Indonesia IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

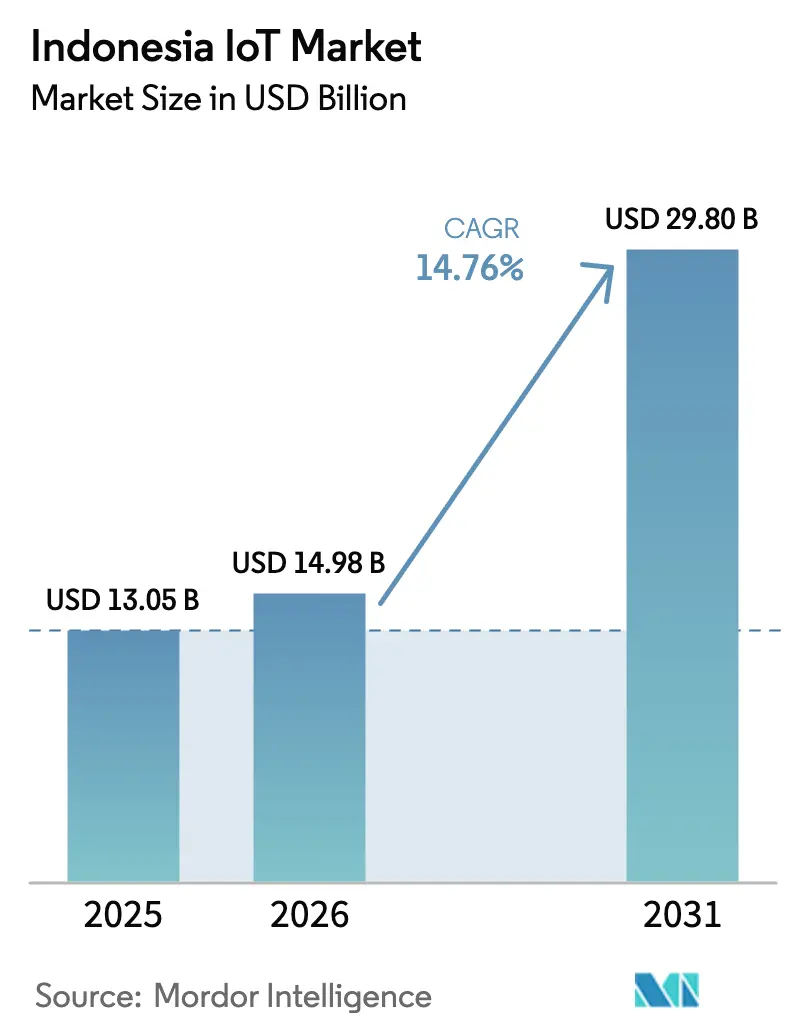

| Base Year Market Size (2025) | USD 13.05 Billion |

| Market Size (2026) | USD 14.98 Billion |

| Market Size (2031) | USD 29.8 Billion |

| Growth Rate (2026 - 2031) | 14.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia IoT Market Analysis by Mordor Intelligence

Indonesia IoT market size in 2026 is estimated at USD 14.98 billion, growing from 2025 value of USD 13.05 billion with 2031 projections showing USD 29.8 billion, growing at 14.76% CAGR over 2026-2031. The expansion stems from national smart-city programs, soaring 5G and LPWAN coverage, and a bold shift toward data sovereignty regulations that draw foreign technology investment. Government procurement frameworks lower adoption barriers, while tax incentives under “Making Indonesia 4.0” accelerate industrial upgrades. The tightening of domestic-content (TKDN) rules spurs local assembly lines, and widespread ESG reporting mandates unlock fresh enterprise demand for real-time monitoring. Telecommunications carriers are densifying edge nodes, which in turn lowers latency and encourages AI-enabled use cases ranging from flood control to precision farming.

Key Report Takeaways

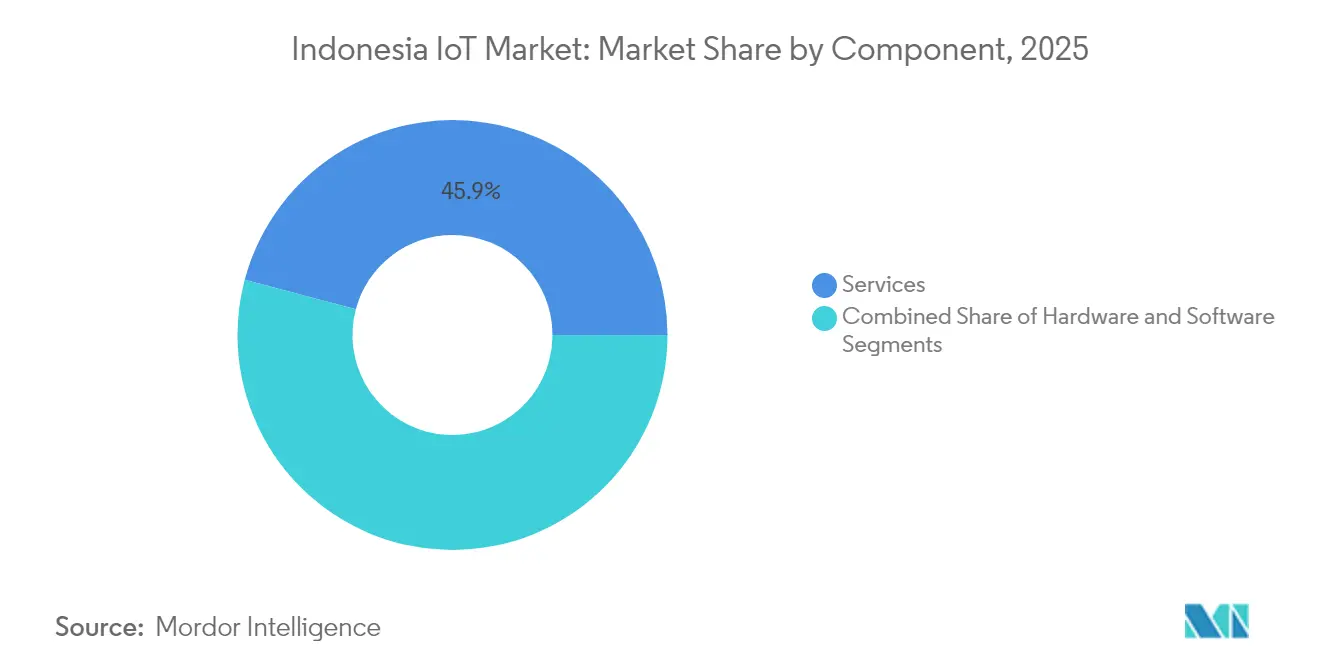

- By component, services held 45.86% of Indonesia IoT market share in 2025, while software is projected to advance at an 17.28% CAGR through 2031.

- By connectivity technology, cellular maintained a 59.35% share of the Indonesia IoT market size in 2025; LPWAN is forecast to expand at a 16.68% CAGR to 2031.

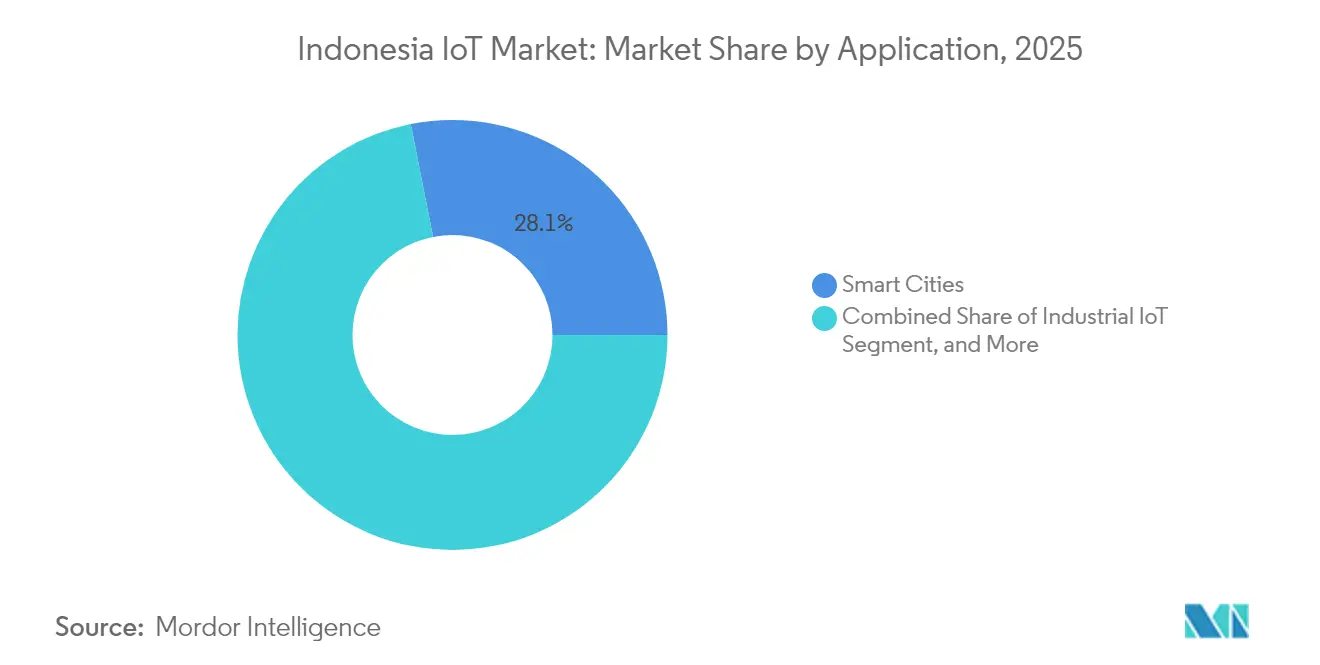

- By application, smart cities captured 28.11% of Indonesia IoT market share in 2025; industrial IoT is moving ahead at an 17.62% CAGR through 2031.

- By end-user industry, manufacturing accounted for 30.12% of the Indonesia IoT market in 2025, while the energy and utilities sector is projected to grow at a 18.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed “100 Smart Cities” roll-out | +1.80% | Nationwide, with priority cities incl. Jakarta, Surabaya, Makassar, Bandung | Medium term (2–4 years) |

| Telco-led 5G / LPWAN network densification | +2.10% | National (urban first: Jakarta, Surabaya, Medan, Bandung) | Short to medium term (1–3 years) |

| Manufacturing push under “Making Indonesia 4.0” | +2.00% | Java, Sumatra, and Batam industrial zones | Medium term (2–4 years) |

| Subsidised satellite back-haul for remote IoT | +1.20% | Remote and maritime regions (Kalimantan, Sulawesi, Papua) | Long term (≥ 4 years) |

| AI-enabled flood-control and urban-resilience use cases in Jakarta | +0.90% | Jakarta and Jabodetabek metro region | Short term (≤ 2 years) |

| Enterprise demand for real-time ESG reporting | +1.10% | Nationwide adoption among large enterprises, SOEs, and extractive industries | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government-backed 100 Smart Cities roll-out

Standardized procurement and centrally funded projects have allowed 76 municipalities to adopt interoperable sensor networks, traffic analytics, and waste-collection optimization. Jakarta’s JAKI platform already integrates 8,700 sensors across 267 sub-districts, enabling real-time flood warnings and dynamic traffic rerouting.[1]Andi Anugrah, “Jakarta Smart City Integrates IoT for Urban Management,” Jakarta Post, jakartapost.com These shared standards spill over into private real-estate developments, where builders embed the same APIs to meet green-building mandates and attract ESG-conscious tenants. Vendor pipelines benefit from bulk hardware orders and uniform software stacks, reducing per-unit costs and speeding deployments. As provincial governments copy Jakarta’s template, demand for cloud-agnostic orchestration tools is surging across second-tier cities such as Surabaya and Bandung.

Telco-led 5G and LPWAN densification

Telkomsel’s 5G grid now spans 150 cities, and XL Axiata’s LoRa-based LPWAN covers 80% of the population, slashing connectivity costs for large-scale sensor roll-outs.[2]“LPWAN Network Expansion Report,” XL Axiata, xl.co.id Carriers differentiate through network slicing and edge caching, which lower latency for mission-critical industrial applications. Indosat Ooredoo Hutchison’s Connectivity+ service offers guaranteed sub-20 ms latencies for predictive maintenance in automotive assembly lines.[3]“IoT Connectivity+ Launch,” Indosat Ooredoo Hutchison, indosatooredoo.com The infrastructure race has moved from basic coverage to deep indoor penetration, enabling smart-building retrofits in dense urban centers. Meanwhile, hybrid cellular-LPWAN modules allow enterprises to toggle bandwidth and battery life trade-offs dynamically.

Manufacturing push under Making Indonesia 4.0

Tax credits cover up to 60% of automation spending, nudging factories toward condition-based maintenance, digital twins, and real-time quality inspection. Toyota’s Karawang plant uses 1,200 edge-connected torque sensors that cut downtime by 18%, while local firm PT Advotics’ inventory platform helps beverage lines reduce spoilage by 30%.[4]“Making Indonesia 4.0 Progress Report,” Ministry of Industry, kemenperin.go.id The roadmap’s focus on automotive, electronics, chemicals, food, and textiles concentrates integrator talent inside Java’s industrial belt. Foreign OEMs comply with TKDN quotas by co-developing solutions with domestic vendors, thereby transferring know-how in robotics and machine vision.

Subsidised satellite back-haul for remote IoT

Outer-island plantations, fisheries, and mining sites gain access to subsidized VSAT terminals that back-haul sensor data to cloud dashboards. PT Telin and Citra Connect plan 200 additional ground stations by 2026 to support methane monitoring at coal mines and asset tracking on offshore rigs. The program trims bandwidth costs by up to 40% and unlocks new use cases such as coral-reef health monitoring and island-grid energy balancing. As satellite latency drops under 100 ms with new LEO constellations, developers can extend advanced analytics to remote areas that lack fiber or 4G.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented device-level security standards | –1.60% | Nationwide, with higher exposure in multi-vendor industrial deployments | Medium term (2–4 years) |

| Rural last-mile fibre deficit outside Java | –1.90% | Eastern Indonesia, Sulawesi, Kalimantan, Papua | Long term (≥ 4 years) |

| High import duties on industrial sensors | –1.40% | Nationwide; strongest impact on manufacturing, utilities, mining | Short to medium term (1–3 years) |

| Shortage of mid-level IoT solution architects | –1.20% | Nationwide; acute in Jakarta, Bandung, Surabaya | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fragmented device-level security standards

Enterprises juggle guidelines from BSSN, BSN, and sector regulators, often integrating three encryption stacks on the same gateway. Project budgets swell 25-30% as integrators retrofit hardware for each compliance audit. Certification delays stretch rollouts by up to 12 months for utilities and transport operators, prompting conservative device selections that slow innovation. While BSSN’s draft framework inches toward harmonization, vendors lobby for a single root-of-trust to reduce overhead. In the interim, managed-security-as-a-service emerges to monitor diverse firmware baselines, but cost-sensitive SMEs postpone deployments until clearer rules arrive.

Shortage of mid-level IoT solution architects

Only 19% of the digital workforce meets integration proficiency, particularly in edge orchestration and sensor fusion. Companies import talent at 2-3 times local salary levels, inflating project costs by 40%. Java attracts most certified professionals, leaving Sumatra and Kalimantan reliant on remote support. Government scholarship schemes produce entry-level coders but not the 3–7-year specialists needed to lead deployments. Skills bottlenecks incentivize low-code platforms, yet complex industrial retrofits still demand seasoned architects, limiting multi-site scale-ups for national conglomerates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services lead integration complexity

Services captured 45.86% of Indonesia IoT market share in 2025, illustrating enterprises’ preference for turnkey offerings that bundle hardware sourcing, software customization, and lifecycle management. Software, however, is scaling fastest at an 17.28% CAGR as local developers craft vertical apps for flood management and cold-chain logistics. Hardware demand remains steady yet import tariffs and TKDN quotas push vendors to establish local assembly lines, compressing margins but satisfying compliance.

Services dominance reflects constrained in-house expertise. Firms gravitate toward carrier-supplied platforms such as Telkomsel’s IoT Marketplace, which integrates connectivity, device management, and analytics in one SLA. As mid-market adopters enter the fray, managed services reduce vendor coordination overhead and ensure security updates across heterogeneous fleets. The trend nudges pure hardware vendors to pivot into support contracts or risk commoditization.

By Connectivity Technology: Cellular dominance faces LPWAN challenge

Cellular technologies account for 59.35% of Indonesia IoT market size in 2025 because nationwide towers already cover 98% of populated areas. LPWAN, however, is growing at a 16.68% CAGR, capturing water-meter, plantation, and livestock-tracking use cases where decade-long battery life outweighs bandwidth needs. Hybrid chipsets that auto-switch between NB-IoT and LoRa cut module SKUs and simplify inventory.

XL Axiata's LPWAN footprint spans 80% of the population, enabling sensor node costs under USD 4 and annual connectivity fees near USD 1. Satellite IoT remains niche but is indispensable for maritime and remote mining telemetry. Short-range (Wi-Fi, BLE, Zigbee) retains a foothold in smart buildings, where dense device counts and private gateways justify local-area networks. The connectivity mix is becoming stratified by geography and power budget.

By Application: Smart-city foundation enables industrial growth

Smart-city deployments held 28.11% of Indonesia IoT market share in 2025, underpinned by centralized funding for public safety, traffic, and waste management. Industrial IoT outpaces all others with an 17.62% CAGR as manufacturers automate quality inspection and predictive maintenance. Consumer IoT trails, constrained by discreet household budgets, yet gains traction from power-subsidy rebate programs for smart thermostats.

Jakarta’s flood-warning grid doubles as a data lake that private factories tap for logistics planning, exemplifying infrastructure spillover. Automotive and logistics applications benefit from e-toll and fleet-tracking regulations mandating GPS+OBD devices on commercial vehicles. Healthcare IoT, boosted by telemedicine expansion into outer islands, is in pilot phase but shows strong policy backing.

By End-User Industry: Manufacturing leads digital transformation

Manufacturing commanded 30.12% of Indonesia's IoT market size in 2025, driven by incentives for robotics, MES, and digital twins. Energy and utilities are advancing at a 18.11% CAGR, buoyed by PLN's USD 200 million smart-meter program that targets 1.5 million units by 2025. Transportation and logistics adopt IoT for cold-chain compliance, while agriculture precision spraying and soil-moisture analytics on palm-oil estates.

OEMs partner with universities in Bandung and Surabaya to co-design edge-AI modules that pass TKDN thresholds. Utilities leverage NB-IoT for pole-top transformer monitoring, cutting outage durations by 22%. Retailers upgrade HVAC and lighting controls to meet green-building codes, yet penetration remains confined to Grade-A malls in Jakarta.

Geography Analysis

Java accounts for roughly 70% of active IoT nodes despite housing 57% of the population, reflecting its fiber backbones, carrier POP density, and concentration of factories and headquarters. Jakarta anchors smart-city and financial-services deployments, while Bandung hosts R&D centers that tailor solutions for tropical and archipelagic conditions. Surabaya’s port and industrial estates drive asset tracking and predictive maintenance rollouts.

Sumatra’s palm plantations and mining pits drive adoption of LPWAN-based remote monitoring, but patchy terrestrial coverage limits high-bandwidth applications. The Palapa Ring fiber backbone now links Kalimantan and Sulawesi, enabling environmental compliance monitoring of forestry concessions. Eastern islands rely on subsidized satellite links for fisheries and micro-grid telemetry.

Regulatory nuances vary as Jakarta insists on in-country data residency, whereas provincial governments focus on connectivity subsidies. Special economic zones, such as Batam, grant customs waivers on sensors that meet the TKDN assembly rules. These regional quirks require channel partners with hyper-local compliance expertise, prompting tier-1 integrators to franchise smaller VARs across 34 provinces.

Competitive Landscape

Indonesia’s IoT arena is moderately fragmented as the top three telcos control most connectivity pipes, yet hundreds of niche ISVs compete at the application layer. Telkom Indonesia bundles cloud, edge, and device management to lock in enterprise accounts, whereas Indosat Ooredoo teams with Cisco for secure connectivity slices in manufacturing. XL Axiata’s merger with Smartfren produced the second-largest IoT SIM base, yielding scale benefits in LPWAN infrastructure.

Global clouds such as Microsoft and AWS build Jakarta and Surabaya regions to meet data-sovereignty rules and court multinational clients. Hardware suppliers, including Huawei and Schneider Electric, open local R&D or assembly sites to cross the 40% TKDN hurdle. Startups like DycodeX and Banoo carve agritech niches with AI-driven aquaculture monitoring, while PT Advotics expands from FMCG inventory analytics to predictive shelf-replenishment in hypermarkets.

M&A momentum shows telcos acquiring edge-analedge analytics firms to shorten go-to-market cycles in verticals. Patent filings in IoT security surged 28% in 2024, signalling intensifying IP battles. Vendor lock-in risk drives some enterprises toward open-source stacks, but support gaps push most toward carrier-managed SaaS platforms with bundled SLAs.

Indonesia IoT Industry Leaders

Accenture

Microsoft

Hewlett Packard Enterprise Development LP

Fujitsu

Toshiba IT-Services Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Telkomsel and Sumitomo Corporation signed a USD 150 million agreement to co-develop 5G-enabled predictive maintenance solutions for automotive and electronics plants.

- December 2025: XL Axiata completed its merger with Smartfren, creating the second-largest telco and amassing 2.5 million IoT connections with LPWAN coverage topping 85% of residents.

- November 2025: PLN launched a USD 200 million advanced-metering program targeting 1.5 million smart meters across Java and Sumatra by the end of 2025.

- October 2025: Huawei Indonesia opened a USD 50 million R&D center in Bandung, focused on smart-city and agri-IoT solutions designed for humid tropical climates.

Indonesia IoT Market Report Scope

The Internet of Things (IoT) is a network of connected devices and related technologies that facilitates communication between various devices and the cloud and between devices. IoT services represent end-to-end services that enable organizations to collaborate with external providers to design, build, and operate IoT solutions and consulting for IoT planning.

The Indonesia IoT market is segmented by type (hardware, software, and services), by application (automotive IoT, consumer IoT, healthcare IoT, industrial IoT, smart cities, and other applications), by region (Java, Sumatra, Kalimantan, and other regions).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Cellular IoT (2G/4G/5G) |

| LPWAN (NB-IoT, LoRa, Sigfox) |

| Short-Range (Wi-Fi/Bluetooth/Zigbee) |

| Satellite-based IoT |

| Smart Cities |

| Industrial IoT |

| Consumer IoT |

| Automotive IoT |

| Healthcare IoT |

| Others Applications |

| Manufacturing |

| Transportation and Logistics |

| Energy and Utilities |

| Agriculture |

| Retail and Smart Buildings |

| By Component | Hardware |

| Software | |

| Services | |

| By Connectivity Technology | Cellular IoT (2G/4G/5G) |

| LPWAN (NB-IoT, LoRa, Sigfox) | |

| Short-Range (Wi-Fi/Bluetooth/Zigbee) | |

| Satellite-based IoT | |

| By Application | Smart Cities |

| Industrial IoT | |

| Consumer IoT | |

| Automotive IoT | |

| Healthcare IoT | |

| Others Applications | |

| By End-User Industry | Manufacturing |

| Transportation and Logistics | |

| Energy and Utilities | |

| Agriculture | |

| Retail and Smart Buildings |

Key Questions Answered in the Report

How big is the Indonesia IoT Market?

The Indonesia IoT Market size is expected to reach USD 14.98 billion in 2026 and grow at a CAGR of 14.76% to reach USD 29.8 billion by 2031.

What is the current Indonesia IoT Market size?

In 2026, the Indonesia IoT Market size is expected to reach USD 14.98 billion.

Who are the key players in Indonesia IoT Market?

Accenture, Microsoft, Hewlett Packard Enterprise Development LP, Fujitsu and Toshiba IT-Services Corporation are the major companies operating in the Indonesia IoT Market.

What years does this Indonesia IoT Market cover, and what was the market size in 2025?

In 2025, the Indonesia IoT Market size was estimated at USD 13.05 billion. The report covers the Indonesia IoT Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Indonesia IoT Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: