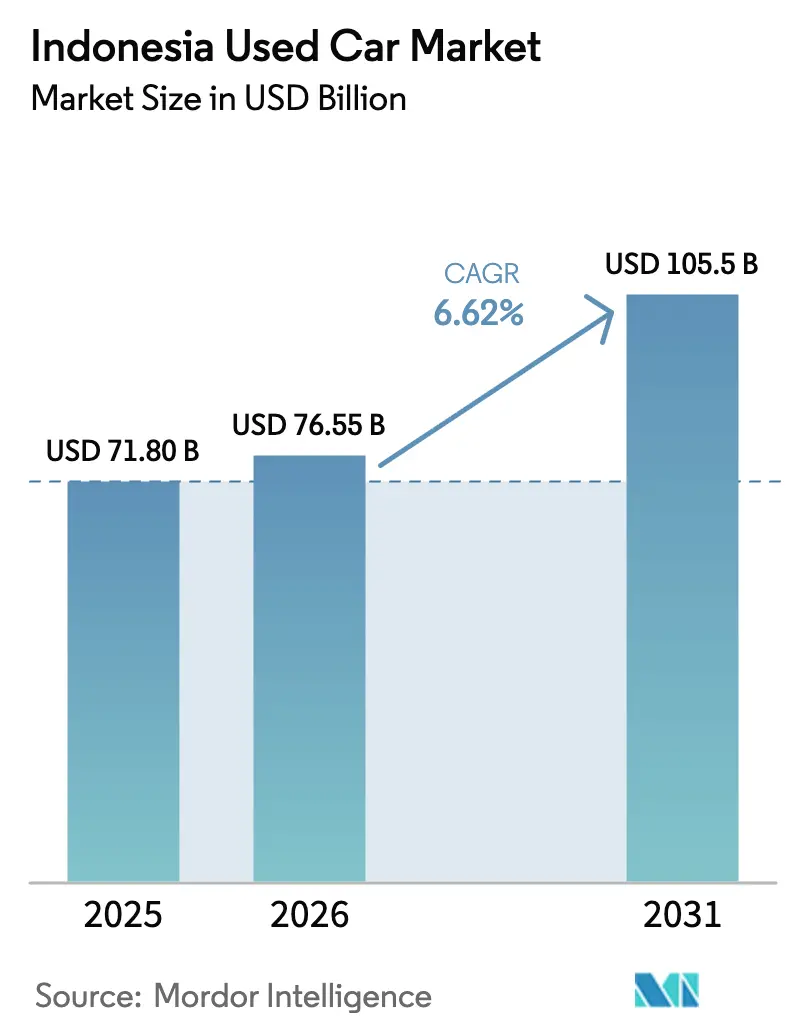

| Base Year Market Size (2025) | USD 71.80 Billion |

| Market Size (2026) | USD 76.55 Billion |

| Market Size (2031) | USD 105.5 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Used Car Market Analysis by Mordor Intelligence

The Indonesia used car market size is expected to grow from USD 71.80 billion in 2025 to USD 76.55 billion in 2026 and is forecast to reach USD 105.5 billion by 2031 at 6.62% CAGR over 2026-2031. Demand resilience reflects a structural tilt toward pre-owned vehicles as tighter credit conditions and waning purchasing power push households to stretch budgets without postponing mobility goals. Used-car financing outpaced new-car loans for the first time in 2024, signalling a lasting recalibration of consumer behavior. Online classifieds now dominate discovery journeys, and emerging AI-grading tools narrow price dispersion by giving buyers objective condition scores. Financing pivots by major banks boost accessibility and margins, while ride-hailing fleet renewals inject a steady stream of high-quality cars into dealer inventories.

Key Report Takeaways

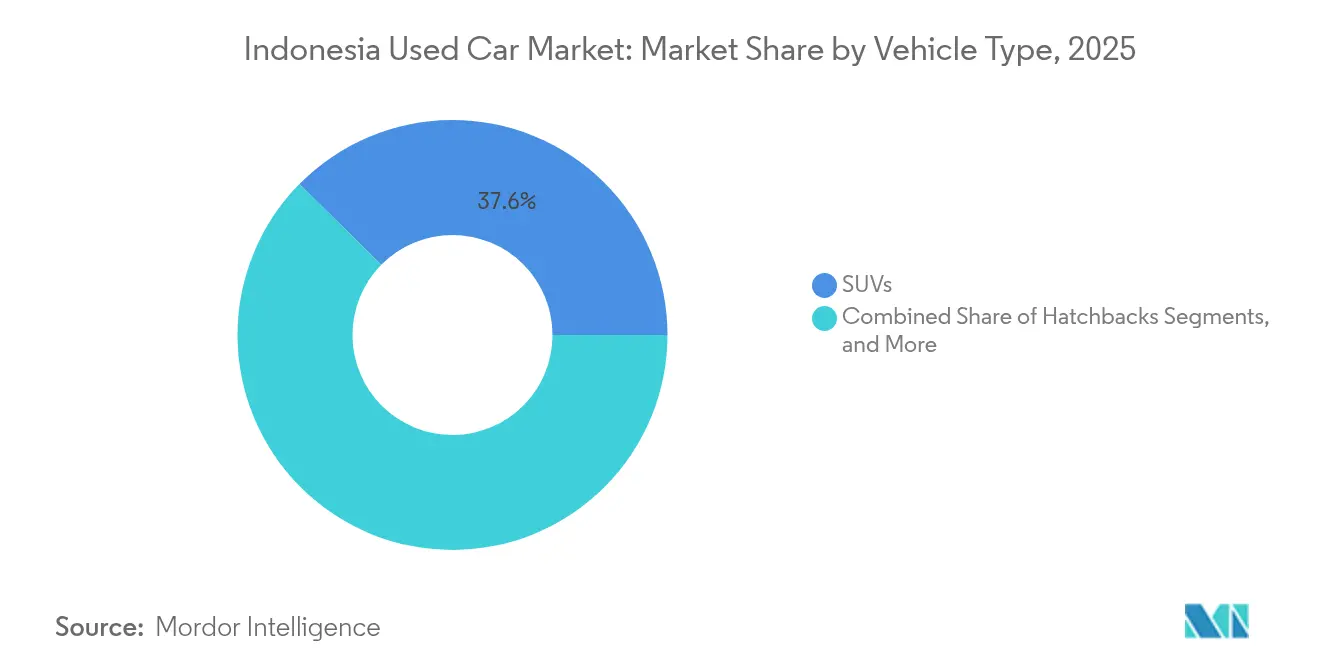

- By vehicle type, SUVs held 37.62% of the Indonesia used car market share in 2025, whereas MPVs are projected to expand at a 7.05% CAGR through 2031.

- By fuel type, petrol models accounted for 63.10% of the Indonesia used car market size in 2025; hybrid and electric vehicles are advancing at a 12.34% CAGR to 2031.

- By price segment, the USD 11,000-21,999 band captured 39.05% of the Indonesia used car market revenue in 2025 and is growing at a 7.33% CAGR through 2031.

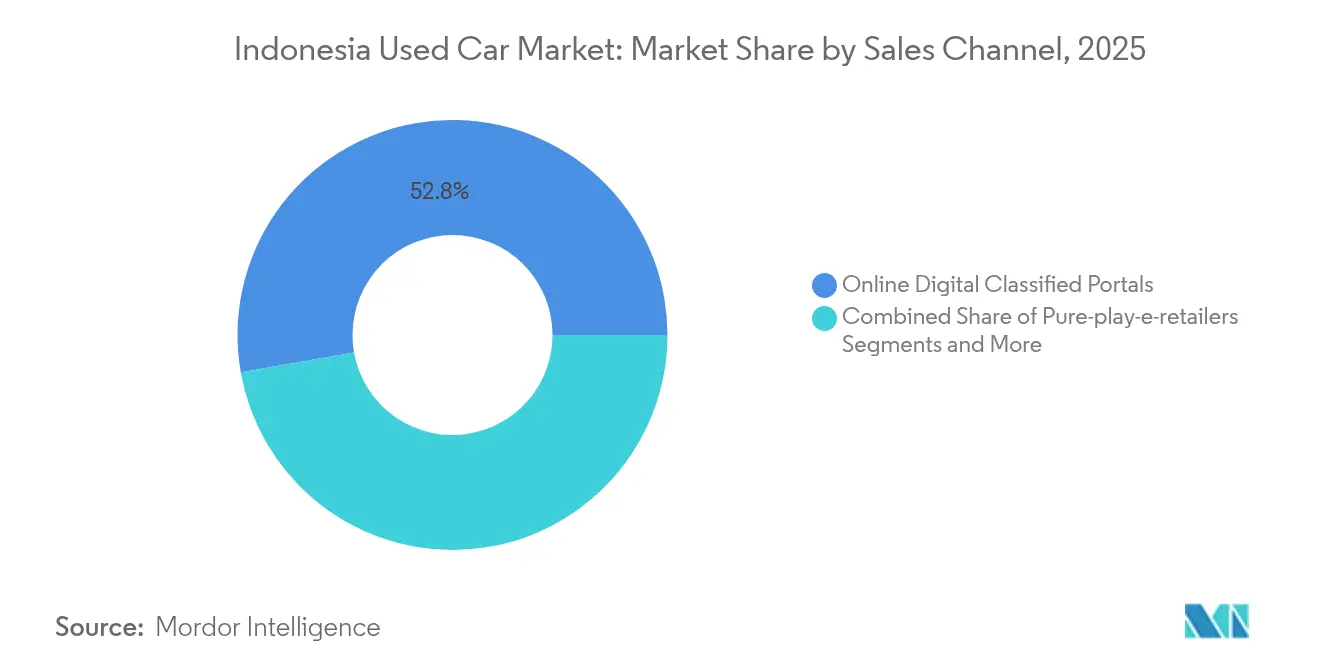

- By sales channel, online digital classified portals accounted for 52.78% of the Indonesia used car market size in 2025; pure-play e-retailers are advancing at a 10.74% CAGR to 2031.

- By vendor type, unorganized dealers retained 66.20% of the Indonesia used car market size in 2025, but organized players are scaling faster with an 8.25% CAGR to 2031.

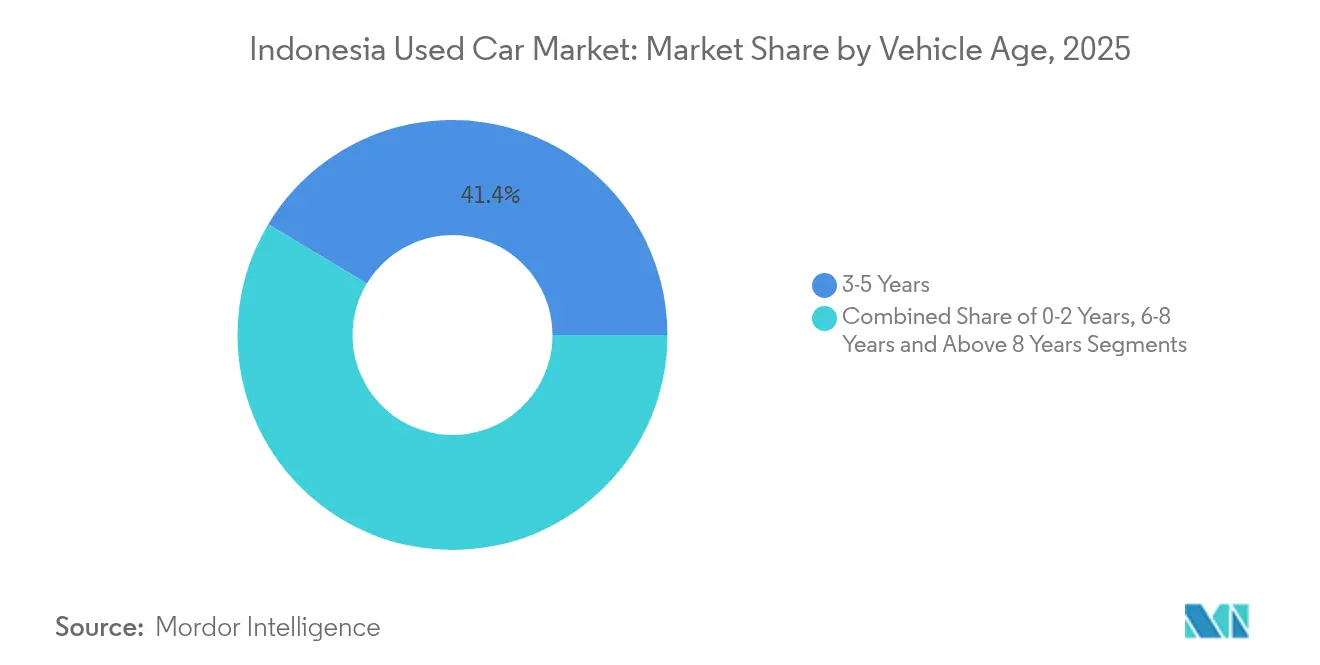

- By vehicle age, 3-5-year-old vehicles accounted for 41.38% share in 2025, whereas 0-2-year-old vehicles are projected to grow at a 7.74% CAGR to 2031.

- By financing providers, banks captured 75.40% of revenue in 2025 and is growing at a 7.19% CAGR.

- By geography, Jakarta commanded 33.20% of revenue in 2025, while North Sumatra is on track for the fastest 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Online Classified, E-retail Activity Grows | +1.8% | National; Java core with Sumatra spillover | Short term (≤ 2 years) |

| Banks' Pivot to Used-car Loans | +1.5% | Jakarta, West Java, East Java | Short term (≤ 2 years) |

| Organized Dealer Network Expansion | +1.2% | Sumatra, Kalimantan, Sulawesi | Medium term (2-4 years) |

| Ride-hailing Fleet Renewal Cycles | +0.9% | Urban centers | Medium term (2-4 years) |

| OEM Buy-back Schemes | +0.7% | National | Long term (≥ 4 years) |

| AI-led Condition Grading | +0.4% | Major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Online Classified and E-retail Activity

Digital portals empower consumers to compare prices, mileage, and photos, streamlining their transactions before reaching out to sellers. Platform operators integrate inspection, financing, and documentation, reducing search friction in secondary cities where dealer density is low. SEVA’s 17,500-unit throughput and IDR 8.2 trillion gross transaction value in 2024 validated the model, encouraging capital inflows and unicorn creation [1]OCBC Ventura, “SEVA Catat Pertumbuhan di Tengah Tren Suram,” OCBCVENTURA.COM. Traditional conglomerates have reacted: Astra’s OLX acquisition aligned captive financing, inspection centers, and logistics into a single stack. Regulatory support from OJK for in-platform digital lending completes a frictionless experience, propelling the Indonesian used car market toward deeper online penetration.

Banks’ Pivot to Used-car Specific Loan Products

Major banks such as BCA expanded vehicle loan books to IDR 65.3 trillion (USD 4.1 billion) in 2024, with used cars forming an increasing share as lenders chase higher yields [2]BCA, “Kredit Kendaraan BCA Naik 14,8%,” BCA.CO.ID. Proprietary scorecards have evolved to incorporate a range of crucial factors, including mileage bands, detailed inspection grades, and projected resale values, moving beyond the traditional focus on borrower income. This innovative approach allows for instant pre-approval within online marketplaces, significantly reducing approval times to just a few hours. As a result, this streamlined process not only enhances conversion rates but also invigorates liquidity in the Indonesian used car market, creating dynamic opportunities for both buyers and sellers.

Expanding Organized Dealer Networks Outside Java

Organized dealers are moving into Sumatra, Kalimantan, and Sulawesi, taking with them standardized 150-point inspections and warranty offers that lift consumer trust [3]PT Toyota Astra Motor, “Ekspansi Dealer Toyota di Daerah,” ASTRA.CO.ID. Toyota-backed outlets illustrate how franchise scale can cut logistics costs and shorten inventory turns. Outer-island consumers, once limited to unorganized yards, now access reliable cars and financing, accelerating motorization where ownership ratios still trail Java. Improved roads and port upgrades lower unit transport costs, enhance margins, and reinforce the growth loop for the organized segment.

Ride-hailing Fleet Renewal Cycles (Grab and Gojek)

Three-year churn cycles release thousands of well-maintained units that carry full service histories, creating premium stock for certified programs. Gojek’s pledge to electrify 100% of its fleet by 2030 implies even larger disposals of gasoline cars mid-decade, bolstering supply in key urban hubs. Fleet cars’ documented upkeep lifts residuals, reducing depreciation shocks for second owners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Odometer and Accident-history Fraud | -1.1% | Nationwide; unorganized yards | Short term (≤ 2 years) |

| Fragmented Provincial Registration Databases | -0.8% | All provinces | Medium term (2-4 years) |

| High Inter-island Logistics Cost | -0.6% | Outer-island flows | Long term (≥ 4 years) |

| Limited Certified Battery Checks | -0.3% | Early EV clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Odometer and Accident-history Fraud Remains Pervasive

Provincial STNK and BPKB systems operate in silos, letting bad actors reset mileage or hide flood damage when vehicles cross borders. First-time buyers and online shoppers bear the brunt, paying inflated prices for compromised cars. Trust deficits raise financing risk premiums, dampening the Indonesia used car market velocity until AI inspection and centralized data become mainstream.

Fragmented Provincial Registration Databases

Transfers between Indonesia’s 34 provinces demand serial paperwork and multiple fees, extending transaction cycles and opening graft windows. Dealers scaling nationally must master disparate rules, pushing overheads that unorganized sellers often circumvent. The administrative drag curbs inter-provincial trade, limiting demand pooling and sustaining regional price divergence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Lead Despite MPV Momentum

SUVs owned 37.62% of the Indonesia used car market share in 2025, buoyed by high ground clearance and perceived safety in congested streets. MPVs, climbing at 7.05% CAGR, appeal to multi-generational households that prize sliding doors and flexible seating. Sedans cater to commuters seeking fuel efficiency, and hatchbacks target first-time owners navigating tight parking norms. The Indonesia used car market size for SUVs is projected to keep pace with robust supply from fleet replacements, yet MPVs fetch quicker days-to-sale in suburban Java as school-run demand rises. Chinese OEMs have entered both segments with competitive hybrid trims, pushing Japanese incumbents to refresh line-ups more frequently.

New-energy SUVs feed aspirational buyers in Jakarta and Surabaya, while compact MPVs dominate outer-island lanes where road quality varies. Digital platforms algorithmically recommend SUVs to ride-hailing prospects and MPVs to growing families, increasing match efficiency. Certified programs overweight SUVs and MPVs because warranty upsells monetize better than sedans.

By Fuel Type: Petrol Dominance Faces Electric Disruption

Petrol models still command 63.10% of the Indonesia used car market size in 2025, yet hybrids and electric models exhibit a 12.34% CAGR, propelled by VAT cuts and zero luxury tax. The diesel share erodes amid rising subsidy talk and emissions scrutiny. The Indonesia used car market size for electric models remains small, but fast-charger rollouts and government roadmaps catalyze future secondary sales. Residual values of hybrids have outperformed petrol peers in Jakarta auctions by 6-8% since 2024, hinting at shifting buyer calculus.

Battery degradation uncertainty curbs wider uptake. Dealers hesitate to stock older BEVs without OEM testing. Banks apply shorter tenures and higher collateral haircuts for BEVs pending battery warranties. Petrol cars, however, keep liquidity advantages in rural exchanges where charging remains scarce.

By Price Segment: Mid-Range Vehicles Dominate Market

Units priced USD 11,000-21,999 held 39.05% of the Indonesia used car market revenue in 2025 and expanded at 7.33% CAGR, aligning with median household affordability and bank lending brackets. Entry models under USD 5,500 attract cash buyers in tier-3 cities, while premium brackets above USD 22,000 serve affluent urbanites eyeing luxury badges. The Indonesia used car market share of mid-range vehicles benefits from abundant trade-ins and certified programs bundling one-year warranties.

Online calculators showcasing installment scenarios boost mid-range visibility: a USD 15,000 Avanza with a 20% down payment and a 48-month tenor remains the most-searched combination on leading portals. Growth in premium slices rides on expatriate turnovers and corporate fleet disposals, but remains niche relative to value-centric core segments.

By Sales Channel: Digital Platforms Reshape Distribution

Digital classifieds captured 52.78% of the Indonesia used car market share in 2025, while pure-play e-retailers show the fastest 10.74% CAGR. Franchise dealers safeguard relationships via omnichannel models offering test drives at home, but independent lots rely on community ties and negotiable payment plans. Auction hybrids liquidate fleet turnovers rapidly, reinforcing wholesale price discovery. The Indonesian used car market size transacted online will keep expanding as lenders embed APIs for real-time credit scoring.

Modern physical showrooms are evolving into crucial last-mile fulfillment centers for vehicle buyers who have already narrowed down their choices online. Utilizing advanced geo-fencing technology, online platforms now allow potential buyers in Jakarta to access vehicle listings from depots located within a convenient 30-kilometer radius. This innovation significantly reduces the time and effort required for in-person inspections, enhancing the overall shopping experience and driving higher conversion rates for dealerships.

By Vendor Type: Organized Segment Gains Ground

Unorganized sellers still account for 66.20% of the Indonesia used car market revenue in 2025, yet organized channels grow at 8.25% CAGR with scale advantages in inspection, refurbishment, and financing tie-ups. For consumers, a three-day return policy and fixed-price transparency offset slight price premiums, driving repeat purchase intent. The Indonesia used car market size handled by organized dealers has tripled since 2019 as pandemic-era hygiene concerns nudged buyers toward professional outfits.

Institutional investors are increasingly drawn to asset-light online dealers that strategically outsource their refurbishment processes to partner workshops. This approach allows them to conserve capital, which can then be allocated towards robust marketing initiatives and maintaining an adequate inventory float. Additionally, franchise models provide small, family-owned dealerships with valuable branding opportunities and access to advanced technological platforms. This not only enhances their operational efficiency but also accelerates their journey towards formalization in a competitive marketplace.

By Vehicle Age: Prime Years Drive Demand

Models aged 3-5 years controlled 41.38% of the Indonesia used car market share in 2025 as buyers seek depreciation sweet spots with modern infotainment and safety tech. Nearly-new 0-2 year vehicles clock the fastest 7.74% CAGR, thanks to ride-hailing disposals and OEM buy-backs. The Indonesia used car market share for 6-8 year cars holds as cost-focused rural demand persists. Age dictates financing tenor caps: banks typically cap 0-2 year cars at 60 months, 3-5 year at 48 months, and 6-8 year at 36 months, shaping affordability outcomes.

Fleet-grade maintenance histories keep turnover swift in the 0-5 year bracket, while older stock faces lengthier lot times and higher reconditioning budgets. AI-based condition scoring helps older vehicles find price-appropriate buyers faster.

By Financing Providers: Banks Maintain Leadership

Banks possessed 75.40% of the Indonesia used car market share during 2025 and are projected to expand to a 7.19% CAGR by 2031, leveraging branch reach, low funding costs, and bundled insurance. NBFCs cherry-pick self-employed customers that banks view as higher risk but price loans 150-250 bps higher. OEM captives entice switchers with loyalty rebates and bundled maintenance. Indonesia's used car market size, financed via digital channels, surged after banks embedded instant approvals in marketplace apps.

Risk-based pricing aligns interest rates with inspection grades, incentivizing buyers to opt for certified vehicles. Delinquency ratios remain manageable at 1.9% versus 3.4% for new-car portfolios, underscoring improved collateral valuation algorithms.

Geography Analysis

Jakarta delivered 33.20% of the Indonesia used car market revenue in 2025, fueled by high per-capita income, dense dealer grids, and mature credit infrastructure. Average ticket values surpass national norms by 22% as buyers favor late-model SUVs. Competition compresses gross margins, spurring players to scout spillover demand into satellite cities like Depok and Tangerang.

West Java and East Java enjoy deep manufacturing linkages that create steady trade-in flows and ready access to service centers. Road and rail connectivity keeps logistics costs low, supporting brisk turnover. Central Java’s emerging industrial zones bolster middle-class formation, widening the customer base for value-oriented MPVs.

North Sumatra’s 6.74% CAGR to 2031 illustrates the archipelago’s diversification. Medan’s logistics hub status draws organized dealers building multi-brand superstores. Province-level incentives for digital startups streamline e-retail expansion, narrowing price gaps with Java. Other outer-island provinces like South Sulawesi and East Kalimantan grow from small bases as mining and plantation booms lift purchasing power, though high shipping costs still temper cross-island arbitrage.

Competitive Landscape

Competition is intensifying as incumbents and tech disruptors vie for a share in a market where unorganized lots still dominate volumes. Astra, leveraging its Toyota distributorship, now controls inspection centers, finance arms, and OLX’s digital reach, forging a closed ecosystem difficult to replicate. The Indonesia used car market rewards platforms that integrate credit, warranty, and logistics; hence, vertical consolidation is accelerating.

Specialists target pain points: Autopedia’s AI grading underpins financing risk models; logistics start-ups trial roll-on-roll-off aggregation to slash inter-island costs; and battery analytics firms prepare for looming second-life EV demand.

Foreign entrants such as CARS24 leverage global data pools to refine Indonesian residual curves, but must localize inspection to account for climate-induced corrosion and road conditions. Regulatory oversight by OJK supports fintech innovation yet compels greater consumer disclosure, raising compliance barriers for small dealers.

Indonesia Used Car Industry Leaders

OLX Indonesia

Toyota Astra Motor (Toyota Trust)

Carro Indonesia

Carsome Indonesia

Mobil88 (PT Serasi Auto Raya (SERA))

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Astra and Toyota have expanded their alliance as Toyota Motor Asia acquired 40% of PT Astra Digital Mobil for USD 120 million to enhance certified used car operations across Indonesia.

- December 2024: CarDekho’s South Asia division raised USD 60 million, led by Navis Capital and Dragon Fund, to expand used-vehicle financing in Indonesia and the Philippines.

Indonesia Used Car Market Report Scope

The Indonesian used car market refers to the segment of the automotive industry that involves the buying, selling, and trading of pre-owned vehicles in Indonesia. It encompasses a wide range of vehicles, including sedans, hatchbacks, SUVs, and vans, that have been previously owned and used by individuals or businesses.

Indonesia used car market is segmented by vehicle type, booking channel, financing providers, and province. By vehicle type, the market is segmented as the hatchback, sedan, sport utility vehicle (SUV), and multi-purpose vehicle (MPV). By booking channel, the market is segmented as online, OEM certified/authorized dealerships, and multi-brand dealerships. By financing providers, the market is segmented as OEMs, banks, and non-banking financial companies, and by province, the market is segmented as West Java, East Java, Central Java, North Sumatra, Banten, and Other Provinces.

The report offers market size and forecasts for all the above segments in value (USD).

By Vehicle Type

| Hatchbacks |

| Sedans |

| SUVs |

| MPVs |

By Fuel Type

| Petrol |

| Diesel |

| Hybrid and Electric |

| Others (LPG, CNG, etc.) |

By Price Segment

| Below USD 5,500 |

| USD 5,500 – 10,999 |

| USD 11,000 – 21,999 |

| ≥ USD 22,000 |

By Sales Channel

| Online Digital Classified Portals |

| Pure-play e-Retailers |

| Dealer/OEM Online Platforms |

| Physical Franchise Dealerships |

| Independent Used-Car Lots |

| Auction Houses (Physical and Online Hybrid) |

| Peer-to-Peer (Private) Sales |

By Vendor Type

| Organized |

| Unorganized |

By Vehicle Age

| 0 – 2 Years |

| 3 – 5 Years |

| 6 – 8 Years |

| Above 8 Years |

By Financing Providers

| Original Equipment Manufacturers (OEMs) |

| Banks |

| Non-Banking Financial Companies |

By Province

| West Java |

| East Java |

| Central Java |

| North Sumatra |

| Banten |

| Jakarta |

| Other Provinces |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| SUVs | |

| MPVs | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid and Electric | |

| Others (LPG, CNG, etc.) | |

| By Price Segment | Below USD 5,500 |

| USD 5,500 – 10,999 | |

| USD 11,000 – 21,999 | |

| ≥ USD 22,000 | |

| By Sales Channel | Online Digital Classified Portals |

| Pure-play e-Retailers | |

| Dealer/OEM Online Platforms | |

| Physical Franchise Dealerships | |

| Independent Used-Car Lots | |

| Auction Houses (Physical and Online Hybrid) | |

| Peer-to-Peer (Private) Sales | |

| By Vendor Type | Organized |

| Unorganized | |

| By Vehicle Age | 0 – 2 Years |

| 3 – 5 Years | |

| 6 – 8 Years | |

| Above 8 Years | |

| By Financing Providers | Original Equipment Manufacturers (OEMs) |

| Banks | |

| Non-Banking Financial Companies | |

| By Province | West Java |

| East Java | |

| Central Java | |

| North Sumatra | |

| Banten | |

| Jakarta | |

| Other Provinces |

Key Questions Answered in the Report

What is the projected value of Indonesia’s used-car trade in 2031?

The Indonesia used car market size is expected to reach USD 105.5 billion by 2031.

How fast is the organized dealer segment growing?

Organized vendors are expanding at an 8.25% CAGR, outpacing unorganized lots.

Which vehicle types are gaining the most traction among Indonesian buyers?

SUVs lead by share at 37.62% in 2025, while MPVs post the fastest 7.05% CAGR due to family-centric demand.

Why are banks focusing more on pre-owned car financing?

Used-car loans offer higher margins and now account for 75.40% of financed transactions, supported by refined risk models.

Page last updated on: