Indonesia Construction Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

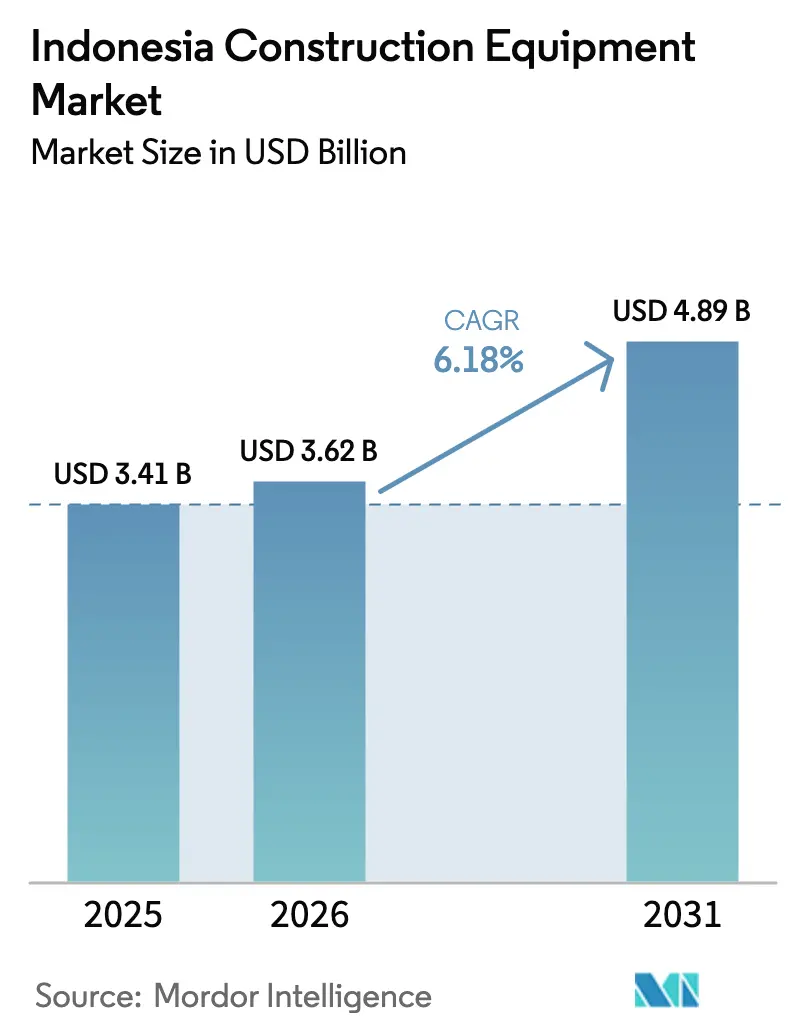

| Base Year Market Size (2025) | USD 3.41 Billion |

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 4.89 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

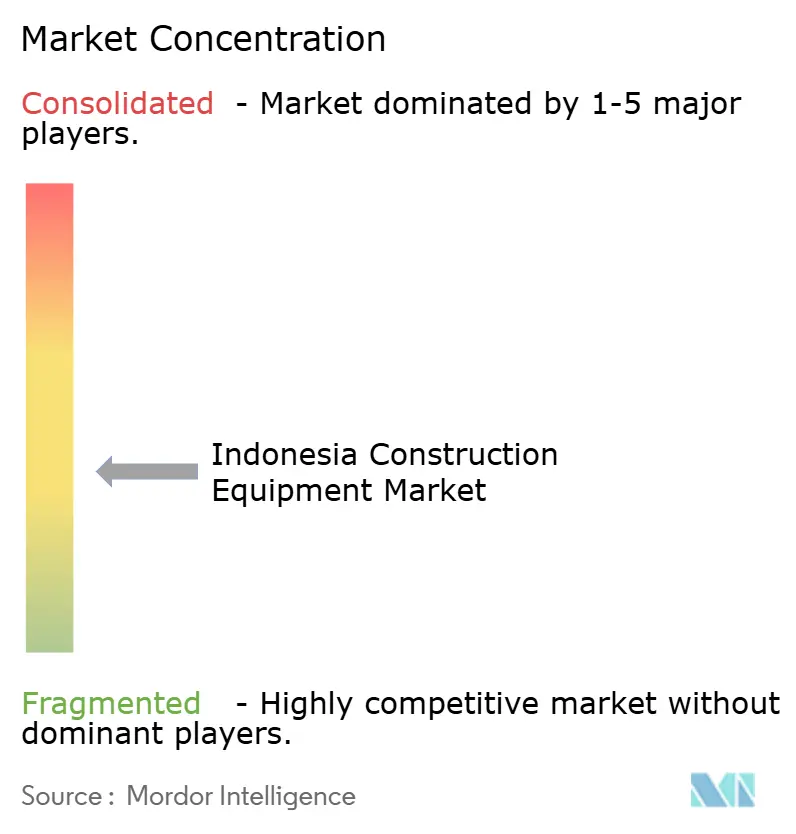

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Construction Equipment Market Analysis by Mordor Intelligence

The Indonesia Construction Equipment Market size was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 4.89 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). Continued implementation of the Proyek Strategis Nasional (PSN) pipeline, the USD 35 billion New Capital City (IKN) program, and resilient mining investment jointly anchors demand across earth-moving, material-handling, and specialized machinery categories. Suppliers that blend local assembly, flexible financing, and telematics services are best positioned to capitalize on utilization rates in Jakarta-centric fleets.

Key Report Takeaways

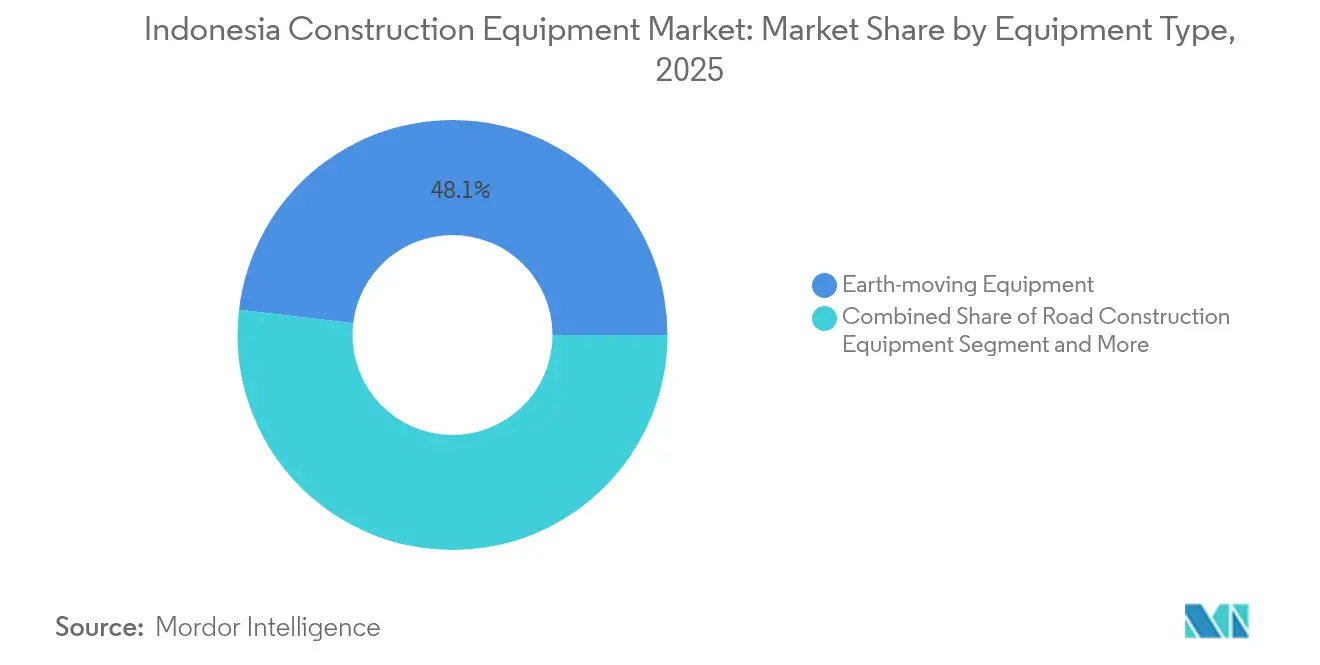

- By equipment type, earth-moving equipment led with 48.12% of Indonesia's construction equipment market share 2025, while material-handling equipment is expected to log the fastest 7.32% CAGR through 2031.

- By drive type, hydraulic systems held 84.55% share of the Indonesian construction equipment market size in 2025; electric/hybrid units are projected to expand at a 6.45% CAGR by 2031.

- By power output, the 101–200 kW segment accounted for 34.66% of the Indonesian construction equipment market size in 2025; sub-100 kW models will advance at a 6.78% CAGR to 2031.

- By end-user, infrastructure and real-estate contractors commanded 41.72% revenue in 2025, whereas manufacturing facilities show the highest 6.84% CAGR outlook.

- By application, transportation projects generated 38.22% of revenue in 2025, and warehouse construction is forecast to post a 7.10% CAGR through 2031.

- By region, Java dominated with 57.05% revenue share in 2025, while Kalimantan is poised for a 6.28% CAGR supported by mining and IKN works.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Public-Sector Spend | +1.8% | National, with concentration in Java and Sumatra | Long term (≥ 4 years) |

| Rapid Urban Rail & Toll-Road Build-Outs | +1.2% | Java, Sumatra, with spillover to Kalimantan | Medium term (2-4 years) |

| Commodity Super-Cycle Fueling Mining-Sector | +1.1% | Kalimantan, Sulawesi, Papua | Medium term (2-4 years) |

| E-Commerce Warehousing Boom | +0.9% | Java core, expanding to major urban centers nationwide | Short term (≤ 2 years) |

| ASEAN-Wide Supply-Chain Re-Shoring into Indonesia | +0.7% | Java, Batam, emerging industrial zones in Sumatra | Medium term (2-4 years) |

| Carbon-Credit Incentives Pushing Contractors Toward Electric/Hybrid Fleets | +0.4% | National, with early adoption in Java industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Public-Sector Spend on Indonesia’s 2030 Infrastructure Vision

Indonesia’s 41 final-stage PSN schemes require uninterrupted equipment deployment across toll roads, dams, ports, and industrial parks. Every rupiah spent on infrastructure has generated 1.9 rupiah in economic value, reinforcing procurement budgets for contractors and rental houses. The multiplier appears strongest in economic zones and power projects, prompting nationwide demand peaks rather than the historical Java concentration. North Sumatra and South Sulawesi have posted the sharpest output lifts, turning each province into a regional rental hotspot. Longer project pipelines permit suppliers to structure five- to seven-year maintenance contracts, locking in parts and service revenue throughout machine life cycles.

Rapid Urban Rail & Toll-Road Build-Outs Driving Earth-Moving Fleet Renewal

Completed in 2024, the Cimanggis–Cibitung Toll Road exemplifies high earth-moving intensity, with significant deployment of excavators and dump trucks during peak construction. On-site digital monitoring at the Karangjoang–Kariangau Section 3A helped reduce equipment idle time significantly while improving utilization rates—highlighting the growing importance of telematics integration. Contractors adopting precision guidance systems are seeing notable gains in fuel efficiency and operational speed. These practices are now being extended by provincial authorities to infrastructure corridors like Parapat in North Sumatra, indicating that technology-driven upgrades are expanding beyond Java. With stricter emission norms tightening around aging Tier 2 equipment, contractors are increasingly turning to cleaner, low-hour Tier 3 and hybrid machines.

E-Commerce Warehousing Boom Lifting Demand for Material-Handling Equipment

Indonesia’s digital-economy surge has turned logistics real estate into a priority asset class. Fulfilment hubs require narrow-aisle reach trucks, automated storage and retrieval cranes, and battery-electric forklifts compatible with warehouse-management systems. Logistics costs already retreated to decent amount of GDP in 2023, yet handling still absorbs 9% of the bill, signaling headroom for mechanization.[1]“Annual Report 2024,” PT Pelabuhan Indonesia, pelindo.co.id Pelindo’s port merger trimmed vessel dwell time, driving uptake of rubber-tyred gantries and remote-controlled ship-to-shore cranes at Tanjung Priok. E-commerce operators insist on 24/7 uptime, pushing rental providers to guarantee multi-shift coverage with quick-swap lithium-ion battery packs.

Commodity Super-Cycle Fueling Mining-Sector Capex in Kalimantan

High-grade nickel, coal, and copper projects sustain a heavy-plant procurement cycle distinct from civil construction rhythms. Thiess’s six-year Kapuas Bara Utama contract alone mobilizes more than 250 large dozers, rigid trucks, and blasthole drills beginning in 2025.[2]“Contract Award for Kapuas Bara Utama,” Thiess, thiess.com CIMIC’s Vale infrastructure mandate layers additional demand for articulated haulers and high-torque excavators suited to laterite terrain. Peripheral townships need roads, water, and power networks, creating secondary orders for graders, compactors, and concrete pumps. Regional authorities fast-track approvals to synchronize with IKN milestones, compressing delivery schedules and elevating the rental premium on late-model 300-tonne excavators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Rupiah Elevating Imported Equipment Prices | -0.8% | National, with higher impact on import-dependent regions | Short term (≤ 2 years) |

| Project Execution Delays | -0.6% | National, with acute impact in densely populated Java | Medium term (2-4 years) |

| Fragmented Rental Ecosystem | -0.4% | National, with acute impact in outer islands and remote regions | Medium term (2-4 years) |

| Persistent Skills Gap in Advanced Machine-Control Operation | -0.3% | National, with higher impact in emerging technology adoption areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Rupiah Elevating Imported Equipment Prices & Financing Costs

Capital-goods imports form a significant share of Indonesia’s trade basket, exposing contractors to foreign-exchange swings that erode purchasing budgets by quarter-points in weeks. Letters of credit add cost buffers, while local content mandates complicate specification choices for global brands. Trade Ministerial Regulation No. 8/2024 streamlines port clearance, yet currency risk persists, prompting equipment financiers to tighten loan-to-value ratios for smaller firms. Dealers increasingly bundle dollar-indexed parts contracts with rupiah-denominated machine loans, reducing mismatch but raising documentation overheads. Local assembly in Batam and Cikarang mitigates exposure, though Tier 4F engine imports remain priced in USD.

Project Execution Delays Tied to Land-Acquisition Bureaucracy

The eight-year gestation of the Cimanggis–Cibitung Toll Road showcased how fragmented land titles elongate mobilization windows, depressing annual fleet utilization. PPP sponsors face multipart approval loops despite viability-gap sweeteners, complicating deployment timelines for core fleet assets. Large conglomerates absorb the delays by rotating equipment among sites, but micro-contractors lack the geographic spread, forcing premature idling. Ministry-level task forces now monitor parcel clearing in real time, yet densely populated Java still reports right-of-way resolution at half the target pace. Schedule volatility filters into rental pricing, inserting risk premiums on monthly standby clauses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Earth-Moving Leadership Faces Material-Handling Disruption

Earth-moving machinery generated more than a billion USD within the Indonesian construction equipment market in 2025, translating into a 48.12% share amid a surge of PSN and mining groundwork. Motor graders, crawler excavators, and articulated haulers form the backbone of toll-road and dam packages, while batching plants and crushing units round out larger EPC scopes. Advanced telematics now track idle fuel-burn and undercarriage wear, nudging contractors to upgrade older Tier 2 models ahead of emission mandates.

Material-handling equipment contributed significant share and is expanding at a 7.32% CAGR, propelled by warehouse automation and port modernization. Forklifts with lithium-ion packs enable triple-shift operations without battery swaps, cutting downtime by 25%. At Tanjung Priok, remote-operated quay cranes improve berth productivity, driving follow-on orders from Tanjung Perak and Kijing.

By Drive Type: Hydraulic Systems Sustain Dominance While Hybrids Advance

Hydraulic platforms captured 84.55% revenue in 2025, underpinned by cost-performance equilibrium and familiarity among Indonesian operators. Suppliers refine spool-valve tuning and energy-recovery circuits to cut fuel consumption by 8% without shifting working habits. Remote drilling projects value hydraulic robustness over electrical complexity, sustaining replacement demand in 100 km-plus radius mines.

Electric and hybrid variants, although only 4,200 units on rent today, post a 6.45% CAGR backed by carbon-credit incentives and 10% VAT discounts on locally contented EVs. Pilot retrofits on 20-tonne excavators show operating-cost drops of 30 basis points per cubic meter moved. Contractors adopting hybrids often secure preferential scoring in public tenders aligned with CCS/CCUS compliance. Financing bundles include green-label asset-backed securities, trimming coupon spreads versus conventional loans, and nudging adoption into mainstream bids for 2027 onward.

By Power Output: Mid-Range Versatility Anchors Fleet Planning

Machines in the 101–200 kW bracket held 34.66% of Indonesia's construction equipment market size in 2025, balancing digging power with transportability for island-hopping projects. Rental houses favor this bracket to ease redeployment between urban rail cut-and-cover jobs and dam spillway digs. Telematics benchmarks reveal that these units transport the lowest cost per engine hour at 80% load factors.

Sub-100 kW equipment advances at 6.78% CAGR as municipalities restrict axle loads and noise levels in CBD zones. Compact excavators below 35 kW now feature zero-tail-swing designs critical for Jakarta MRT extension shafts. Conversely, 201–400 kW bulldozers remain indispensable for Kalimantan’s overburden stripping, while above 400 kW class serves niche pipelines such as highwall mining and tall-pier bridge projects over the Mahakam River. OEMs increasingly offer modular powerpacks so contractors can upsize or downsize horsepower at overhaul intervals rather than purchase new frames.

By End-User: Contractors Hold Sway as Manufacturing Accelerates

Infrastructure and real-estate firms retained 41.72% revenue in 2025, owning much of the heavy civil backlog rewired into the PSN roadmap. Their cross-province portfolios allow locomotive and earth-moving fleets to circulate across toll-road contracts, maintaining utilization above 85%. Integrated conglomerates-housing development, cement production, ready-mix supply-leverage in-house equipment pools to squeeze cost curves.

Manufacturing and industrial facilities report the highest 6.84% CAGR, buoyed by supply-chain reshoring and industrial-park rollout. The 4,300-hectare KITB complex in Central Java anchors automotive and equipment parts clusters, attracting presses and lift-and-carry equipment built to precision tolerances. Electronics and glass producers demand dust-controlled construction zones, raising the use of electric skid-steer loaders that cut particulate emissions. Industrial tenants lock contracts early, giving equipment suppliers forward visibility and enabling customized preventive-maintenance regimens embedded in lease agreements.

By Application: Transport Projects Dominate While Warehouses Surge

Transport and infrastructure packages booked 38.22% revenue in 2025, powered by 20,000 km of toll-road objectives and double-track rail extensions across Java and Sumatra. Contracts typically bundle bridge erection, piling rigs, and concrete pumps, smoothing demand across equipment classes. Segment scheduling uses 24-hour shifts, elevating the preference for premium machines with uptime records above 95%.

At 7.10% CAGR, warehouse construction rises on e-commerce growth and the cold-chain upgrade for agrifood exports. High-bay racks exceeding 30 m require specialized articulated booms and narrow-aisle pickers. Data centers built in Greater Jakarta add orders for precision lifting and generators with ISO-Class 8 clean-room compatibility. Residential and commercial builds still claim sizable volumes, but value per unit lags the logistics segment.

Geography Analysis

Java maintains its status as the epicenter of the Indonesian construction equipment market, accounting for 57.05% share in 2025 and posting dense deployment across Jakarta, Bandung, and Surabaya corridors. High-rise commercial builds, MRT tunneling, and port expansions converge within short transport radii, pushing rental utilization to 92% and elevating spot rates for 20-tonne excavators by 11% over the year. The government’s Trans-Java toll program feeds steady orders for graders and asphalt pavers. At the same time, industrial estates from Bekasi to Karawang require forklifts and reach-stackers compatible with automated storage systems.

Kalimantan is the fastest-growing territory at a 6.28% CAGR through 2031. The IKN Nusantara mega-project accelerates earth-moving starts, with early civil packages issuing tenders that specify equipment idle-time tracking via telematics. Simultaneously, the region’s mining renaissance sustains demand for 100–400 tonne class trucks and 5 m³ wheel loaders. Balikpapan port upgrades complement this cycle, needing cranes and pile-drivers tailored to soft soil. Suppliers that build local rebuild centers capture parts revenue otherwise lost to Java’s entrenched distribution network.

Sumatra, Sulawesi, Papua, and Maluku collectively contribute the remaining market and present differentiated growth vectors. Sumatra benefits from the Trans Sumatra Toll Road development and the Kuala Tanjung-Indrapura-Tebing Tinggi-Parapat project with Rp 13.77 trillion, creating sustained equipment demand for transportation infrastructure. Sulawesi’s nickel and cobalt corridors invite heavy shovels and long-reach excavators for laterite handling.

Competitive Landscape

The Indonesian construction equipment market reflects moderate fragmentation as multinational OEMs, regional assemblers, and rental specialists contest a customer base that ranges from EPC conglomerates to family-run contractors. Caterpillar leverages manufacturing plants in Cileungsi and Batam to localize popular D6 and 320 series models, hedging against currency volatility and meeting local-content quotas. Komatsu partners with United Tractors to re-engineer hydraulic digs for coal seams unique to Kalimantan, capturing share through an extensive remanufacturing program that trims lifecycle costs.

LiuGong’s dispatch of 30 units to Merauke in December 2024 underlines Chinese OEMs’ strategy of rapid delivery to underserved eastern provinces. Hitachi and JCB pursue telematics-driven service contracts, promising 95% uptime or penalty rebates that resonate with schedule-sensitive rail jobs. Domestic fabricators such as PT Pindad replicate articulated dump-truck frames, targeting niche military engineering and disaster-relief opportunities and signaling gradual import substitution at the low-horsepower end.

Rental houses fill allocation gaps; PT Mulia Rentalindo Persada operates a 700-unit, multi-brand fleet with centralized asset tracking, serving PSN and mining accounts. Telematics overlays show fleet-wide idle running at 18% versus the industry’s 25%, illustrating efficiency gains that outcompete one-machine owner-operators. Digital platforms trial peer-to-peer equipment sharing, but regulatory clarity on insurance and inspection standards remains a hurdle, maintaining an advantage for professionally managed rental conglomerates.

Indonesia Construction Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery Co., Ltd.

SANY Heavy Industry Co., Ltd.

Zoomlion Heavy Industry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Thiess secured a USD 330 million mining contract for the Kapuas Bara Utama project in Central Kalimantan, covering site establishment and overburden removal over six years.

- December 2024: LiuGong deployed 30 construction equipment units in Merauke to support food security and local development initiatives.

- May 2024: The Indonesian government enacted Trade Ministerial Regulation No. 8/2024, easing import restrictions on essential capital goods, including construction machinery.

Indonesia Construction Equipment Market Report Scope

Construction equipment refers to machines designed and used for construction and allied activities. The construction equipment market consists of a wide range of companies involved in the designing, manufacturing, and selling construction equipment, such as excavators, backhoe loaders, and cranes, among others, to its end users.

The Indonesian construction equipment market is segmented by equipment type and drive type. By equipment type, By equipment type, the market is segmented into earthmoving equipment (excavators, backhoe loaders, motor graders, and other earthmoving equipment (bulldozers, etc.)), road construction equipment (road rollers and asphalt pavers), material handling equipment (cranes, forklifts, and telescopic handlers, and other material handling equipment (articulated boom lifts, etc.), and other construction equipment (concrete pump trucks, dumpers, tippers, etc.)). By drive type, the market is segmented into hydraulic and electric/hybrid.

The report offers market size and forecasts for construction equipment in value (USD) and volume (units) for all the above segments.

| Earth-moving Equipment | Excavators |

| Backhoe Loaders | |

| Motor Graders | |

| Bulldozers | |

| Road Construction Equipment | Road Rollers |

| Asphalt Pavers | |

| Material-Handling Equipment | Cranes |

| Forklifts & Telescopic Handlers | |

| Articulated Boom Lifts | |

| Other Construction Equipment |

| Hydraulic |

| Electric / Hybrid |

| Less than 100 kW |

| 101 to 200 kW |

| 201 to 400 kW |

| More than 400 kW |

| Infrastructure & Real-estate Contractors |

| Mining & Quarrying Companies |

| Manufacturing & Industrial Facilities |

| Agriculture & Plantation Sector |

| Residential Construction |

| Commercial Construction |

| Industrial Construction |

| Transportation & Infrastructure Projects |

| Energy & Utilities Projects |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Papua & Maluku |

| Rest of Indonesia |

| By Equipment Type | Earth-moving Equipment | Excavators |

| Backhoe Loaders | ||

| Motor Graders | ||

| Bulldozers | ||

| Road Construction Equipment | Road Rollers | |

| Asphalt Pavers | ||

| Material-Handling Equipment | Cranes | |

| Forklifts & Telescopic Handlers | ||

| Articulated Boom Lifts | ||

| Other Construction Equipment | ||

| By Drive Type | Hydraulic | |

| Electric / Hybrid | ||

| By Power Output (kW) | Less than 100 kW | |

| 101 to 200 kW | ||

| 201 to 400 kW | ||

| More than 400 kW | ||

| By End-user | Infrastructure & Real-estate Contractors | |

| Mining & Quarrying Companies | ||

| Manufacturing & Industrial Facilities | ||

| Agriculture & Plantation Sector | ||

| By Application | Residential Construction | |

| Commercial Construction | ||

| Industrial Construction | ||

| Transportation & Infrastructure Projects | ||

| Energy & Utilities Projects | ||

| By Region | Java | |

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Papua & Maluku | ||

| Rest of Indonesia | ||

Key Questions Answered in the Report

How large is the Indonesian construction equipment market in 2026?

The market was USD 3.62 billion in 2026 and is forecast to reach USD 4.89 billion by 2031, with a 6.18% CAGR trajectory.

Which equipment segment holds the greatest share?

Earth-moving machinery led the Indonesian construction equipment market, with a 48.12% share in 2025, driven by toll roads, dams, and mining projects.

What growth potential exists for electric or hybrid machines?

Electric/hybrid models are expanding at a 6.45% CAGR thanks to carbon-credit incentives, VAT discounts, and lower lifetime operating costs.

Why is Kalimantan viewed as a high-growth region?

The region hosts the USD 35 billion IKN capital project and multiple large-scale mining contracts, which are projected to deliver a 6.28% CAGR through 2031.

What restrains faster market expansion?

Rupiah volatility inflates import costs, and protracted land acquisition processes delay project start-ups, trimming forecast CAGR by 1.4 percentage points.

How competitive is the supplier landscape?

Indonesia’s construction-equipment market pairs global OEM leaders-Komatsu, Caterpillar, Hitachi, Kobelco, Volvo-with vibrant rental fleets and local assembly hubs, ensuring reliable, cost-effective machinery supply for major mining, road-building, and port projects.

Page last updated on: